Insurance for Subcontractors: Ensure Coverage and Compliance

Subcontractors face unique risks that standard homeowner or auto policies simply don’t cover. Working on job sites, managing employees, and operating specialized equipment creates liability exposures that can bankrupt your business if you’re not properly protected.

At Heaton Bennett Insurance, we’ve seen too many subcontractors operate without adequate coverage-only to face devastating financial consequences when accidents happen. The right insurance for subcontractors isn’t optional; it’s the foundation of a sustainable business.

Why Subcontractors Need Specialized Insurance

Standard Policies Leave You Exposed

Standard homeowner and auto policies exclude work-related liability, which means you operate without protection the moment you step onto a job site. Most homeowner policies explicitly exclude business activities, and auto policies don’t cover commercial use of vehicles. Construction workers face injury rates significantly higher than the national average, yet many subcontractors rely on personal policies that won’t pay a dime when accidents happen. State laws in most jurisdictions require workers’ compensation insurance for any business with employees. New York specifically enforces subcontractor coverage through the Construction Fair Play Act, and operating without mandated coverage results in fines, license suspension, and personal liability for injuries. A single claim from an employee injury or third-party property damage can cost tens of thousands of dollars out of pocket.

Trade-Specific Risks Demand Specialized Coverage

Your trade creates unique hazards that standard policies ignore. A roofer faces fall hazards and weather-related property damage claims that a homeowner policy won’t touch. An electrician needs professional liability coverage if a wiring mistake causes a fire months after the job ends. A plumber requires coverage for water damage claims that arise after installation. These scenarios demand coverage designed specifically for construction work, not personal use.

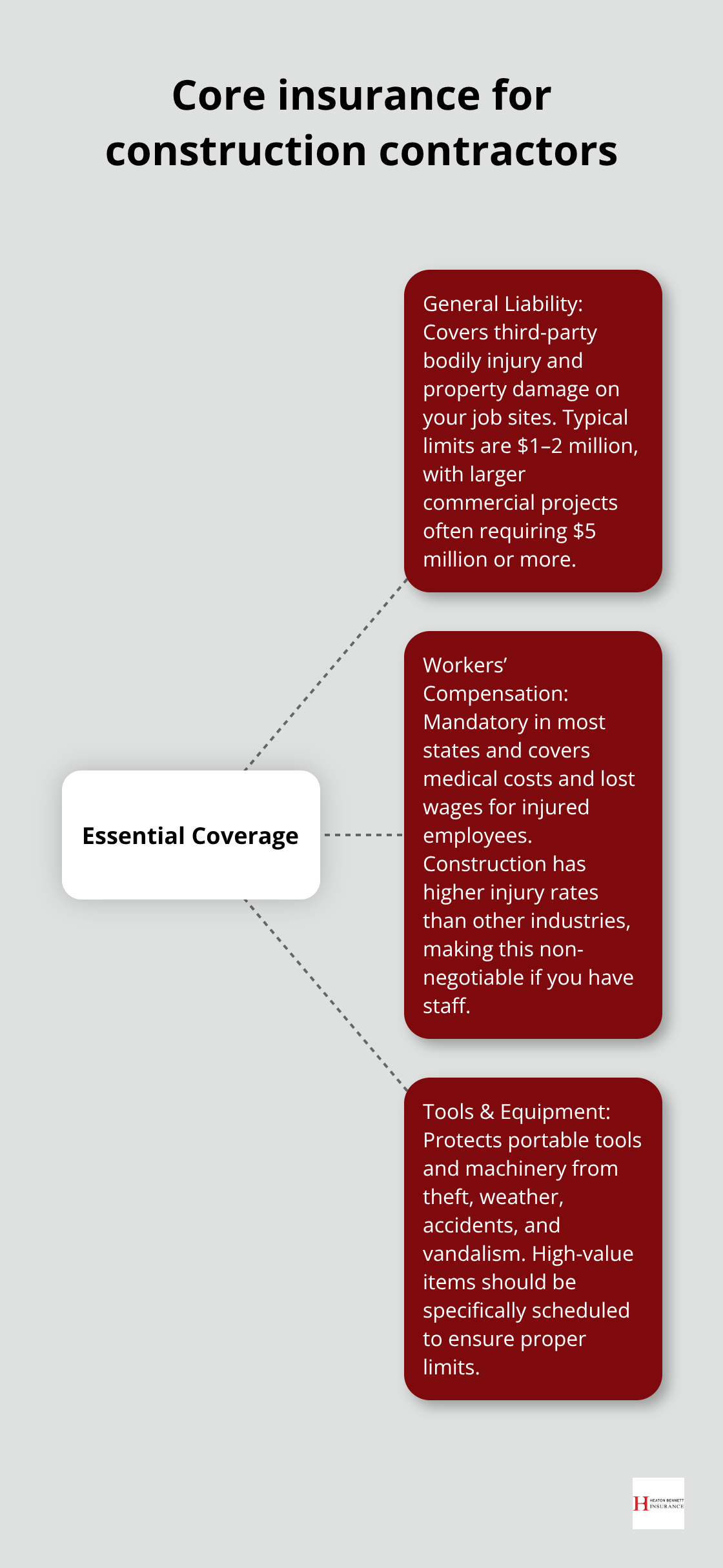

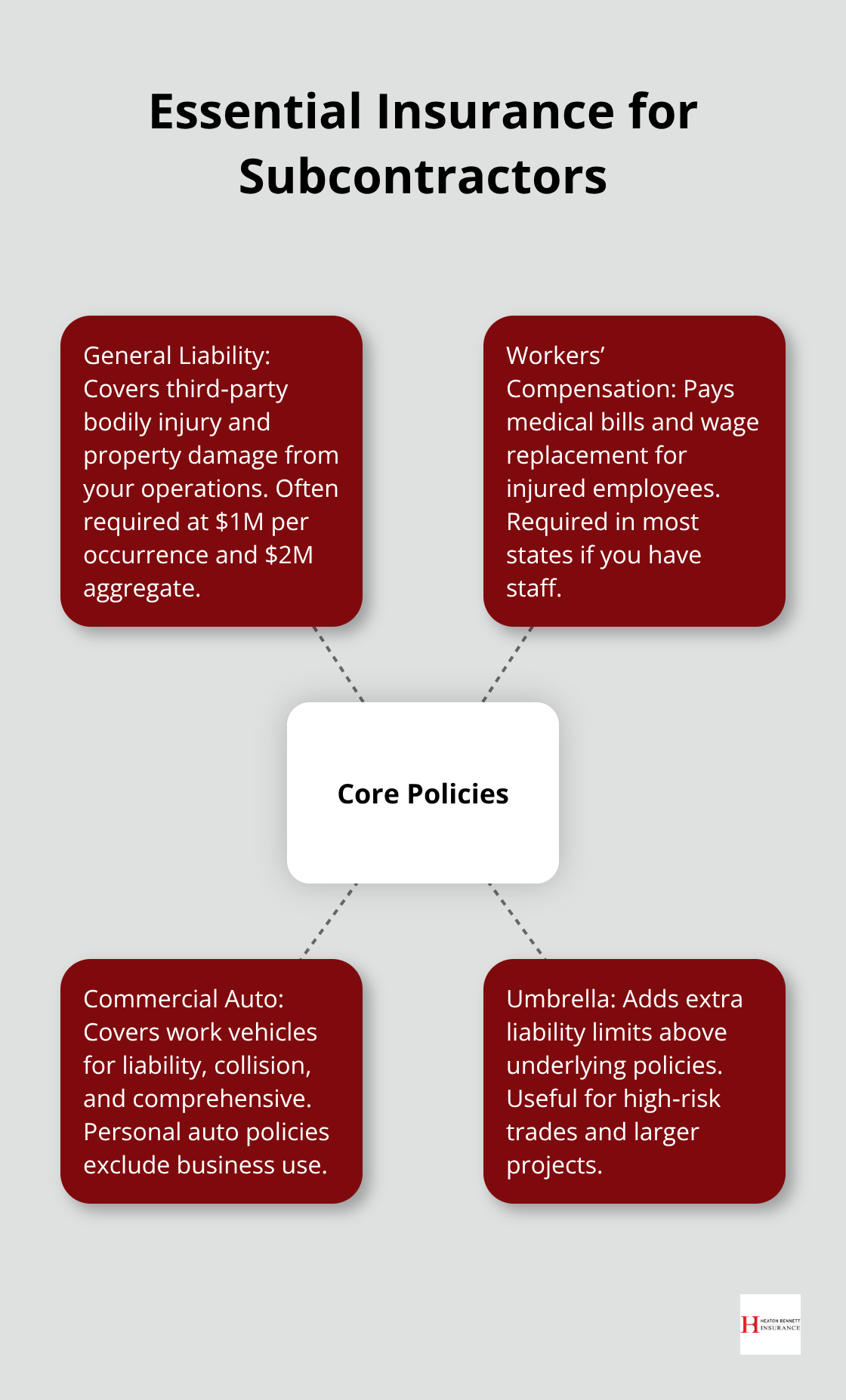

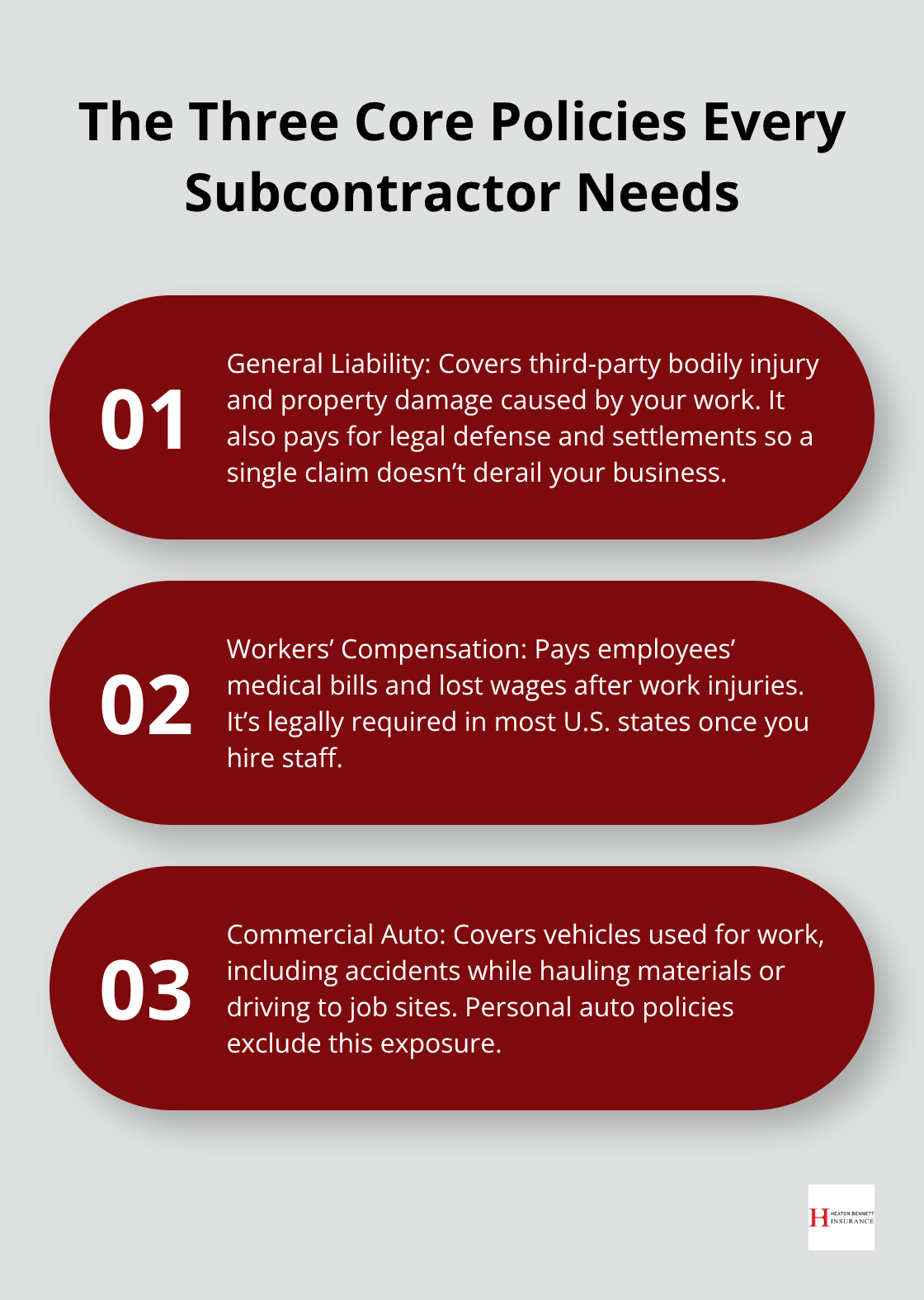

The Three Core Policies Every Subcontractor Needs

General liability insurance protects you when your work causes bodily injury or property damage to someone else, covering legal defense costs and settlements. Workers’ compensation covers your employees’ medical expenses and lost wages if they’re injured on the job, which is legally required in most states once you hire staff.

Commercial auto insurance covers vehicles used for work, protecting you from liability if you cause an accident while transporting materials or traveling to job sites. Without these three core policies, you’re personally liable for costs that could exceed your annual revenue.

Insurance as a Competitive Requirement

Many general contractors and property owners now require proof of specific coverage limits before hiring subcontractors, making insurance a competitive necessity. Contracts increasingly demand that you name the property owner and general contractor as additional insureds on your general liability policy, which protects them if your work causes damage. Failing to meet these contractual insurance requirements results in contract termination and loss of future work opportunities. The contractors and property owners you want to work with won’t hire you without proper coverage in place.

What Coverage Do Subcontractors Actually Need

General Liability: The Foundation of Protection

General liability insurance protects you when your work injures someone or damages their property, but the coverage limits matter more than most subcontractors realize. A $1 million general aggregate limit sounds substantial until a single claim exhausts it, leaving you exposed for everything beyond that threshold. Construction industry data shows that property damage claims from subcontractor work average between $50,000 and $150,000 depending on the trade, which means a $2 million aggregate limit is the practical minimum for any established subcontractor.

Your general liability policy must also include products and completed operations coverage, which protects you against claims that arise months or years after you finish the job. A roof leak discovered six months post-installation or a deck collapse a year later both qualify for this protection. When general contractors require you to name them as additional insureds, they’re protecting themselves from your liability exposure, and refusing this endorsement typically disqualifies you from the bid. Most commercial projects now demand proof that your policy includes this additional insured endorsement before work begins.

Workers’ Compensation: A Legal Mandate with Real Costs

Workers’ compensation insurance is legally mandatory in nearly every state the moment you hire your first employee, and New York enforces this through the Construction Fair Play Act with penalties that can reach $1,000 per day of non-compliance. The coverage pays for medical treatment and replaces lost wages, typically at two-thirds of the employee’s average weekly wage, which means a serious injury can cost your business tens of thousands in claims over months or years.

Subcontractors often underestimate their workers’ compensation costs because rates vary dramatically by trade. Roofing and excavation carry the highest rates at 15 to 25 percent of payroll, while carpentry and general labor sit around 5 to 8 percent. Understanding your specific trade’s rate helps you budget accurately and avoid surprises during policy renewal.

Commercial Auto: Beyond Personal Coverage

Commercial auto insurance covers liability if you cause an accident while using a vehicle for work, but your personal auto policy explicitly excludes this coverage, making it illegal to operate work vehicles without a commercial policy in place. A single accident causing injuries or property damage to a third party can trigger a liability judgment exceeding $500,000, which your personal auto policy won’t cover, leaving you personally responsible for the full amount.

This gap between personal and commercial coverage represents one of the most dangerous exposures subcontractors face. Your insurance broker can help you determine whether you need a commercial auto policy, a commercial general liability endorsement, or both, depending on how frequently you use vehicles for work and what you transport.

Selecting an Insurance Provider That Understands Your Trade

Why Generic Agents Fall Short

Choosing an insurance provider matters far more than most subcontractors realize, and the wrong choice will cost you thousands in unnecessary premiums or inadequate coverage when you need it most. Generic insurance agents who handle homeowner policies and personal auto coverage lack the construction expertise needed to identify your actual exposure. An agent unfamiliar with your trade cannot assess whether you face fall hazards, handle hazardous materials, or perform work that carries post-completion liability. Without this knowledge, they quote generic policies that either overcharge you for unnecessary coverage or leave dangerous gaps in protection.

Ask the Right Questions Before Committing

Start with brutal honesty about your operation’s size and risk level. A solo electrician working alone faces fundamentally different exposures than a roofing contractor with five employees and a fleet of vehicles, and your insurance must reflect that reality. Insurance brokers who ask detailed questions about your specific trade, the types of projects you undertake, your payroll size, and your equipment investments are the ones who build accurate coverage. Your agent should ask about your highest-value projects, your worst-case injury scenarios, and your contractual insurance requirements before recommending coverage limits. This investigation phase takes time, but it prevents you from overpaying for coverage you don’t need or discovering coverage gaps after a claim occurs.

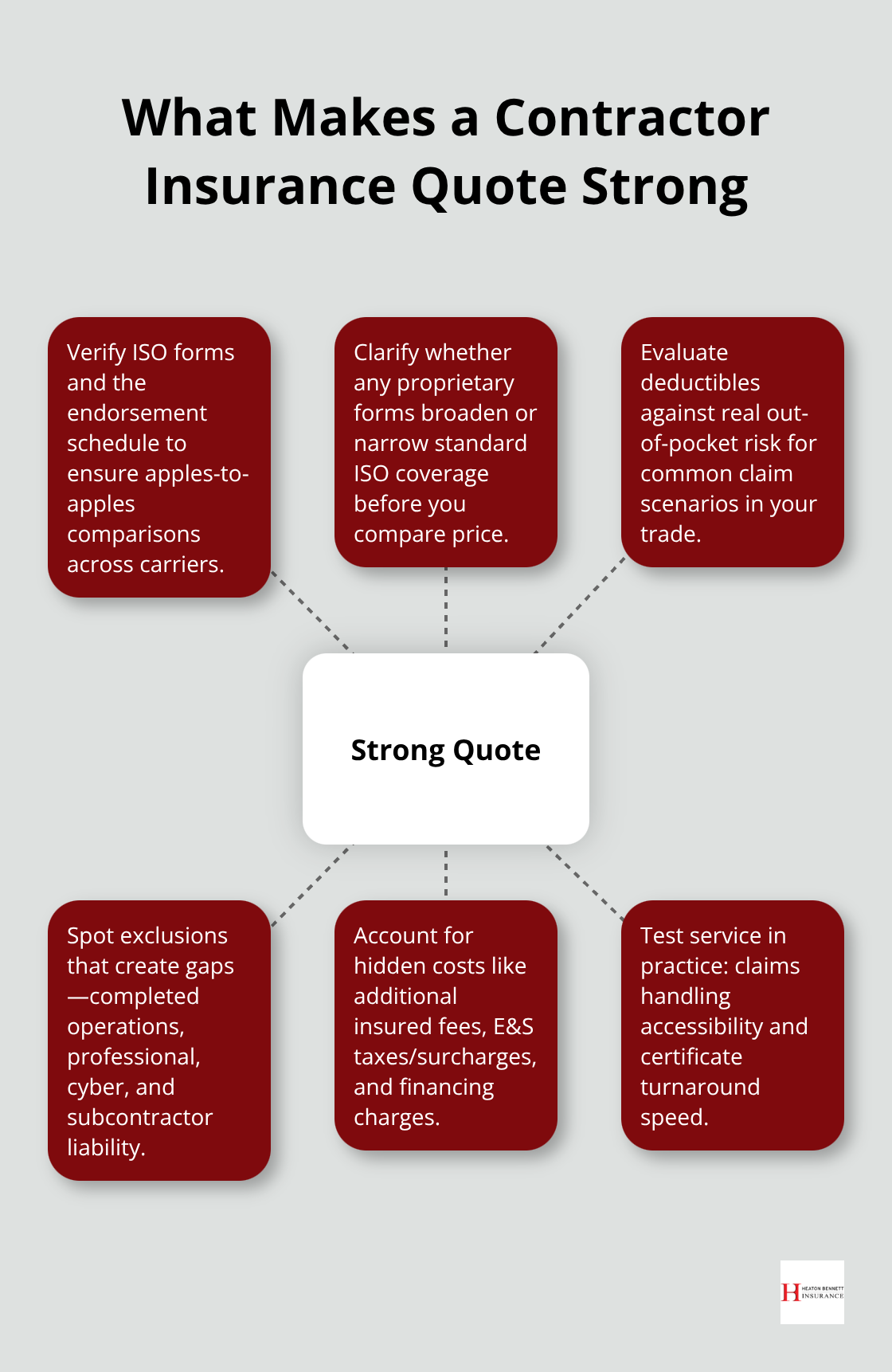

Compare Quotes Across Multiple Carriers

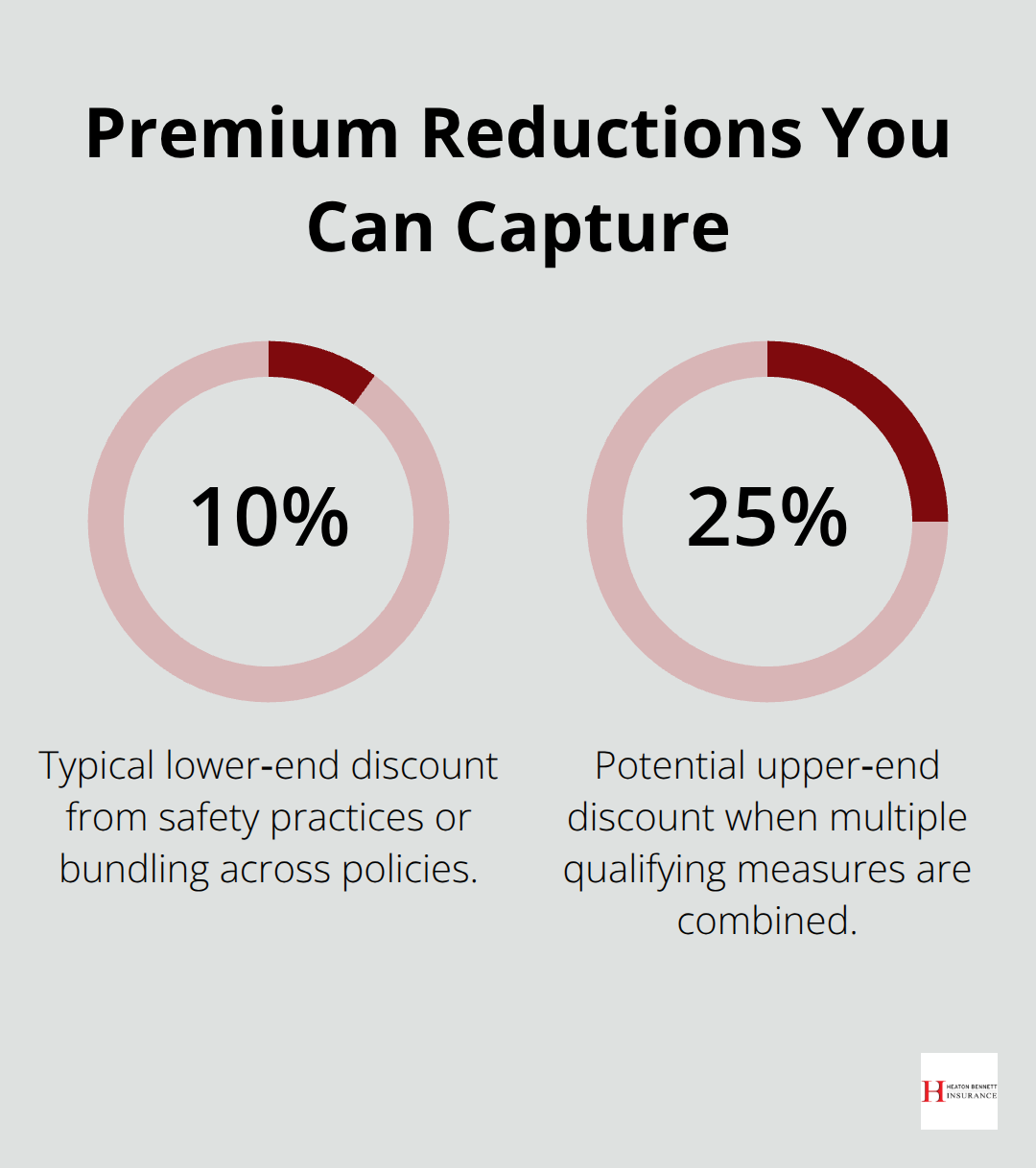

Insurance rates for the same trade vary substantially across carriers, sometimes by 30 to 40 percent for identical coverage, which means comparing quotes directly impacts your bottom line. Request quotes from at least three carriers for your specific trade before making a decision, and ask each insurer about available discounts for safety training, claims-free history, or multiple policies bundled together. Carriers often offer 10 to 15 percent reductions for completing OSHA training or maintaining excellent safety records (savings that accumulate significantly over multiple years of coverage).

Verify Carrier Access and Flexibility

An independent agency with access to multiple carriers can match your specific risk profile to the insurers offering the best rates and coverage for your trade rather than forcing you into one carrier’s limited options. This flexibility matters because some carriers specialize in roofing while others focus on electrical work, and the best rates come from carriers who understand your specific trade. Ask your broker whether they represent multiple carriers and how they select which insurer handles your policy.

Prioritize Trade-Specific Expertise

Your insurance broker must understand construction work, not just insurance products. A broker who asks whether you work at height, handle hazardous materials, or perform work that carries post-completion liability demonstrates the expertise you need. Those who quote you coverage without understanding these details are cutting corners and will likely miss critical exposures that could leave you unprotected when claims occur.

Final Thoughts

Your coverage needs shift as your business grows, your equipment investments increase, and your project scope expands. A policy that protected you five years ago may leave dangerous gaps today, which is why annual reviews with your insurance broker matter. Insurance for subcontractors requires expertise that goes beyond standard policies, and working with a broker who understands your trade beats shopping for the cheapest quote every time.

Start by documenting your current operation honestly: how many employees you have, what vehicles you use for work, what equipment you own, and what types of projects you typically undertake. Then contact an independent agency with access to multiple carriers who can match your specific risk profile to insurers that specialize in your trade. Request quotes from at least three carriers and ask about discounts for safety training or claims-free history before making your decision.

Your next step is straightforward: reach out to Heaton Bennett Insurance and schedule a conversation about your specific operation. We work with you through a personalized process to build coverage that actually protects your business. Protecting your business starts with a single conversation.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.