How to Choose the Best Business Insurance for Retailers

Retail businesses face unique risks that can devastate operations without proper protection. From customer slip-and-fall accidents to inventory theft, the threats are real and costly.

We at Heaton Bennett Insurance understand that selecting the right business insurance for retailers requires careful consideration of coverage types, limits, and costs. The wrong choice can leave your business vulnerable to financial ruin.

Which Insurance Types Do Retailers Need Most

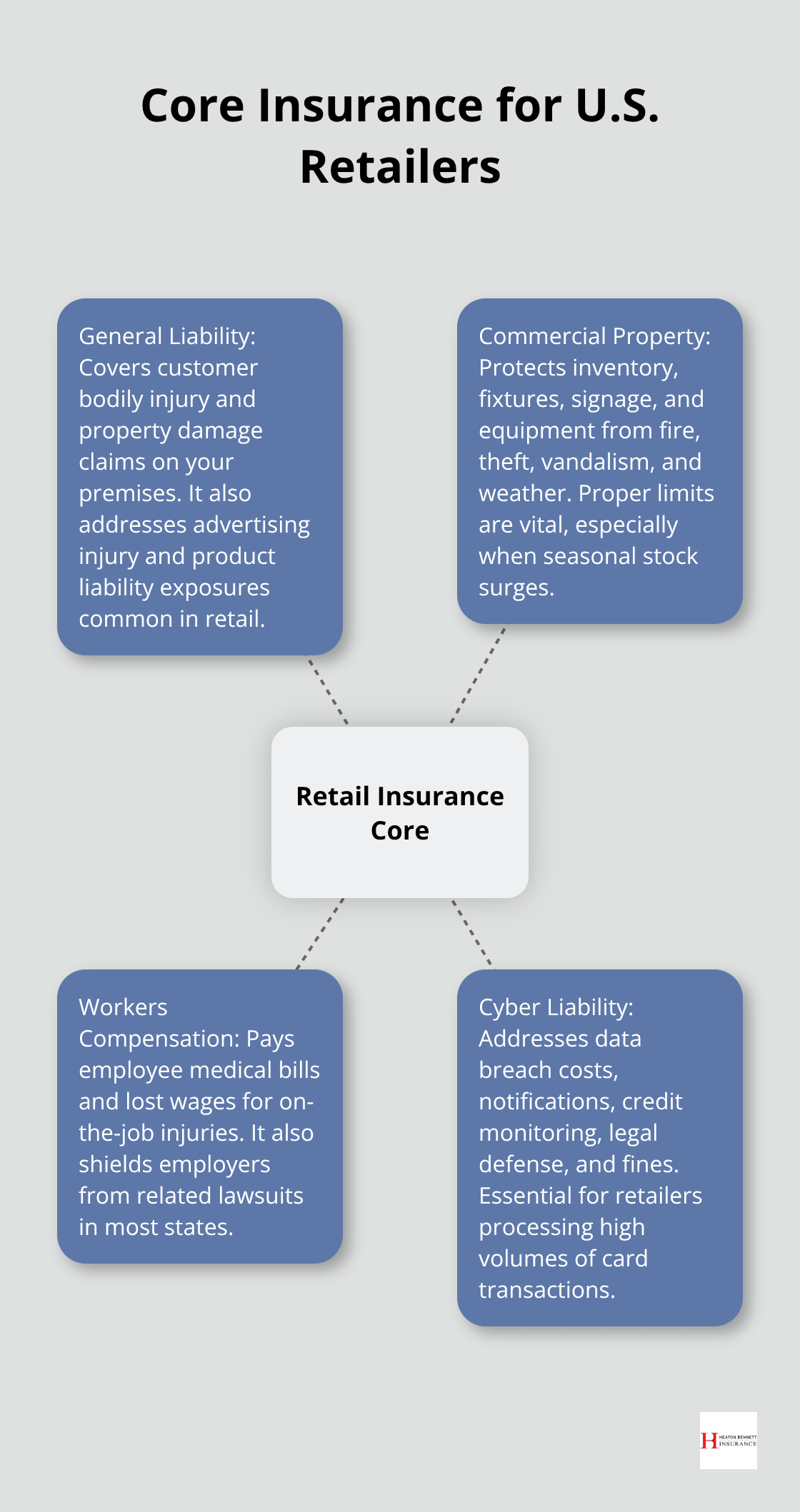

General Liability Insurance Protects Against Customer Claims

General liability insurance forms the foundation of retail protection and covers bodily injury and property damage claims that occur on your premises. The Insurance Information Institute reports that slip-and-fall accidents account for over 1 million emergency room visits annually, with retail establishments facing average settlement costs between $15,000 to $45,000 per incident.

This coverage extends beyond physical injuries to include advertising injury claims and product liability issues. Retailers who operate in high-traffic areas face significantly higher exposure, which makes this coverage non-negotiable rather than optional.

Commercial Property Insurance Safeguards Physical Assets

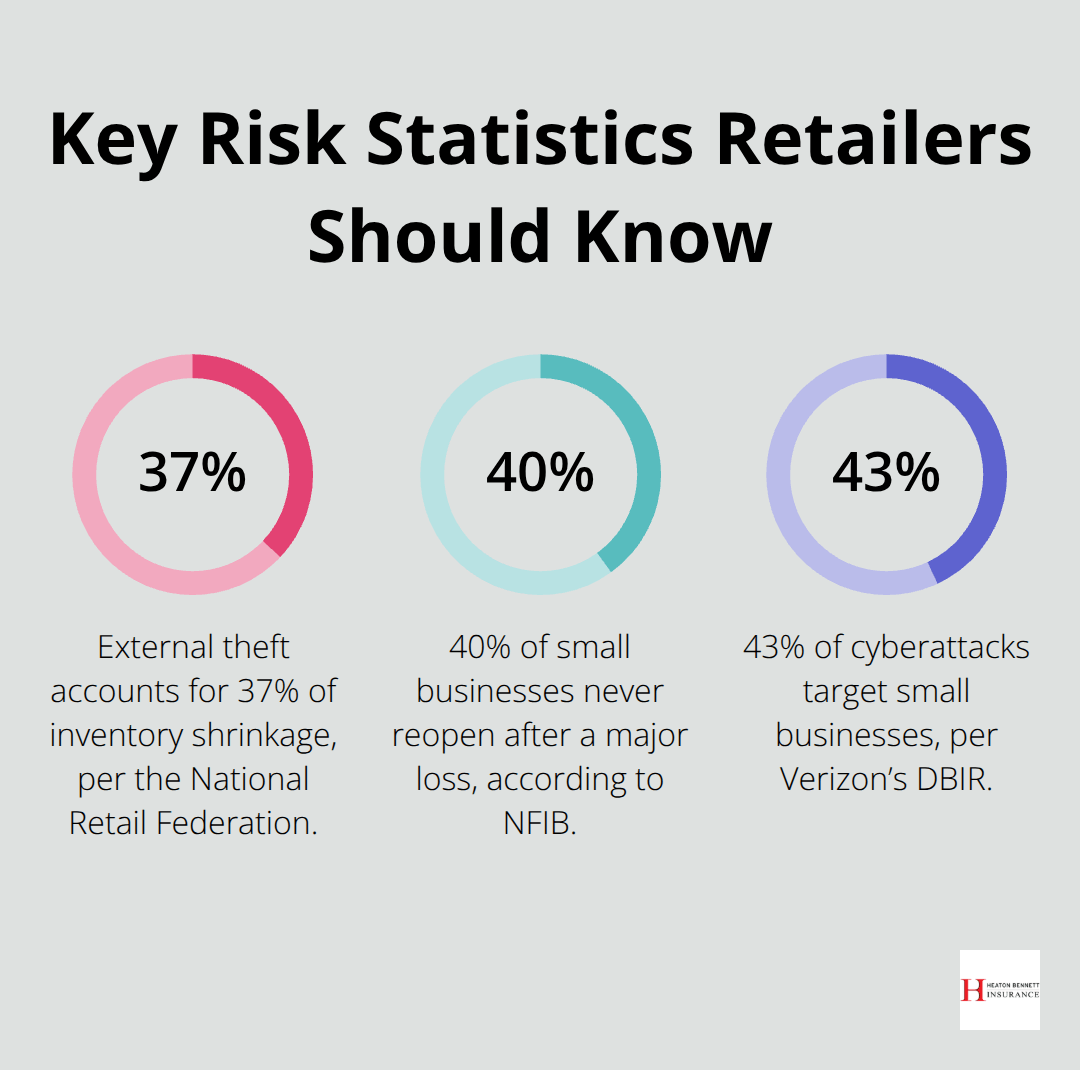

Commercial property insurance protects your inventory, equipment, and physical location from fire, theft, vandalism, and weather damage. The National Retail Federation’s 2023 security survey revealed that inventory shrinkage cost retailers $112.1 billion, with external theft representing 37% of losses.

This insurance covers not just merchandise but also fixtures, signage, and specialized equipment like point-of-sale systems. Seasonal retailers face particular challenges, as holiday inventory can represent 40-60% of annual stock value (making accurate coverage limits essential for survival).

Workers Compensation Insurance Covers Employee Injuries

Workers compensation insurance provides mandatory coverage for employee medical expenses and lost wages from workplace injuries. The Bureau of Labor Statistics reports retail workers experience 3.2 injuries per 100 full-time employees annually, with back injuries and cuts representing the most common claims.

This insurance also protects employers from lawsuits related to workplace injuries. Retailers with even one employee must carry this coverage in most states, with penalties for non-compliance reaching $10,000 in fines plus potential criminal charges for willful violations.

These three core insurance types provide the foundation, but smart retailers must also consider several key factors when they select their coverage levels and carriers. Working with a local insurance agency can provide professional guidance tailored to your specific retail operation.

How Do You Match Coverage to Your Retail Operation

Assess Your Business Size and Risk Profile

Retail insurance selection requires a systematic approach that begins with honest risk assessment and business size evaluation. Small retailers with under $500,000 in annual revenue need different coverage levels than established chains, yet both face similar core exposures. The National Federation of Independent Business found that 40% of small businesses never reopen after a major loss, which makes proper coverage selection a survival issue rather than just a cost consideration.

Your business size directly impacts premium calculations and coverage needs. Single-location retailers average $2,500-$4,500 annually for comprehensive coverage, while multi-location operations can expect $15,000-$25,000 based on NAIC data.

Set Appropriate Coverage Limits and Deductibles

Coverage limits should reflect your actual asset values plus potential lawsuit settlements, not arbitrary round numbers. Deductibles between $1,000-$5,000 typically provide the best premium-to-protection balance, though cash flow constraints may require higher deductibles.

Geographic location heavily influences rates, with urban retailers paying 40-60% more than rural counterparts due to higher claim frequencies and lawsuit settlements. This variation makes location-specific quotes essential for accurate budget planning.

Compare Multiple Insurance Carriers

Smart retailers obtain quotes from at least five carriers since premiums can vary by 200-300% for identical coverage. Independent agencies access multiple carriers simultaneously, which streamlines this comparison process while avoiding the bias of captive agents who represent single insurers.

The comparison process reveals significant differences in coverage terms, exclusions, and claim handling procedures that affect your long-term protection. These variations become apparent only through detailed side-by-side analysis of policy documents and carrier financial ratings.

Most retailers discover that the cheapest option often lacks adequate protection, while the most expensive doesn’t always provide superior coverage. This reality leads many business owners to question whether they can trust their current coverage to protect against the specific mistakes that destroy retail operations.

What Costly Insurance Mistakes Destroy Retail Businesses

Inventory Coverage Falls Short During Peak Seasons

Retailers consistently underestimate their inventory values, particularly during seasonal peaks when stock levels can triple normal amounts. The National Retail Federation data shows that holiday inventory represents 60-70% of annual purchases for many retailers, yet 45% maintain static coverage limits year-round.

This gap leaves businesses exposed to catastrophic losses during their most vulnerable periods. Smart retailers adjust their coverage quarterly to match actual inventory levels, with some implementing automatic seasonal increases that activate during peak months.

The cost difference between adequate and inadequate coverage becomes apparent only after a loss occurs. Insufficient limits can force permanent closure when retailers face their highest inventory exposure.

Payment Security Risks Remain Unprotected

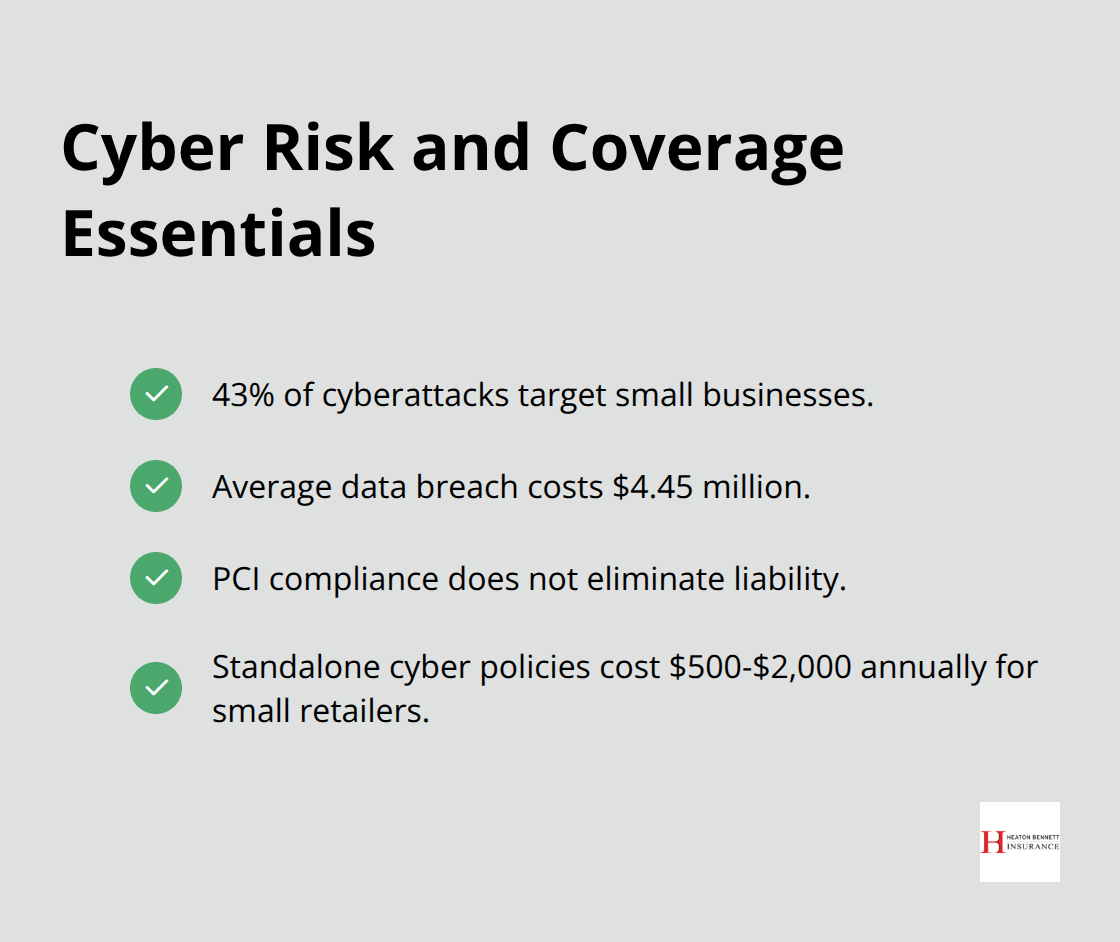

Cyber liability coverage represents the most overlooked protection in retail insurance, despite 43% of cyberattacks targeting small businesses according to Verizon’s Data Breach Investigations Report. Retailers process thousands of credit card transactions monthly, creating massive exposure to data breach costs that average $4.45 million per incident based on IBM Security research.

Traditional business insurance excludes cyber-related losses, leaving retailers responsible for notification costs, credit monitoring, legal fees, and regulatory fines. Payment processors require PCI compliance, but this doesn’t eliminate liability when breaches occur.

Standalone cyber policies cost $500-$2,000 annually for small retailers (making this protection financially accessible compared to potential losses).

Cheap Insurance Creates Expensive Problems

Selecting insurance based solely on price creates dangerous coverage gaps that become apparent only during claims. Policies with identical names often contain vastly different exclusions, coverage triggers, and claim procedures that affect payout amounts.

The cheapest options frequently exclude common retail exposures like employee theft, product recalls, or business interruption from utility failures. These exclusions can eliminate coverage precisely when retailers need protection most, transforming manageable incidents into business-ending disasters.

Price-focused decisions ignore the financial strength ratings of insurance carriers, which determine their ability to pay claims during widespread disasters. A carrier’s A.M. Best rating below “A-” signals potential payment delays that can cripple cash flow when retailers need funds most urgently. Companies make costly mistakes by choosing inadequate protection or paying for unnecessary coverage.

Final Thoughts

Successful retail operations require three essential insurance types: general liability coverage for customer injuries, commercial property protection for inventory and equipment, and workers compensation for employee safety. These policies form the foundation that protects against the most common and costly retail exposures. Smart retailers understand that proper coverage selection prevents financial disasters that destroy businesses.

The selection process demands careful assessment of your business size, risk profile, and coverage limits. Retailers who skip this analysis often face gaps during claims, when protection matters most. Price and coverage differences between carriers can save thousands annually while improving protection quality (making comparison shopping essential for smart business owners).

Common mistakes like underestimated seasonal inventory values, overlooked cyber liability coverage, and price-only decisions create devastating financial losses. The cheapest option frequently excludes critical retail exposures that can destroy businesses. We at Heaton Bennett Insurance help retailers find comprehensive business insurance for retailers through our personalized guidance and access to multiple carriers. Contact Heaton Bennett Insurance today to review your current coverage and identify gaps that could threaten your retail operation’s future success.