Contractor Policy Options: Finding the Right Coverage

Picking the wrong contractor insurance can leave your business exposed to costly claims and legal trouble. The right contractor policy options protect your assets, your team, and your bottom line.

At Heaton Bennett Insurance, we help contractors navigate coverage decisions that actually match their operations. This guide walks you through the types of coverage you need, how to compare costs, and what factors matter most when selecting your policy.

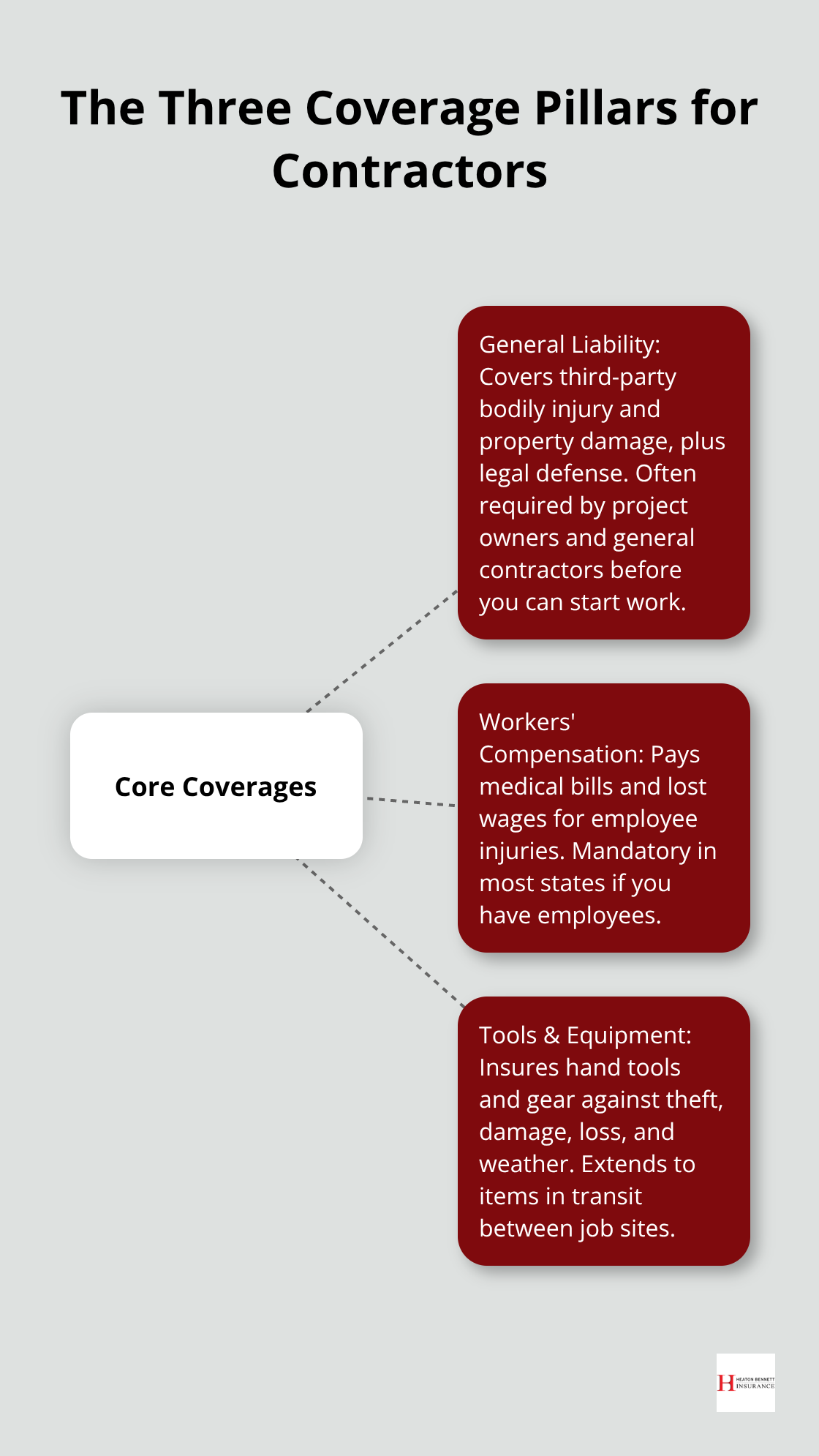

The Three Coverage Pillars Every Contractor Needs

General liability insurance protects your business when a third party claims you caused their bodily injury or property damage. This covers legal defense costs, medical expenses, and settlements up to your policy limit. The Hartford reports that general liability serves as the foundational coverage for contractors, addressing claims from clients, property owners, or bystanders harmed during your work. Most states don’t legally require it, but project owners and general contractors almost always demand proof before hiring you. Without it, a single accident-a worker accidentally damaging a client’s home or a passerby injured on your site-can bankrupt a small operation.

General liability protects against third-party claims

Policy limits typically range from $300,000 to $1 million, with most contractors carrying at least $500,000 in coverage. Higher limits cost more but provide meaningful protection; underinsuring leaves you paying claims out of pocket. A claim for bodily injury or property damage can easily exceed $100,000 when legal fees and medical costs combine. Your policy should match the scale of your projects and the assets you want to protect.

Workers’ compensation covers your team’s injuries

Workers’ compensation is mandatory in most states if you have employees, and it covers medical bills, wage replacement, rehabilitation, and disability benefits when someone gets hurt on the job. The Hartford notes that costs depend heavily on your payroll and the specific work you do; electricians and roofers pay significantly more than office-based contractors because injury risk is higher. Your premium is calculated as a percentage of gross payroll-typically ranging from 10 to 40 percent depending on trade and claims history. A contractor with five employees earning $50,000 annually might pay $2,500 to $10,000 per year. The real financial protection comes from avoiding claims that would otherwise drain cash reserves; a serious injury claim can easily exceed $50,000 in medical and wage replacement costs.

Tools and equipment require dedicated protection

Tools and equipment sitting on job sites or in your vehicle face constant theft and damage risks. Standard business property policies often exclude tools or limit coverage to just a few hundred dollars. Contractors tools and equipment insurance covers hand tools, power equipment, and specialty gear against theft, damage, loss, and weather-related incidents. For contractors carrying $20,000 to $100,000 in equipment value, this coverage typically costs $300 to $1,500 annually depending on deductible and risk level. The coverage also extends to tools in transit between job sites, which matters if you move equipment frequently. Without it, replacing a stolen generator, compressor, or saw set costs come directly from your profit margin.

These three pillars form your baseline protection, but your actual coverage needs depend on your specific business structure, the trades you perform, and the projects you take on. The next section walks you through how to assess your unique risks and compare the costs of different coverage options.

What Coverage Limits and Deductibles Mean for Your Bottom Line

Policy Limits Control Your Protection Level

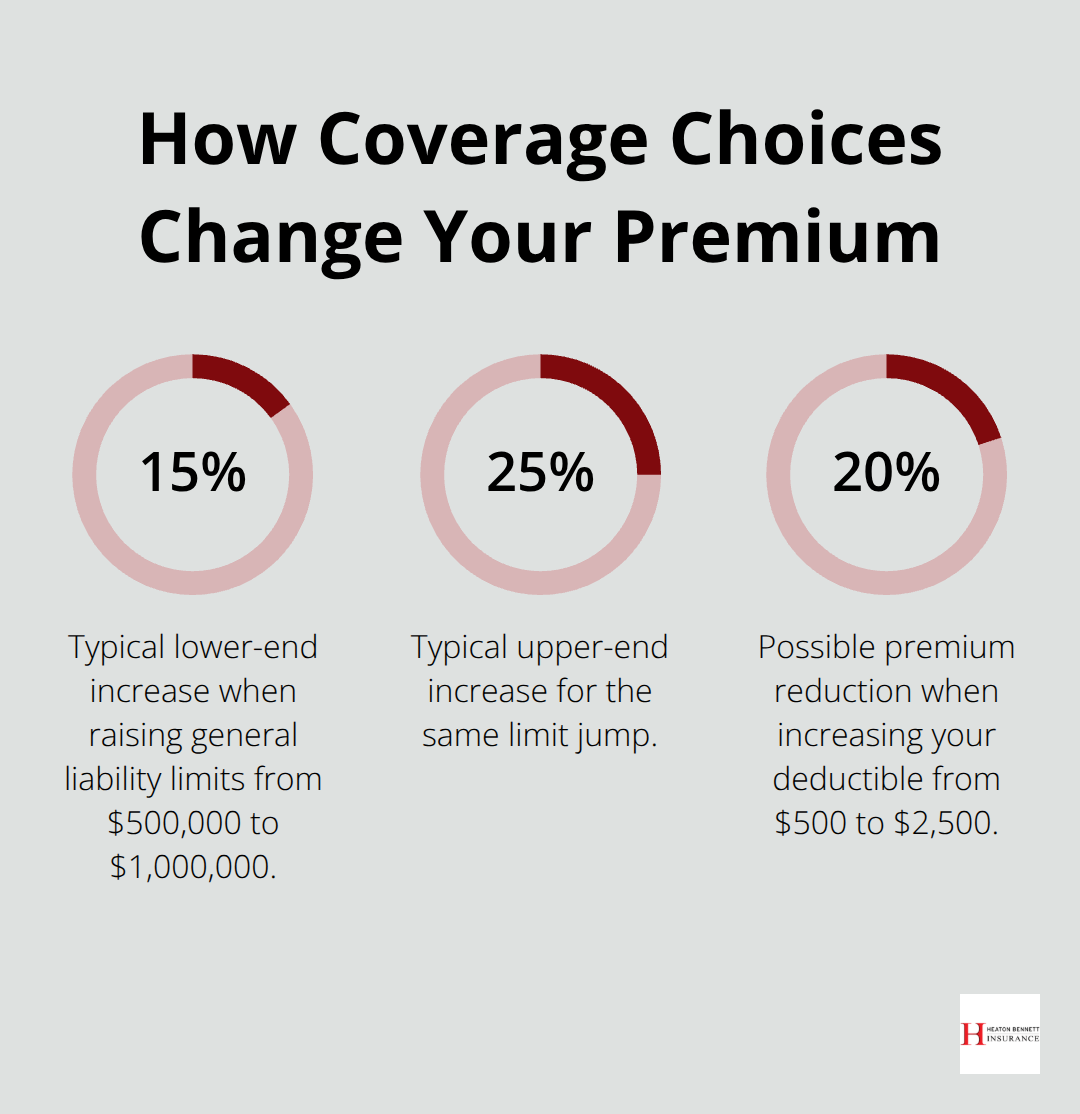

Your policy limits directly determine how much protection you actually have when a claim hits. Most contractors underestimate this relationship and end up either overpaying for coverage they don’t need or exposing themselves to massive out-of-pocket costs. General liability limits range from $300,000 to $2 million, but jumping from $500,000 to $1 million in coverage typically adds only 15 to 25 percent to your annual premium-a difference of $200 to $500 per year for most contractors. That modest increase can save you from a $500,000 claim that would otherwise wipe out years of profit. The Hartford’s data shows that contractors working on residential projects face average third-party claims between $50,000 and $150,000 when accidents occur, so a $500,000 limit makes far more sense than a $300,000 one unless you handle only small-scale work.

Your coverage should match the scale of your projects and the assets you want to protect.

Deductibles Shape Your Out-of-Pocket Costs

Your deductible works opposite to your policy limit: raising it from $500 to $2,500 might cut your premium by 20 percent, but you now pay the first $2,500 of every claim yourself. Policy structure directly impacts both your costs and protection level, making this choice critical to your financial planning. A $500 deductible makes far more sense than a $5,000 one for most residential contractors, since average claims fall between $50,000 and $150,000. Workers’ compensation has less flexibility-your payroll determines the base cost, and most states set minimum limits-but you can still control expenses by maintaining strict safety records and reducing injury claims over time. The real question is whether the premium savings justify the increased financial risk you accept.

Multiple Quotes Reveal Dramatic Price Differences

Three different insurers quoting the same contractor might offer $1,500, $2,100, and $2,800 annually for equivalent general liability and workers’ compensation, an 87 percent spread that makes comparison shopping non-negotiable. When requesting quotes, provide identical information to each carrier: your exact payroll, job types, past claims history, years in business, and the specific coverage limits you’re considering. Vague requests produce useless comparisons. Ask each insurer about available discounts-safety training completion, long-term customer loyalty, bundling auto and liability coverage, and maintaining claims-free records can each reduce premiums by 5 to 15 percent. The Hartford notes that bundling property and auto coverage together often yields around 12 percent savings.

Evaluate More Than Just Price

Don’t chase the lowest price alone; evaluate response time for certificate of insurance requests, claims handling speed, and whether the carrier has strong financial stability (an A.M. Best rating of A or better indicates the insurer can actually pay claims when you need them). Many contractors find that paying $200 more annually for faster claims service and responsive customer support prevents weeks of costly downtime after an accident. Your coverage decisions must align with your contract requirements; if a client demands $1 million in general liability with them named as additional insured, a $500,000 policy disqualifies you before you can even bid.

Align Coverage with Your Project Demands

The contracts you sign often dictate your minimum coverage levels and additional insured requirements. A general contractor on a commercial project might require all subcontractors to carry $2 million in general liability, while residential clients typically accept $500,000 to $1 million. Verify these requirements before you quote a job, since inadequate coverage can cost you the contract or leave you personally liable for damages. Your next step involves understanding which state laws and project-specific regulations actually mandate certain coverages and which ones remain optional based on your business structure.

Key Factors When Selecting Contractor Insurance

Read Your Policy Exclusions Before a Claim Arrives

Your existing policy likely has blind spots that remain hidden until a claim gets denied. Pull your current declarations page and read the exclusions section carefully-this is where carriers list what they won’t cover. General liability policies typically exclude coverage for employee injuries (that’s workers’ compensation territory), contractual liability you assume in client agreements, and pollution damage from hazardous materials. If you perform work involving environmental exposure, asbestos removal, or chemical handling, your standard general liability won’t protect you. Tools and equipment coverage often excludes items permanently attached to vehicles or left unattended in high-theft areas, meaning your expensive tool box bolted to your truck bed might not be covered if stolen.

The Hartford’s data shows that contractors discover these gaps most often when they file a claim and learn their coverage doesn’t apply.

List Your Work Activities and Match Them to Coverage

Create a comprehensive list of every type of work your business performs over the next year, then cross-reference it against your policy exclusions. If your work involves subcontractors, confirm your policy covers you for their actions and that you can add them as additional insureds. Many contractors carry general liability but lack professional liability coverage for design errors or specification mistakes that cause financial losses to clients-a critical gap if you estimate projects or handle client funds. This exercise takes two hours and prevents expensive claim denials later.

Understand State Requirements and Legal Obligations

State laws and project contracts create non-negotiable coverage requirements that vary dramatically by location and job type. Workers’ compensation is mandatory in every state except Texas if you have employees, but the specific benefit levels and premium structures differ significantly. Arizona, California, Nevada, Oregon, and Washington each have distinct requirements for contractor licensing and insurance minimums that affect your ability to legally operate and bid work. Federal contractors face additional scrutiny; the Small Business Administration tracks federal contracting performance through annual scorecards that show which agencies prioritize small business participation, and many federal projects mandate specific coverage types and limits as prerequisites to bidding.

Verify Baseline Requirements and Client Demands

Your state’s contractor licensing board publishes minimum insurance requirements, and these baseline limits are often insufficient for actual protection. A residential remodeling project in California might require $500,000 in general liability as a legal minimum, but the homeowner’s lender frequently demands $1 million coverage before approving the project. Contact your state’s licensing board and request the specific insurance requirements for your trade, then review the last three client contracts you signed to identify their additional demands. Many contractors miss that clients often require you to name them as additional insured on your policy, which costs nothing to add but disqualifies you from the job if you refuse.

Work with an Insurance Professional to Close Gaps

An independent insurance agent helps you decode state requirements and build policies that satisfy both legal minimums and actual client demands. This approach prevents bid rejections and coverage disputes down the road. Your agent can identify which optional coverages address your specific risks and which ones you can safely skip based on your actual operations.

Final Thoughts

The contractor policy options you select today determine whether your business survives a major claim or collapses under financial pressure. General liability, workers’ compensation, and tools and equipment coverage form your essential foundation, but the specific limits, deductibles, and additional coverages you choose must match your actual operations and client demands. A $500,000 general liability limit costs significantly less than $1 million coverage, yet that difference often amounts to only $200 to $500 annually-a modest investment that prevents catastrophic exposure on mid-sized projects.

Your coverage needs shift as your business grows and your project scope expands. A contractor handling small residential repairs faces different risks than one managing commercial construction with multiple subcontractors and environmental exposure. Reviewing your policy annually ensures your coverage keeps pace with these changes and that you haven’t accumulated exclusions that leave critical gaps (state requirements and client contracts also evolve, making regular audits non-negotiable for staying compliant and competitive).

Finding the right insurance partner matters as much as selecting the right coverage. You need someone who understands contractor operations, responds quickly to certificate of insurance requests, and handles claims efficiently when accidents happen. At Heaton Bennett Insurance, we work with contractors across multiple carriers to build tailored coverage that protects your assets without forcing you into unnecessary expenses. Contact us today to discuss your contractor insurance requirements and get quotes that reflect your real business operations.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.