Contractor Insurance Coverage Texas: Ensure Your Projects Are Protected

Running a contracting business in Texas means navigating complex insurance requirements. Without proper contractor insurance coverage in Texas, you’re exposing your business to serious financial and legal risks.

We at Heaton Bennett Insurance know that choosing the right coverage can feel overwhelming. This guide breaks down what you actually need to protect your projects and your bottom line.

What Insurance Coverage Do Texas Contractors Actually Need

General Liability Insurance Protects Your Bottom Line

General liability insurance is your first line of defense, and it’s non-negotiable if you want to win contracts in Texas. This coverage protects you when someone gets injured on your job site or you accidentally damage a client’s property. Most project owners won’t even let you bid without proof of active general liability coverage, and many contracts demand a Certificate of Insurance before work begins. According to Insureon, Texas general contractors pay an average of around $152 monthly for general liability insurance, though this varies based on your construction type, the value of properties you work on, and your claims history. The standard minimum coverage limit sits around $1 million per occurrence, but larger projects often demand higher limits. You’ll want to add the general contractor as an additional insured on your policy and maintain clear documentation showing your policy limits and effective dates. Without a valid Certificate of Insurance, a general contractor can withhold payment or cancel your contract entirely, so this coverage directly affects your cash flow and bid eligibility.

Workers’ Compensation Protects Your Team and Your Business

Workers’ compensation insurance in Texas isn’t mandatory for all private employers, but it’s essential if you have employees, and many general contractors won’t hire subcontractors without proof of coverage. According to Insureon, average monthly premiums run around $306 for workers’ compensation. This coverage pays medical costs and lost wages when an employee gets injured on the job, and it protects your business from lawsuits by injured workers seeking damages. If you work on public projects or government contracts, workers’ compensation becomes legally required regardless of your employee count.

Commercial Auto Insurance Covers Your Fleet and Your Liability

Commercial auto insurance is equally critical because your personal auto policy won’t cover business use of vehicles. Texas requires minimum limits of 30/60/25 for company vehicles, and Insureon data shows average monthly premiums around $254. You need this coverage for any vehicle transporting tools, equipment, or employees to job sites. If your crew drives personal vehicles for work, add hired and non-owned auto coverage to fill the gaps your employees’ personal policies won’t touch.

These three coverages form the foundation of contractor protection in Texas. Your next step involves understanding which additional protections your specific projects demand, from builder’s risk to inland marine coverage.

What Texas Actually Requires From Contractor Insurance

Texas Licensing Takes a Hands-Off Approach

Texas takes a hands-off approach to contractor licensing compared to other states, but that doesn’t mean you’re free from insurance obligations. Texas has no statewide general contractor license requirement, which sounds like freedom until you realize that individual cities and counties impose their own rules.

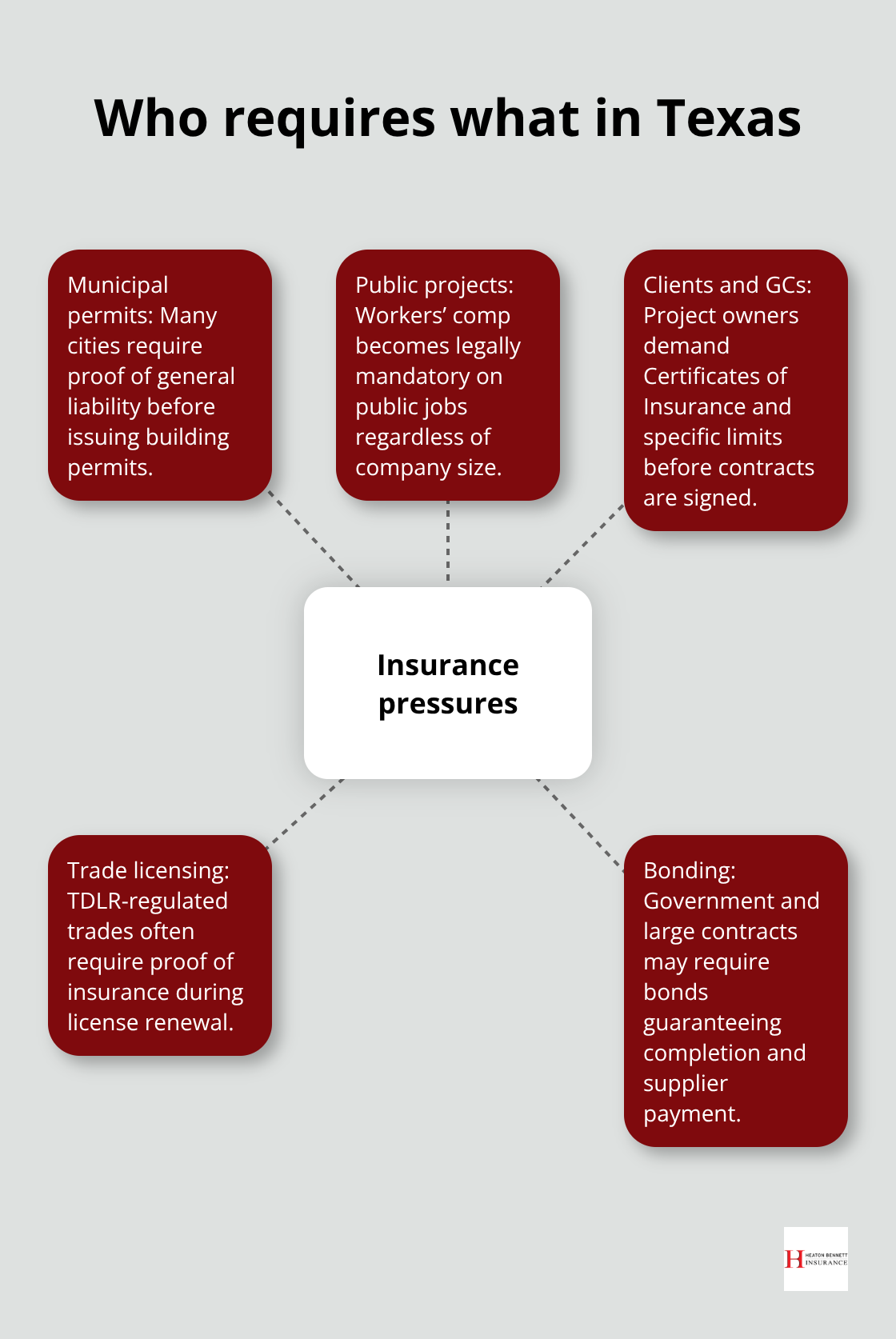

Many municipalities require proof of general liability insurance before issuing building permits, so you can’t simply skip coverage because the state doesn’t mandate it. The real pressure comes from project owners and clients who won’t sign contracts without a Certificate of Insurance showing active coverage.

Workers’ Compensation: Legal Gray Area, Practical Requirement

Workers’ compensation sits in a gray area that trips up many contractors. Texas doesn’t require private employers to carry workers’ comp, but the moment you work on public projects or government contracts, it becomes legally mandatory regardless of your company size. Most general contractors and project owners demand proof of workers’ compensation from subcontractors before allowing them on site, making it a practical requirement even when it’s not a legal one. According to Insureon, contractors pay around $306 monthly for workers’ comp on average, but skipping it when clients require it means losing bids entirely.

Coverage Limits Vary by Project Type and Client

Liability coverage minimums vary dramatically by project type and client, which is why a one-size-fits-all approach fails in Texas contracting. Residential projects often demand $1 million per occurrence, while commercial or government work frequently requires $2 million or higher. Some municipalities specify exact limits in their permit applications, so you need to review each project’s requirements upfront rather than assuming your existing policy covers everything. The Texas Department of Licensing and Regulation handles licensing for specific trades like electrical, plumbing, and HVAC work, and many of these trades require proof of insurance as part of their licensing renewal.

Professional Certifications and Bonding Demands

Professional certifications through the National Association of Home Builders also require documented insurance coverage, giving you another reason to maintain active policies beyond just legal compliance. Bonding requirements typically apply to government projects and larger contracts, guaranteeing project completion and payment to suppliers. These aren’t insurance policies but financial guarantees that protect your clients, and they become essential when bidding on public work in Texas cities.

Align Your Coverage With Each Project’s Specific Demands

Don’t assume Texas requirements end at the state level. Review your specific project’s contract language for insurance demands, confirm coverage limits with clients before submitting bids, and maintain current Certificates of Insurance accessible for immediate delivery. Larger projects scale up your coverage needs significantly, so a policy adequate for a $50,000 residential job won’t protect you on a $500,000 commercial renovation. Document every project’s insurance requirements in writing and verify your coverage aligns with those demands before work begins, preventing payment holds and contract cancellations that drain cash flow. With your Texas requirements mapped out, the next step involves selecting the right coverage limits and deductibles that match your business’s actual risk profile.

How to Choose the Right Contractor Insurance for Your Business

Map Your Actual Projects to Coverage Needs

Start with your last twelve months of projects instead of imagining worst-case scenarios. Pull your contracts and identify the coverage limits clients demanded, then examine the dollar values of properties you worked on and the number of employees on typical job sites. A roofing contractor working residential projects worth $75,000 to $150,000 per job with five employees has vastly different insurance needs than a commercial general contractor managing $2 million office renovations with fifty workers. Your claims history matters enormously-contractors with zero claims over five years often qualify for lower premiums and better terms than those with recent losses. Insureon data shows Texas contractors pay around $152 monthly for general liability on average, but this fluctuates based on construction type and your specific risk profile.

Compare Quotes With Identical Coverage Limits

Obtain quotes from at least three carriers and request identical coverage limits across all quotes so you’re comparing apples to apples. Many contractors select the cheapest option without verifying that deductibles and coverage limits actually meet their project requirements, then discover mid-project that their policy won’t cover a claim because limits fell short. Higher deductibles lower your monthly premium but increase what you pay out-of-pocket when claims happen-a $2,500 deductible works fine if your cash flow can absorb that hit, but a $10,000 deductible strangles businesses operating on thin margins.

Work With an Independent Agent for Your Trade

An independent agent who specializes in contractor insurance understands which carriers write aggressive policies for your specific trade and which ones shy away from your work type. Agents at independent agencies can often issue a Certificate of Insurance the same day you’re approved, which matters when you’ve got a bid deadline or need to start work immediately.

Ask your agent whether bundling your general liability, workers’ compensation, and commercial auto policies together saves money-many carriers offer bundle discounts that rival shopping policies individually.

Request a Risk Assessment Specific to Your Business

Request a risk assessment that identifies coverage gaps specific to your business, not generic contractor advice that applies to everyone. Some agents will review your actual project contracts and flag insurance requirements you might otherwise miss, preventing costly coverage disputes later. When you receive quotes, verify that additional insured endorsements are included at no extra charge, since project owners almost always demand this protection.

Understand Subcontractor Coverage and Documentation

Texas contractors frequently work with subcontractors, and your agent should help you understand what your policy covers regarding sub liability and what documentation you need from subs before they step on a job site. Your policy rarely covers subcontractors fully, so each sub must carry their own insurance and provide a Certificate of Insurance to you before starting work. Verify that your agent explains which endorsements protect you when subs work under your name and what happens if a sub causes damage or injury on your project.

Final Thoughts

Contractor insurance coverage in Texas protects your business from financial disaster and positions you to win contracts that competitors without proper coverage can’t touch. General liability shields you from third-party injury and property damage claims, workers’ compensation protects your employees while keeping lawsuits at bay, and commercial auto coverage keeps your fleet legally compliant as your crew transports tools and equipment between job sites. Texas municipalities, project owners, and government agencies all impose different insurance demands, so your coverage strategy must adapt to each contract rather than relying on a single policy year after year.

Cities demand proof of coverage before issuing permits, clients specify exact limits before signing contracts, and government work triggers mandatory workers’ compensation regardless of your company size. Ignoring these variations costs you bids, delays projects, and exposes you to payment holds when clients discover your coverage falls short of their requirements. Your actual business operations-your trade, project values, employee count, and claims history-determine what protection you truly need.

Contact Heaton Bennett Insurance to discuss your specific contractor insurance needs and receive quotes that match your actual risk profile rather than generic contractor assumptions. Our team works with multiple carriers to find coverage that protects your projects, your team, and your bottom line without forcing unnecessary extras or leaving dangerous gaps.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.