Nonprofit Board Coverage: Protecting Directors and Officers

Nonprofit board members face real legal and financial risks that many organizations overlook. Lawsuits against directors and officers have increased, with claims ranging from financial mismanagement to employment disputes.

At Heaton Bennett Insurance, we believe nonprofit board coverage isn’t optional-it’s a necessity. This guide walks you through the risks your board faces and how to protect your leadership team with the right insurance.

Directors and Officers Liability Risks

Common Claims Against Nonprofit Board Members

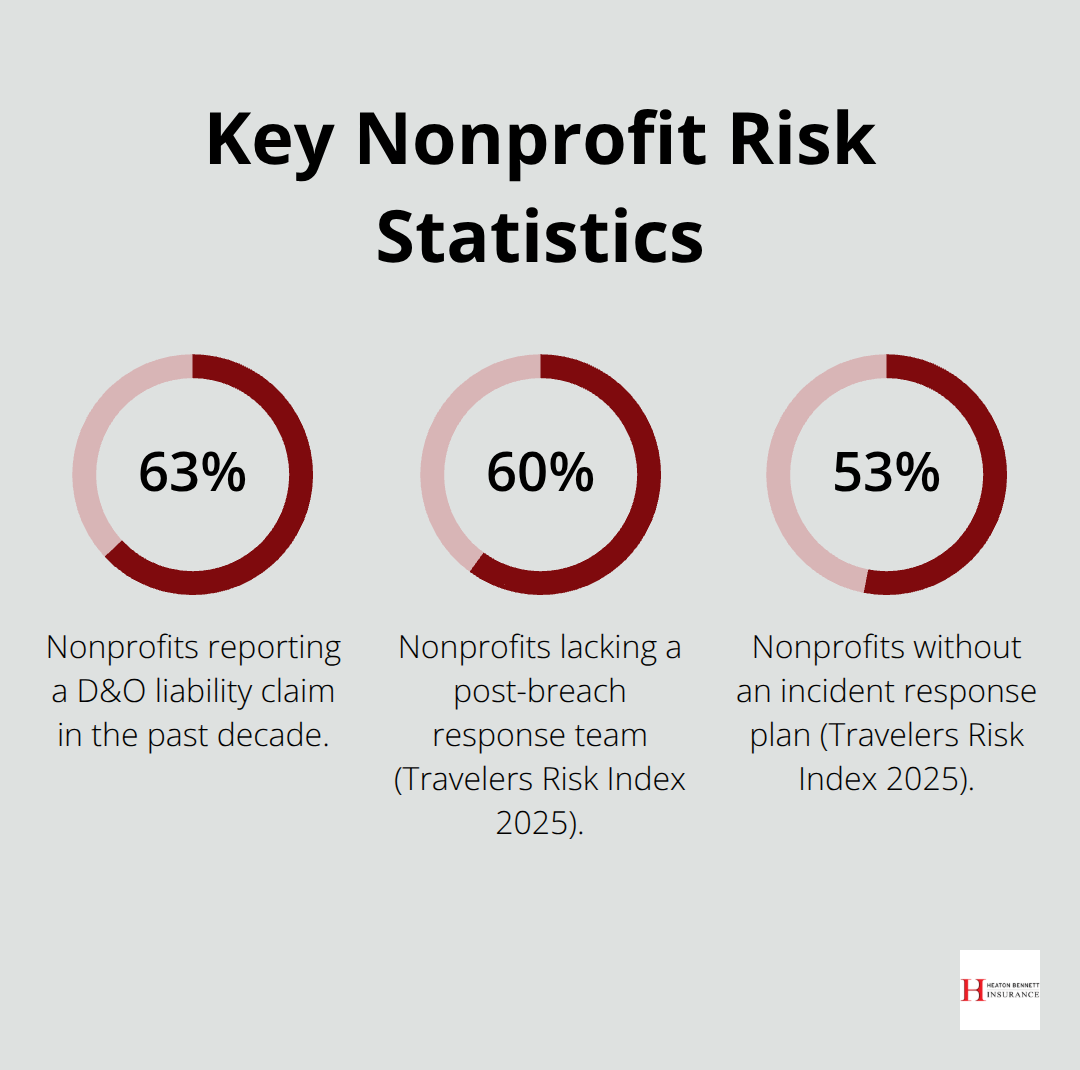

Nonprofit directors and officers face exposure from multiple directions, and the claims are far more concrete than many leaders realize. According to the National Center for Charitable Statistics, about 63% of nonprofits reported a D&O liability claim in the past decade-roughly twice the claim rate of the for-profit sector. The most common triggers are mismanaged funds and violations of donor restrictions, followed closely by fiduciary duty breaches tied to inadequate financial records or mishandling donations.

Employment practices allegations represent the largest share of actual D&O claim dollars. Accusations of discrimination, harassment, retaliation, and wrongful termination appear regularly across nonprofit boards. Compliance failures also generate lawsuits: boards that ignore bylaws or violate federal, state, or local regulations face legal action and removal. Conflicts of interest and self-dealing expose individual directors to personal liability.

How Claims Damage Your Organization

A single claim can drain an organization’s reserves through defense costs, settlements, and judgments. Beyond the financial hit, D&O incidents damage reputation, erode stakeholder trust, depress donations, and disrupt mission delivery. The Volunteer Protection Act provides only limited immunity and does not shield the organization or cover defense costs, making insurance essential rather than optional.

The Financial and Reputational Fallout

Defense costs alone can reach tens of thousands of dollars before any settlement or judgment occurs. Social inflation is driving higher litigation costs and jury awards, eroding the outdated perception that nonprofits are softer targets in court. A nonprofit with 1.5 million organizations operating across the United States and generating roughly 2.4 trillion dollars in revenue collectively represents enormous exposure for individual boards.

Without D&O protection, a single claim threatens the personal finances of directors and officers while straining organizational resources at the moment when leadership is most needed. Prevention through written policies, board training, and strong governance helps reduce risk, but even well-managed organizations face claims from donors, beneficiaries, regulators, state attorneys general, vendors, and current or former employees. The reality is that governance decisions, fundraising activities, budget oversight, and HR policies all create potential liability.

Why Insurance Matters More Than Prevention Alone

Securing proper D&O coverage with adequate limits and defense cost protection is not about pessimism-it is about protecting your board’s ability to lead and your organization’s ability to survive a legal challenge. The question is not whether your nonprofit will face a claim, but when. Understanding what D&O insurance actually covers helps you make informed decisions about the protection your board needs.

What D&O Insurance Actually Covers

Employment Practices Liability

D&O insurance protects your board in three distinct ways that most nonprofit leaders misunderstand. First, it covers employment practices liability-the single largest source of D&O claim dollars. When a staff member or volunteer alleges discrimination, harassment, retaliation, or wrongful termination, your organization faces defense costs that can exceed $50,000 before any settlement. D&O coverage pays these legal fees and any resulting judgment or settlement. This matters because employment claims are rising in frequency and severity for nonprofits, approaching levels seen in the for-profit sector.

Fiduciary Liability and Financial Protection

Second, D&O insurance covers fiduciary liability, which protects against claims of fraud, mismanagement, or improper financial oversight. This includes ERISA violations if your nonprofit sponsors an employee benefit plan. Fiduciary breaches tied to inadequate financial records or mishandled donations represent a primary claim source, and coverage typically includes an ERISA sublimit of $250,000 with an optional $500,000 increase available. Your board members gain protection when financial decisions come under scrutiny from donors, regulators, or beneficiaries.

Defense Costs Outside Policy Limits

Third, the policy covers defense costs separately in many cases, meaning legal fees are paid outside your policy limits rather than reducing your available coverage for settlements or judgments. This distinction matters enormously-your organization preserves its full coverage amount for actual liability while the insurer handles attorney fees and court costs independently.

Who the Policy Actually Protects

The scope of who is protected matters significantly. D&O coverage extends beyond just the executive director and board chair-it covers directors, trustees, officers, employees, volunteers, committee members, interns, and students-in-training. This broad member-insured definition is critical because claims often arise from mid-level staff decisions or volunteer actions. The policy also covers third-party harassment claims, protecting your organization when someone outside your nonprofit alleges harassment by your board or staff.

Additional Coverage Features That Matter

Prior Acts Coverage is available, meaning claims arising from events before your policy period can still be covered, subject to underwriting. This protects your board during transitions and leadership changes when historical decisions may surface as disputes. Deductible options range as low as $0, allowing you to eliminate out-of-pocket costs entirely if your organization prioritizes comprehensive protection. These three coverage pillars-employment practices, fiduciary protection, and defense costs-form the foundation of what D&O insurance provides. Evaluating whether your current policy truly protects your leadership team or leaves gaps when claims actually occur requires understanding exactly what your carrier will and will not pay for. The next step is assessing your specific organization’s risk profile to determine what limits and features your nonprofit actually needs.

What Size Coverage Limits Does Your Nonprofit Actually Need

Assess Your Organization’s Real Exposure

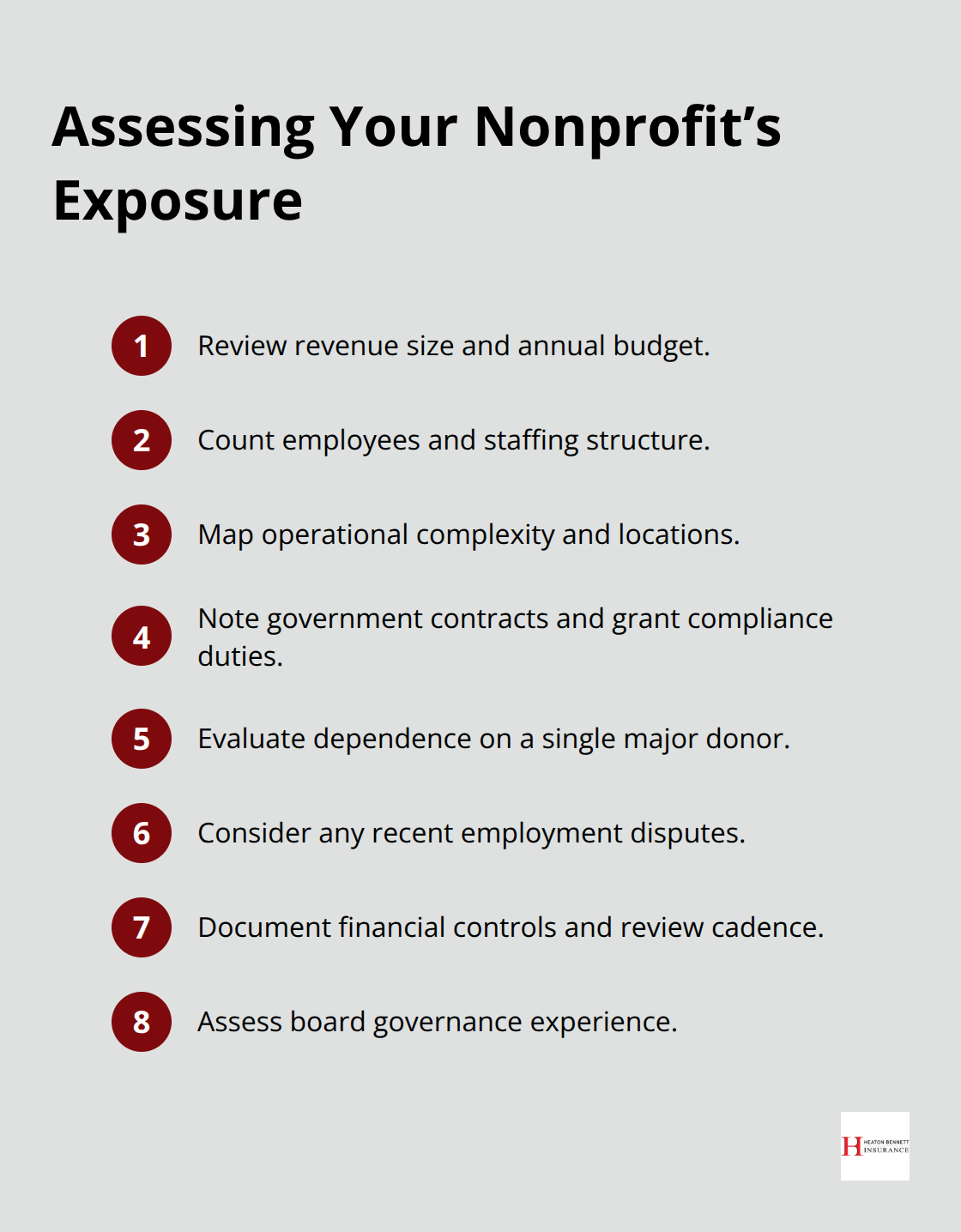

Selecting D&O coverage requires moving past generic policy templates and honestly assessing what your nonprofit would face if a claim hit today. Start by examining your organization’s revenue, employee count, and operational complexity. A nonprofit with $500,000 in annual revenue and five staff members faces fundamentally different exposures than a $5 million organization with forty employees and multiple program locations. Nonprofits with government contracts or complex grant requirements carry heightened compliance risk, while those dependent on a single major donor face concentrated financial vulnerability if that relationship sours into litigation.

The Travelers Risk Index 2025 found that 60% of nonprofits lack a post-breach response team and 53% lack an incident response plan entirely, meaning cyber-related D&O claims are far more likely in your sector than most boards acknowledge. Your risk assessment should inventory specific threats: Do your staff handle sensitive donor or beneficiary data? Does your board include members with limited nonprofit governance experience? Have you had employment disputes in the past three years? Are your financial controls documented and regularly reviewed, or do decisions flow informally through leadership? This honest inventory prevents you from purchasing coverage that sounds impressive but misses your actual exposure.

Understand Standard Policy Limits and What They Mean

Policy limits and deductibles demand equally practical thinking. Standard D&O policies typically start with $1 million per claim and $3 million aggregate limits, with umbrella options reaching $3 to $5 million depending on the plan selected. However, these numbers only matter if they match your organization’s realistic worst-case scenario. A wrongful termination lawsuit in a competitive urban market can easily exceed $200,000 in defense costs alone before settlement; employment practices claims involving multiple accusers or public allegations often run substantially higher.

Choose Deductibles That Fit Your Cash Position

Deductibles ranging from $0 to several thousand dollars shift the financial burden between your organization and the insurer. A $0 deductible eliminates out-of-pocket costs when claims arise, preserving your operational budget during crisis periods when you need reserves most. If your nonprofit operates with tight cash flow or limited reserves, the $0 deductible option is worth the premium increase because a single claim with a $10,000 deductible could force difficult program cuts. Conversely, organizations with substantial reserves and strong cash flow may accept higher deductibles to reduce annual premiums.

Work With an Insurance Professional

The critical step is consulting with an insurance professional who understands nonprofit operations, not accepting whatever coverage a carrier’s standard form offers. An experienced advisor can review your specific operations, leadership structure, and historical claims patterns rather than relying on what competitors market as standard solutions.

Final Thoughts

D&O claims strike nonprofits regularly, and prevention alone cannot stop them. The financial and reputational damage from an uninsured claim can cripple your organization at the moment when strong leadership matters most. The right nonprofit board coverage is affordable and available once you understand what your organization actually needs.

Mismanaged funds, employment disputes, fiduciary breaches, and compliance failures occur across nonprofits of all sizes, and your board members face personal liability exposure that extends beyond the organization itself. A single lawsuit can drain your reserves, damage your reputation with donors and beneficiaries, and force difficult decisions about program cuts when you should focus on your mission. Without proper protection, your leadership team carries unnecessary personal financial risk.

Assess your organization’s real risk profile, select policy limits that match your worst-case exposure, and work with an insurance professional who understands nonprofit operations. Connect with us at Heaton Bennett Insurance to review your specific operations and recommend tailored nonprofit board coverage that fits your unique exposures and budgets.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.