Restaurant Insurance Texas: Protecting Your Eatery in a Vibrant Market

Running a restaurant in Texas means facing unique risks that most business owners underestimate. From food-borne illness lawsuits to severe weather damage, the threats to your operation are real and costly.

Restaurant insurance in Texas isn’t optional-it’s the foundation that keeps your business standing when problems hit. We at Heaton Bennett Insurance help restaurant owners across the state build coverage that actually matches their specific challenges.

Why Restaurant Insurance Matters in Texas

Food Service Liability Threatens Your Bottom Line

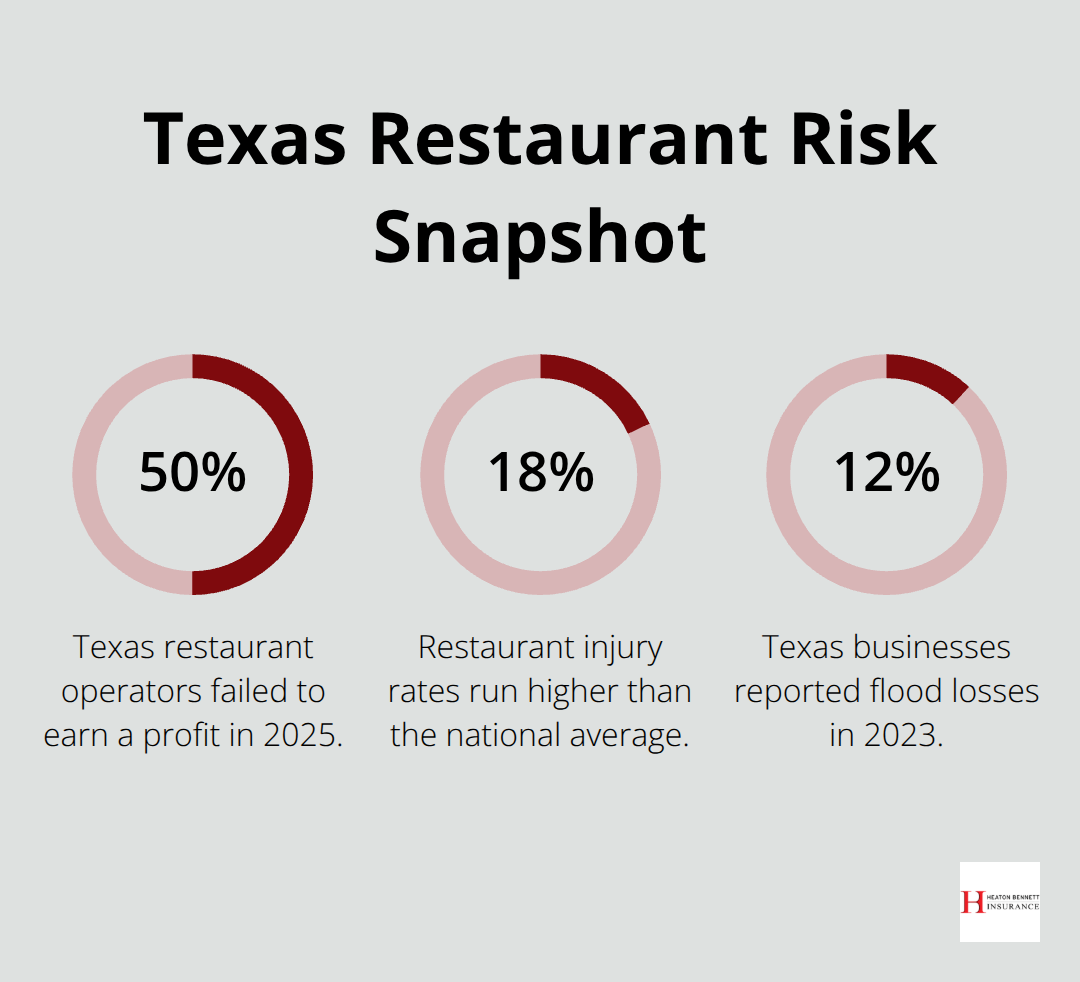

Food service liability in Texas restaurants demands serious attention from owners. The National Restaurant Association reported that 50% of Texas restaurant operators failed to earn a profit in 2025, and a single lawsuit can wipe out what little margin remains. Slip-and-fall claims, food poisoning incidents, and alcohol-related injuries occur regularly in this state, and they cost significant money.

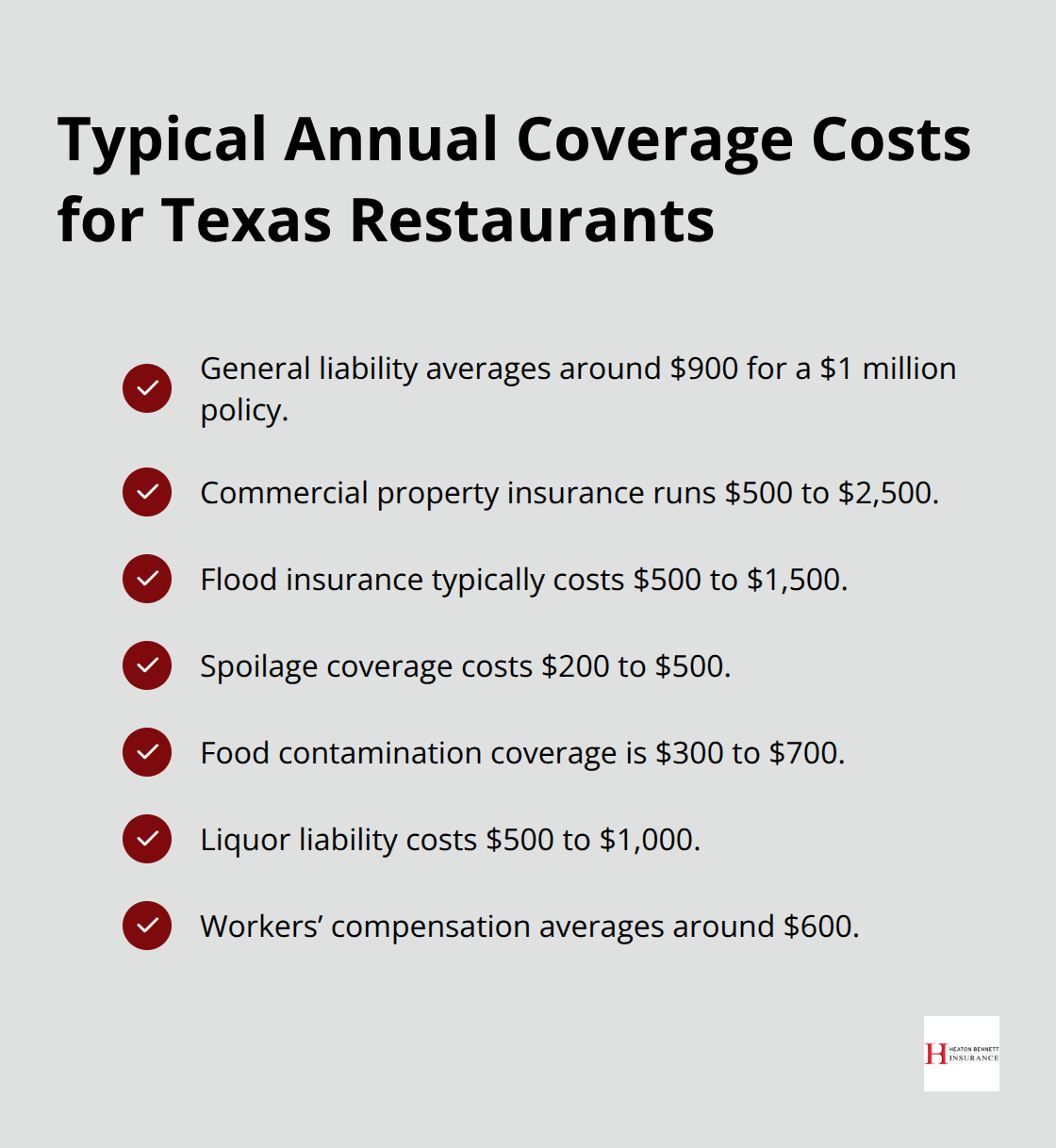

General liability insurance for $1 million in Texas costs between $500 and $2,500 annually, with an average around $900 according to industry data. One customer injury claim can cost tens of thousands out of pocket without coverage. Texas dram shop laws create particular risk around alcohol service, which is why liquor liability insurance costs $500 to $1,000 per year for establishments serving drinks.

Staff Injuries and Workers’ Compensation Obligations

Your staff faces real hazards in daily operations. OSHA data show restaurant injury rates run about 18% higher than the national average, meaning workers’ compensation claims happen frequently in Texas kitchens and dining areas. Operating without workers’ compensation coverage exposes you to personal liability for employee medical bills and lost wages, which in Texas can reach $3,000 annually per employee on average. This exposure grows with each staff member you hire, making coverage essential rather than optional.

Hurricane and Flood Risks Along the Coast

Texas weather creates insurance exposures that other states simply don’t face. Coastal areas near Galveston see property insurance premiums run 20% to 30% higher due to hurricane and flood risk, and about 12% of Texas businesses reported flood losses in 2023 according to FEMA data. Standard commercial property policies exclude flood coverage entirely, leaving restaurants vulnerable during heavy rainfall or storm surge. Flood insurance costs $500 to $1,500 annually but becomes essential in high-risk zones.

Power Outages and Spoilage Protection

Wildfires threaten restaurants in central and west Texas, destroying buildings and equipment with little warning. Power outages from storms create another hidden risk-spoiled food losses. Spoilage coverage typically costs $200 to $500 per year and protects your inventory when refrigeration fails during weather events. Many restaurant owners skip this coverage and absorb thousands in losses when a summer thunderstorm knocks out power for hours.

Food contamination coverage, running $300 to $700 annually, covers cleanup costs and lost income after contamination events, whether from weather-related issues or operational failures.

Moving Forward with Comprehensive Protection

These specialized coverages aren’t luxuries in Texas; they’re practical necessities that keep your business operating through the unpredictable weather patterns this state experiences regularly. Understanding what risks your restaurant faces sets the stage for selecting the right coverage types-each designed to address specific threats your operation encounters.

What Coverage Do Texas Restaurants Actually Need

General Liability: Your First Line of Defense

General liability insurance forms the foundation for any Texas restaurant, yet many owners carry limits that fall dangerously short of their actual exposure. A $1 million policy costs around $900 annually on average, but a single serious food poisoning outbreak or slip-and-fall injury can exceed that coverage in legal fees alone. Food contamination claims in Texas restaurants frequently involve multiple customers, multiplying medical costs and legal expenses. Restaurant owners should verify their liability limits match their annual revenue; a good benchmark is coverage equal to at least one year of gross revenue. One customer injury claim can cost tens of thousands out of pocket without adequate protection.

Property Insurance Covers Your Physical Assets

Commercial property insurance protects your building, kitchen equipment, and inventory from fire, theft, and weather damage, typically costing $500 to $2,500 annually depending on property value and location. Urban restaurants in Dallas and Houston pay 10% to 20% more than rural operations due to higher litigation risk. Your landlord’s insurance does not cover your equipment or inventory-you must carry your own property policy. Standard property policies exclude flood damage entirely, which matters critically in Texas where 12% of businesses reported flood losses in 2023 according to FEMA data. Adding flood coverage costs $500 to $1,500 yearly but prevents catastrophic losses during the heavy rainfall events Texas experiences regularly.

Workers’ Compensation and Employment Liability

Workers’ compensation remains optional in Texas, creating a false sense of savings that exposes you to serious personal liability. Restaurant injury rates run 18% higher than the national average according to OSHA data, meaning your kitchen and dining floor generate claims more frequently than other business types. Operating without this coverage leaves you personally responsible for employee medical bills, lost wages, and disability claims that can reach thousands per incident. Average costs run around $600 annually but climb with payroll size and kitchen complexity; each additional employee typically adds $100 to $200 per year. Employment practices liability insurance protects against wrongful termination, discrimination, and harassment claims-exposures that grow sharply as your team expands.

Liquor Liability and Policy Bundling

Liquor liability insurance costs $500 to $1,000 annually and becomes mandatory if you serve alcohol; Texas dram shop laws hold restaurants liable for injuries caused by intoxicated patrons, making this coverage non-negotiable rather than optional. Bundling general liability, property, and business interruption into a Business Owner’s Policy saves approximately 10% to 15% on premiums compared to purchasing policies separately, making a BOP the most practical starting point for Texas restaurant owners. This bundled approach simplifies administration while reducing your overall insurance costs. The right coverage combination protects your investment while keeping premiums manageable, but selecting that combination requires understanding how different policy types interact with your specific operation. Location, size, and service model all influence which coverages matter most-factors that shape the cost and structure of your insurance strategy.

What Restaurant Size and Location Really Cost You

How Location Shapes Your Insurance Expenses

Your restaurant’s location fundamentally determines your insurance costs, and understanding these geographic price drivers helps you budget accurately. A Houston barbecue joint with $1 million in annual revenue pays roughly $4,000 for a Business Owner’s Policy, while a Waco food truck generating $200,000 in revenue pays around $2,200 according to industry benchmarks. Urban restaurants in Dallas and Houston face general liability premiums 10% to 20% higher than rural operations because dense urban areas create elevated litigation risk and higher jury awards. Coastal Texas locations near Galveston experience property premiums 20% to 30% above inland rates due to hurricane and flood exposure that insurers price aggressively.

Restaurant Type and Size Impact Your Bottom Line

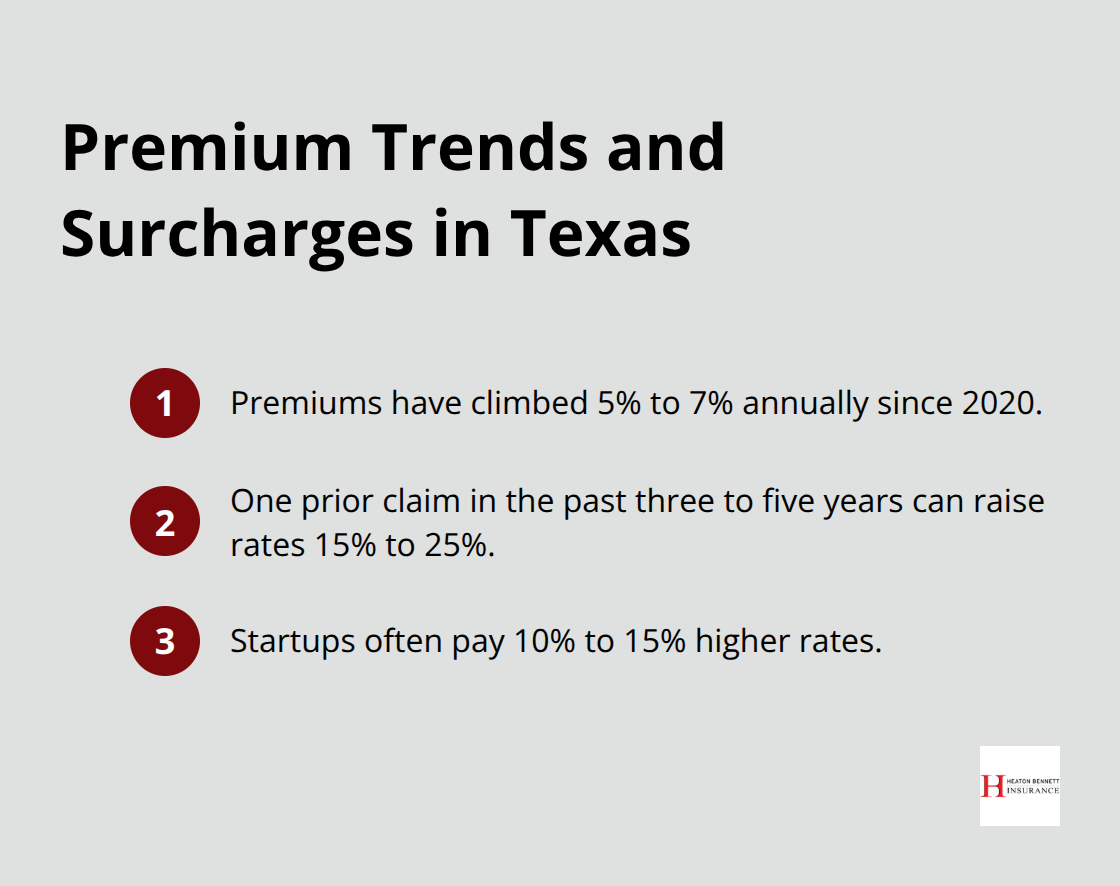

Fast-food operations typically cost less than full-service restaurants, with fast-food Business Owner’s Policies ranging $2,000 to $3,500 annually compared to $3,500 to $5,500 for fine dining establishments. Each additional employee adds $100 to $200 annually to your workers’ compensation costs, so payroll expansion directly impacts your insurance budget. Restaurant insurance premiums across Texas have climbed 5% to 7% annually since 2020 due to inflation and larger jury awards, meaning your costs this year will almost certainly exceed last year’s expenses. One insurance claim in the past three to five years pushes premiums up 15% to 25%, which underscores why preventing incidents matters more than accepting claims and absorbing rate increases.

Bundling Policies Delivers Real Savings

A Business Owner’s Policy bundling property and general liability saves 10% to 15% compared to purchasing separate policies, and many Texas Restaurant Association members qualify for additional 3% to 5% discounts on bundled coverage. Implementing staff safety training cuts injury claims by up to 25%, while regular equipment maintenance yields 5% to 10% premium discounts that offset the maintenance costs themselves. Upgrading fire alarms or installing security cameras saves hundreds of dollars annually because insurers reward loss prevention investments with concrete rate reductions.

Comparing Quotes Across Multiple Carriers

You need quotes from multiple carriers to identify the best value, but the lowest quote often reflects aggressive underwriting that creates claim denial risk later. When you evaluate policies, request quotes with identical limits and deductibles across multiple insurers so you compare actual risk pricing rather than coverage variations. Startups without established claims history face 10% to 15% higher rates because insurers lack loss data, but that premium penalty drops significantly after two years of clean claims history.

Final Thoughts

Restaurant insurance in Texas protects your investment when unexpected events threaten your operation, and the costs of inadequate coverage far exceed the premiums you pay annually. A single liability claim or weather event can eliminate years of profit, making comprehensive protection essential rather than optional. Texas-specific hazards like hurricanes, floods, and wildfires demand coverage tailored to your location and business model, not generic policies designed for restaurants elsewhere.

The data shows that 50% of Texas restaurant operators failed to earn profit in 2025, with rising food, labor, and insurance costs continuing to squeeze margins across the state. A Business Owner’s Policy bundled with workers’ compensation and liquor liability provides the foundation most restaurants need, though your specific operation may require additional protections like spoilage coverage or cyber insurance depending on your service model and location. Staff safety training, regular equipment maintenance, and prompt hazard repairs reduce your claims frequency and lower your premiums over time, turning risk prevention into concrete savings.

We at Heaton Bennett Insurance work with restaurant owners across Texas to build coverage that matches your specific challenges and helps you find the right balance between protection and cost. Contact Heaton Bennett Insurance to discuss your restaurant’s coverage needs and access multiple carriers through our personalized approach.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.