Restaurant Liability Insurance Demystified for Owners

Running a restaurant means managing countless risks every single day. From slip-and-fall accidents to foodborne illness claims, the threats to your business are real and costly.

Restaurant liability insurance protects you against these dangers, but many owners don’t fully understand what it covers or how much protection they actually need. At Heaton Bennett Insurance, we’ve helped restaurant owners navigate these decisions, and we’re here to break down the confusion.

What Your Restaurant Liability Policy Actually Covers

Bodily Injury and Medical Payments Protection

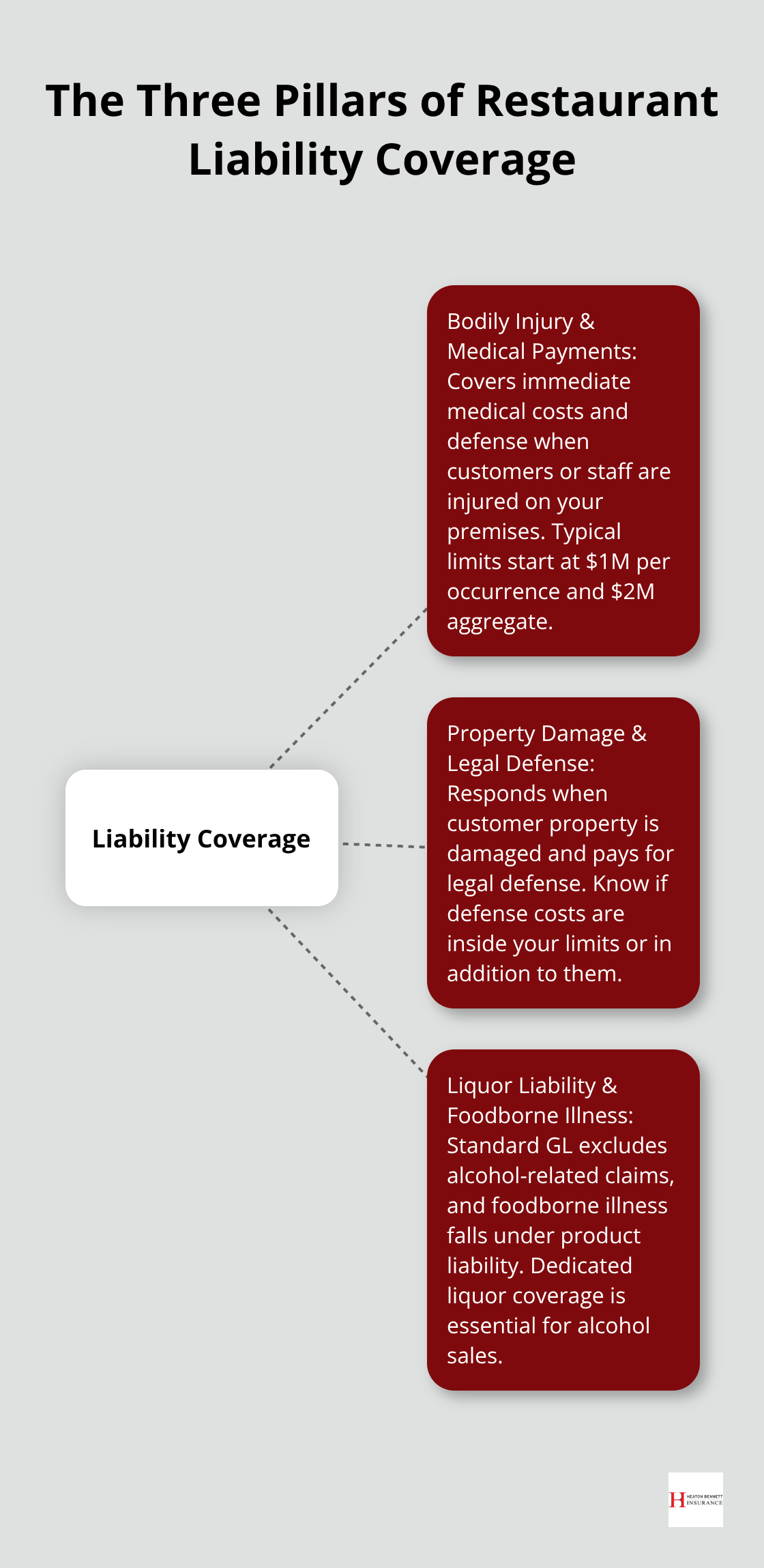

Restaurant liability insurance protects against three major categories of loss that hit your bottom line hard. The first covers bodily injury and medical expenses when a customer or staff member gets hurt on your premises. A slip on a wet floor near the bar, a burn from touching a hot plate, or an allergic reaction to an ingredient-these incidents trigger medical payments coverage that handles immediate treatment costs and, if needed, defense against a lawsuit. Most policies carry limits of $1 million per occurrence and $2 million aggregate, though high-traffic locations or venues with outdoor seating should push to $2 million per occurrence and $4 million aggregate to reduce the risk of large settlements exceeding your coverage.

Property Damage and Legal Defense Costs

The second category covers property damage and legal defense costs. A customer’s personal property gets damaged-a coat ruined by a kitchen fire, a phone dropped during an incident-and your policy responds. More importantly, legal defense costs come out of your coverage limits or, in some policies, in addition to them. This distinction matters enormously. A liquor liability claim from an alleged overserving incident can cost $50,000 to $150,000 just in defense expenses before a verdict, so knowing whether defense is inside or outside your limit changes your actual protection significantly.

Liquor Liability and Foodborne Illness Exposure

The third category-liquor liability and foodborne illness-represents your highest-risk exposures. Liquor liability is separate from general liability because standard GL policies exclude alcohol-related claims entirely. If a customer becomes intoxicated at your bar and causes harm to themselves or others, your GL won’t respond. You need a dedicated liquor liability policy with at least $1 million in coverage, or $2 million or higher if alcohol accounts for more than 40% of your revenue. As of 2025, 43 states plus Washington D.C. have dram shop laws that allow third parties to sue restaurants and bars for injuries caused by overservice. Texas remains particularly challenging for liquor liability pricing, while South Carolina’s 2025 reforms lowered thresholds for some venues, creating opportunities for better rates if you implement server training and loss-control measures.

Foodborne Illness Claims and Prevention

Foodborne illness claims fall under product liability within your GL policy and cover claims when a customer suffers illness from contaminated food or drink. The National Restaurant Association reports that 9 in 10 food establishments identify food costs as a major challenge, but cost-cutting on food safety creates enormous exposure. A norovirus outbreak traced to your kitchen can generate medical expense claims, business interruption losses if you’re forced to close for deep cleaning, and reputation damage that persists for months. Your policy’s foodborne illness coverage typically includes defense costs and medical payments up to your policy limits, but the real protection comes from prevention-rigorous time and temperature controls, handwashing protocols following FDA Food Code 2022 standards, and documented training for all staff handling ready-to-eat foods.

Understanding these three pillars of coverage sets the foundation for your protection strategy. However, liability insurance alone doesn’t tell the complete story of what restaurants actually face in claims.

Where Restaurant Claims Actually Happen

Slip and Fall Accidents in High-Risk Zones

Slip and fall accidents dominate restaurant claims because they occur in environments where water, grease, and foot traffic collide constantly. Wet floors near the bar, spilled sauces in the dining room, and cluttered kitchen aisles create liability traps that trigger claims multiple times per week in busy establishments. These incidents affect both customers and staff, but staff injuries also pull from your workers’ compensation policy simultaneously, creating overlapping exposure.

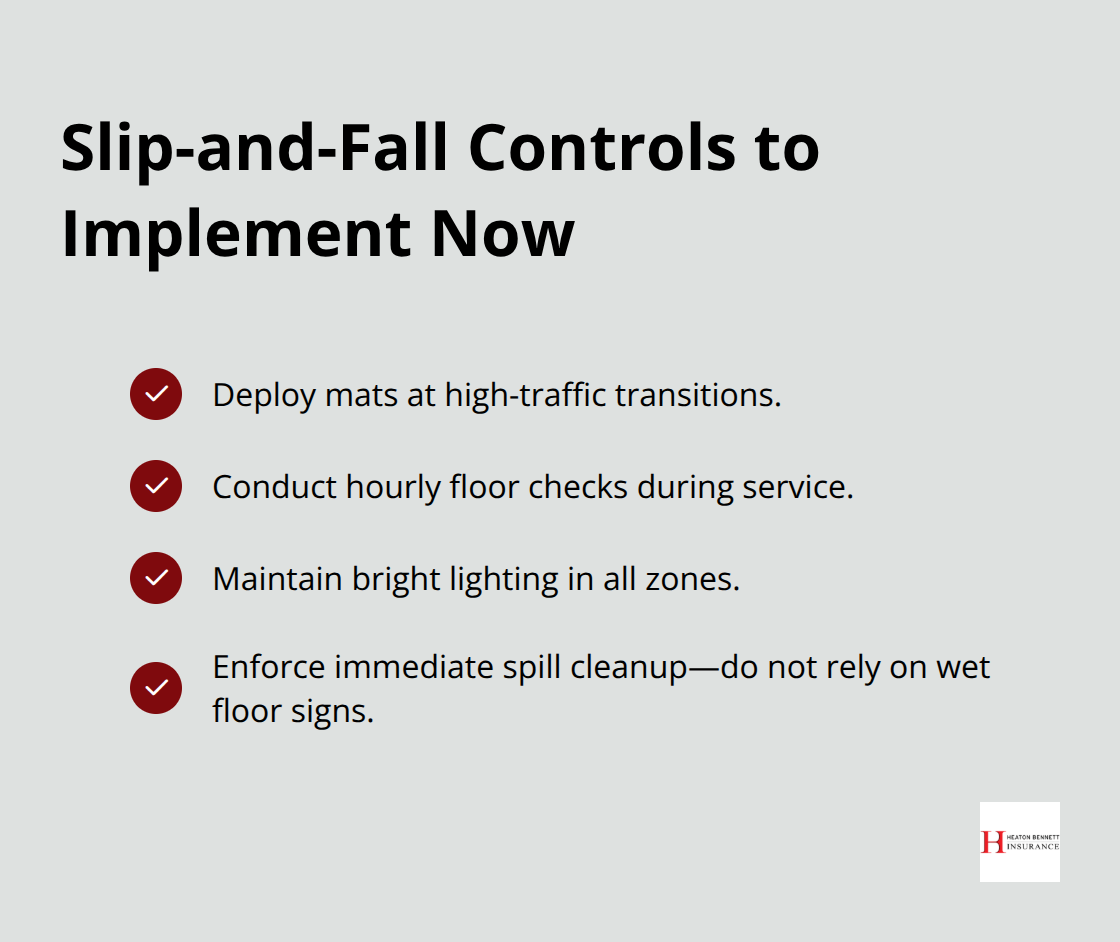

Front-of-house hotspots include entrances where customers track moisture inside, restrooms where soap and water accumulate, and crowded aisles during peak service. Back-of-house zones like dish stations and fryer areas pose even higher risk because heat and humidity intensify slip hazards. Deploy mats at high-traffic transitions, conduct hourly floor checks during service, maintain bright lighting in all zones, and enforce a culture where staff immediately cleans spills rather than leaving wet floor signs as a substitute.

Foodborne Illness Outbreaks and Prevention

Foodborne illness claims arrive when ready-to-eat foods are handled bare-handed or when time and temperature controls fail. Norovirus, Salmonella, and E. coli outbreaks traced to your kitchen generate medical expense claims, business interruption losses if you’re forced to close for deep cleaning, and reputation damage that persists for months. The FDA Food Code 2022 provides the standard that underwriters and plaintiffs’ attorneys use to evaluate your practices, so strict adherence to handwashing protocols, temperature logging, and documented staff training becomes your defense.

A single outbreak can cost $50,000 to $200,000 in direct claims plus lost revenue during closure. Your liability policy covers medical expenses and defense costs, but prevention stops the claim from happening in the first place. Implement temperature logs for all cold storage, require handwashing at designated intervals, and train all staff handling ready-to-eat foods on contamination risks.

Alcohol-Related Incidents and Dram Shop Exposure

Alcohol-related incidents create the highest-severity claims because dram shop laws in 43 states allow third parties to recover damages from alleged overservice. A customer becomes intoxicated at your bar, leaves, and causes a vehicle accident that injures or kills someone; the injured party sues your restaurant for negligent overservice. Defense costs alone run $50,000 to $150,000 before any verdict, and verdicts in high-award states like California, Texas, and New York regularly exceed $500,000.

Server training that documents refusal techniques, ID checking procedures, and incident logs demonstrating your loss-control measures directly influences what underwriters charge for liquor liability coverage and whether they’ll renew your policy at all. Establishments with at least three years of clean loss history and documented server training access more favorable liquor liability markets. Your training program should cover recognizing intoxication signs, refusing service politely but firmly, and handling ejections without escalating conflict. These controls transform your risk profile from a liability concern into an underwriting asset, which matters enormously when renewal time arrives and carriers evaluate whether to continue coverage.

Building Your Coverage Strategy

Calculate Your Revenue Mix and Exposure Profile

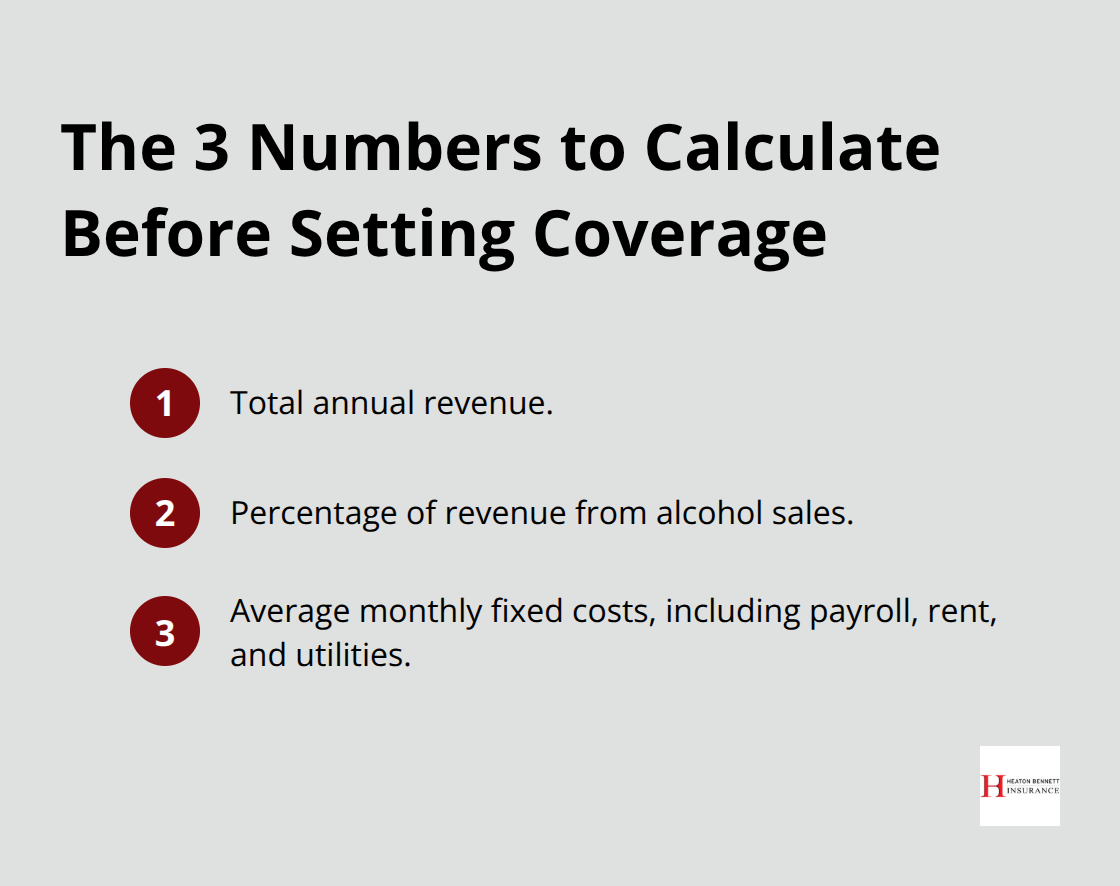

Choosing the right liability coverage starts with understanding what your restaurant actually generates in revenue and where your exposure concentrates. Pull your last two years of tax returns, your current POS data, and your lease agreement, then calculate three specific numbers: total annual revenue, the percentage of revenue from alcohol sales, and your average monthly fixed costs including payroll, rent, and utilities. These numbers drive every coverage decision. A $2 million annual revenue restaurant with alcohol representing 15% of sales faces fundamentally different underwriting than a $5 million venue where alcohol hits 50% of revenue.

Carriers price liquor liability at 3 to 5 times higher rates for high-alcohol venues, so knowing your exact mix determines whether you’re looking at $2,000 or $8,000 annually just for liquor coverage.

Align Your Policy with Lease Requirements

Your lease dictates minimum coverage requirements that you cannot ignore. Most commercial leases require general liability of at least $1 million per occurrence and $2 million aggregate, with additional insured status for your landlord, waiver of subrogation language, and proof of coverage delivered within 30 days of lease execution. Misalignment between your lease requirements and your actual policy can trigger lease violation notices or forced insurance requirements, so cross-check your lease language against your declarations page before your policy renews. For restaurants with owned delivery vehicles or employees using personal vehicles for business errands, hired and non-owned auto coverage costs $400 to $1,500 annually but covers liability when an employee causes an accident in their own car. Without HNOA, your business faces vicarious liability that your general liability policy won’t touch.

Right-Size Your Coverage Limits to Actual Exposure

Coverage limits matter more than premium price because undershooting your limit creates an out-of-pocket gap when a claim exceeds it. A Phoenix restaurant with a $291,000 kitchen fire loss faced a $100,000 business interruption limit that left them $191,000 short. Business interruption coverage should reflect 12 to 18 months of your fixed costs plus lost profit, not just a round number that feels comfortable. If your restaurant generates $15,000 in monthly fixed costs, you need $180,000 to $270,000 in business interruption limits to cover a major closure. Equipment breakdown coverage protecting refrigeration, fryers, and POS systems typically costs $500 to $2,500 annually for $100,000 to $250,000 in limits and prevents spoilage losses that can exceed $10,000 overnight when a compressor fails.

Account for Payroll and State-Specific Wage Requirements

Workers compensation costs range from $1.50 to $6 per $100 of payroll depending on your state and job classifications, meaning a restaurant with $300,000 in annual payroll pays roughly $4,500 to $18,000 yearly. California’s $20 minimum wage for fast-food workers has reshaped payroll calculations, so verify your state’s current wage requirements and recalculate coverage annually as labor costs climb. Each state imposes different minimum wage thresholds and workers compensation formulas, so what you paid last year may not reflect what you owe this year.

Conduct a Consultative Risk Review Before Binding

An independent insurance professional should read your lease, verify state and local liquor authority requirements, cross-check those against your current policy language, and identify gaps before binding coverage. This consultative process ensures your policy aligns with lease obligations, liquor regulations, and your actual operational footprint rather than accepting default limits that leave you exposed.

Final Thoughts

Restaurant liability insurance protects your business from the financial devastation that slip-and-fall accidents, foodborne illness claims, and alcohol-related incidents create. Understanding what your policy covers matters, but matching your coverage limits to your actual exposure determines whether you stay protected or face out-of-pocket gaps when claims arrive. A $1 million general liability limit works for small cafes but leaves high-traffic locations vulnerable to settlements that exceed your coverage, while business interruption limits that don’t reflect 12 to 18 months of fixed costs create dangerous shortfalls when major losses force closures.

Professional guidance transforms restaurant liability insurance from a compliance checkbox into a strategic asset that carriers recognize during renewal negotiations. An independent insurance professional reads your lease, verifies state liquor authority requirements, cross-checks those against your policy language, and identifies gaps before they become claims. They help you calculate revenue mix accurately, right-size coverage limits to your actual exposure, and implement documented loss-control measures that influence your renewal pricing and carrier appetite.

We at Heaton Bennett Insurance understand that restaurant owners juggle countless operational decisions while managing tight margins. Schedule a consultative risk review with an independent insurance professional who understands restaurant operations, state liquor laws, and lease requirements, and bring your lease agreement, current declarations page, last two years of tax returns, and your POS data showing revenue mix. Contact Heaton Bennett Insurance today to start building the restaurant liability insurance strategy your business deserves.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.