Restaurant Property Insurance: Safeguarding Your Premises

Your restaurant faces constant risks-from kitchen fires to theft to unexpected closures. Restaurant property insurance protects your building, equipment, and inventory from these threats.

We at Heaton Bennett Insurance know that one disaster can devastate your business. The right coverage gives you the financial security to recover and keep operating.

What Restaurant Property Insurance Actually Covers

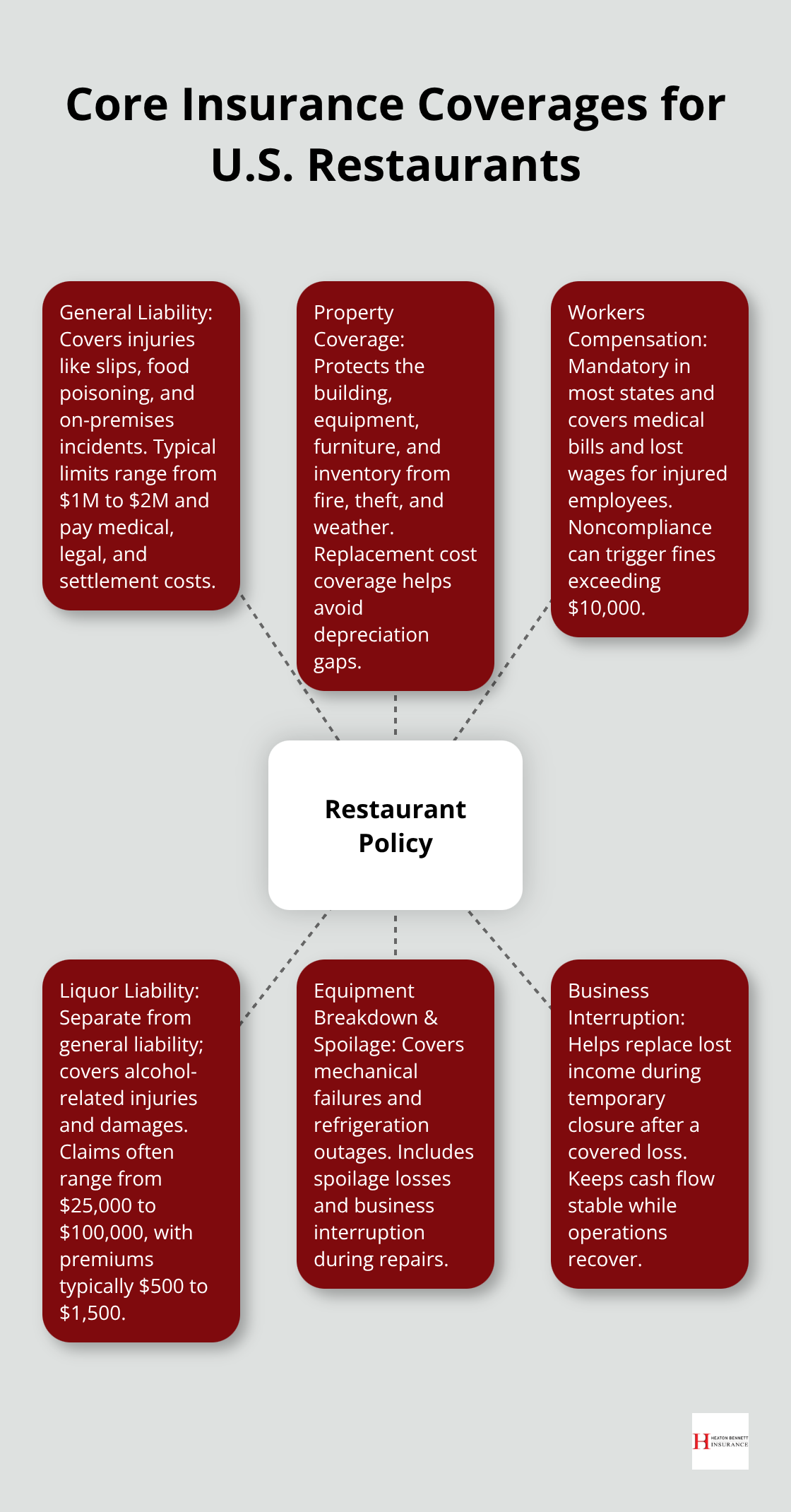

Restaurant property insurance protects three core assets that directly impact your ability to operate. Your building structure-walls, roof, flooring, electrical systems, and HVAC-receives coverage against fire, windstorms, hail, theft, and vandalism. If you lease your space, you need coverage for tenant improvements and built-in equipment you’ve installed, since your landlord’s policy covers only the building shell. A 2,000-square-foot restaurant building typically costs $300,000 to $500,000 to rebuild at current prices, so your policy limits must reflect this reality. Many operators underestimate replacement costs and end up underinsured; the solution is obtaining current quotes from contractors for major systems before setting your coverage limits.

Kitchen Equipment Demands Explicit Coverage

Your six-burner range costs $4,000 to $7,000, a walk-in cooler runs $8,000 to $15,000, and a hood system with suppression can reach $12,000 to $25,000. Standard property policies do not automatically cover equipment breakdown from mechanical or electrical failures-you need an explicit equipment breakdown endorsement. This gap matters because refrigeration failures cause immediate spoilage; without a spoilage endorsement, you absorb the full loss on perishable inventory. Add equipment breakdown coverage starting at around $5 monthly, and pair it with spoilage protection that covers loss from power outages and compressor failures. Document your equipment with photos and receipts, then request replacement-cost quotes to set accurate limits.

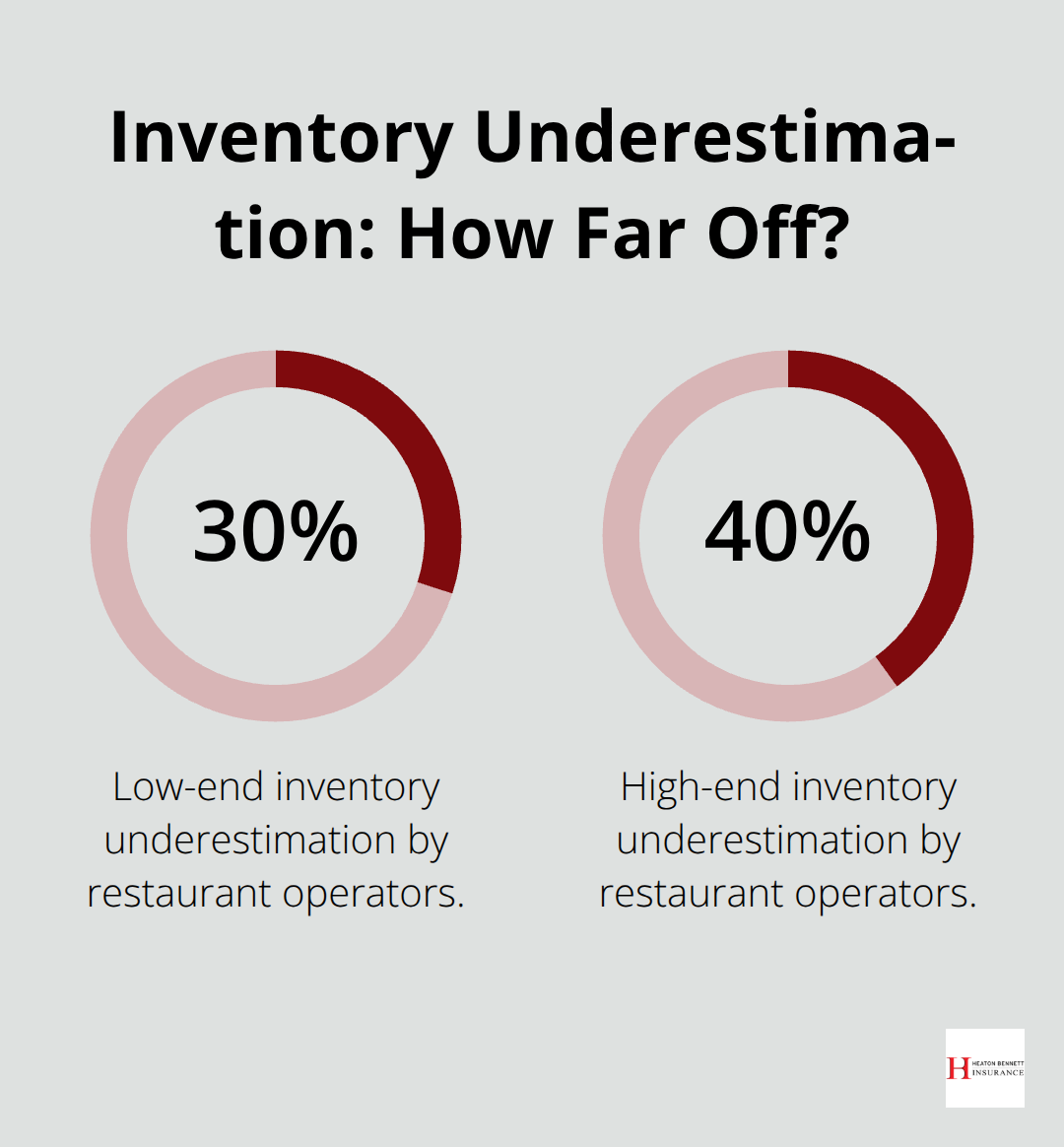

Inventory Underestimation Drains Your Bottom Line

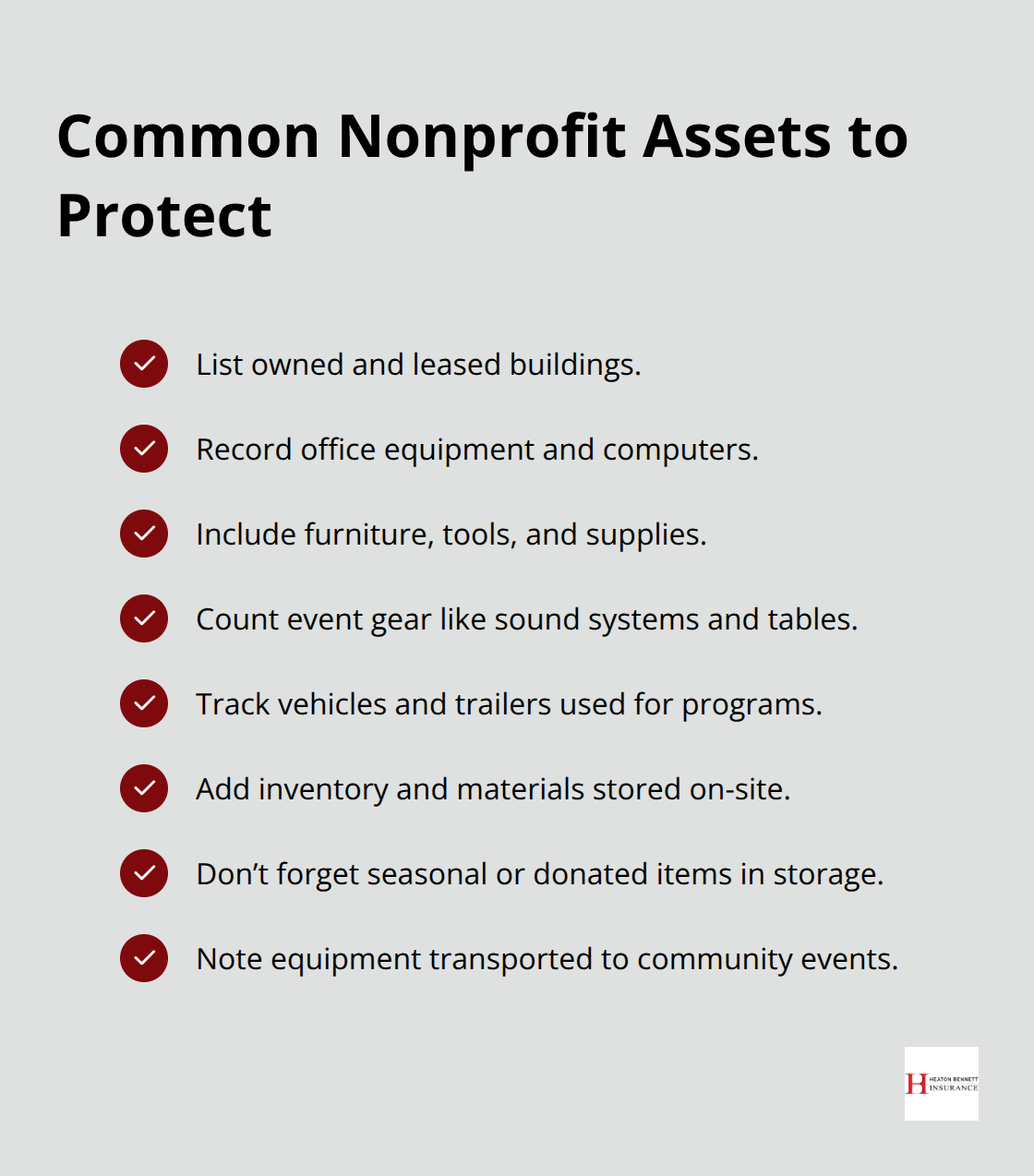

Most restaurant operators underestimate stock value by 30 to 40 percent. Your inventory endorsement should cover items at replacement cost-what you’d pay today to replace them-not actual cash value, which applies depreciation and leaves you short.

Count everything: food in freezers and walk-ins, dry goods, beverages, takeout containers, and smallwares. If a power outage spoils your stock or a kitchen fire destroys your inventory, replacement-cost coverage reimburses you fully rather than a depreciated amount. Review and adjust these limits annually, especially after menu changes, seasonal expansions, or new equipment purchases that increase your on-hand stock value.

Water Damage and Spoilage Need Separate Protection

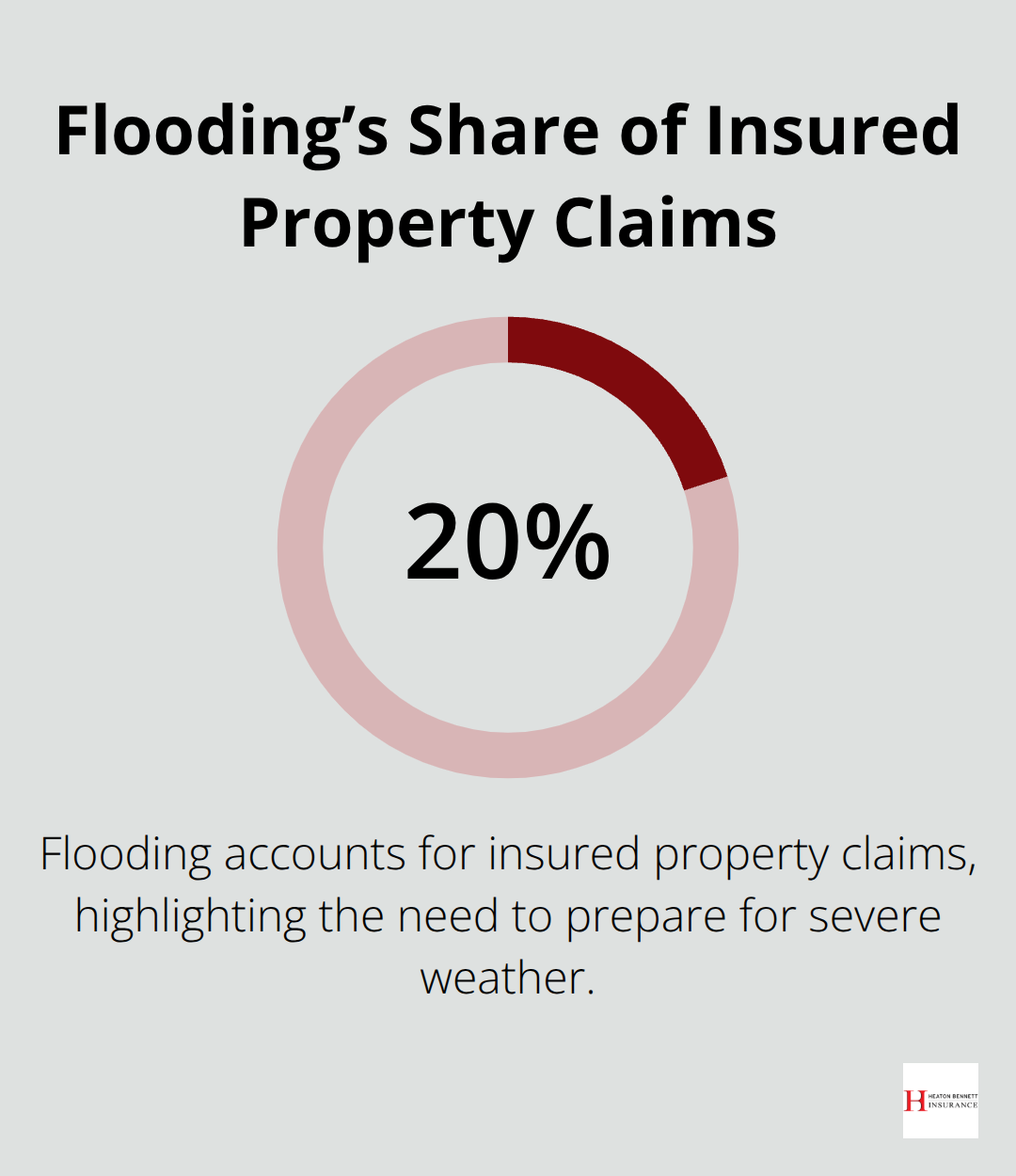

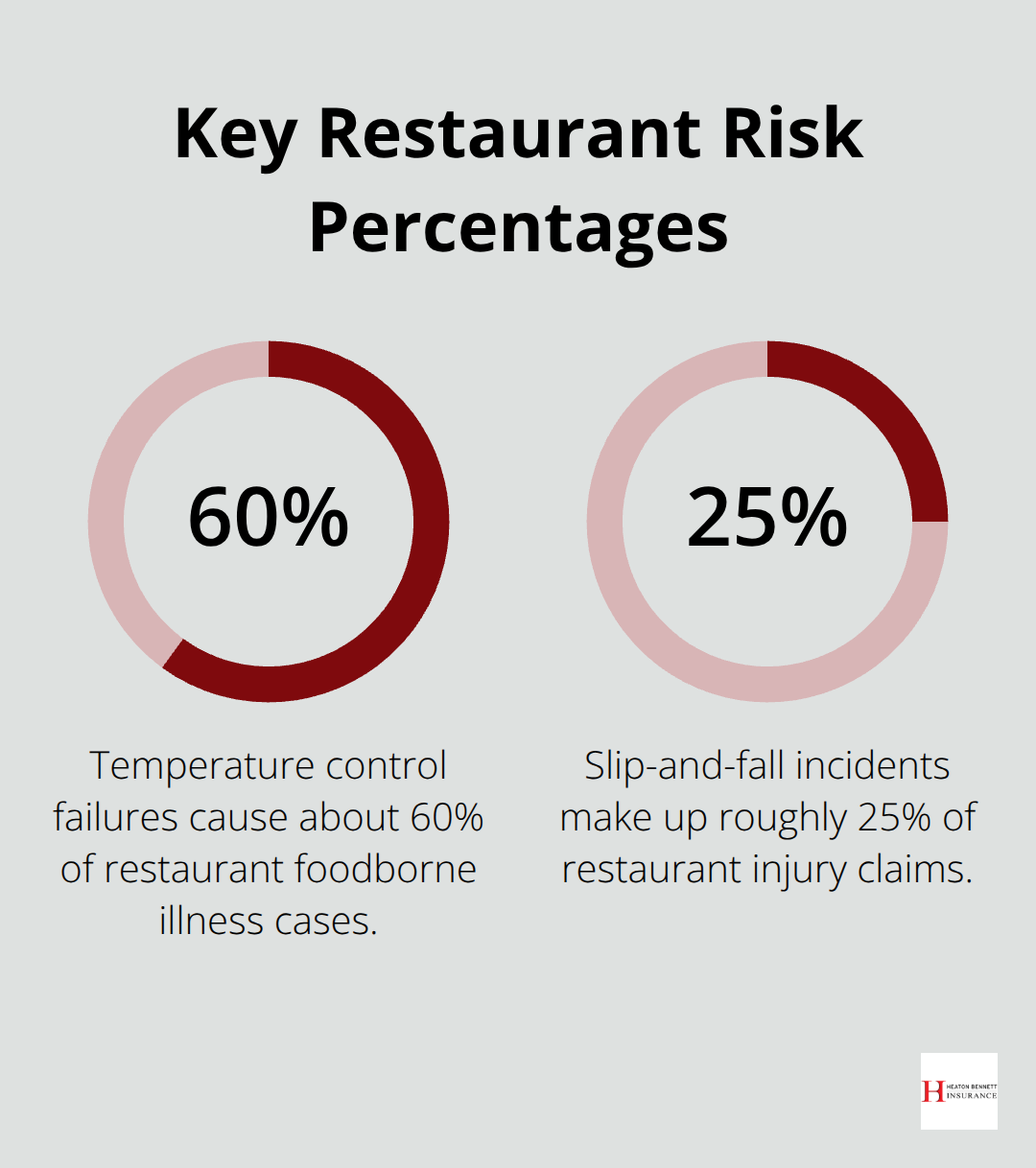

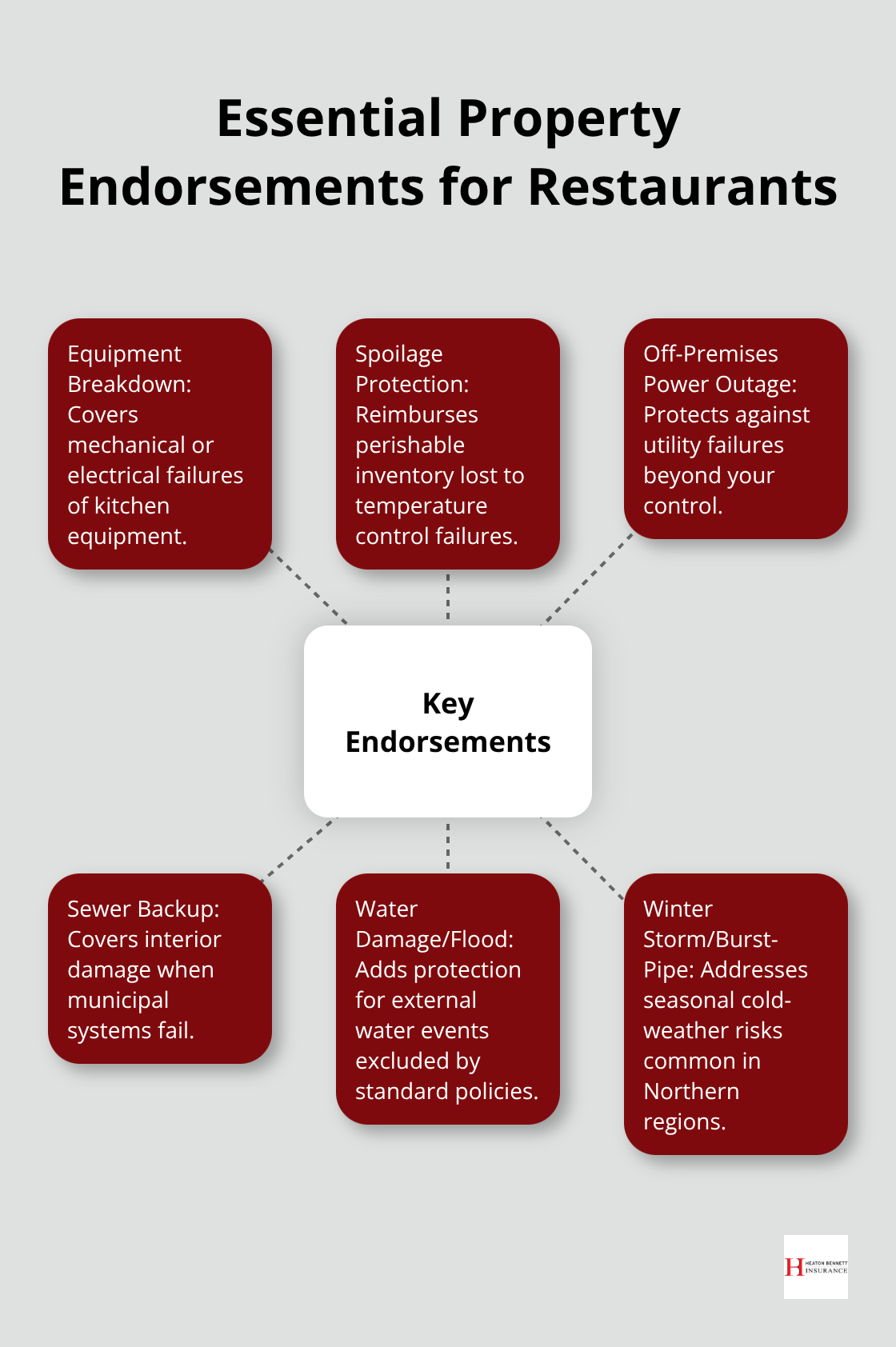

Water damage from burst pipes or flooding often falls outside standard property policies; you need separate endorsements or riders to cover water damage from external sources. Temperature control failures in refrigeration lead to immediate spoilage, and standard coverage excludes this loss unless you add a spoilage endorsement. Off-premises power outage spoilage protection covers inventory loss when utility failures strike your neighborhood, not just your equipment. Sewer backup coverage protects against interior damage when municipal systems fail. These endorsements cost little but prevent catastrophic losses that standard policies leave uncovered.

Location and Seasonal Risks Shape Your Coverage

Northern Indiana restaurants face winter storms that damage roofs and burst pipes, making region-specific endorsements necessary beyond standard coverage. Weather-related threats follow seasonal patterns and can include wind, hail, and power outages; premiums in flood-prone areas typically rise 15 to 25 percent based on historical loss data. Your location risk directly influences both your premium and the endorsements you need. An independent insurance agency can compare multiple carriers to tailor a property-damage program for competitive pricing and coverage that matches your specific geographic exposure. Understanding your building’s replacement cost, equipment values, and inventory levels positions you to select limits that actually protect your operation when disaster strikes.

Why Your Restaurant Cannot Afford to Skip Property Insurance

Kitchen Fires Demand Immediate Financial Protection

Kitchen fires destroy restaurants faster than most operators realize. The National Fire Protection Association reports that unattended cooking causes the leading restaurant fires, and a grease fire spreads to your ventilation system within minutes, risking thousands of dollars in equipment damage and forcing a shutdown if your suppression system fails inspection. Property insurance covers the financial aftermath of fire, but only if your coverage limits match your actual replacement costs. A hood system with suppression runs $12,000 to $25,000, and losing it mid-service without proper coverage means weeks of closure while you fundraise for replacements. Your suppression system requires annual inspection and certification per NFPA 96 standards; regular maintenance prevents small fires from becoming catastrophic losses that expose coverage gaps.

Winter Storms and Weather Events Hit Hard in Northern Indiana

Winter storms in Northern Indiana burst pipes and damage roofs regularly; premiums in flood-prone areas rise 15 to 25 percent because weather events strike frequently and cause substantial losses. Without property coverage, a single winter event forces you to close indefinitely while you pay out of pocket for structural repairs, equipment replacement, and lost inventory. Your location risk directly influences both your premium and the endorsements you need. Region-specific endorsements address seasonal threats that standard policies leave uncovered, and an independent agency can compare multiple carriers to identify gaps before a loss exposes them.

Theft and Vandalism Drain Your Operation Silently

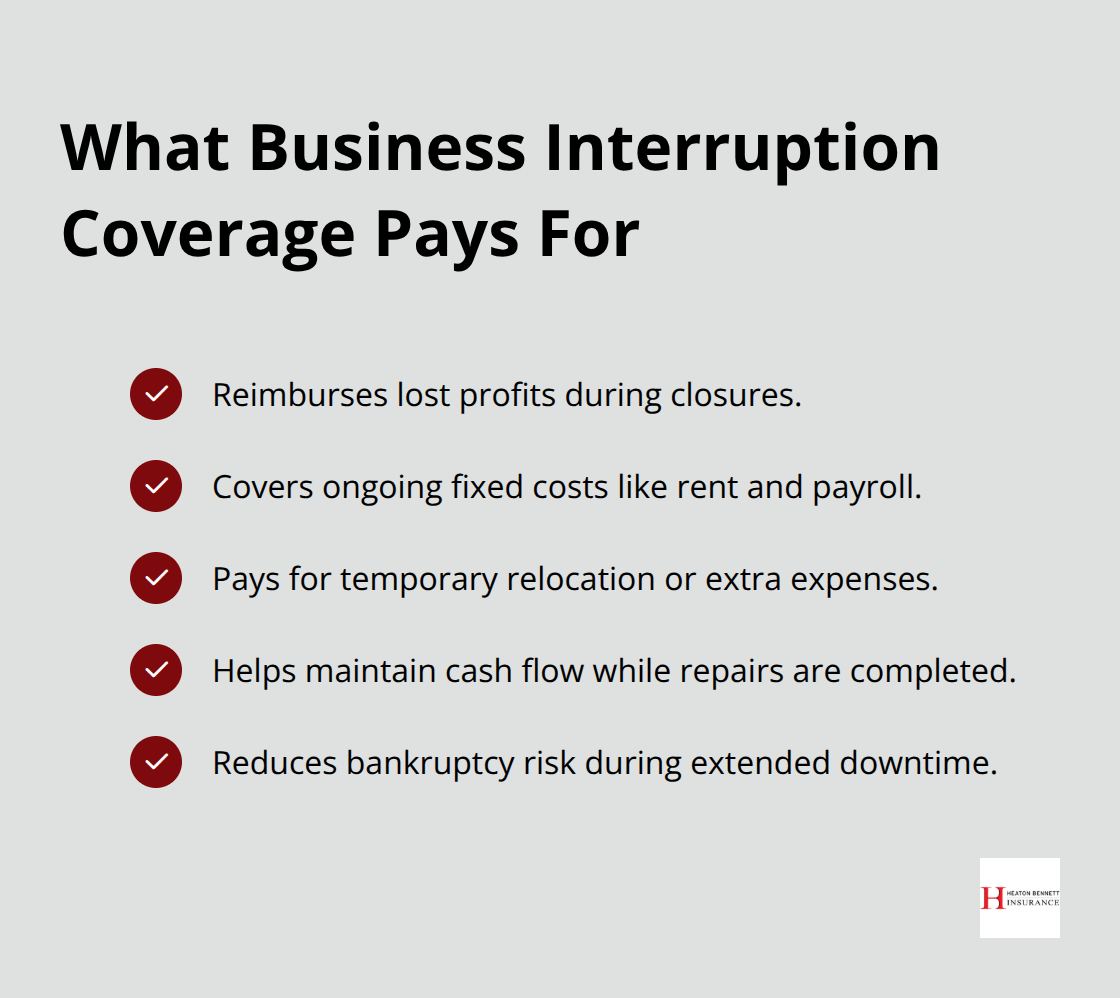

Theft and vandalism drain restaurants silently, but property insurance responds when they strike. Employee theft costs the restaurant industry billions annually, and property coverage protects against dishonest acts that your other policies may exclude. A break-in that damages your storefront, steals your POS system, or destroys inventory leaves you both short on equipment and unable to serve customers until repairs finish. Business interruption coverage becomes your lifeline during forced closures from fire, storm damage, or equipment failure. This coverage reimburses lost profits and ongoing fixed costs like rent and payroll while your restaurant sits dark, and it covers temporary relocation costs or extra expenses to keep operating from another location. A 12 to 36-month business interruption policy costs between $750 and $10,000 annually depending on your revenue, but it prevents bankruptcy during the weeks or months your building remains unusable.

Temperature Failures and Spoilage Losses Require Specific Endorsements

Temperature control failures in refrigeration cause immediate spoilage; without a spoilage endorsement, you lose thousands in perishable inventory when a compressor fails or a power outage strikes your neighborhood. Off-premises power outage coverage specifically protects against utility failures beyond your control, and sewer backup endorsements cover interior damage when municipal systems fail. These endorsements cost little individually but stack into comprehensive protection that keeps your operation solvent through disasters. Water damage from burst pipes or flooding often falls outside standard property policies; you need separate endorsements or riders to cover water damage from external sources and prevent inventory loss that standard coverage excludes.

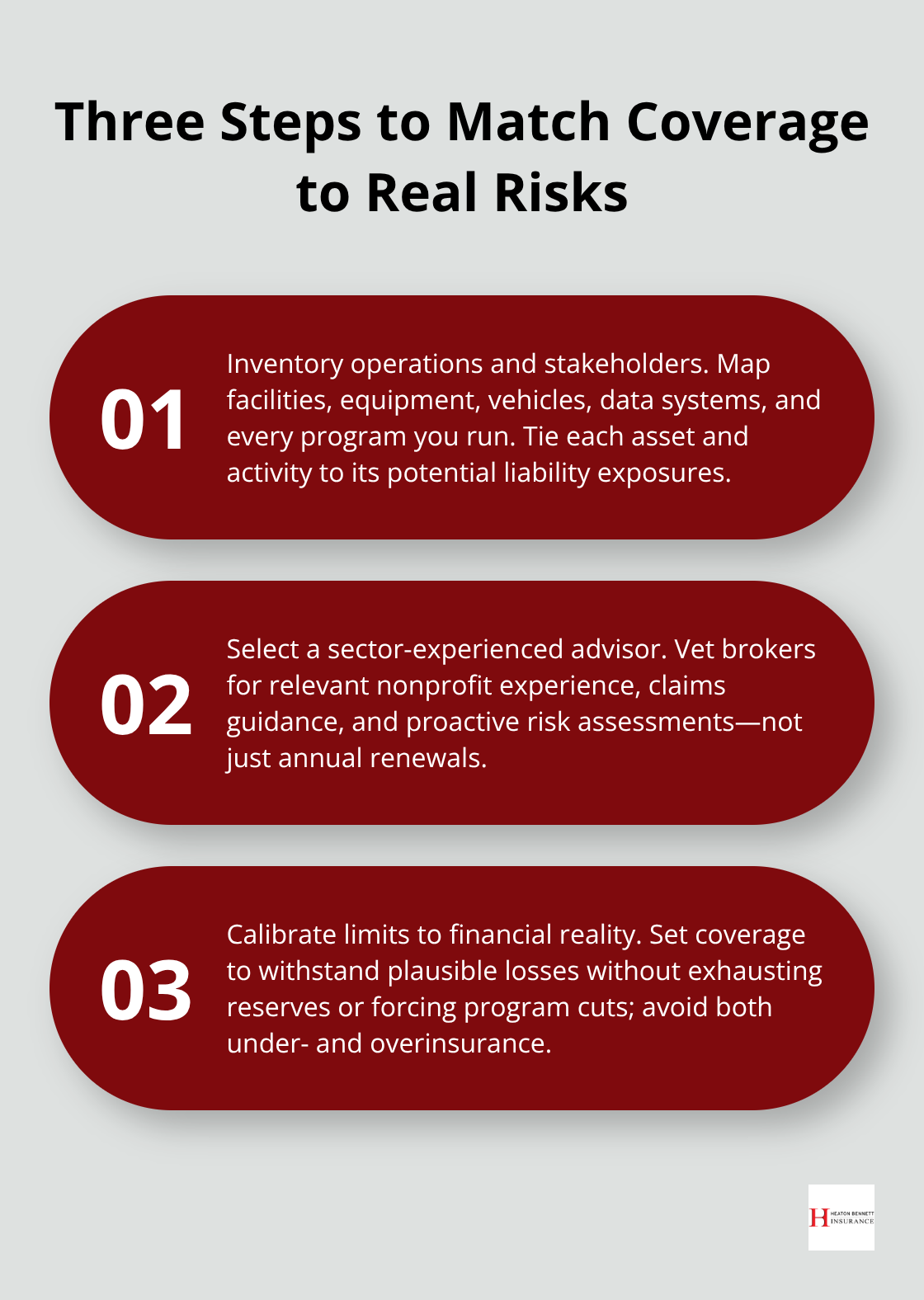

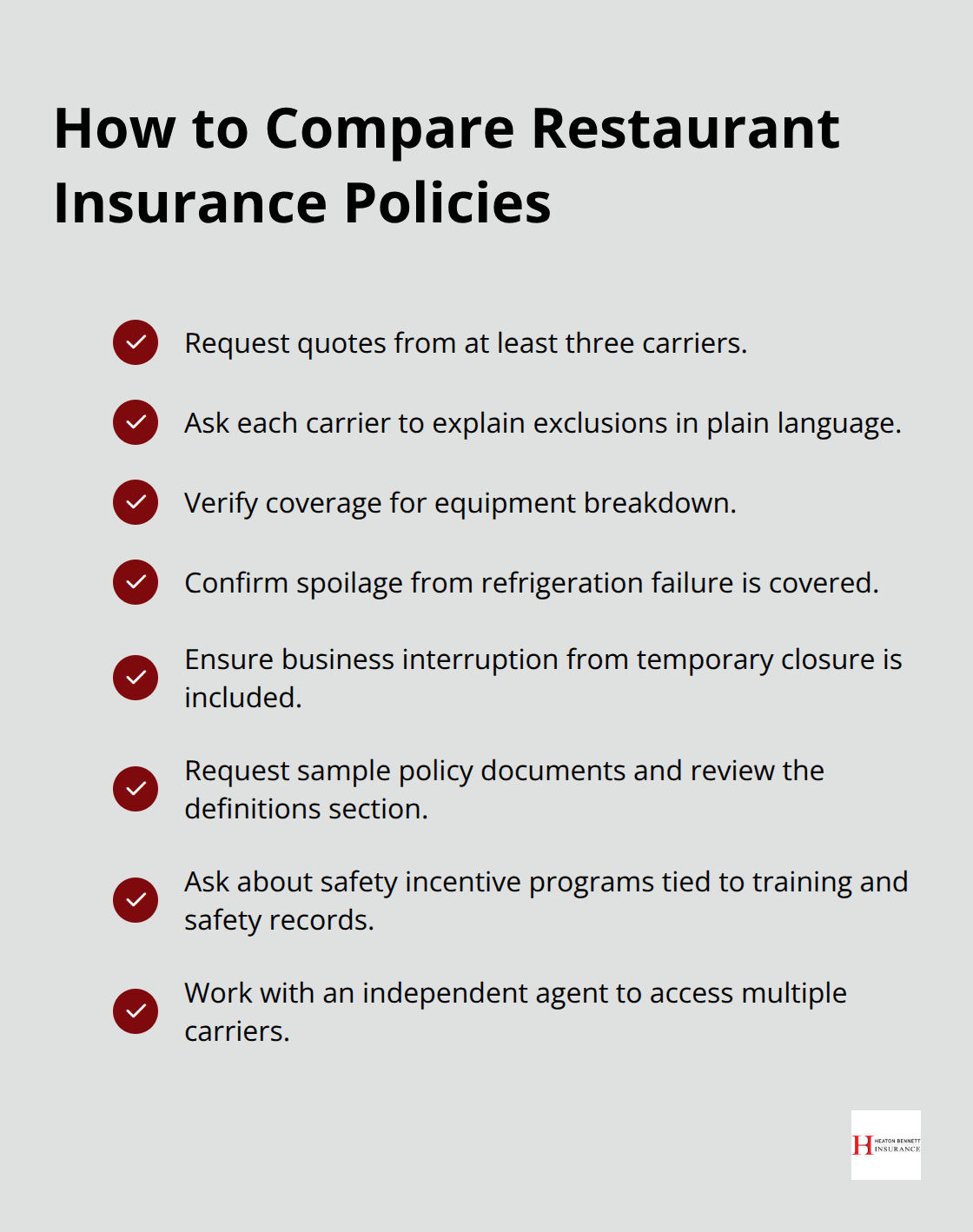

Your Next Step: Matching Coverage to Your Actual Risks

Your Northern Indiana restaurant faces unique seasonal risks that require region-specific endorsements beyond standard policies. An independent insurance agency compares multiple carriers to identify gaps in standard policies before a loss exposes them, and this comparison process reveals which endorsements your operation actually needs. Understanding your building’s replacement cost, equipment values, and inventory levels positions you to select limits that protect your operation when disaster strikes. The right coverage strategy starts with a detailed assessment of your specific business needs and the threats your location faces.

How to Match Coverage to Your Restaurant’s Real Costs

Document Every Asset and Its Replacement Price

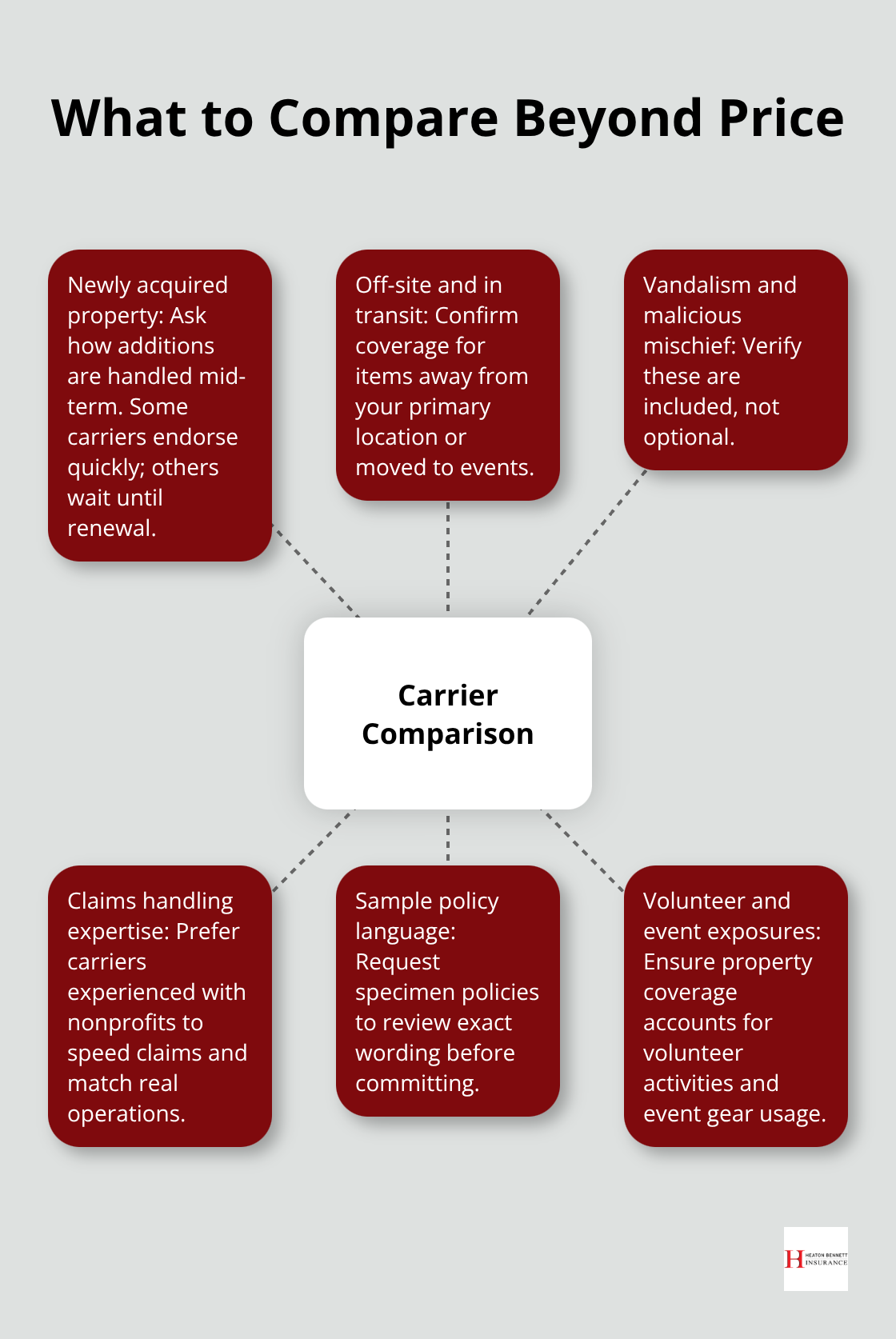

Walk your restaurant with a notebook or phone camera and photograph every asset: the six-burner range, walk-in cooler, hood system, refrigeration units, POS terminals, furniture, and smallwares. Request replacement-cost quotes from equipment suppliers for your major kitchen systems, then add 10 to 15 percent for installation and unforeseen upgrades. Most operators underestimate inventory value by 30 to 40 percent, so count your freezer stock, dry goods, beverages, and packaging at current wholesale prices, not what you paid months ago. For a 2,000-square-foot restaurant building, expect reconstruction costs between $300,000 and $500,000 at current labor and material rates. Match your coverage limits to actual replacement costs rather than a wishful guess that leaves you short.

Account for Tenant Improvements and Leased Spaces

If you lease, photograph and document every tenant improvement you installed, since your landlord’s policy covers only the building shell. Your landlord’s coverage protects the walls, roof, and structural systems, but your improvements-custom counters, built-in equipment, flooring upgrades, and specialized HVAC modifications-require your own protection. Standard property policies often exclude tenant improvements unless you add explicit coverage, leaving you to absorb replacement costs out of pocket. Request current quotes from contractors for the improvements you’ve made, then set your policy limits to match these actual costs. This step prevents the common mistake of assuming your landlord’s insurance covers your investments in the space.

Identify Location-Specific Endorsements Your Operation Needs

Northern Indiana restaurants need winter storm and burst-pipe coverage because seasonal weather patterns consistently cause these losses in your region, and premiums in flood-prone areas rise 15 to 25 percent based on historical data. Temperature control failures demand spoilage endorsements plus off-premises power outage coverage, because a compressor failure or utility outage can destroy thousands in perishable inventory that standard policies exclude.

Sewer backup coverage costs little but prevents interior damage when municipal systems fail. An independent insurance professional can compare multiple carriers and identify exactly which endorsements your operation needs, avoiding both gaps that leave you exposed and unnecessary coverage you do not need.

Select a Deductible You Can Actually Afford

Choose a deductible you can actually afford to pay out of pocket when a claim occurs, because a $2,500 deductible saves premium but creates real financial pressure if a fire or theft strikes. A lower deductible ($500 to $1,000) means higher monthly premiums but reduces your out-of-pocket exposure when losses happen. A higher deductible ($2,500 or more) cuts your premium costs but requires cash reserves to cover the gap between a loss and your insurance payment. Review this choice annually as your financial position and risk tolerance shift, and adjust your deductible if your cash reserves grow or your operation faces tighter margins.

Update Policy Limits After Changes to Your Operation

Review your policy limits annually after renovations, equipment purchases, or seasonal menu changes that increase your on-hand inventory value, because underinsurance during a major loss means you rebuild with depreciated cash values rather than full replacement costs. A new walk-in cooler, expanded seating area, or upgraded kitchen equipment raises your replacement-cost exposure and requires higher policy limits to match. Seasonal menu additions that require additional freezer stock or specialty equipment also increase your inventory value and demand coverage adjustments. An annual review prevents the gap between your actual assets and your policy limits from widening unnoticed, leaving you exposed to catastrophic underinsurance when disaster strikes.

Final Thoughts

Restaurant property insurance protects your building, equipment, and inventory from the threats that force you to close indefinitely. Your action plan starts with documenting every asset in your restaurant-photograph your six-burner range, walk-in cooler, hood system, and inventory, then request replacement-cost quotes from suppliers and contractors. Most operators underestimate stock value by 30 to 40 percent, so count everything at current wholesale prices rather than what you paid months ago.

Next, identify the endorsements your Northern Indiana location actually needs. Winter storms burst pipes and damage roofs regularly in your region, making seasonal coverage essential, and temperature control failures demand spoilage endorsements plus off-premises power outage protection because a compressor failure can destroy thousands in perishable inventory that standard policies exclude. Select a deductible you can afford to pay out of pocket, then review your policy limits annually after renovations, equipment purchases, or menu changes that increase your replacement-cost exposure. For a 2,000-square-foot building, expect reconstruction costs between $300,000 and $500,000, and match your policy limits to this reality rather than guessing.

We at Heaton Bennett Insurance understand that restaurant property insurance requires more than a generic business policy. Contact us at Heaton Bennett Insurance to compare multiple carriers and tailor solutions that match your specific location, assets, and seasonal risks.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.