How to Choose Business Insurance and Bonding Coverage

Business insurance and bonding protect your company from financial losses and legal requirements. Many business owners struggle to understand which coverage they actually need.

We at Heaton Bennett Insurance see companies make costly mistakes by choosing inadequate protection or paying for unnecessary coverage. The right combination of insurance and bonding safeguards your business while meeting contractual obligations.

What Makes Insurance Different From Bonding

Insurance transfers financial risk from your business to an insurance company, while bonds guarantee performance or financial responsibility to a third party. Insurance covers losses that happen to your business, but bonds protect others from your business’s failure to meet obligations.

The Insurance Information Institute reports that nearly 40% of small businesses face lawsuits annually. This statistic makes general liability insurance a necessity rather than an option. Workers compensation insurance costs average $936 per employee annually and remains mandatory in almost every state for businesses with employees.

Core Business Insurance Types You Need

General liability insurance protects against third-party injury claims and property damage. Most small businesses pay an average of $42 monthly for this coverage. Commercial property insurance covers buildings and equipment but excludes earthquake and flood damage from standard policies.

Professional liability insurance defends service providers against quality-related lawsuits. Accountants and consultants face the highest claim rates in this category. A Business Owner’s Policy combines general liability and commercial property coverage into one package, typically costing $57 monthly while providing better value than separate policies.

When Bonds Become Mandatory Requirements

Construction companies must secure performance bonds for projects that exceed $100,000 in most states. License bonds guarantee compliance with local regulations and range from one to five years in validity (depending on your business type and location).

Surety bonds cost up to 15% of coverage amounts annually. A $100,000 bond could cost $15,000 yearly under this pricing structure. Fidelity bonds protect against employee theft and fraudulent activities, and they become mandatory for businesses that handle client funds or sensitive financial data.

Your next step involves a thorough assessment of your specific business risks and exposures to determine which combination of insurance and bonds will provide adequate protection.

Which Risks Should Your Business Prioritize

Manufacturing businesses face injury claims 3.2 times more frequently than service companies according to the National Safety Council. Construction firms need commercial auto coverage for fleet vehicles and equipment floaters for expensive machinery. Technology companies require cyber liability insurance with coverage limits that start at $1 million due to data breach costs that average $4.88 million per incident (according to IBM Security).

Professional service firms like accountants and consultants need errors and omissions coverage with minimum limits of $1 million per claim and $3 million aggregate. Restaurants must secure product liability insurance since foodborne illness claims average $75,000 in settlements.

Asset Values Determine Coverage Amounts

Your coverage limits must reflect actual asset values rather than arbitrary amounts. Commercial property insurance should cover 100% of replacement costs for buildings plus contents at current market prices. Equipment schedules require annual updates since technology depreciates rapidly while specialized machinery often appreciates.

Business interruption coverage should equal 12 months of gross profits plus fixed expenses that continue during shutdowns. Professional liability limits should match your largest client contracts plus a 50% buffer for legal defense costs.

Workers Compensation Calculations Matter

Workers compensation must cover your highest-paid employees at full salary replacement since state minimums rarely provide adequate protection. Manufacturing workers face higher claim rates than office employees, which affects premium calculations significantly.

Construction workers require specialized coverage for high-risk activities like roofing and electrical work. Service industry employees need coverage for repetitive stress injuries that develop over time rather than sudden accidents.

Annual Reviews Prevent Coverage Gaps

Asset appraisals help maintain appropriate coverage levels as your business grows and equipment values change. Technology companies should review cyber coverage annually since breach costs continue to rise across all industries.

Professional service firms must adjust liability limits when they take on larger clients or expand service offerings. The next step involves understanding specific bond requirements that your industry and contracts demand.

Which Bond Type Does Your Business Actually Need

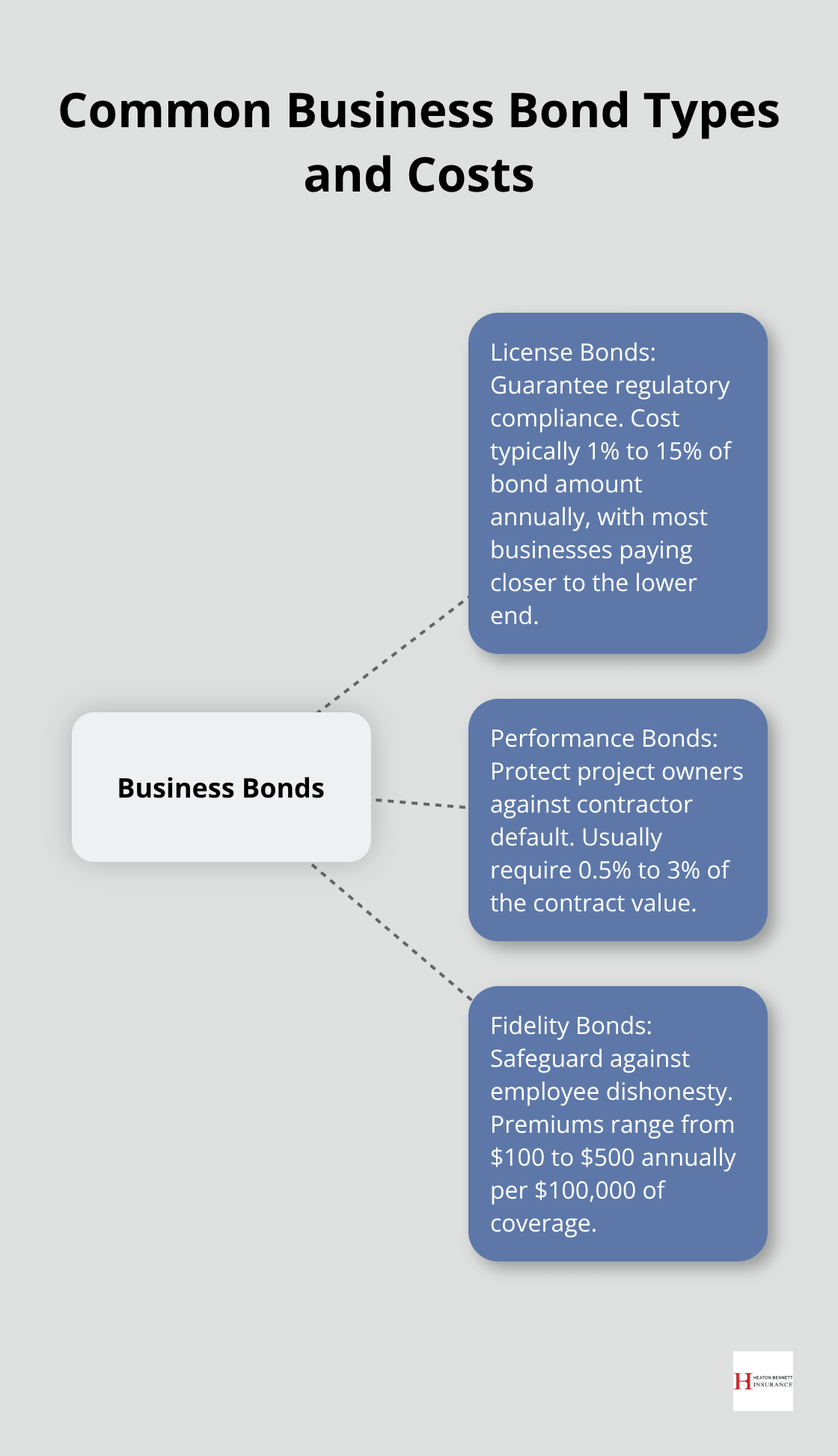

License bonds, performance bonds, and fidelity bonds serve different purposes and carry distinct cost structures that directly impact your bottom line. License bonds guarantee regulatory compliance and typically cost between 1% to 15% of the bond amount annually, with most businesses paying closer to the lower end for standard operations. Performance bonds protect project owners against contractor default and usually require 0.5% to 3% of the contract value, while fidelity bonds safeguard against employee dishonesty with premiums that range from $100 to $500 annually per $100,000 of coverage.

Performance Bond Requirements Hit Specific Thresholds

Federal construction projects that exceed $100,000 mandate performance bonds under the Miller Act, while state thresholds vary from $25,000 in some jurisdictions to $500,000 in others. Contractors must provide both performance and payment bonds simultaneously, which effectively doubles bond costs for large projects. Surety companies evaluate your business credit score, financial statements, and project history before they issue performance bonds, with approval rates that drop to 60% for companies with less than three years of operation history. Bond capacity typically equals 10 times your capital (meaning a company with $500,000 in capital can secure bonds up to $5 million in aggregate).

Fidelity Bonds Target Employee Access Levels

Businesses that handle client funds, process payments, or manage sensitive financial data need fidelity bonds regardless of employee count. Banks require fidelity coverage for any business that maintains commercial accounts above $250,000, while government contracts often mandate coverage equal to the largest single transaction your employees can access. Janitorial services need $50,000 minimum coverage per the Service Contractors Association International, while firms require coverage equal to their largest client relationship value plus six months of expenses.

License Bond Costs Vary by Industry

Professional service providers pay lower rates than construction companies due to reduced risk profiles. Real estate agents typically pay $100 to $300 annually for license bonds, while contractors face costs between $500 to $2,000 depending on their specialty and location. Auto dealers require bonds that range from $25,000 to $100,000 with annual premiums between $250 to $1,500 (based on credit scores and business history).

Final Thoughts

Smart business insurance and bonding decisions require accurate risk assessment and proper coverage calculations. Most businesses underestimate their actual exposure levels, which creates inadequate protection when claims occur. Your coverage limits must reflect current asset values, not outdated appraisals from previous years.

Independent insurance agents provide access to multiple carriers and can compare coverage options that single-carrier representatives cannot offer. We at Heaton Bennett Insurance help evaluate your specific risks and match you with appropriate carriers from our network. This approach saves time while providing comprehensive protection tailored to your business operations.

Business insurance and bonding requirements change as your company grows and takes on new contracts (especially in construction and professional services). Annual policy reviews prevent coverage gaps that could expose your business to significant financial losses. Professional guidance helps you navigate complex policy terms and state-specific requirements that vary across jurisdictions.