Nonprofit Liability Coverage: Aligning with Your Mission and Risk

Nonprofits face unique risks that most organizations don’t encounter. From board decisions to employment disputes, the threats to your mission are real and costly.

At Heaton Bennett Insurance, we’ve seen how the right nonprofit liability coverage protects what you’ve built. This guide walks you through the coverage types that matter most for your organization.

Where Your Nonprofit’s Biggest Liability Risks Hide

Board Decisions Create Personal and Organizational Liability

Board members make governance decisions every day, and those choices carry personal and organizational liability. When a board votes on budget cuts, program changes, or personnel matters, members can face lawsuits claiming their decisions harmed the organization or violated fiduciary duties. The Alera Group’s 2023 Property & Casualty Market Outlook warns that underwriters increasingly scrutinize nonprofit governance, and verdicts against boards are climbing. Directors and Officers liability insurance shields board members from personal financial loss and covers legal defense costs, but many nonprofits skip this coverage thinking their small size protects them. That assumption is dangerous. A single board decision-whether about hiring, fund allocation, or program direction-can trigger litigation that exhausts your reserves if you lack D&O coverage.

Employment Disputes Drain Resources Faster Than You Expect

Employment disputes cost nonprofits far more than most leaders expect. The Alera Group data shows that employment law claims involving harassment, wrongful termination, discrimination, and wage violations rank among the costliest exposures nonprofits face, with rates rising across the sector. Your staff and volunteers are human, conflicts happen, and one disgruntled employee can file a claim that consumes months of operating budget on legal fees alone. Employment Practices Liability Insurance protects your organization from these lawsuits and covers the legal costs that follow.

General Liability Exposures Multiply With Every Program

General liability claims from visitors injured at events, property damage during programs, or accidents involving your facilities add another layer of risk. If someone slips at your fundraiser or a volunteer accidentally damages a donor’s property, your organization pays unless you have coverage in place. These incidents happen more often than nonprofits anticipate, and the costs accumulate quickly without proper protection.

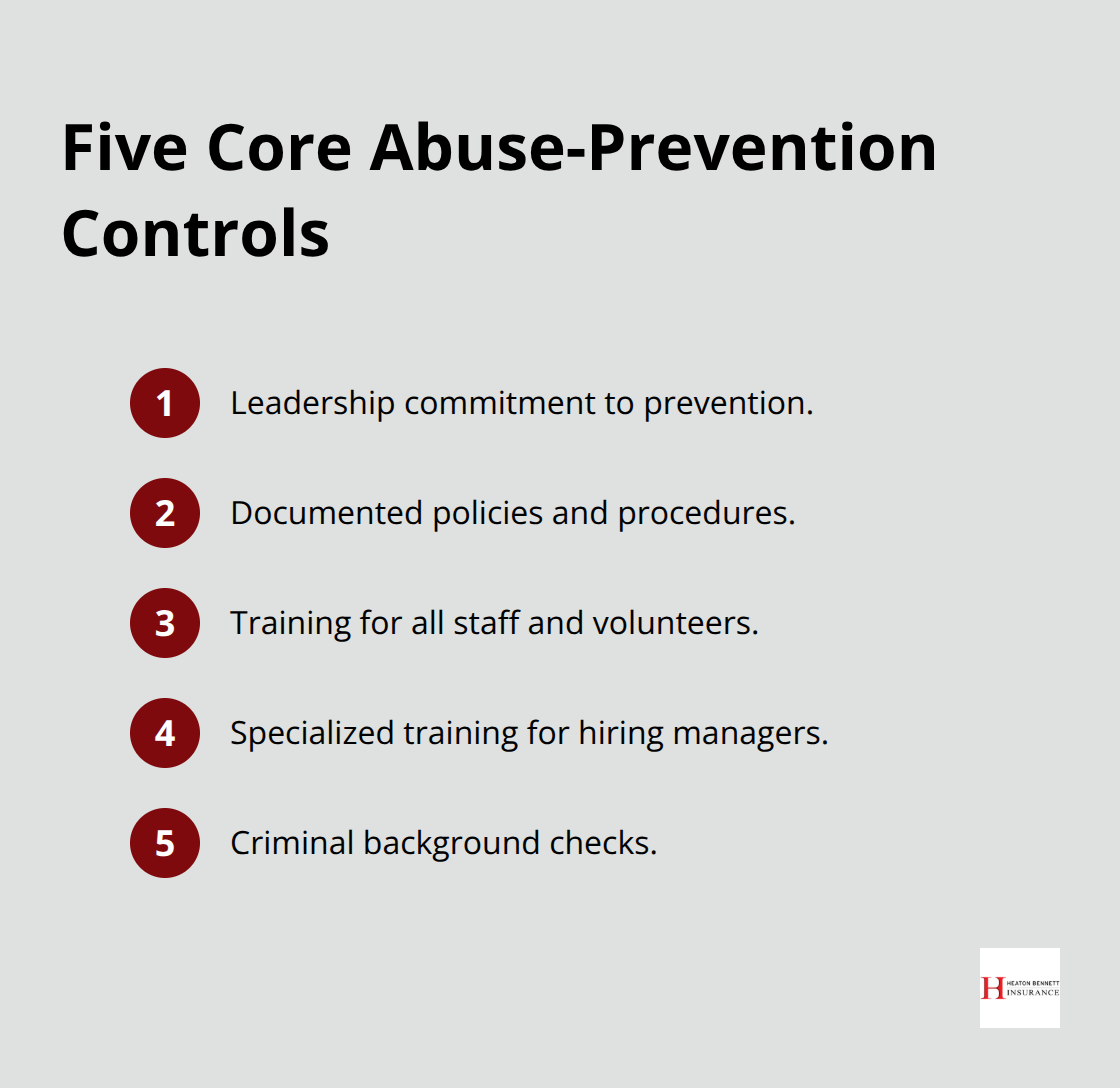

Abuse Liability Requires Documented Prevention and Coverage

Nonprofits serving youth or vulnerable populations face heightened abuse liability exposure. According to Philadelphia Insurance Companies, organizations must implement five core protections: leadership support for prevention, documented policies, staff and volunteer training, specific hiring manager training, and criminal background checks. The Boy Scouts of America settlement of 2.46 billion dollars demonstrates that insufficient abuse prevention policies create catastrophic financial and reputational consequences. Your liability exposure isn’t theoretical-it’s operational, and it grows with every program you run and every person you serve.

Your Risk Profile Demands a Tailored Response

The combination of board liability, employment claims, general liability, and abuse exposure means your nonprofit operates in a complex risk environment. No two organizations face identical threats, which is why a one-size-fits-all insurance approach fails most nonprofits. Understanding what coverage types exist is only the first step; the real work involves matching those coverages to your specific mission, activities, and risk profile.

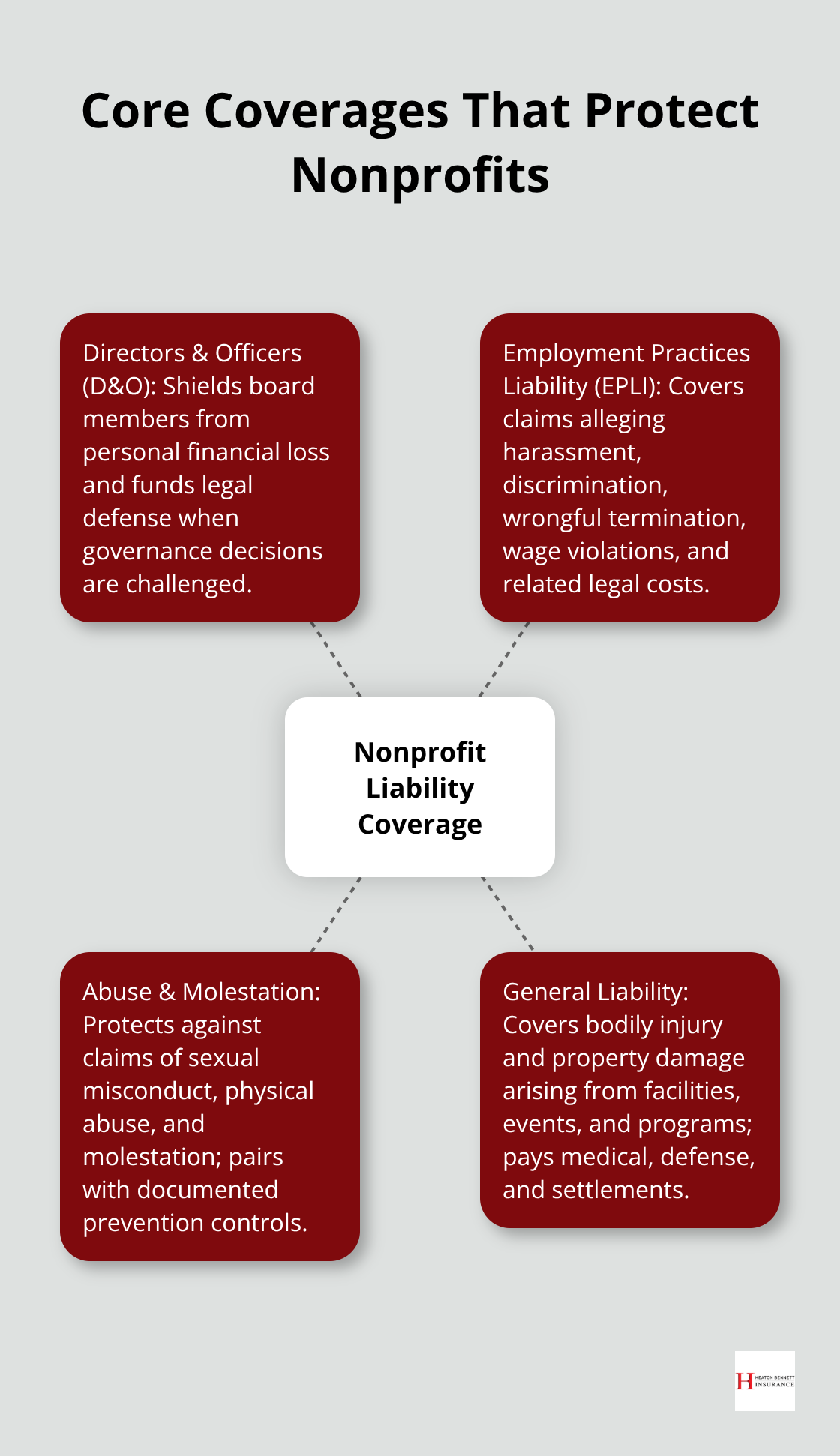

Coverage Types That Actually Protect Your Mission

Directors and Officers Insurance Shields Board Members and Budgets

Directors and Officers insurance protects board members from personal liability when their governance decisions face legal challenge. This coverage pays for legal defense costs and settlements if a board member faces a lawsuit for breach of fiduciary duty, mismanagement of funds, or decisions that allegedly harmed the organization. The Alera Group’s 2023 Property & Casualty Market Outlook reveals that underwriters now favor nonprofits that demonstrate strong risk controls and documented governance practices, which means organizations with solid D&O coverage and board training receive better pricing. Without this protection, board members face personal financial exposure that discourages qualified leaders from serving, and your organization absorbs litigation costs that drain operating funds. D&O coverage becomes even more critical when your nonprofit serves vulnerable populations or makes decisions affecting public safety, where legal standards are higher and verdicts larger.

Employment Practices Liability Insurance Protects Against Workforce Claims

Employment Practices Liability Insurance covers claims from employees and volunteers alleging harassment, wrongful termination, discrimination, wage violations, and workplace bullying. The Alera Group data shows employment law claims rank among the costliest exposures nonprofits face, with rates rising as employment standards tighten. EPLI pays legal defense costs and settlements, protecting your organization from depleting reserves on litigation. One wrongful termination lawsuit can cost $50,000 to $150,000 in legal fees alone before any settlement, making this coverage essential for nonprofits with staff. Coverage should extend to volunteers when they perform substantive work, since volunteer disputes create identical legal exposure to employee claims.

Abuse and Molestation Coverage Addresses Your Highest-Stakes Exposure

Nonprofits serving youth or vulnerable populations face catastrophic liability from abuse claims. Philadelphia Insurance Companies identifies five core protections organizations must implement: documented leadership commitment to prevention, written policies and procedures, training for all staff and volunteers, specialized training for hiring managers, and criminal background checks. Coverage alone isn’t sufficient without these operational controls in place, but insurance is non-negotiable. The Boy Scouts of America settlement reached $2.46 billion, demonstrating that inadequate prevention policies and insufficient coverage create financial devastation. Abuse liability coverage protects against claims of sexual misconduct, physical abuse, and molestation involving staff, volunteers, or program participants. Underwriters increasingly scrutinize nonprofits in this space, and capacity for abuse coverage is shrinking, making it harder to obtain affordable rates. Organizations serving vulnerable populations should treat abuse liability coverage as mandatory, not optional.

General Liability Covers Day-to-Day Operational Risks

General liability insurance protects against bodily injury claims when someone is injured at your facility or during your programs, and property damage claims when your operations damage someone else’s property.

A visitor slipping at your fundraiser, a volunteer accidentally damaging a donor’s equipment, or property damage during an event all trigger general liability exposure. This coverage pays medical expenses, legal defense, and settlements. Many nonprofits underestimate how frequently these incidents occur; they’re not rare edge cases but routine operational risks. Coverage limits should reflect your program scope and attendance at events, with higher limits if you host large public gatherings.

Your nonprofit’s liability landscape extends beyond these core coverages. The next section walks you through how to assess your organization’s specific risks and match them to the right protection strategy.

How to Match Your Coverage to Your Organization’s Real Risks

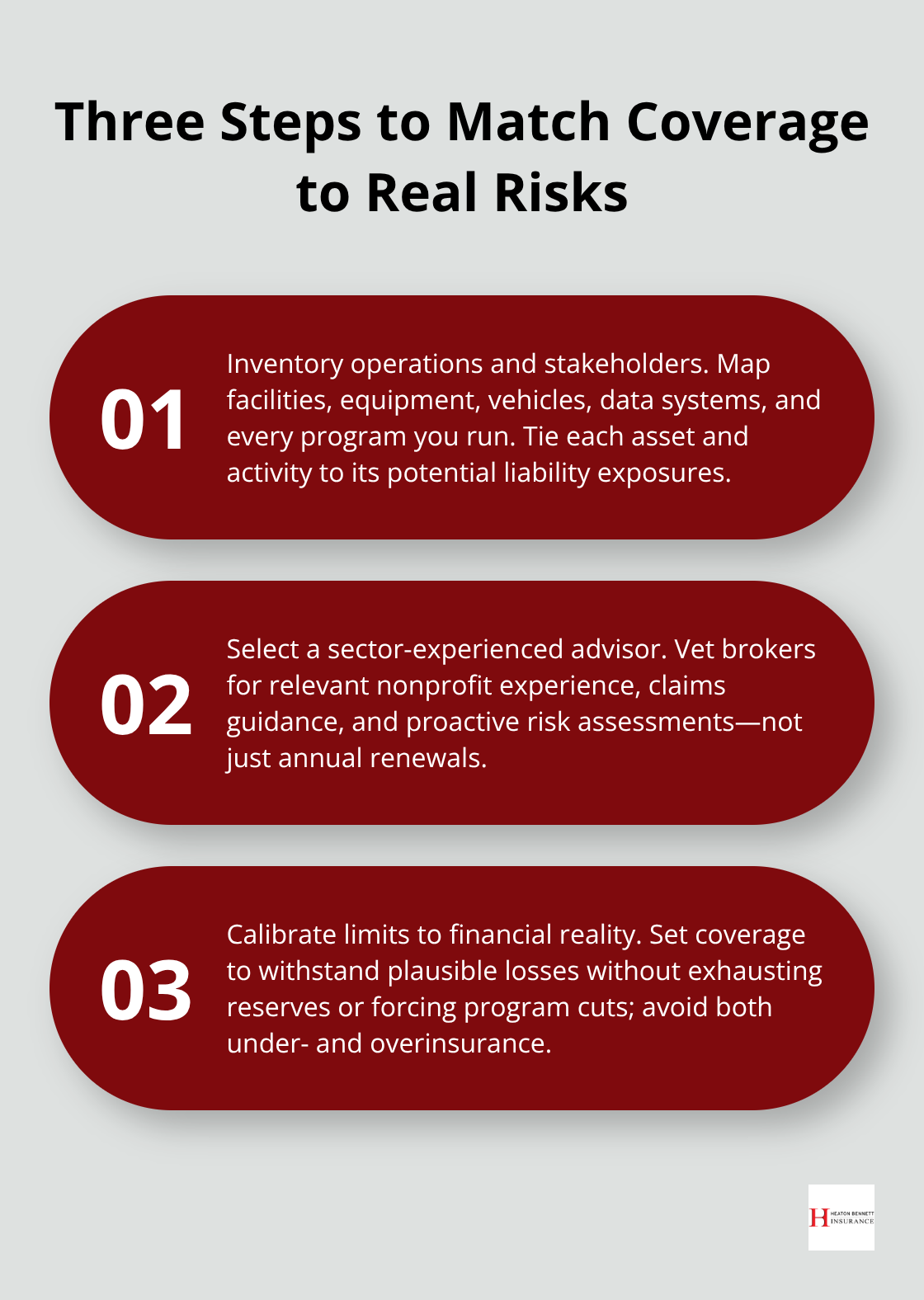

Inventory Your Operations and Identify Your Exposure

Start with a specific inventory of your nonprofit’s operations and the people you serve. Walk through your facility and document what exists: the building itself, equipment, vehicles, technology systems holding donor data, and any specialized assets. Then map your programs and activities. If you run youth mentoring, you face abuse liability exposure that a food bank doesn’t. If you operate a fleet of vans for transportation, commercial auto coverage becomes non-negotiable. If your board makes significant decisions affecting vulnerable populations, D&O coverage protects against higher-stakes litigation. The Alera Group’s 2023 Property & Casualty Market Outlook shows that underwriters favor nonprofits that demonstrate strong risk controls and documented governance practices, which means you need to articulate exactly what you do and who you serve.

A counseling center serving trauma survivors faces different risks than a community garden nonprofit. Don’t rely on generic nonprofit checklists that claim every organization needs the same coverage. Your real risk profile is specific, and your coverage should match it.

Select an Advisor With Real Nonprofit Sector Experience

Work with an insurance professional who has measurable experience with nonprofits in your sector, not a generalist who handles nonprofits as a side business. Ask potential advisors how many nonprofit clients they serve, what types of organizations they work with, and whether they specialize in your mission area. A broker familiar with youth-serving organizations understands abuse liability intricacies. One experienced with international nonprofits knows how mission scope affects coverage needs. The quality of guidance you receive depends on the advisor’s depth of nonprofit experience.

Ask whether they’ve helped clients navigate claims, not just sold policies. Ask if they conduct regular risk assessments or simply renew coverage annually without review. Prioritize advisors who push back on underinsurance rather than accept whatever budget you propose, because accepting insufficient coverage to save money creates catastrophic exposure.

Calibrate Coverage Limits to Your Financial Reality

Your coverage limits should reflect your actual financial risk. If a single claim could exhaust your reserves or force program cuts, your limits are too low. If you’ve never had a claim and your limits exceed your total assets by five times over, you may be overinsured. An experienced advisor helps you calibrate limits to your organization’s financial capacity and operational reality.

Final Thoughts

Your nonprofit’s mission matters too much to leave liability protection to chance. The coverage types we’ve outlined-Directors and Officers insurance, Employment Practices Liability Insurance, abuse and molestation coverage, and general liability-form the foundation of nonprofit liability coverage that actually works. But coverage alone doesn’t protect your organization; the real protection comes from matching those policies to your specific operations, the populations you serve, and the decisions your board makes every day.

Nonprofits that survive claims and continue their work share one characteristic: they aligned their insurance strategy with their actual risk profile before crisis struck. They didn’t assume their size protected them or that generic nonprofit policies covered their unique exposures. They conducted honest assessments of what could go wrong, worked with advisors who understood their sector, and calibrated coverage limits to their financial reality.

The cost of nonprofit liability coverage is real, but it’s far smaller than the cost of operating without it. A single employment dispute, board decision challenged in court, or abuse claim can consume years of operating budget and damage your reputation beyond repair. Contact Heaton Bennett Insurance to discuss your nonprofit’s specific risks and coverage needs-their team understands that every organization operates differently and provides tailored solutions that match your mission and financial capacity.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.