How Much Is Business Liability Insurance?

Business liability insurance costs vary dramatically based on your company’s size, industry, and location. Small businesses typically pay between $400 to $1,500 annually for general liability coverage.

We at Heaton Bennett Insurance see many business owners struggle with understanding how much is business liability insurance and what drives these price differences. The right coverage protects your business without breaking your budget.

What Drives Business Liability Insurance Pricing?

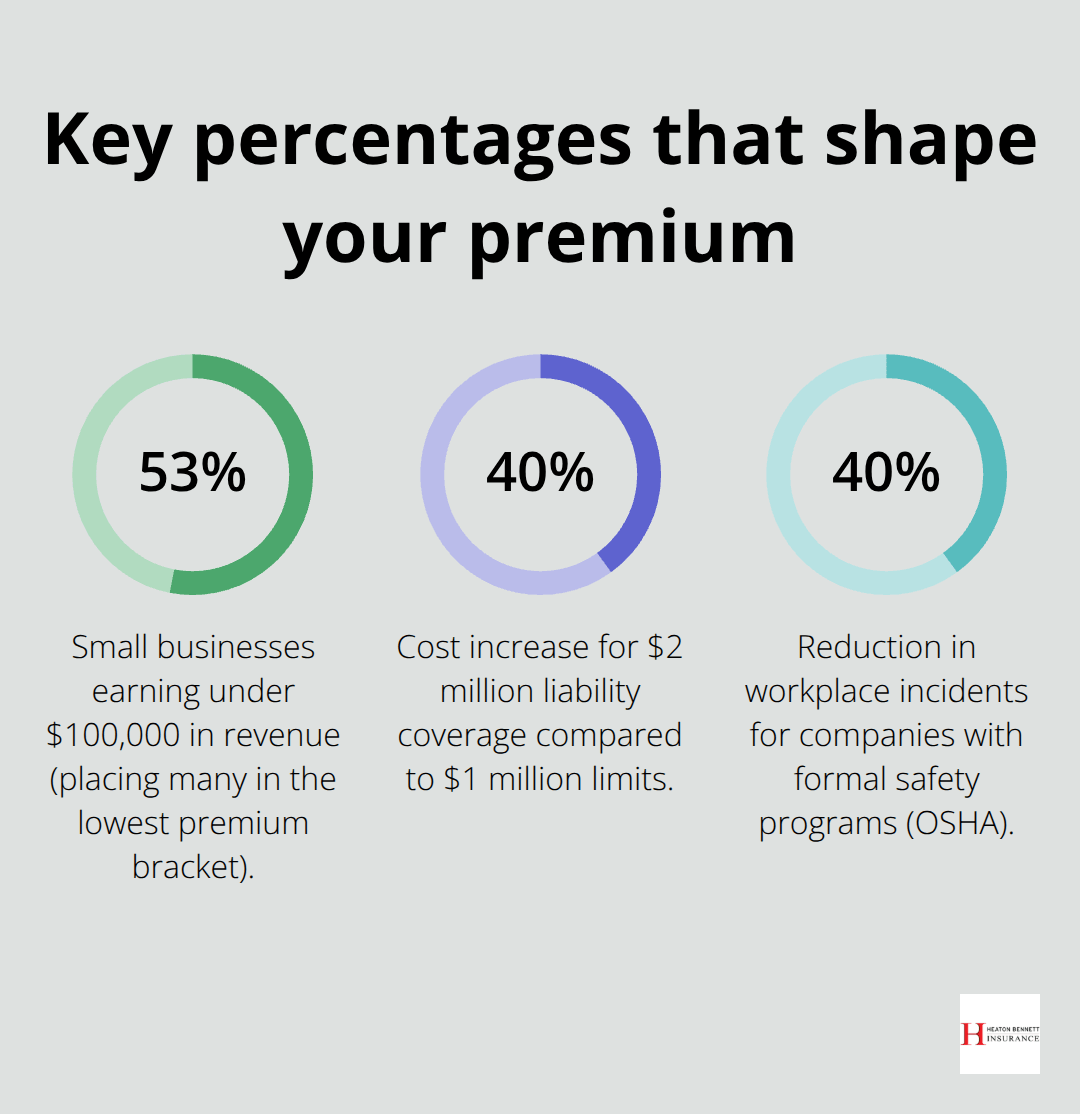

Business size directly impacts your insurance costs. Small businesses under $100,000 annual revenue typically pay $400-$1,500 annually for general liability coverage. Medium-sized businesses with revenues between $100,000-$1 million face premiums that range from $1,500-$3,500, while larger companies often exceed $5,000 annually. The National Federation of Independent Business found that 53% of small businesses earn less than $100,000, which places them in the lowest premium bracket.

Industry Risk Levels Shape Your Premiums

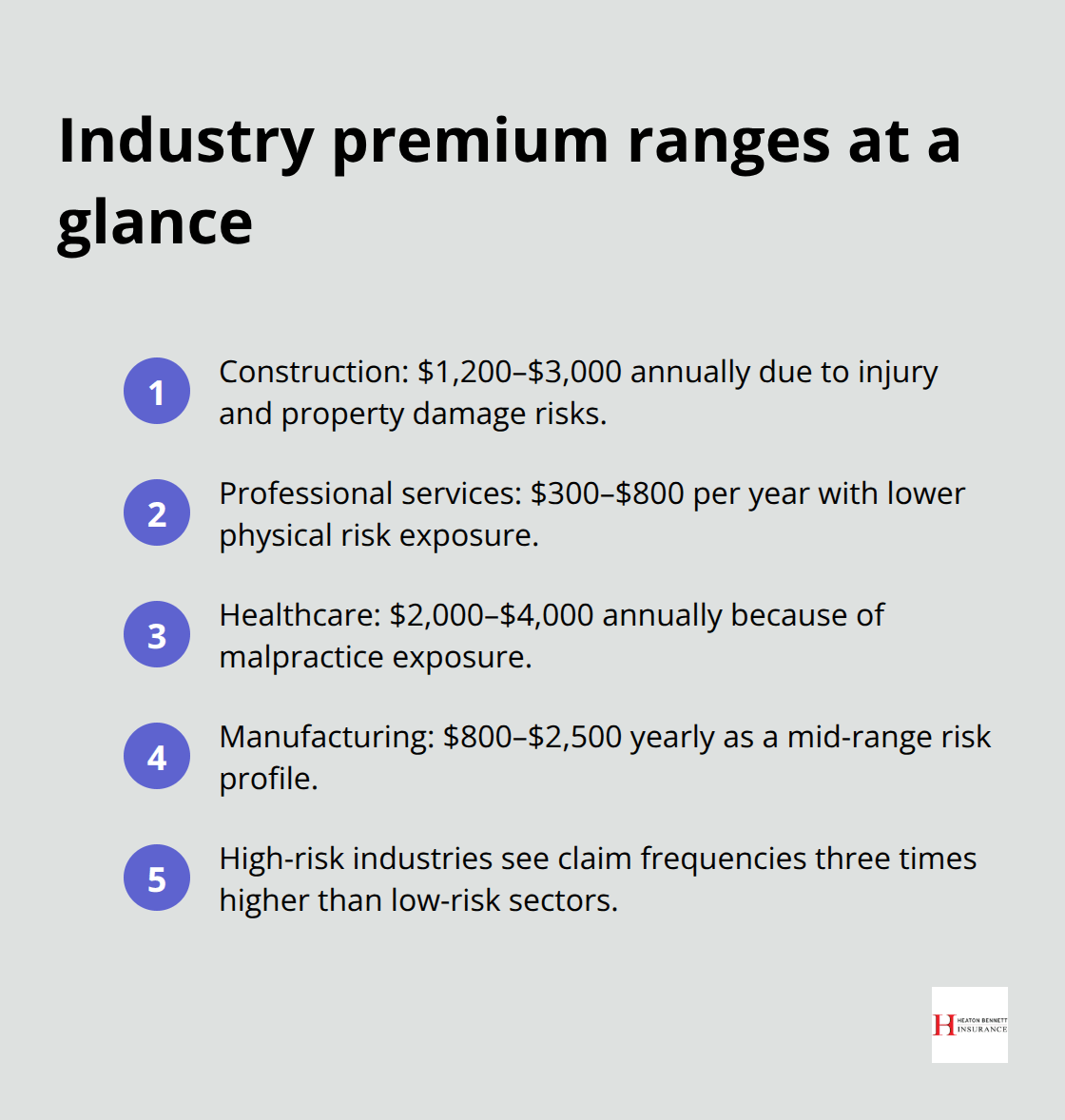

Construction companies pay the highest premiums, with costs that average $1,200-$3,000 annually due to physical injury risks and property damage exposure. Professional services like accounting or consulting pay significantly less, typically $300-$800 per year. Healthcare businesses face elevated costs around $2,000-$4,000 annually because of malpractice exposure. Manufacturing operations fall in the middle range at $800-$2,500 yearly.

The Insurance Information Institute reports that high-risk industries experience claim frequencies three times higher than low-risk sectors.

Geographic Location Creates Premium Variations

Texas businesses pay 15-20% more than the national average due to severe weather risks and higher litigation rates. California companies face similar increases because of earthquake exposure and strict liability laws. Florida businesses deal with hurricane-related surcharges that add 25-30% to base premiums. Conversely, businesses in states like Wyoming or Vermont often pay 10-15% below national averages. Urban locations within any state typically cost 20-40% more than rural areas due to higher property values and increased lawsuit frequency.

Employee Count Affects Your Risk Profile

Companies with more employees face higher premiums because additional staff increases potential liability exposure. Businesses with 1-5 employees typically pay base rates, while companies with 10-25 employees see premium increases of 20-30%. Organizations with over 50 employees often pay 50-75% more than small operations due to workers’ compensation requirements and general liability exposure. Each additional employee represents potential claims risk that insurers factor into their calculations.

These factors work together to determine your final premium, but you can take specific steps to reduce these costs through strategic choices.

What Determines Your Business Liability Premium

Your annual revenue directly controls your premium calculations because insurers view higher-earning businesses as greater liability targets. Companies that earn under $100,000 pay base rates, while businesses that generate $500,000-$1 million face premium increases of 40-60% according to Progressive Commercial data. Revenue over $2 million often triggers premium multipliers of 2-3 times the base rate. This structure reflects the reality that successful businesses attract more lawsuits and face higher settlement demands.

Risk Classification Drives Premium Structure

Insurers use specific industry classification codes that place your business into predetermined risk categories with fixed premium ranges. Construction trades face the highest multipliers at 3.5-4 times base rates due to injury exposure, while professional consultants receive the lowest multipliers at 0.8-1.2 times base rates. Manufacturing operations sit in the middle at 1.8-2.2 times base rates. Your business description on the application determines your rate category, so accuracy matters more than you think. Misclassification of your business operations can result in denied claims or premium adjustments later.

Claims History Creates Long-Term Cost Impact

A single liability claim increases your premiums by 25-40% for the next three to five years according to Insurance Information Institute research. Two claims within five years can double your annual costs, while three or more claims often make coverage difficult to obtain through standard markets. The claims-free discount works in reverse too – businesses with five-year clean records receive premium reductions of 10-15%.

Coverage Limits Multiply Base Costs

Your coverage limits also multiply your base premium: $2 million coverage costs roughly 40% more than $1 million coverage, while umbrella policies that add $5 million in additional protection typically cost $600-$1,200 annually. Higher limits protect your business assets but come with proportional cost increases that compound over time.

These premium factors work together to create your final rate, but smart business owners can implement specific strategies to reduce these costs significantly.

How Can You Cut Your Insurance Costs

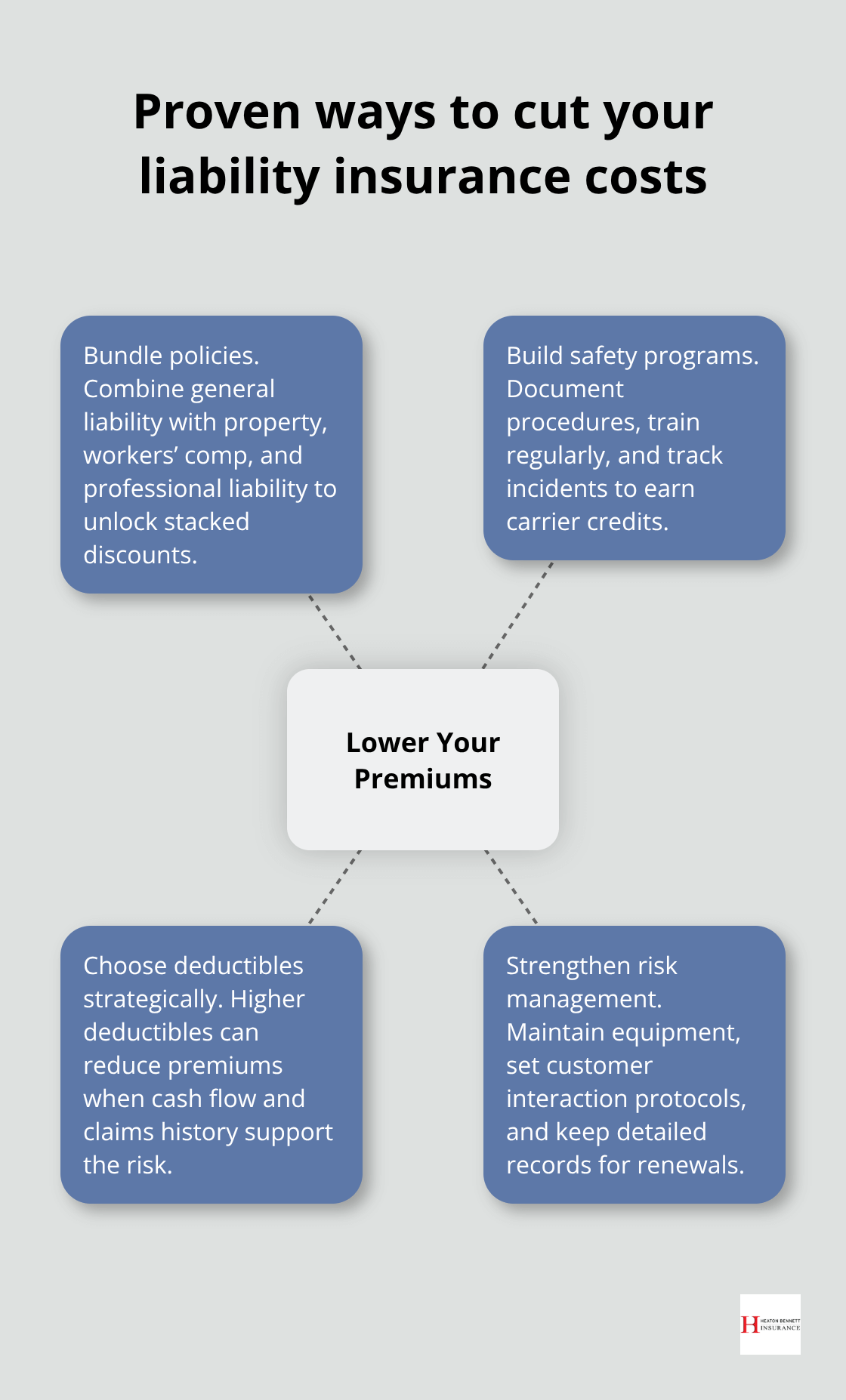

Smart bundling delivers the most immediate savings on your business liability premiums. You combine general liability with commercial property insurance through a Business Owner’s Policy and reduce costs by 15-25% compared to separate policies according to The Hartford data. You add workers’ compensation to your bundle and create additional discounts of 10-15%, while professional liability inclusion saves another 5-10%.

Commercial umbrella policies become significantly cheaper when bundled, often costing 40-50% less than standalone umbrella coverage.

Safety Programs Generate Measurable Premium Reductions

Insurance companies reward businesses that implement documented safety programs with premium discounts of 10-20%. The Occupational Safety and Health Administration reports that companies with formal safety programs experience 40% fewer workplace incidents, which directly translates to lower insurance costs. Monthly safety meetings, written safety protocols, and incident reports qualify for these discounts. Equipment maintenance logs and employee safety certifications provide additional premium reductions. You install security systems, fire suppression equipment, and proper lights and reduce premiums by another 5-15%. Regular safety audits conducted by third-party professionals often unlock the highest discounts available.

Strategic Deductible Selection Reduces Annual Costs

You increase your deductible from $500 to $2,500 and typically reduce annual premiums by 15-25%, while you jump to $5,000 and can cut costs by 25-35% according to Progressive Commercial analysis. Higher deductibles work best for businesses with strong cash flow and low claims frequency. The key calculation involves you compare annual premium savings against your increased out-of-pocket exposure per claim. Businesses that have maintained claims-free records for three or more years (particularly those with consistent revenue streams) benefit most from higher deductibles because their low claims probability makes the risk worthwhile.

Risk Management Practices Lower Long-Term Costs

You implement comprehensive risk management and create substantial premium reductions over time. Employee training programs that focus on workplace safety reduce incident rates by up to 30% according to industry data. You document all safety procedures and maintain detailed records, which insurers view favorably during renewal periods. Regular equipment inspections and maintenance schedules prevent accidents that lead to claims. You establish clear protocols for customer interactions and reduce liability exposure in service-based businesses.

Final Thoughts

Business liability insurance costs depend on multiple interconnected factors that work together to determine your final premium. Your industry risk level, business size, geographic location, employee count, and claims history create the foundation for pricing calculations. Construction companies face the highest costs at $1,200-$3,000 annually, while professional services pay significantly less at $300-$800 per year.

Revenue levels directly impact premiums, with businesses that earn over $500,000 facing increases of 40-60% compared to smaller operations. Geographic factors add another layer of complexity, with Texas businesses that pay 15-20% above national averages due to weather risks and litigation rates. Independent insurance agents provide access to multiple carriers and competitive pricing options that single-carrier agents cannot match.

We at Heaton Bennett Insurance help Austin businesses navigate these complex pricing factors when they ask how much is business liability insurance. Our team evaluates your unique risk profile and compares options from multiple carriers to find optimal coverage at competitive rates (through our comprehensive approach to commercial insurance). Contact us today for personalized quotes that reflect your actual business operations and risk exposure through our commercial insurance coverage services.