Equipment Insurance for Contractors: Safeguard Your Gear

Your equipment is your livelihood. When a drill breaks down mid-job or a vehicle gets stolen, the financial hit can derail your entire operation.

Equipment insurance for contractors protects your tools, machinery, and vehicles from theft, damage, and unexpected breakdowns. At Heaton Bennett Insurance, we help contractors like you build policies that cover what matters most to your business.

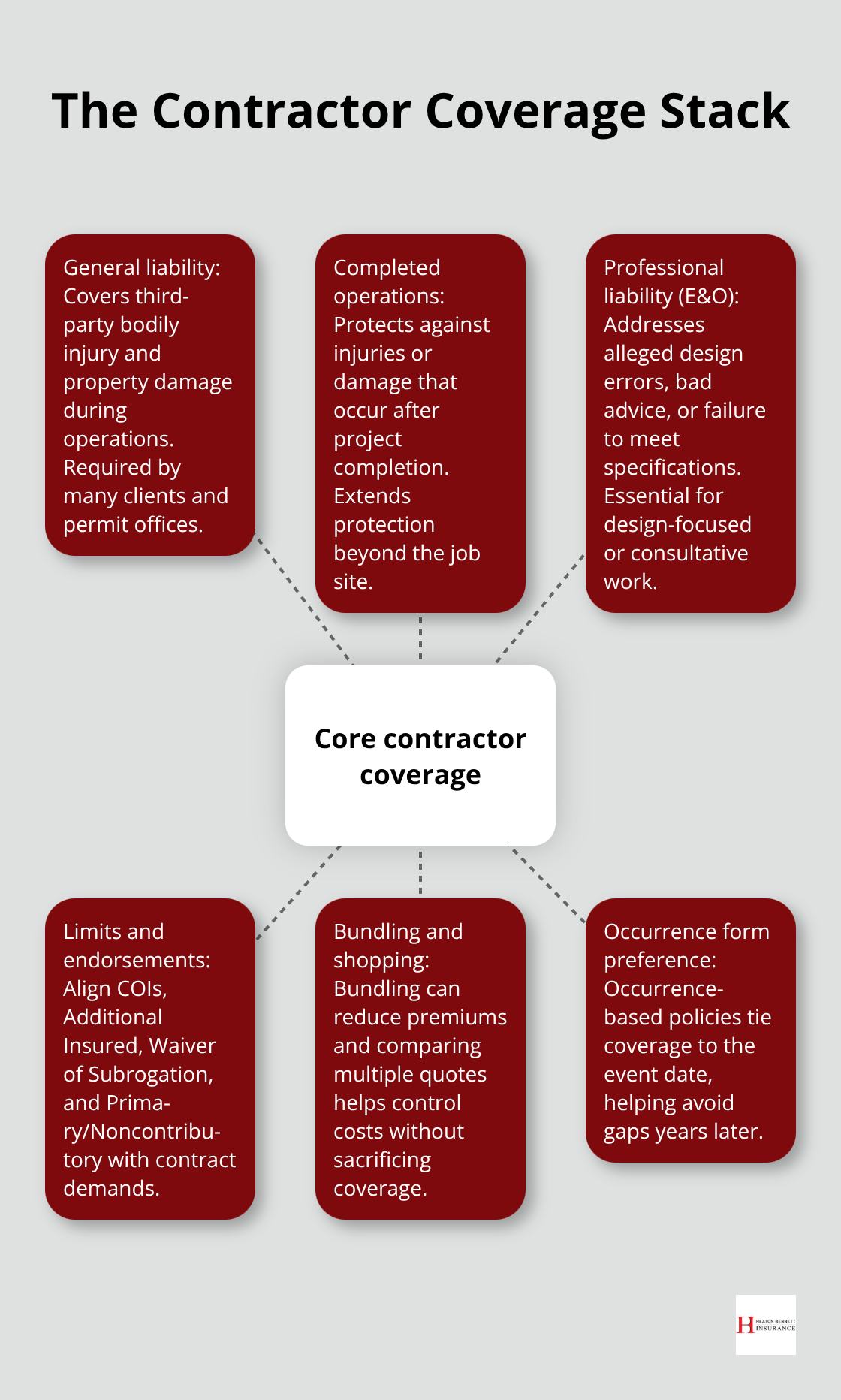

What Your Contractor Equipment Insurance Actually Covers

Contractor equipment insurance protects the specific assets that keep your jobs moving forward. The coverage isn’t one-size-fits-all, and understanding what’s included matters because gaps in protection can cost you thousands.

Heavy Machinery Takes Priority

Heavy machinery like excavators, compressors, and generators attracts thieves-construction equipment theft costs between 300 million and 1 billion dollars annually. These machines often sit on jobsites overnight or travel between locations, making them vulnerable targets. Your policy should cover owned equipment, rented or leased gear you’re responsible for, and borrowed equipment under written agreements. The right coverage protects your investment whether the machinery stays stationary or moves constantly across multiple projects.

Hand Tools and Power Equipment Add Up Fast

Hand tools and power equipment form the backbone of daily operations, yet many contractors underestimate their replacement costs. A single lost cordless drill set, circular saws, nail guns, and impact drivers can easily run 2,000 to 4,000 dollars. Ladders, lighting equipment, protective clothing, and safety gear also qualify for coverage. Smart contractors schedule high-value items individually on their policies-if you own tools worth more than 2,500 dollars, they typically need separate coverage limits to guarantee full replacement rather than depreciated value.

Technology and Weather Threats

Laptops used for jobsite estimates, tablets for blueprints, GPS equipment, and diagnostic tools represent significant investments that travel with you daily. Weather events create another coverage gap (a record number of billion-dollar weather and climate events occurred between 1980 and 2022 according to NOAA data). Hail, lightning, and flooding can destroy expensive equipment in minutes. Your policy should explicitly cover these perils and distinguish between replacement cost coverage, which pays for brand-new equipment, and actual cash value coverage, which accounts for depreciation. For equipment under five years old, replacement cost coverage makes financial sense because depreciation hasn’t significantly reduced value.

Understanding what your policy covers sets the foundation, but selecting the right limits and deductibles requires a closer look at your specific operation and equipment inventory.

Why Equipment Theft and Damage Cost More Than You Think

Theft Hits Your Bottom Line Hard

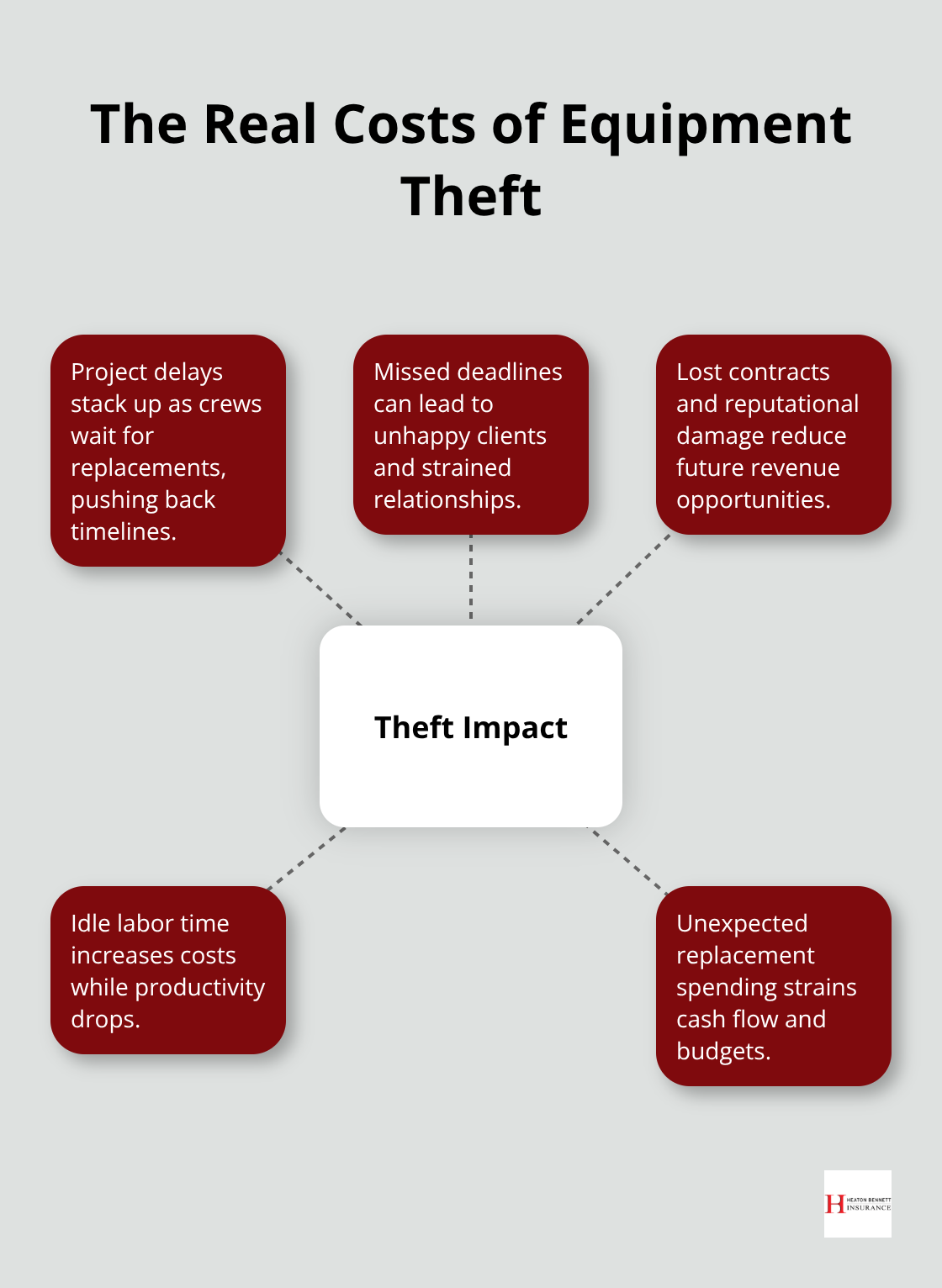

Theft represents the most immediate threat to your equipment investment. Construction equipment theft ranges from 300 million to 1 billion dollars annually, and thieves specifically target contractor sites because they know the gear has resale value. A single theft doesn’t just mean replacing one tool-it means project delays, missed deadlines, unhappy clients, and potentially lost contracts. When a generator disappears from your jobsite or someone steals your truck full of power tools, you lose the equipment cost plus the labor hours spent searching for replacements and the income lost while your crew sits idle waiting for gear to arrive.

Accidental Damage Creates Different Exposure

Accidental damage creates a separate but equally serious problem. Tools drop from heights, equipment gets damaged during transport between sites, and weather events destroy machinery in minutes. According to NOAA data, a record number of billion-dollar weather and climate events occurred between 1980 and 2022, and contractors operating in storm-prone regions face real exposure to hail and flooding losses. Without coverage, a single weather event or accident wipes out thousands in equipment value. The financial impact extends beyond replacement costs-it includes project delays that damage your reputation and reduce cash flow when you need it most.

Replacement Speed Determines Your Recovery

Without equipment insurance, contractors face a choice between absorbing losses themselves or going without critical tools. When your core equipment gets stolen or damaged, the replacement timeline matters enormously. High-value items like compressors or generators can take weeks to replace, especially if you need to order new units rather than rent temporary replacements. Insurance with replacement cost coverage for equipment under five years old means you receive payment for brand-new gear rather than depreciated value, allowing you to get back to work faster. Actual cash value coverage costs less but reimburses you at reduced amounts based on equipment age, which often leaves contractors short when they need to buy replacements.

Financial Security Protects Your Operations

The financial security that equipment insurance provides isn’t theoretical; it’s the difference between absorbing a 5,000-dollar loss yourself or having your policy cover it while you keep operations running. Assessing whether your equipment portfolio includes items purchased within the last five years matters-if so, replacement cost coverage becomes essential rather than optional. The right policy structure protects your investment and keeps your crew productive when unexpected losses occur.

Selecting the right coverage limits and deductibles requires understanding your specific equipment inventory and operational risks.

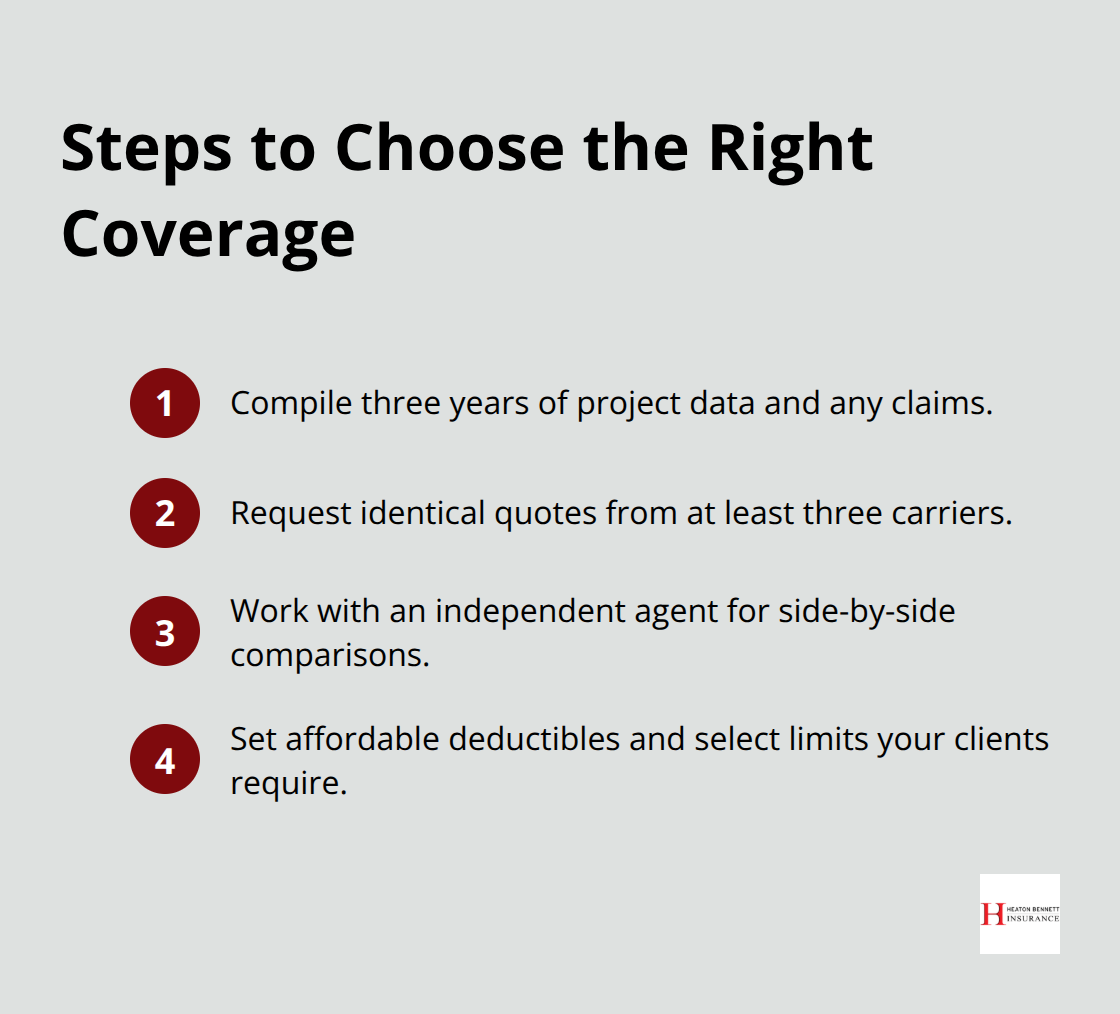

How to Choose the Right Equipment Insurance Policy

Build Your Equipment Inventory and Assign Values

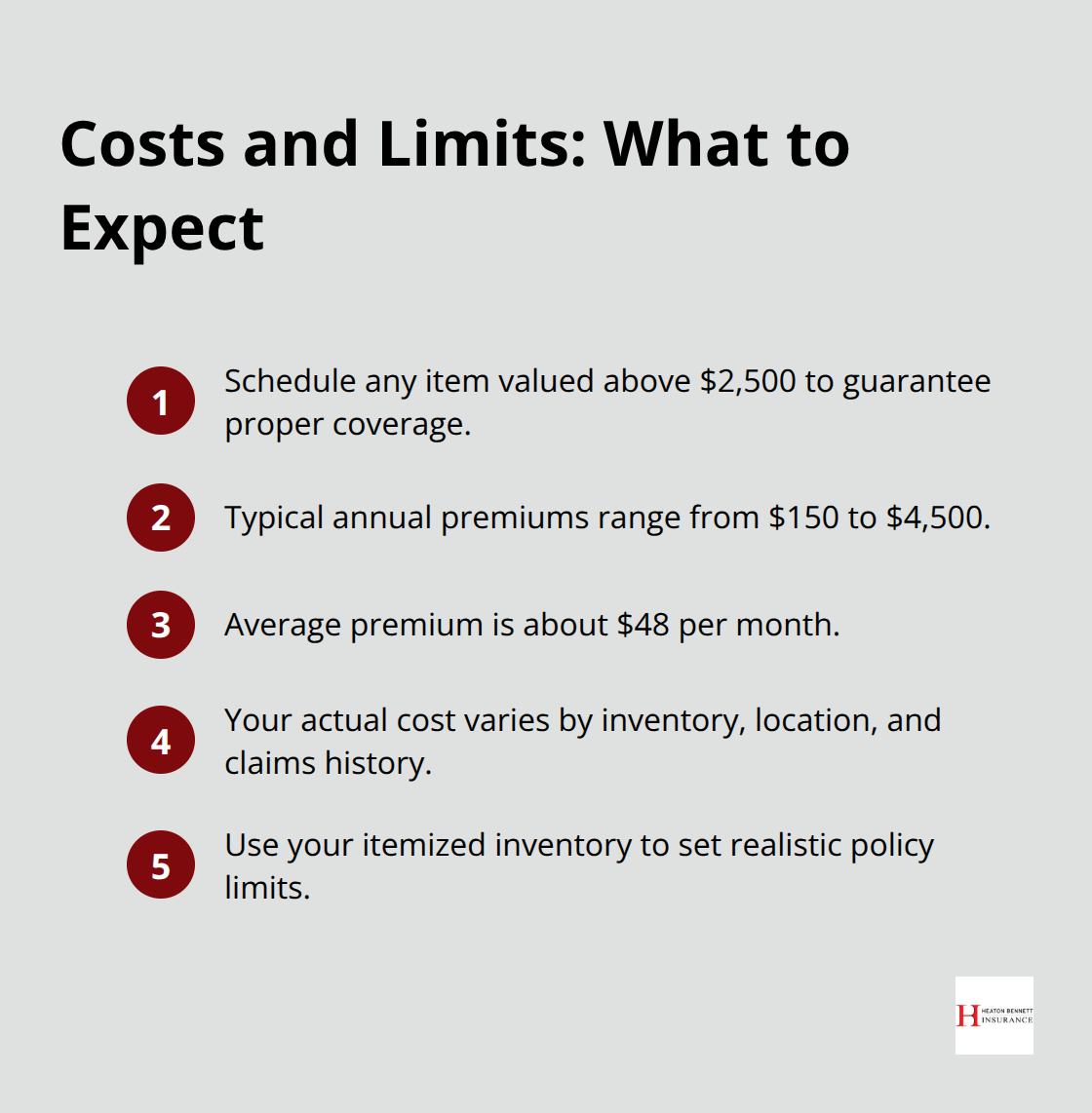

Start by listing every piece of equipment your operation depends on, then assign realistic replacement costs to each item. This inventory becomes your foundation for selecting coverage limits. Equipment valued above 2,500 dollars should be scheduled individually on your policy to guarantee replacement cost coverage rather than depreciated value, according to industry standards. Small businesses typically pay between 150 and 4,500 dollars annually for tools and equipment insurance, with premiums averaging around 48 dollars per month, according to Insureon data from roughly 100,000 small business customers. Your actual cost depends entirely on what you own, where you operate, and your claims history.

Understand How Location and Coverage Type Affect Your Premium

A contractor in a high-theft urban area pays significantly more than one in a rural region with lower crime rates. Location factors including local crime rates, natural disaster risk, population density, and proximity to emergency services substantially affect your premium. If your equipment includes items purchased within the last five years, replacement cost coverage costs more upfront but saves you thousands when you file a claim because you receive payment for brand-new gear rather than depreciated amounts. Actual cash value coverage costs less monthly but reimburses you at reduced amounts based on equipment age, often leaving contractors unable to afford quality replacements without additional out-of-pocket spending.

Select Deductibles That Balance Cost and Risk

Deductibles directly impact your monthly cost and your financial exposure after a loss occurs. Higher deductibles like 2,500 dollars reduce premiums significantly compared to 500-dollar deductibles, but they mean you absorb more of each claim yourself. Many contractors choose deductibles between 500 and 1,000 dollars as a balance between affordability and manageable out-of-pocket risk. Policy limits require attention to both per-item sublimits and your overall policy maximum. An example structure might include a 10,000-dollar total limit with 500-dollar per-item sublimits and 2,500-dollar per-occurrence limits, which works for contractors with smaller tool inventories but fails catastrophically if a single theft involves multiple high-value items.

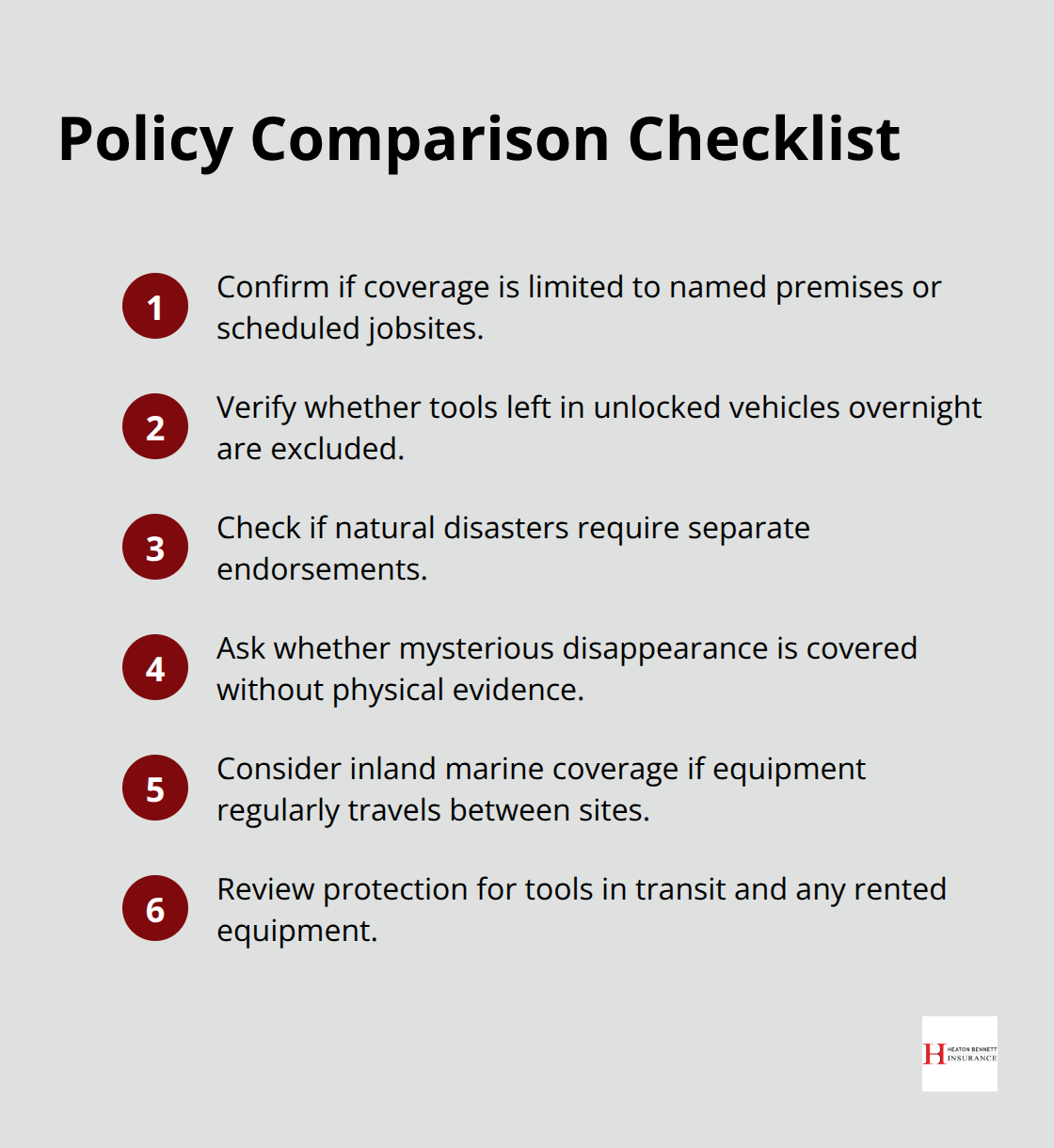

Review Exclusions and Compare Coverage Types

Review what your policy explicitly excludes because standard exclusions typically include normal wear and tear, rust and corrosion, internal mechanical breakdown, mysterious disappearance without evidence of theft, earthquakes, and floods unless you purchase separate endorsements. Open perils coverage costs more than named perils because it protects against all losses except those specifically excluded, whereas named perils coverage only protects against losses you specifically select like theft, vandalism, fire, and hail.

Maximize Savings Through Bundling and Payment Options

Bundling tools and equipment coverage with a business owner’s policy or commercial package policy typically yields lower premiums than purchasing coverage separately, and paying your full annual premium upfront rather than monthly installments often provides an additional discount of 10 to 15 percent.

Final Thoughts

Equipment insurance for contractors protects your business when theft, damage, or accidents strike without warning. A single loss-whether a stolen generator or weather damage to your power tools-forces you to absorb thousands in costs or scramble for replacements while your crew sits idle. The contractors who invest in comprehensive coverage avoid these scenarios entirely and return to work without derailing schedules or damaging client relationships.

Your equipment represents significant invested capital that demands protection matching its value. Build your inventory with realistic replacement costs, identify items exceeding the $2,500 threshold that need individual scheduling, and decide whether replacement cost or actual cash value coverage fits your operation. Consider your location’s theft and weather risks, select deductibles that balance affordability with manageable out-of-pocket exposure, and review policy exclusions carefully to avoid surprises when you file a claim.

At Heaton Bennett Insurance, we work with contractors to build tailored equipment insurance for contractors policies that match your specific risks and equipment portfolio. Contact us today to discuss your equipment protection needs and receive a customized quote based on your actual operation. Your business deserves protection that works as hard as you do.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.