Nonprofit Insurance Options: Finding Flexible Coverage

Nonprofits operate under unique constraints that standard business insurance simply doesn’t address. Your organization faces distinct risks-from volunteer liability to specialized property needs-that require tailored protection.

We at Heaton Bennett Insurance understand that nonprofit insurance options must balance comprehensive coverage with tight budgets. This guide walks you through the coverage types your organization actually needs and how to find flexible solutions that fit your mission.

What Risks Does Your Nonprofit Actually Face?

The Coverage Gaps in Standard Business Insurance

About 1.8 million nonprofit organizations operate across the United States, yet most operate with insurance gaps that expose them to catastrophic financial loss. Standard business policies exclude the specific exposures nonprofits encounter daily. General liability policies typically don’t cover volunteers as insureds, leaving your organization vulnerable when a volunteer causes injury or property damage. Directors and officers face personal liability for governance decisions, employment disputes, and fiduciary failures that commercial policies don’t address.

Specialized Exposures Require Tailored Protection

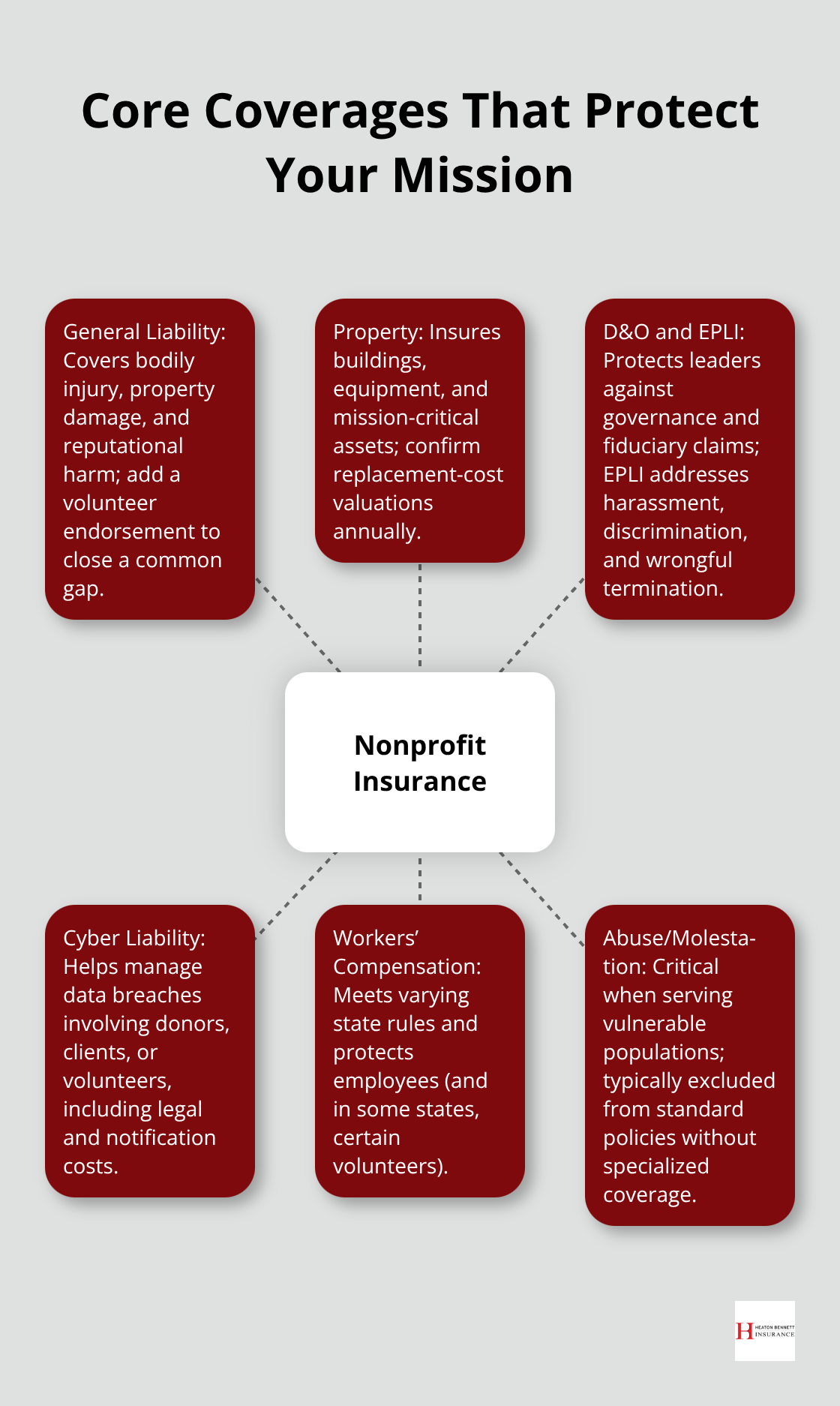

If your nonprofit serves vulnerable populations-children, elderly individuals, or people with disabilities-you need sexual abuse and physical abuse coverage that ordinary business insurance simply won’t provide. Property coverage must account for donated equipment and materials, client property in your care, and the unique value of mission-critical assets that standard valuations miss. Workers’ compensation requirements vary dramatically by state; some states exempt certain nonprofits while others mandate coverage for all employees and sometimes volunteers.

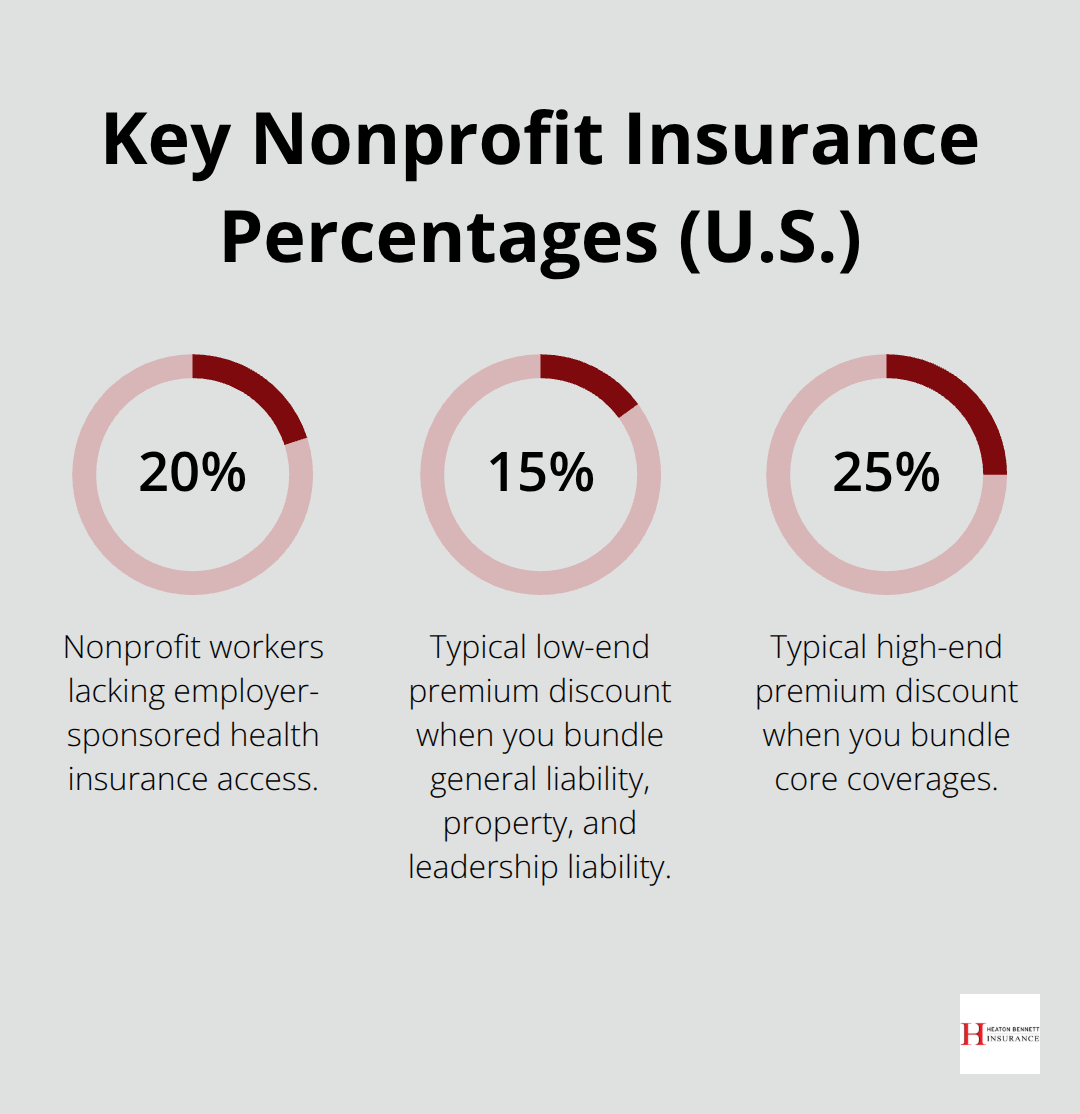

According to the Urban Institute, roughly 20 percent of nonprofit workers lack employer-sponsored health insurance access, creating gaps in your employee benefits strategy that ripple through retention and morale.

The True Cost of Underinsurance

The financial pressure to cut corners on insurance is real, but it’s also the fastest way to destroy a nonprofit’s mission. A single liability claim can exceed $500,000 when legal defense costs and settlements combine. Cyber liability becomes critical once you store donor information, client health records, or volunteer screening data-breaches involving nonprofit donor databases cost organizations between $100,000 and $1 million in notification, legal, and regulatory penalties.

Market Dynamics Shape Your Renewal Strategy

The 2023 reinsurance market stress highlighted that larger nonprofits with budgets over $50 million faced non-renewals or sharp rate increases as carriers tightened capacity, while smaller agencies with favorable loss histories actually found better pricing as more carriers competed for stable business. This means your renewal strategy matters enormously. Start carrier conversations four months before renewal and document your safety training, loss control investments, and claims management approach-these factors influence underwriting decisions significantly.

Why Specialized Providers Understand Your Mission

Specialized nonprofit insurance providers understand these nuances in ways general carriers don’t, pricing based on your actual operations rather than market volatility and offering flexible limits and deductibles that align with constrained budgets. These providers recognize that your organization’s risks shift as your programs expand, your volunteer base grows, or your service population changes. Understanding your specific exposures positions you to select the right coverage types and limits that protect your mission without overpaying for unnecessary protection.

The Core Coverage Your Nonprofit Needs

General Liability: Your Foundation

General liability forms the foundation of nonprofit protection, covering bodily injury, property damage, and reputational harm when someone is injured at your facility or by your operations. The critical distinction for nonprofits is that standard general liability policies typically exclude volunteers as insureds, leaving a dangerous gap. If a volunteer causes injury or property damage, your organization bears the liability exposure. An enhancement endorsement explicitly includes volunteers as covered parties and extends protection to property in your care-donated equipment, client belongings, or materials temporarily under your stewardship. This addition costs nothing extra but closes a major exposure that catches many nonprofits off guard.

Property Coverage: Valuation Matters

Property coverage protects buildings, equipment, and mission-critical assets, but the valuation matters enormously. Many nonprofits undervalue donated inventory or specialized equipment, then face inadequate payouts after a loss. Conduct a detailed asset inventory annually and work with your insurance provider to ensure valuations reflect replacement costs, not book value. This step alone prevents thousands of dollars in uncompensated losses when fire, vandalism, or weather strikes.

Leadership Liability: Protecting Your Board and Staff

Directors and officers liability protects your board members and staff from personal financial exposure when governance decisions, employment actions, or fiduciary responsibilities trigger claims. A wrongful termination suit, discrimination allegation, or breach of fiduciary duty can cost $50,000 to $250,000 in legal defense alone. Employment practices liability insurance covers harassment, discrimination, and wrongful termination claims-exposures that grow as your nonprofit expands its workforce and volunteer base. Gallagher research shows that D&O markets are becoming more competitive with flat to single-digit premium increases as more carriers enter the nonprofit space, making now an ideal time to review your coverage.

Bundling for Maximum Savings

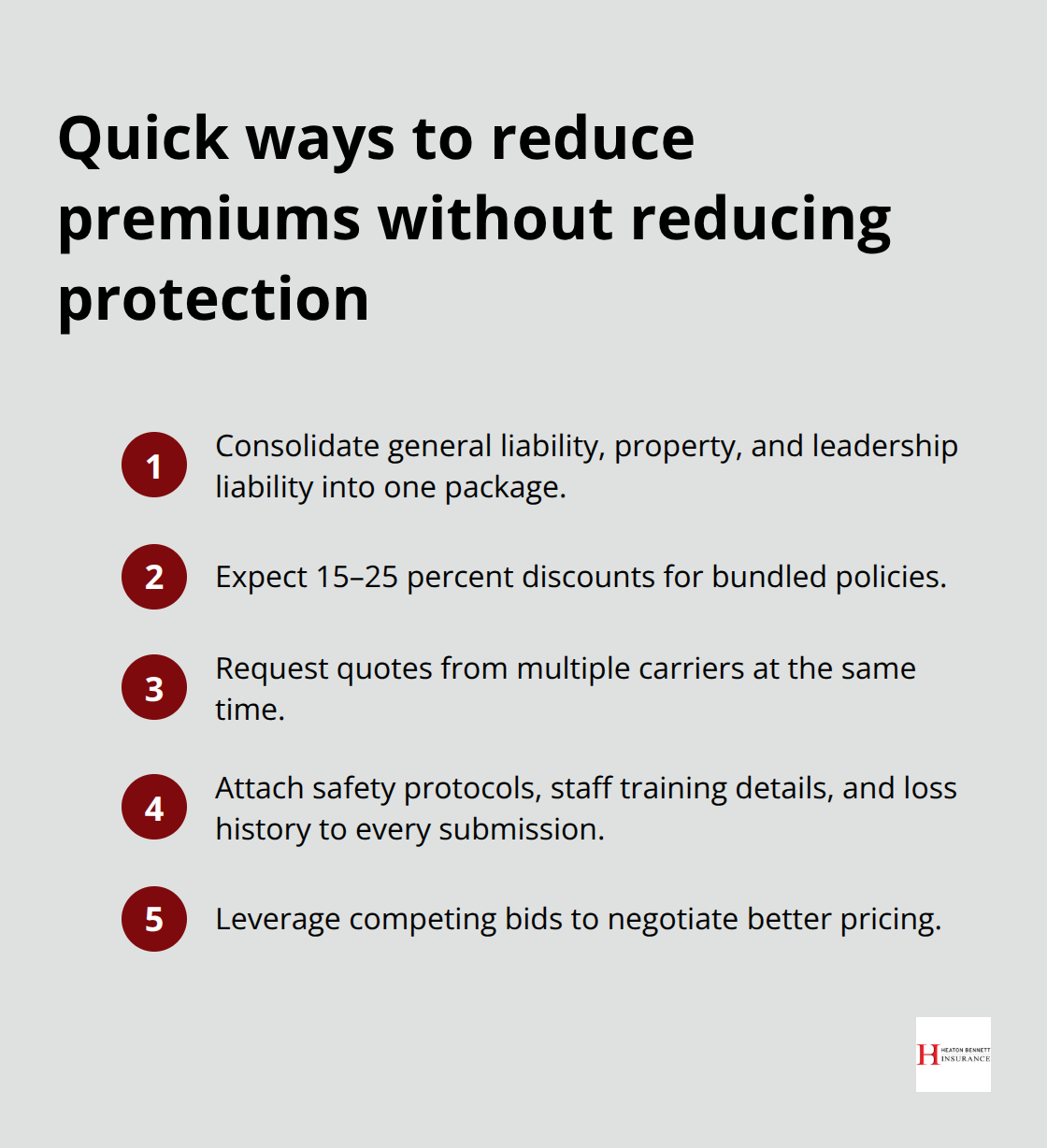

Bundle general liability, property, and leadership liability together rather than purchasing separately; carriers offer substantial discounts when these coverages travel as a package. Small nonprofits often secure these bundled quotes within two to three days when applications are complete, while larger organizations typically wait about two weeks. Document your safety protocols, staff training investments, and loss history when requesting quotes-these factors directly influence pricing and underwriting appetite. The right combination of coverages protects your mission while controlling costs, but your specific needs depend on the populations you serve and the programs you operate.

How to Cut Nonprofit Insurance Costs Without Cutting Coverage

Bundle Coverages for Immediate Savings

Combining your general liability, property, and leadership liability policies into a single package reduces premiums substantially-carriers typically offer 15–25 percent discounts when you consolidate coverages rather than purchase separately. Small nonprofits with complete applications receive quotes within two to three days, while larger organizations should expect about two weeks for underwriting review. The speed matters because you can compare multiple carriers simultaneously and negotiate based on competitive bids.

When requesting quotes, attach documentation of your safety protocols, staff training investments, and loss history. These factors directly influence pricing and show underwriters that your organization manages risk actively.

Document Your Risk Management Efforts

Carriers view nonprofits with documented safety cultures and loss control measures as lower-risk accounts, which translates to better rates. Start your renewal process four months before your policy expires, not at the last minute when you have no leverage. Research shows that smaller nonprofits under $50 million in annual budget with favorable loss experience actually saw rate reductions in recent years as more carriers competed for stable business. Your loss history is a genuine asset in negotiations-use it.

Work with Providers Who Understand Nonprofit Operations

Specialized nonprofit insurance providers price based on your actual operations and mission-specific exposures rather than general market volatility. They understand that your coverage needs evolve as your programs expand or your volunteer base grows. Schedule an annual review with your insurance provider-not just at renewal-to discuss new programs, changes in staffing, or shifts in the populations you serve. Many nonprofits operate with outdated coverage limits that no longer reflect their current operations, which means they either overpay for unnecessary protection or carry dangerous gaps.

Assess Hidden Exposures and Update Valuations

A cyber liability assessment costs nothing when offered by your carrier and reveals whether your donor database, client health records, or volunteer screening files face genuine breach risk. Property valuations require annual updates because donated equipment and mission-critical assets often appreciate or depreciate in ways that book values miss entirely. If your nonprofit experienced claims in the past three years, work with your broker to explain the circumstances and demonstrate the corrective actions you implemented. This narrative directly influences underwriter decisions and can shift pricing from punitive to competitive.

Final Thoughts

Finding flexible nonprofit insurance options requires understanding your organization’s actual exposures and selecting coverages that address your mission-specific risks. We at Heaton Bennett Insurance understand that nonprofit leaders juggle mission delivery with financial constraints, which is why we focus on tailored solutions rather than one-size-fits-all policies. As an independent agency in Austin, Texas, we access multiple carriers and match your organization with providers who price based on your actual operations and offer flexible limits and deductibles that align with your budget.

Your next step is straightforward: contact Heaton Bennett Insurance to review your current coverage against your actual exposures. Bring your recent loss history, documentation of your safety protocols, and a list of any programs or populations you serve that might require specialized protection (such as youth programs or services for vulnerable populations). Many nonprofits discover coverage gaps or overpayment opportunities during this review that translate directly into better protection or lower premiums.

The investment in getting your nonprofit insurance options right pays dividends through reduced financial risk and genuine peace of mind that your mission stays protected. Starting your renewal conversations four months early gives you negotiating leverage based on your loss history and documented safety practices. Schedule your conversation today and take control of your nonprofit’s insurance strategy.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.