Nonprofit Director Insurance: Protecting Leadership and Mission

Nonprofit board members make decisions that shape organizations and communities. Yet many leaders operate without understanding the legal and financial risks they face personally.

Nonprofit director insurance protects you from claims that can drain personal assets and distract from your mission. We at Heaton Bennett Insurance help nonprofit leaders get the coverage they need to lead with confidence.

What Coverage Do Nonprofit Leaders Actually Need?

The Three Liability Exposures Every Nonprofit Faces

Nonprofit directors face three distinct liability exposures, and each demands separate protection. Directors and Officers Liability covers governance decisions-board votes, policy changes, strategic choices-where leaders face personal lawsuits for alleged negligence or breach of duty. This forms the foundation. Employment Practices Liability covers employment-related claims: discrimination, harassment, wrongful termination, retaliation. According to Insurance Business America, employment practices rank among the most frequent nonprofit liability exposures, making this coverage essential if your organization has staff. Fiduciary Liability protects financial oversight, particularly for ERISA-related decisions involving employee benefit plans. Many nonprofits bundle these three, but that approach creates a false sense of security. The real issue is that policy limits are shared across all three coverage types and between the organization and individual directors.

Why Shared Limits Create Hidden Gaps

A $1 million combined limit sounds substantial until defense costs mount in a contested claim. That limit depletes rapidly, leaving directors personally exposed. Defense costs alone can consume half the policy limit before any settlement or judgment occurs. This reality means your organization must understand exactly how much protection remains for individual directors after the organization claims its share. High-net-worth directors face particular risk because their personal assets become targets once policy limits exhaust.

Assess Your Organization’s Actual Risk Profile

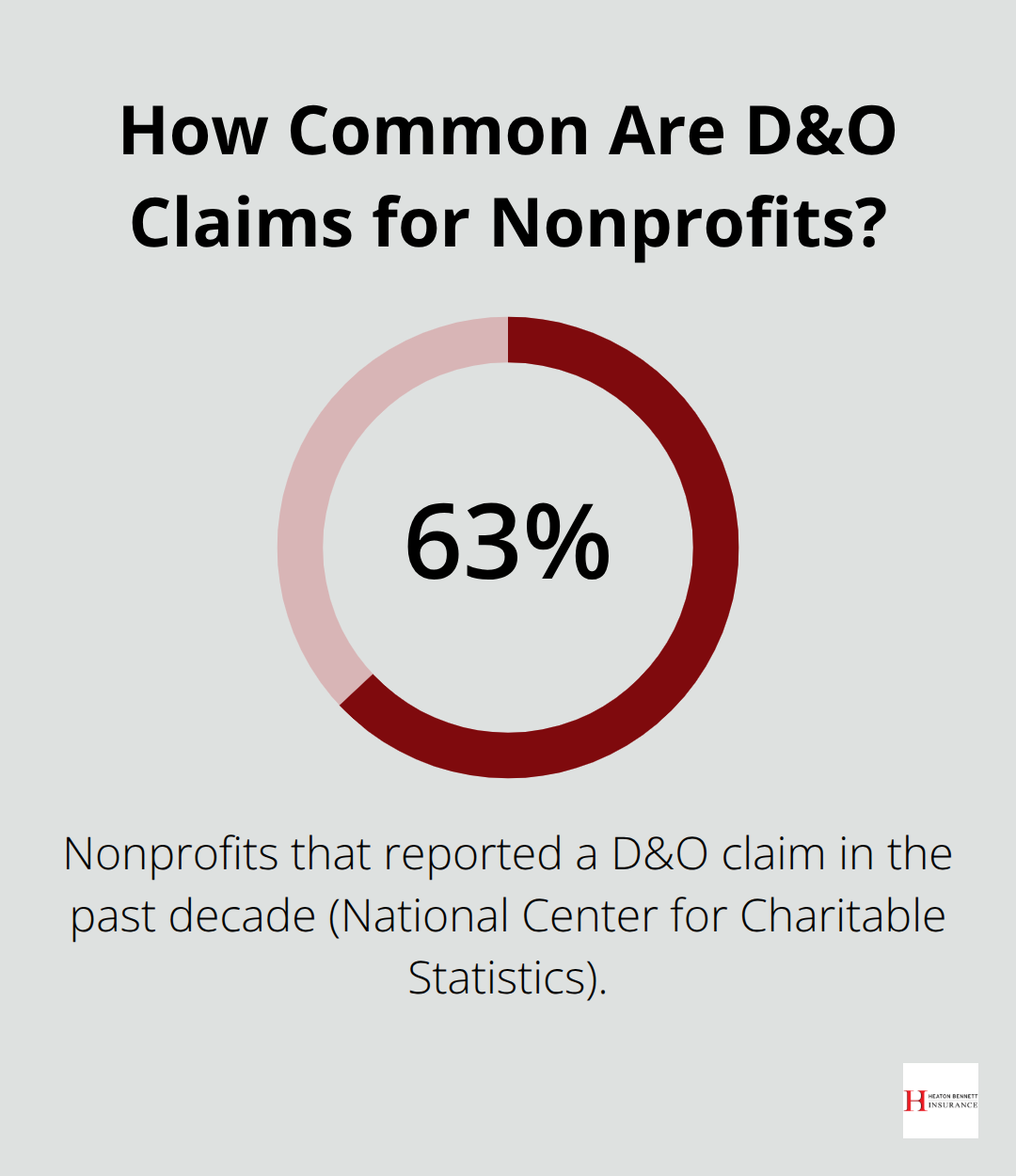

Start with honest assessment: How many employees do you have? Do you manage retirement or health plans? Have you faced employment disputes in the past five years? The answers determine which coverages matter most. A small volunteer-led nonprofit with no staff has different priorities than a mid-sized social service agency with 30 employees and a 403(b) plan. According to the National Center for Charitable Statistics, there are over 1.5 million nonprofits in the U.S., yet about 63% reported a D&O claim in the past decade-higher than the for-profit sector. That statistic means your organization is statistically more likely to face a claim than you might assume.

Coverage Limits and Deductibles Shape Your Real Protection

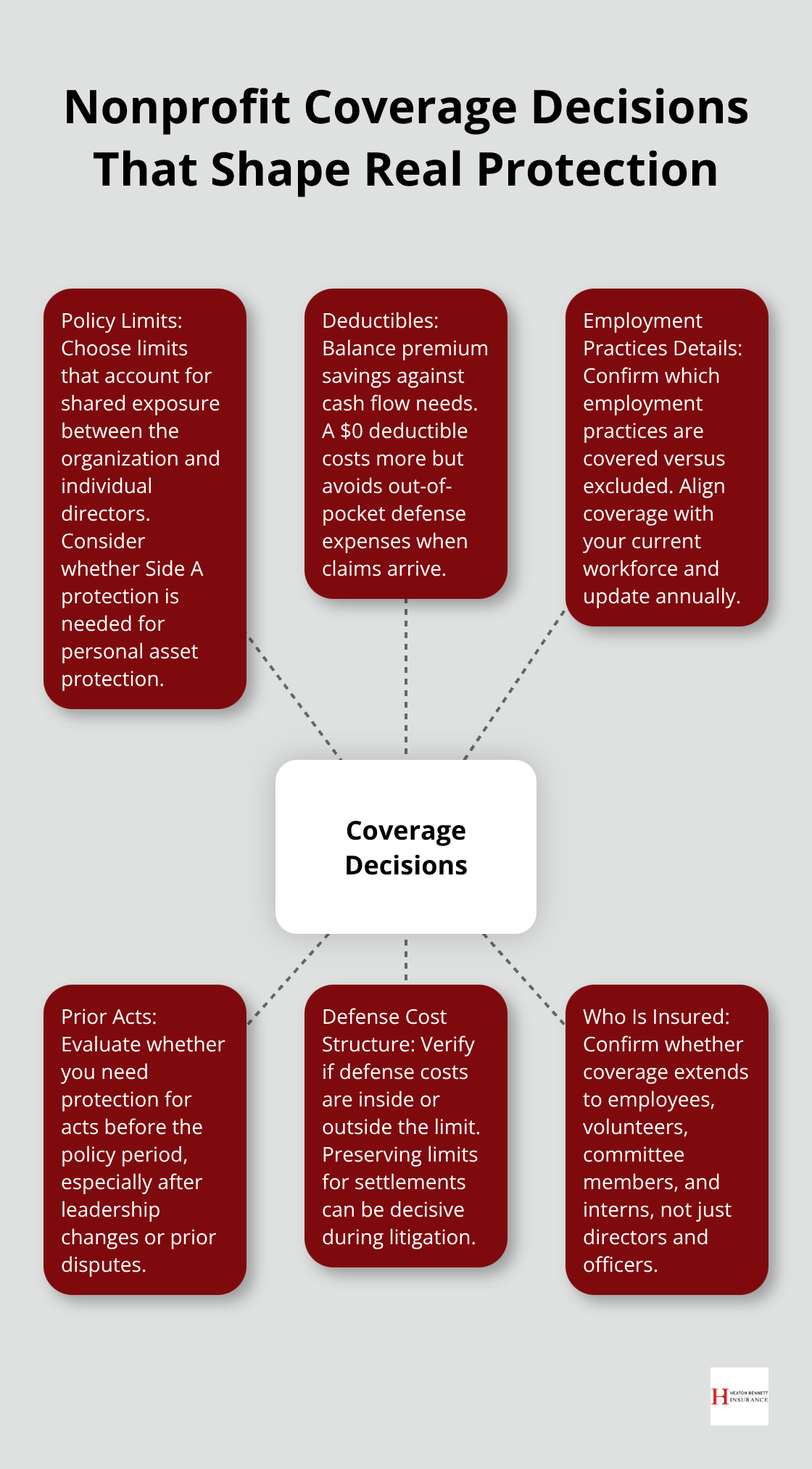

Coverage limits matter enormously. Many nonprofits start at $1 million, but high-net-worth directors should ask whether that limit-shared with the organization-adequately covers personal defense costs if allegations arise. Deductibles typically range from $0 to $10,000; a $0 deductible costs more but eliminates out-of-pocket defense expenses when claims hit. Review what your policy actually excludes: prior acts, cyber incidents, or specific employment practices. Exclusions are where coverage fails when you need it most. Your policy document should clearly state which employment practices it covers and which it does not.

What Happens When You Face an Actual Claim

The gap between what nonprofit leaders think they have and what their policies actually cover often emerges only after a claim arrives. A director accused of discrimination discovers the policy excludes certain employment practices. Another leader learns that the organization’s indemnification agreement does not extend to personal defense costs. These gaps force directors to choose between personal bankruptcy and fighting claims without legal representation. The solution is not to hope claims never happen-the statistics show they do-but to understand your coverage now, before allegations surface.

What Claims Actually Hit Nonprofit Boards

Governance Decisions Trigger Real Lawsuits

Nonprofit board decisions spark real lawsuits, and they arrive faster than most leaders expect. According to Insurance Business America, mismanagement of funds ranks as a major liability exposure for nonprofits, yet many directors underestimate how quickly governance decisions become legal disputes. A board votes to restructure programs without adequate stakeholder consultation, and a major donor sues for breach of fiduciary duty. Another board fails to properly vet a new executive director who later embezzles funds, and state regulators investigate board oversight. These scenarios happen regularly, not hypothetically.

The Volunteer Protection Act Falls Short

The Volunteer Protection Act provides limited immunity for volunteers, but it does not shield directors or officers from personal liability, nor does it protect the organization itself. This gap means board members remain personally exposed even when acting in good faith. Financial mismanagement allegations particularly sting because they often involve multiple defendants-the organization, individual directors, and sometimes officers. Defense costs alone can reach $50,000 to $150,000 before any settlement occurs, and those costs come directly from the organization’s resources unless D&O insurance covers them.

Employment Disputes Escalate Rapidly in Nonprofit Settings

Employment disputes represent the second major liability vector, and they escalate faster in nonprofit environments where staff often wear multiple roles and reporting lines blur. A staff member claims discrimination based on race or gender, or alleges retaliation after reporting a compliance concern. A volunteer accuses a supervisor of harassment, and the organization faces both the original claim and potential regulatory investigation. Insurance Business America identifies employment practices as among the most frequent nonprofit liability exposures, yet many boards assume their D&O policy covers these claims automatically. It does not.

Employment Practices Liability Requires Separate Coverage

Employment Practices Liability must be purchased separately or as a bundled endorsement, and many nonprofits discover this gap only after a claim arrives. Disputes with employees and volunteers also trigger indirect costs-lost productivity, damaged reputation, difficulty recruiting future staff-that insurance cannot recover. What insurance does cover is the legal defense, settlements, and judgments that protect both the organization and individual directors from personal bankruptcy. The practical reality is that nonprofits with staff cannot operate safely without explicit employment practices coverage, and that coverage must be reviewed annually to match your actual workforce composition and risk exposure.

How Your Coverage Gaps Determine Your Next Steps

The gap between what nonprofit leaders think they have and what their policies actually cover often emerges only after a claim arrives. A director accused of discrimination discovers the policy excludes certain employment practices. Another leader learns that the organization’s indemnification agreement does not extend to personal defense costs. These gaps force directors to choose between personal financial ruin and fighting claims without legal representation. Understanding your actual coverage now-before allegations surface-determines whether your organization can respond effectively when claims hit.

Choosing the Right Coverage Limits for Your Nonprofit

Start With Your Organization’s Financial Reality

Start with your organization’s financial reality, not industry averages. A $1 million policy limit sounds adequate until you calculate actual exposure. If your nonprofit has 20 employees, manages a 403(b) retirement plan, and operates multiple programs, you face simultaneous risk across governance, employment, and fiduciary domains. That $1 million limit covers the organization and all directors combined, which means a single employment discrimination claim consuming $200,000 in defense costs leaves only $800,000 for all other exposures and individual director protection.

About 63% of nonprofits reported a D&O claim in the past decade, yet most started with insufficient limits that forced difficult choices between organizational defense and individual director protection. High-net-worth directors should push for $2 million to $3 million combined limits, with consideration of Side A coverage that protects individual directors above the organization’s policy.

Deductibles and Cash Flow Protection

Deductibles matter less than many boards assume. A $0 deductible costs 15% to 25% more in premium but eliminates out-of-pocket expenses when claims arrive, which protects cash flow during investigations.

A $5,000 or $10,000 deductible saves premium dollars but forces your organization to fund initial defense costs from operations.

Most nonprofits choose $2,500 to $5,000 as the practical middle ground, but organizations with weak cash reserves should prioritize the $0 deductible option. This choice directly impacts whether your organization can afford quality legal representation when claims hit.

Employment Practices Coverage Requires Explicit Detail

Request a detailed policy comparison that shows exactly which employment practices the policy covers and which it excludes. Discrimination and harassment claims typically receive coverage, but retaliation, wage and hour disputes, and wrongful termination exclusions vary significantly between carriers. Your policy document should explicitly list covered employment practices rather than using vague language about employment-related claims.

Your next step involves requesting loss runs and claims history from your current insurer, then sharing that information with competing carriers for accurate quotes. Carriers price nonprofits based on prior claims, employee count, revenue, and governance structure, so incomplete information produces inflated quotes.

Test Coverage Against Real Scenarios

When comparing policies, require carriers to address three specific scenarios relevant to your organization: a board member accused of misappropriating funds, a staff member filing a discrimination claim, and a volunteer alleging harassment by a supervisor. Ask how much of the policy limit each scenario would consume, whether defense costs are covered separately or deplete the limit, and what exclusions might apply. This exercise reveals gaps that generic policy summaries hide.

Nonprofit insurance policies also vary on who qualifies as an insured person. Some policies cover only directors and officers, while others extend to employees, volunteers, committee members, and even interns. If your organization relies heavily on volunteers or has significant staff involvement in governance, confirm that your policy covers these groups explicitly.

Prior Acts and Defense Cost Structure

Prior acts coverage deserves attention if your organization has changed leadership or faced past employment disputes. Prior acts coverage protects claims arising from acts committed before the policy period, which shields new directors from inheriting exposure for decisions made by predecessors. Standard policies exclude prior acts unless purchased as an endorsement with additional premium. For nonprofits with recent leadership transitions, prior acts coverage typically costs 10% to 20% more but prevents gaps in protection.

Finally, verify that your policy includes defense cost coverage that operates outside the policy limit, not as a deductible against it. Some carriers include defense costs within the limit, which means a $1 million policy that pays $300,000 in legal defense leaves only $700,000 for settlements and judgments. Other carriers pay defense costs separately, preserving the full limit for indemnification. This distinction determines whether your organization can afford quality legal representation when claims hit.

Final Thoughts

Nonprofit director insurance protects your leadership from claims that statistics show will likely arrive. About 63% of nonprofits reported a D&O claim in the past decade, yet most boards operate with coverage gaps they never understand until allegations surface and personal assets face risk. A single employment discrimination claim or governance dispute consumes months of leadership attention, damages your reputation with donors and staff, and drains operational resources that should fund your mission. The real protection starts when you request your current policy documents and loss runs from your existing carrier, then schedule a detailed review with an insurance professional who understands nonprofit exposures.

Test your coverage against realistic scenarios specific to your organization: a board member accused of misappropriating funds, an employment discrimination claim, a volunteer harassment allegation. Ask carriers directly how much of your policy limit each scenario would consume and what exclusions might apply. Most nonprofits discover their coverage is either inadequate or misaligned with their actual operations, which means your organization needs to assess whether your current limits, deductibles, and coverage types actually match your risk profile.

We at Heaton Bennett Insurance help nonprofit leaders understand protection that actually works. Contact Heaton Bennett Insurance to discuss how nonprofit director insurance can protect your leadership and mission.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.