What Does Commercial Property Insurance Cover?

Commercial property insurance is a vital safeguard for businesses, protecting their physical assets from unexpected events. At Heaton Bennett Insurance, we often encounter questions about what commercial property insurance covers.

This comprehensive guide will explore the key areas of protection, common exclusions, and additional coverage options available. We’ll help you understand how to tailor your policy to meet your specific business needs.

What Is Commercial Property Insurance?

Commercial property insurance protects a company’s physical assets from various risks and potential losses. This type of insurance covers buildings, inventory, equipment, tools, and more. Losses that can be covered range from fires to vandalism.

Who Needs Commercial Property Insurance?

Every business that owns or leases physical property should consider this coverage. This includes:

- Retailers

- Manufacturers

- Service providers

- Home-based businesses

A small boutique in downtown Austin needs protection for its inventory and store fixtures, while a large manufacturing plant requires coverage for its expensive machinery and warehouses.

Commercial vs. Residential Property Insurance

Commercial property insurance differs significantly from residential property insurance. Commercial policies offer:

- Higher coverage limits

- More complex coverage options

- Business interruption coverage (not typically found in residential policies)

For example, a standard homeowners policy might provide $250,000 in dwelling coverage, whereas a commercial policy for a small office building could easily exceed $1 million.

Tailoring Coverage to Your Business

Every business has unique needs for property insurance. A restaurant in Austin might need specialized coverage for expensive kitchen equipment, while a tech startup might prioritize protection for valuable computer systems and data servers.

The Importance of Comprehensive Coverage

Commercial property insurance should cover all aspects of a company’s physical property. This includes:

- Buildings and structures

- Equipment and machinery

- Inventory

- Outdoor fixtures and signage

- Employee personal property (in some cases)

A thorough assessment of your business assets (often called a “Security Snapshot” by insurance professionals) helps ensure that no aspect of a company’s physical property is overlooked when creating a comprehensive insurance plan.

As we move forward, we’ll explore the key coverage areas in commercial property insurance, providing a deeper understanding of how this essential protection safeguards your business assets.

What Does Commercial Property Insurance Protect?

Commercial property insurance forms the foundation of business protection, safeguarding physical assets against various risks. This coverage can determine whether a business recovers from disaster or faces financial ruin.

Building and Structure Protection

The core of commercial property insurance protects physical structures. This includes the main building, additions, and permanently installed fixtures. In 2023, the average cost to rebuild commercial properties increased by 14.3% (according to Marshall & Swift). This trend highlights the need to reassess coverage limits regularly to match current replacement costs.

Business Personal Property Coverage

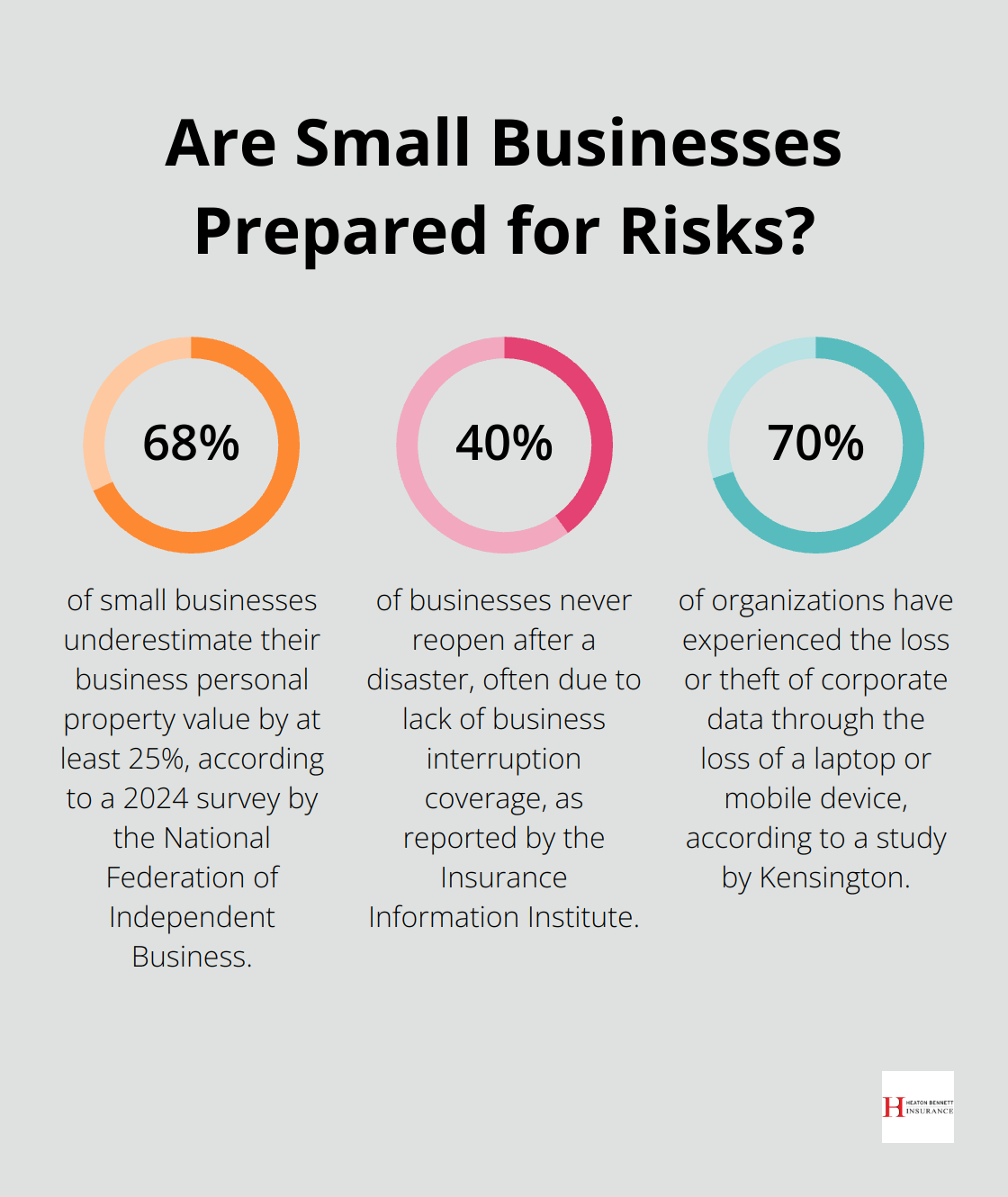

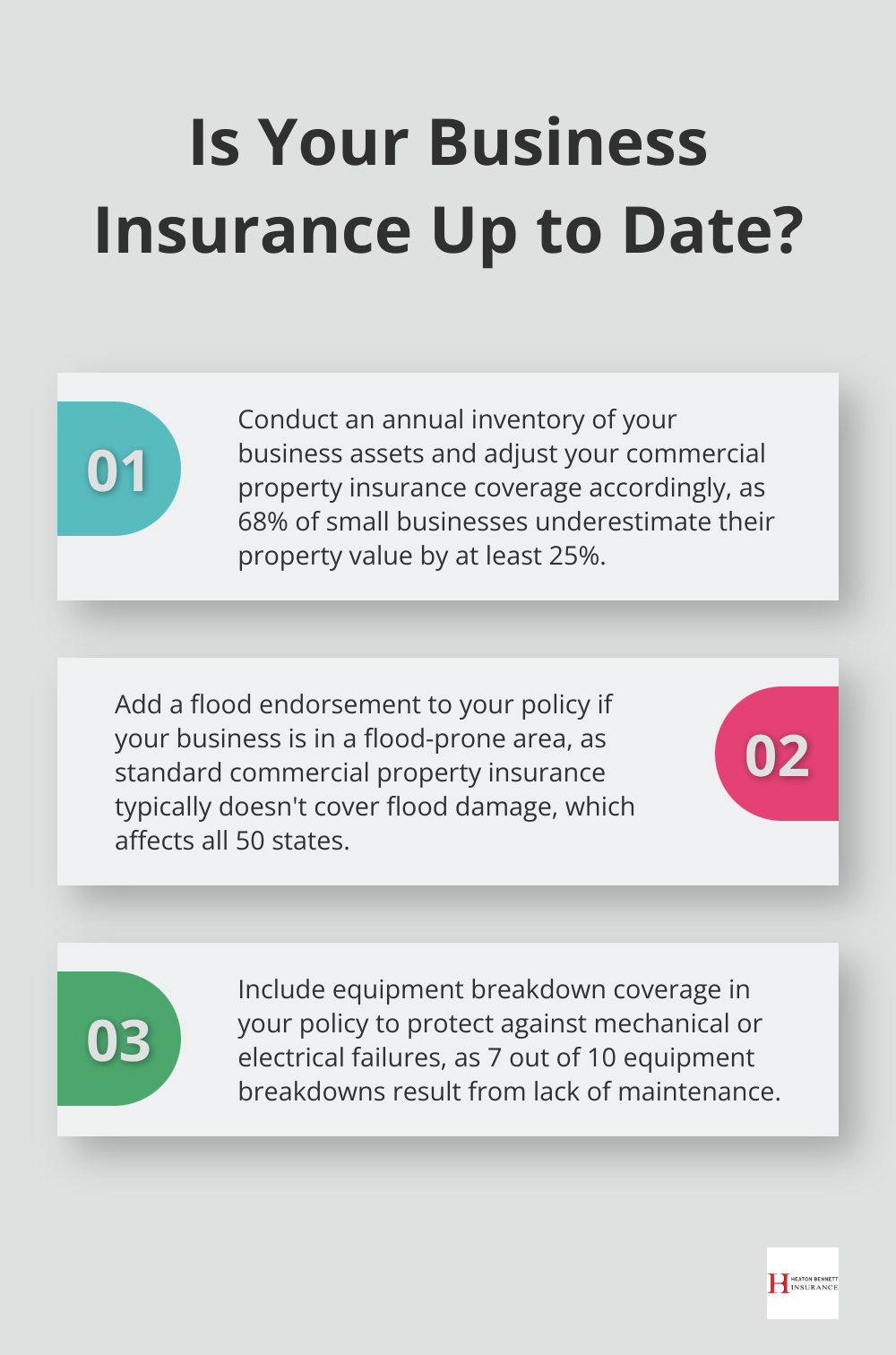

Your policy should extend beyond the building itself. It covers the contents that make your business operational, including furniture, equipment, inventory, and improvements to leased spaces. A 2024 survey by the National Federation of Independent Business revealed that 68% of small businesses underestimate their business personal property value by at least 25%. To avoid this issue, businesses should conduct annual inventories and adjust coverage accordingly.

Business Interruption Insurance

While not always included in standard policies, business interruption insurance compensates for lost income when your business can’t operate due to a covered event. The Insurance Information Institute reports that 40% of businesses never reopen after a disaster, often due to lack of this coverage. When selecting a policy, consider your specific industry and potential downtime scenarios to determine appropriate coverage limits.

Outdoor Property and Signage

External elements of your business require protection too. Many policies can cover outdoor signs, fences, and landscaping. These items face particular vulnerability to weather-related damage. The National Storm Damage Center estimates that severe weather causes billions in property damage annually, with a significant portion attributed to outdoor structures and signage.

Employee Personal Property

Coverage for employee personal property adds value to your policy. This protects items employees bring to work, such as laptops or mobile phones used for business purposes. A study by Kensington found that 70% of organizations have experienced the loss or theft of corporate data through the loss of a laptop or mobile device. Including this coverage can help maintain employee satisfaction and protect against potential liability issues.

The key to effective commercial property insurance lies in tailoring it to your specific needs. A comprehensive approach helps identify potential gaps in coverage before they become costly oversights. As we move forward, we’ll explore common exclusions and additional coverage options to further enhance your understanding of commercial property insurance.

What’s Not Covered and How to Fill the Gaps

Commercial property insurance protects your business assets, but it has limitations. Understanding these gaps proves essential for comprehensive protection. Let’s explore the common exclusions and ways to enhance your coverage.

Common Exclusions in Commercial Property Policies

Standard commercial property policies typically don’t cover damage from floods, earthquakes, or acts of war. FEMA reports that floods affect all 50 states, making them the most common natural disaster in the U.S. Yet, many business owners don’t realize their basic coverage excludes flood damage.

Wear and tear represents another significant exclusion. Gradual deterioration of property falls outside policy coverage, which emphasizes the need for regular maintenance. The Building Owners and Managers Association (BOMA) states that proactive maintenance can reduce unexpected breakdowns by up to 70%.

Certain types of valuable papers and records may also lack coverage under standard policies. This exclusion can cause problems in our data-driven age. The Ponemon Institute found that the average cost of a data breach in 2024 reached $4.35 million, highlighting the potential financial impact of this gap.

Bridging Coverage Gaps with Endorsements

Businesses can add endorsements or riders to their policies to address these exclusions. A flood endorsement can protect against water damage (especially important in flood-prone areas like parts of Austin, Texas).

Equipment breakdown coverage offers another valuable addition. It covers damages caused by mechanical or electrical breakdowns, which standard policies often exclude. The Hartford Steam Boiler Inspection and Insurance Company reports that 7 out of 10 equipment breakdowns result from lack of maintenance, underscoring this coverage’s importance.

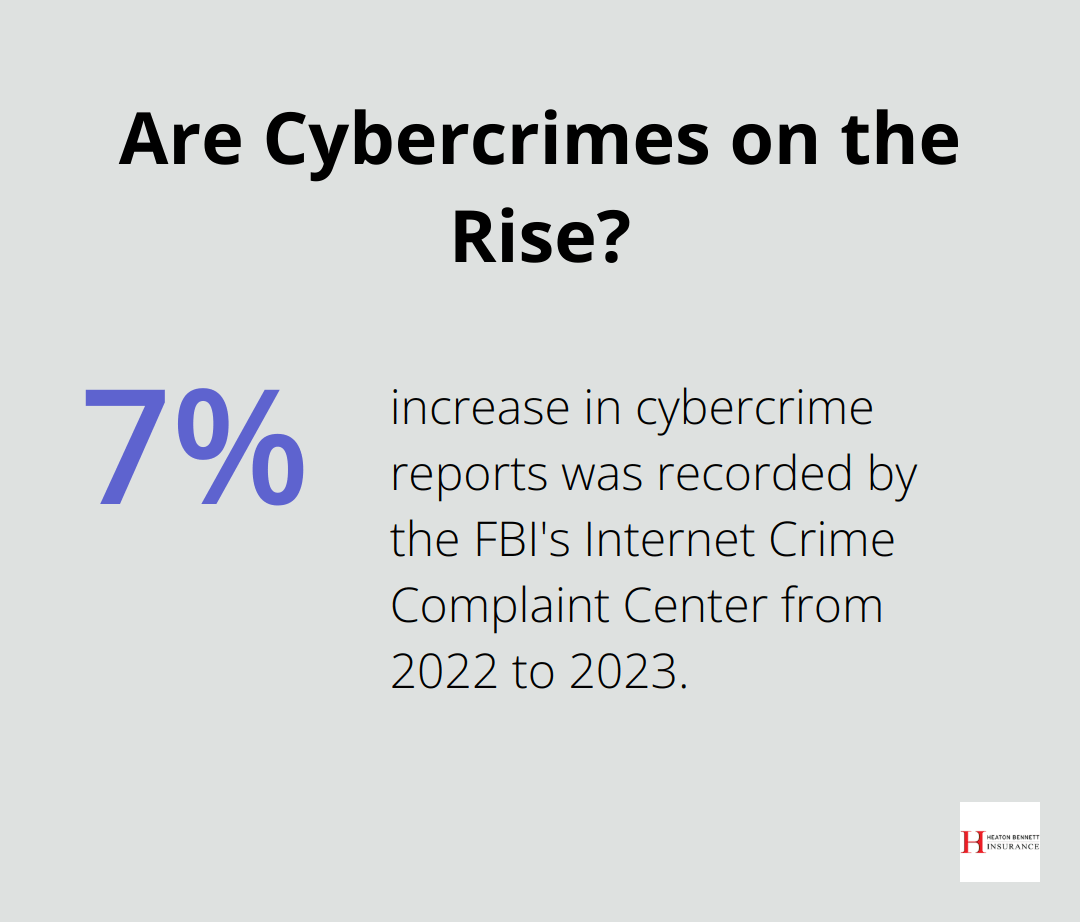

Cyber liability endorsements have gained popularity. With cyber attacks increasing, this coverage can protect against data breaches and other digital threats. The FBI’s Internet Crime Complaint Center recorded a 7% increase in cybercrime reports from 2022 to 2023, emphasizing the growing need for this protection.

The Importance of Regular Policy Reviews

Insurance needs change with your business. Regular policy reviews ensure your coverage keeps pace with changes in your operations, property values, and risk exposure. The Insurance Information Institute recommends reviewing your policy at least annually and after any significant business changes.

During these reviews, consider factors like inflation and market trends. Construction costs have risen significantly in recent years (the Turner Building Cost Index reported a 8.4% increase in 2024 alone). Failing to adjust your coverage limits accordingly could leave you underinsured when filing a claim.

Tailoring Your Coverage

Every business has unique risks and needs. Try to work with an insurance professional who can conduct a thorough assessment of your specific situation. This proactive approach helps businesses stay ahead of evolving risks and ensures they’re not caught off guard by exclusions when they need their insurance most.

Understanding the nuances of commercial property insurance, including its limitations and available enhancements, forms a key part of building a robust risk management strategy. Addressing these aspects allows businesses to create a safety net that truly protects their assets and operations.

Final Thoughts

Commercial property insurance protects businesses from unforeseen events that could damage their physical assets. This coverage extends beyond buildings to include business personal property, outdoor fixtures, and employee belongings. It also provides financial support through business interruption coverage when disasters occur.

Every business owner must understand what commercial property insurance covers. Regular policy reviews and updates ensure that coverage evolves with the business, addressing new risks and accounting for changes in property values. Additional endorsements or riders can bridge gaps in standard policies, providing more comprehensive protection against a wider range of potential threats.

At Heaton Bennett Insurance, we help businesses find the right commercial property insurance cover. Our team assesses your specific needs to create a tailored insurance plan. We offer flexible solutions that provide robust protection without tying you to a single provider (thanks to our access to multiple carriers).