Independent Contractor Insurance: What It Covers for Small Firms

Independent contractors often operate without realizing how exposed they are to liability claims. A single lawsuit or accident can wipe out months of profit, which is why independent contractor insurance isn’t optional-it’s essential.

At Heaton Bennett Insurance, we’ve seen too many small firms learn this lesson the hard way. The right coverage protects your business, your clients, and your income when things go wrong.

What Independent Contractor Insurance Actually Covers

General Liability Protection

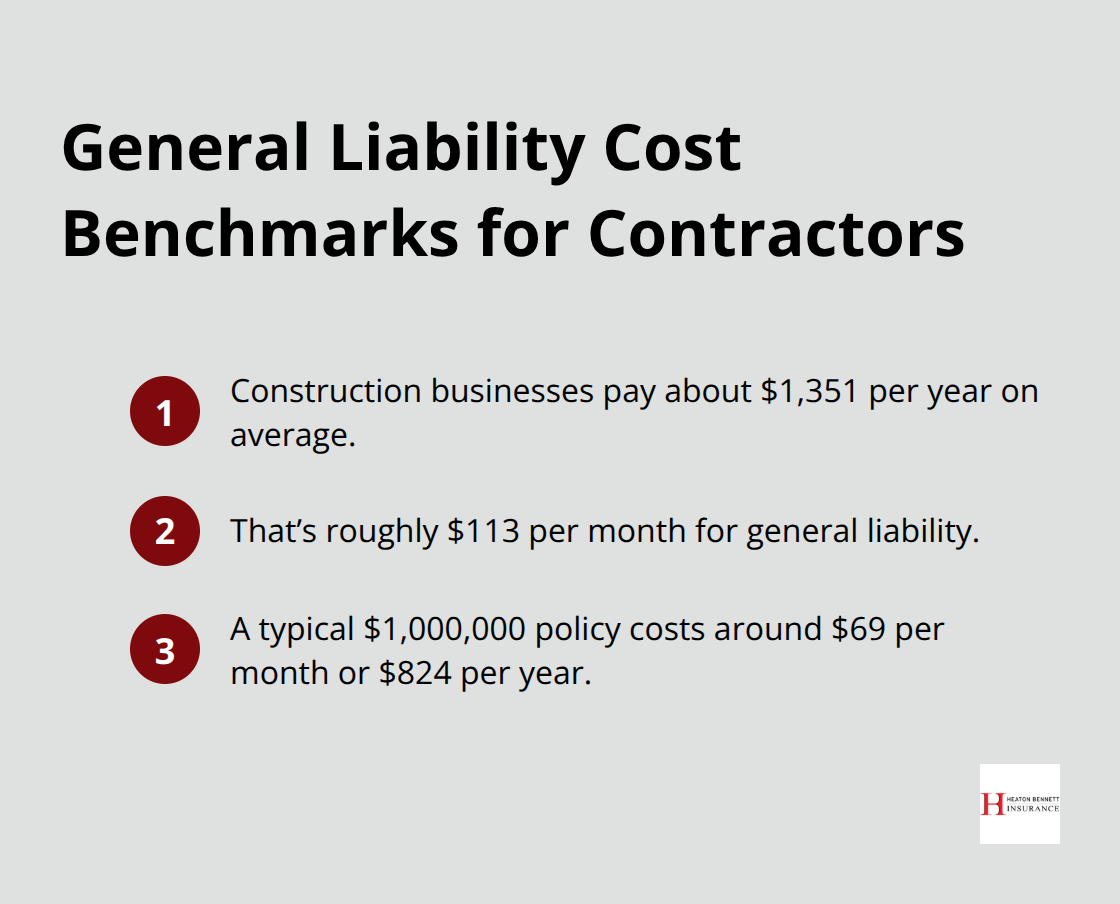

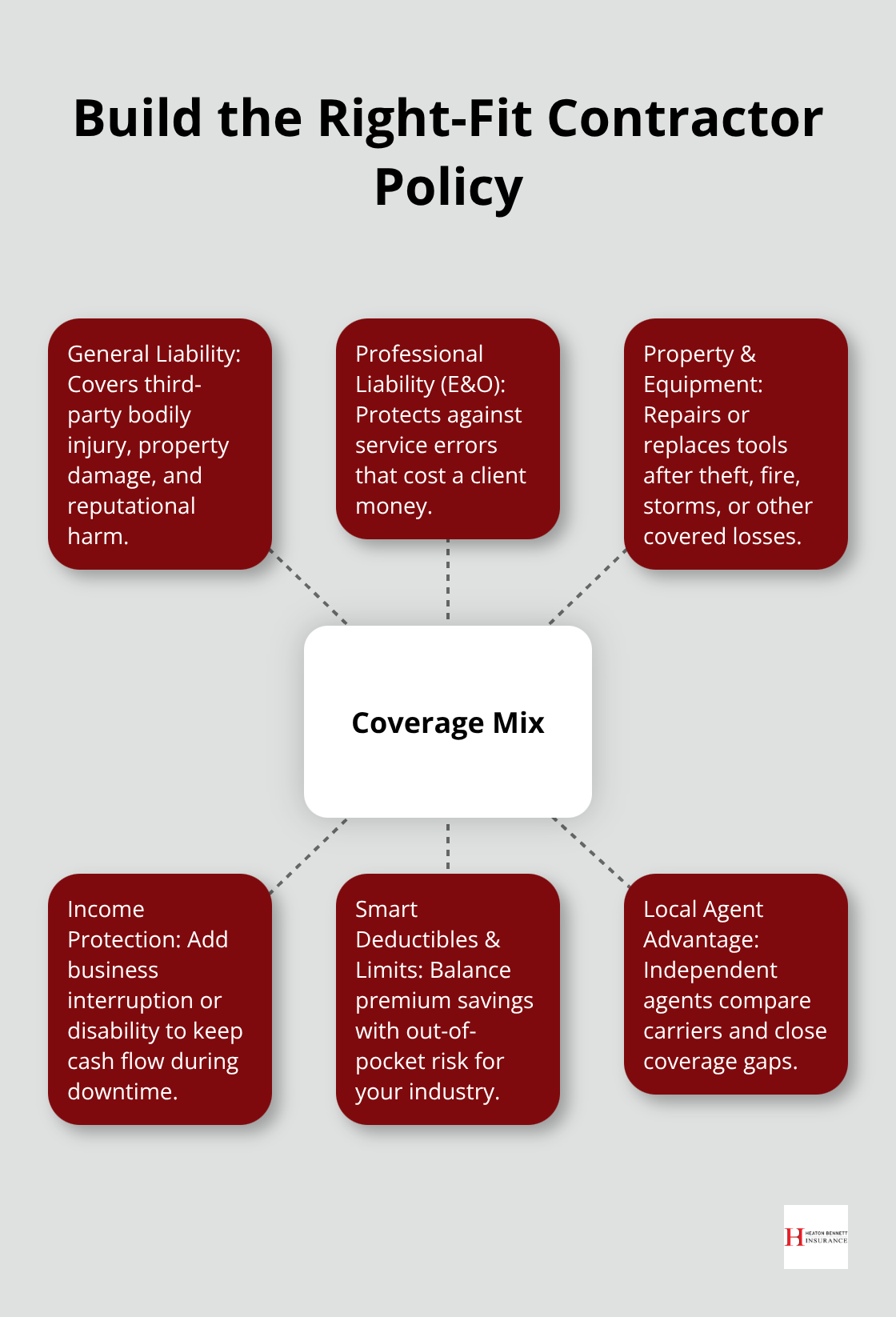

General liability protection forms the foundation of independent contractor insurance and covers third-party claims for bodily injury or property damage caused by your work. If a client claims you damaged their furniture during a cleaning job or someone is injured on a job site, general liability steps in to cover legal defense costs and damages up to your policy limit. On average, construction businesses pay about $1,351 per year for general liability insurance, roughly $113 per month, though a typical $1,000,000 policy costs around $69 per month or $824 per year. The coverage also protects against reputational harm from accusations like slander, libel, or privacy violations arising from your business operations. Without this protection, a single lawsuit can exceed your annual profits and force you to pay damages out of pocket, which is why general liability isn’t just recommended-it’s the bare minimum for any independent contractor.

Professional Liability and Errors and Omissions

Professional liability insurance, also called errors and omissions coverage, protects you when mistakes in your professional services cost a client money. A bookkeeper’s accounting error that costs a client thousands, a web developer’s site issue that causes missed sales, or an accountant filing an incorrect tax return leading to penalties-these scenarios are exactly what professional liability covers. This coverage is essential if you provide services for a fee, particularly in consulting, design, IT, accounting, or similar fields where your advice or work directly impacts client finances.

Property and Equipment Coverage

Property and equipment coverage protects the tools and equipment you own or rent for work, covering damage from fires, storms, theft, or other covered losses. Many independent contractors overlook this coverage until they lose expensive equipment or inventory to a covered event. The combination of these three coverage types-general liability, professional liability, and property coverage-creates a comprehensive shield against the most common and costly risks contractors face.

Your specific industry determines which coverages matter most. Assessing your actual risk exposure before shopping for insurance saves you money and prevents dangerous gaps in protection, which is why the next step involves understanding the specific risks your business faces.

Key Risks Independent Contractors Face Without Proper Coverage

Client Lawsuits Drain Cash Reserves Fast

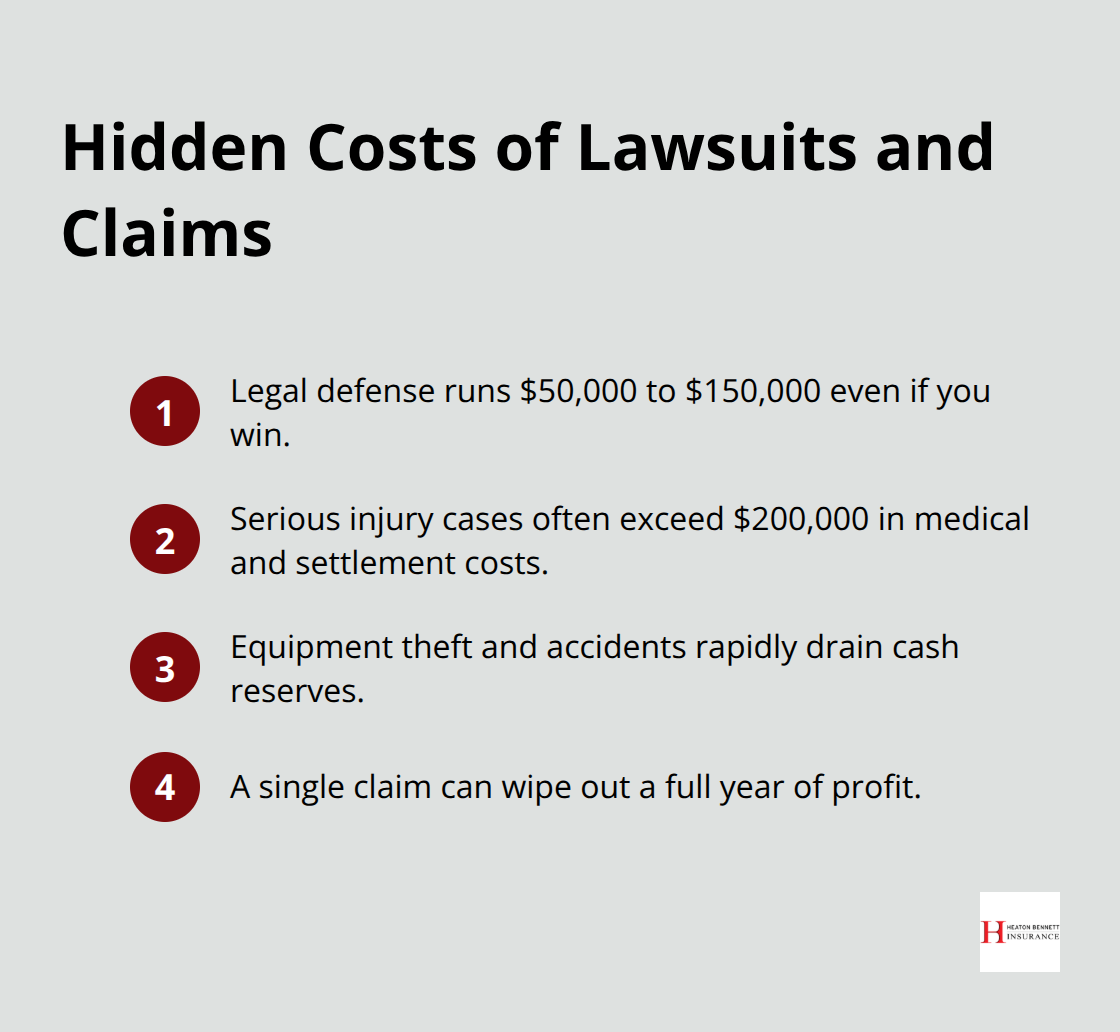

A client lawsuit over property damage or bodily injury costs $50,000 to $150,000 in legal defense alone, even if you win the case. Medical expenses and settlement payouts for serious injuries regularly exceed $200,000, which most contractors cannot absorb without filing for bankruptcy. Equipment theft, job site accidents, or client disputes that turn into litigation drain cash reserves faster than most small firms can recover.

A single claim wipes out an entire year’s profit, and ongoing legal battles prevent you from working while still requiring payment for attorney fees and court costs.

Income Loss Creates Immediate Financial Crisis

If you become injured or seriously ill, you lose income immediately with no safety net unless you have business interruption or disability coverage built into your policy. A construction worker who breaks an arm cannot work for eight weeks, losing roughly $8,000 to $12,000 in income depending on project rates, and general liability alone does not replace that lost revenue. Equipment damage from weather, theft, or accidents forces you to rent replacements at premium rates or pause projects entirely, multiplying losses.

Reputation Damage Destroys Future Revenue

Clients who claim dissatisfaction with your work and refuse payment create cash flow crises that small firms cannot survive without legal protection and professional liability coverage to defend your reputation and fee agreements. A negative review or dispute that escalates into a claim damages your ability to land new projects, compounding the financial impact of the original loss. Without professional liability coverage, you pay attorney fees to defend yourself while simultaneously losing the income you need to cover those costs.

The combination of lawsuit costs, income interruption, and equipment losses transforms a single bad year into permanent business closure for contractors operating without comprehensive insurance. Understanding these specific risks helps you identify which coverage types your business actually needs.

How to Choose the Right Independent Contractor Insurance Policy

Identify Your Specific Business Risks

Start by documenting exactly what your business does and where the financial exposure lives. A plumber faces different risks than a freelance designer, and a painter working on residential properties faces different liability than one handling commercial contracts. Write down the three to five worst-case scenarios specific to your work: What if you damage a client’s property? What if someone gets injured? What if a mistake costs a client money? What equipment would you lose if theft or weather struck? This exercise takes 30 minutes and reveals which coverage types matter most instead of purchasing blanket protection you don’t need.

Many contractors waste money on coverages that don’t apply to their work while leaving critical gaps unprotected. A virtual assistant has no use for property coverage but absolutely needs professional liability because a data handling error could cost a client thousands. A house cleaner needs general liability to cover accidental damage but might skip professional liability entirely since they’re not providing fee-based professional advice.

Compare Coverage Limits Across Multiple Carriers

Once you identify your real risks, compare actual policy limits and deductibles across multiple carriers rather than assuming the cheapest quote offers the best value. A $1,000,000 general liability policy costs around $69 per month on average, but your industry, location, years in business, and claims history shift that number significantly. Request quotes from at least three different insurers and ask each one to explain what scenarios their policy covers and which ones it excludes.

Deductibles matter more than people realize: a $500 deductible saves you roughly 10 to 15 percent in premiums compared to a $250 deductible, but that savings vanishes if you face multiple small claims in a year. Higher-risk industries like construction justify higher coverage limits because a single lawsuit regularly exceeds $200,000, while lower-risk service work might function fine with $500,000 limits.

Work with a Local Insurance Agent

A local independent insurance agent who understands your specific industry prevents costly mistakes that online quote tools often miss. An agent can identify state-specific requirements, flag coverage gaps you wouldn’t catch alone, and bundle policies into a Business Owner’s Policy that costs less than purchasing general liability and property coverage separately. This approach transforms insurance from a compliance checkbox into actual protection that matches your business reality.

Final Thoughts

Independent contractor insurance protects your business from the financial devastation that lawsuits, equipment loss, and income interruption create. General liability covers third-party injury and property damage claims, professional liability protects against mistakes in your services, and property coverage shields your tools and equipment from theft or disaster. Together, these coverage types address the real risks that destroy small firms operating without protection.

Securing adequate independent contractor insurance starts with honest assessment of your specific business risks rather than guessing what you might need. Document your worst-case scenarios, identify which coverage types actually apply to your work, and request quotes from multiple carriers to compare limits and deductibles. A $1,000,000 general liability policy costs around $69 per month on average, but your industry, location, and experience shift that price significantly, which is why comparison shopping matters more than accepting the first quote.

Working with an insurance agent transforms this process from overwhelming to straightforward. At Heaton Bennett Insurance, we access multiple carriers to find coverage that matches your actual exposure rather than forcing you into one-size-fits-all policies that leave gaps or waste money on unnecessary protection. Contact us today to discuss your independent contractor insurance needs and build a protection plan tailored to your business.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.