Contractor Subcontractor Insurance: Why It Matters for Project Risk

Contractor subcontractor insurance is one of the most overlooked aspects of project management, yet it’s where most construction companies face their biggest financial losses.

At Heaton Bennett Insurance, we’ve seen too many projects derailed because general contractors assumed their subcontractors had adequate coverage-only to discover critical gaps when claims arose. The reality is that insurance misalignment between tiers creates exposure that can cost you thousands or even shut down operations entirely.

Who Controls the Work, and Why It Matters for Insurance

The distinction between a general contractor and a subcontractor isn’t just paperwork-it directly determines who bears financial responsibility when things go wrong. A subcontractor is technically an independent party hired to complete specific tasks within a defined scope, yet general contractors often exercise varying degrees of control over how subcontractors perform their work. This control spectrum creates confusion about liability allocation and insurance responsibility. The more a general contractor dictates how work gets done, supervises daily activities, or controls work schedules, the more that contractor can be held liable for subcontractor errors. Construction Executive research highlights that merely labeling someone as a subcontractor provides no shield if the hiring contractor actually controls the work. This means a general contractor who micromanages a subcontractor’s crew, specifies work methods, or maintains day-to-day oversight has created a liability exposure that their own insurance may not adequately cover.

Insurance Gaps at Multiple Tiers

Most construction projects involve multiple insurance layers that rarely align perfectly. A general contractor’s Commercial General Liability policy typically does not automatically extend to subcontractors unless the subcontractor is named as an additional insured through a specific endorsement like CG 20 10 or CG 20 37. Even when a subcontractor is listed as an additional insured on a general contractor’s policy, coverage often applies only to liability claims and excludes tools, equipment, and owned vehicles that the subcontractor operates on site. This creates a dangerous assumption: general contractors believe their policy covers subcontractor work when in reality significant gaps exist. Additionally, if a subcontractor is uninsured entirely, the general contractor or project owner may face direct financial liability for injuries, property damage, or legal defense costs. Workers’ compensation liability extends to the hiring party in many states when a contractor is uninsured, meaning the project owner could be responsible for employee medical expenses and lost wages despite having no control over that worker.

Where Contracts Fall Short

The contract between general contractor and subcontractor is where these coverage requirements should be explicitly defined, yet many contracts lack clear insurance mandates or fail to specify minimum limits and required endorsements. Subcontractors often submit certificates of insurance that appear valid but contain hidden gaps that only surface during claims. A certificate might list a $1 million general liability limit when the contract requires $2 million. A workers’ compensation certificate might show coverage for three employees when the subcontractor actually has five on the job. Renewal dates on certificates frequently slip past without notice, leaving projects operating under expired coverage.

Why Verification Fails in Practice

General contractors who don’t implement a formal Certificate of Insurance tracking system face these risks passively. The solution requires establishing clear prequalification standards before awarding any contract. Verify that the subcontractor’s insurance limits match contract requirements exactly, confirm that additional insured endorsements are in place and properly worded, and document proof of coverage renewal at least 30 days before policy expiration. High-risk trades like electrical work, roofing, and heavy equipment operation carry inherently dangerous activities that courts consider non-delegable-meaning the general contractor retains liability regardless of contract language. For these trades, requiring higher coverage limits and specialized endorsements isn’t optional; it’s a legal necessity that protects your operation from catastrophic exposure.

Building Your Verification Process

The next step involves moving beyond passive certificate collection to active risk management. You need systems that track renewal dates, flag coverage gaps, and alert you when policies approach expiration. This foundation sets the stage for understanding how to select subcontractors strategically and align their insurance with your project’s actual risk profile.

What Happens When Your GC Policy Doesn’t Cover Subcontractor Work

Your general contractor’s commercial general liability policy creates a false sense of security. Most GC policies do not automatically extend coverage to subcontractors performing work on your projects. Coverage applies only if the subcontractor is formally named as an additional insured through specific endorsements like CG 20 10 or CG 20 37, and even then, protection remains limited. The policy covers liability claims that arise from the subcontractor’s negligence, but it excludes tools, equipment, vehicles, and owned property that the subcontractor brings to the job site.

The Hidden Gaps in Your Coverage

This distinction matters enormously in practice. A subcontractor’s power tools damaged by theft, a rental excavator involved in an accident, or a company vehicle used for material transport typically fall outside your GC policy’s scope. You face a choice: require the subcontractor to carry their own coverage for these assets, or accept the financial risk yourself. Many general contractors choose the first option but fail to verify it actually happens. The subcontractor signs the contract agreeing to carry equipment coverage, submits a certificate of insurance that looks legitimate, and then operates without it. When loss occurs, you discover the gap during the claims process, when it’s too late to recover costs.

Direct Liability When Subcontractors Lack Coverage

Uninsured subcontractors create direct liability for you in multiple jurisdictions. In many states, workers’ compensation law extends liability to the hiring party when a contractor is uninsured, meaning you could be responsible for an employee’s medical bills and lost wages despite having no control over their safety practices. Property damage claims work the same way. If an uninsured subcontractor damages a neighboring property or causes injury to a third party on site, your project owner or your GC insurance becomes the defendant’s only source of recovery.

Courts frequently hold general contractors liable for subcontractor negligence when the contractor exercises day-to-day control, fails to properly vet the subcontractor’s qualifications, or neglects to verify insurance requirements. The financial exposure is substantial. A single serious injury claim can exceed $500,000 in medical expenses and legal costs alone. Equipment damage on large projects regularly reaches six figures. Your GC policy’s aggregate limits can be exhausted by a single incident, leaving subsequent claims unprotected.

Three Steps to Protect Your Operation

The practical solution requires three concrete steps. First, establish minimum insurance requirements in every subcontract with specific dollar limits that match your project’s actual risk. Second, implement a formal verification system that checks certificates of insurance before work starts and tracks renewal dates throughout the project. Third, require subcontractors in high-risk trades to carry umbrella or excess liability coverage in increments of at least $1 million to protect against catastrophic claims that exceed primary policy limits.

These steps form the foundation of a resilient insurance strategy, but they only work when you understand which subcontractors pose the greatest risk and how to evaluate their qualifications before awarding contracts.

Building the Right Coverage Mix for Subcontractor Risk

Builders risk insurance and equipment coverage form the foundation of protecting assets on active job sites, yet most general contractors misunderstand what these policies actually cover and which party should carry them. Builders risk protects the structure under construction against loss from fire, theft, vandalism, and weather damage during the building phase, but it does not cover subcontractor-owned tools, equipment, or vehicles on site. This distinction creates immediate tension: if you require subcontractors to bring their own equipment to your project, you need written confirmation that they carry tools and equipment floaters on their policies.

Understanding Equipment Coverage Requirements

A tools floater covers repair or replacement of owned or rented equipment, including theft and vandalism, and it typically attaches to a general liability policy as an endorsement. Most subcontractors skip this coverage to reduce insurance costs, then submit a certificate showing general liability without mentioning the missing equipment protection. Your builders risk policy will not fill this gap. When a subcontractor’s drill press gets stolen from the job site or a rented compressor suffers damage, the subcontractor expects you to cover it under your builders risk, but your policy excludes it.

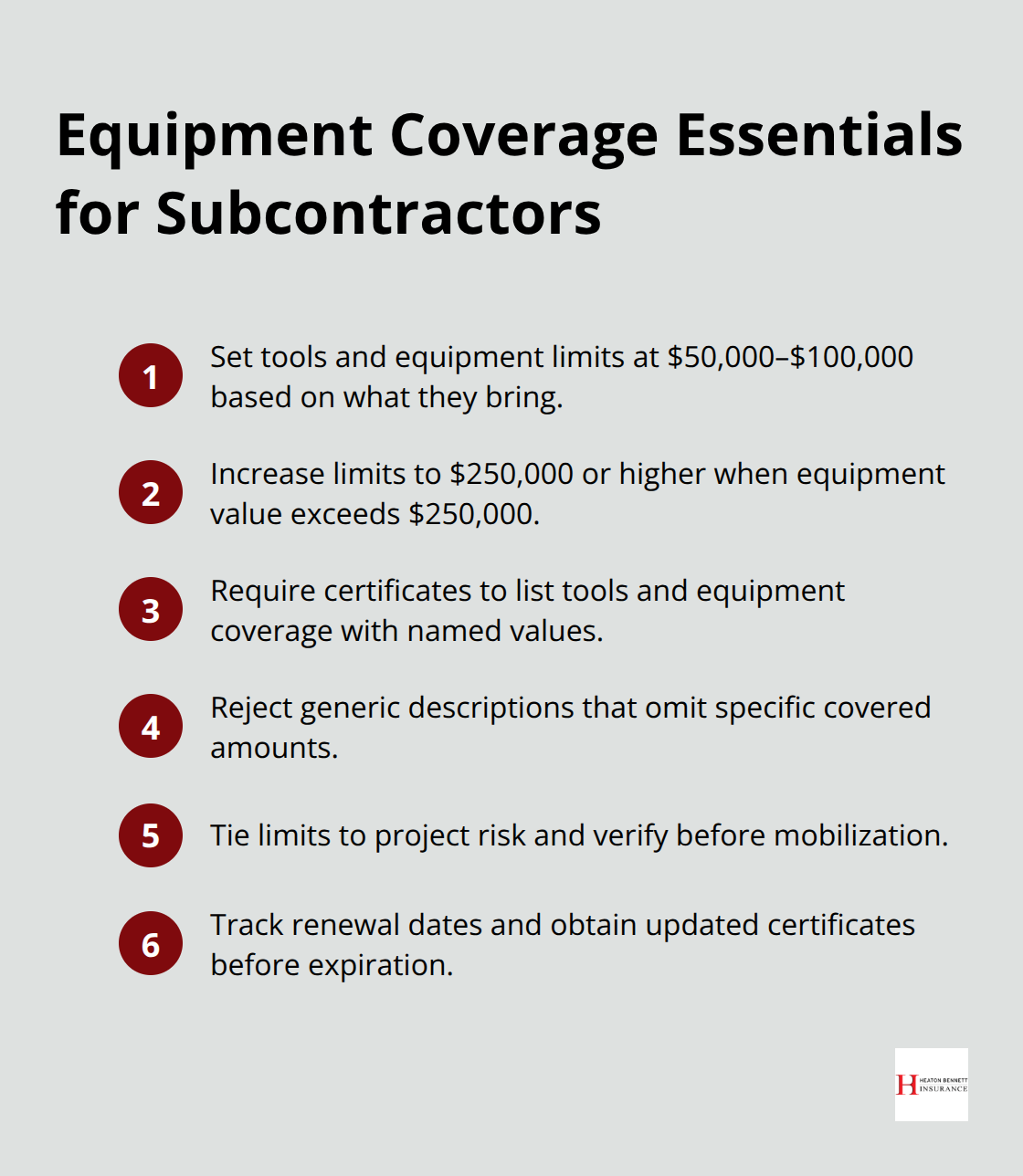

The practical solution requires you to demand that subcontractors carry equipment coverage with minimum limits of $50,000 to $100,000 depending on the equipment they bring. For major projects where equipment value exceeds $250,000, you should increase limits to $250,000 or higher. Request that the certificate of insurance specifically lists tools and equipment coverage with named values rather than generic descriptions.

Verifying Primary and Non-Contributory Language

Certificate of insurance verification has become a compliance necessity rather than an administrative task, yet most general contractors treat it as a checkbox exercise. The industry standard requires that subcontractor certificates include primary and non-contributory language, meaning the subcontractor’s insurance pays first and does not share costs with your policy. Without this language, your insurance becomes the primary payer when a subcontractor causes damage, defeating the entire purpose of requiring them to carry coverage.

Verify that additional insured endorsements CG 20 10 and CG 20 37 appear on the certificate with correct policy numbers and effective dates. Many subcontractors submit outdated certificates or certificates for policies that have already expired. You should implement a system that flags renewal dates 30 days before expiration and requires updated certificates before the old ones lapse.

Umbrella Coverage for High-Risk Trades

For high-risk trades like roofing, electrical work, and heavy equipment operation, you must require umbrella or excess liability coverage in $1 million increments because inherently dangerous activities carry non-delegable liability that your primary coverage limits may not absorb. A roofing subcontractor with only $1 million in general liability coverage poses inadequate protection when a fall from height causes a catastrophic injury claim that reaches $3 million. The subcontractor should carry a $2 million umbrella policy stacked above their primary coverage.

Making Insurance a Material Contract Condition

You should document these requirements in writing within the subcontract itself, not in separate emails or verbal agreements. Courts recognize written contract terms as enforceable whereas informal communications become disputes. Include contract language that explicitly states the subcontractor maintains insurance as a material condition of the agreement, meaning failure to maintain coverage gives you grounds to suspend work immediately without waiting for a claim to arise.

Final Thoughts

A single catastrophic claim exceeds your annual insurance premiums by a factor of ten, making contractor subcontractor insurance a financial necessity rather than an optional expense. Serious injuries on site cost $500,000 or more in medical expenses and legal defense, while equipment theft regularly reaches six figures. When you calculate the actual risk exposure on your projects, requiring subcontractors to carry proper coverage becomes the only rational business decision.

Vetting subcontractors for adequate insurance means moving beyond passive certificate collection to active verification before work starts. Verify that their coverage limits match your project requirements exactly, confirm that additional insured endorsements appear with correct policy numbers, and document proof of renewal at least 30 days before expiration. Request that certificates specifically list tools and equipment coverage with named values rather than generic descriptions, and demand umbrella coverage in $1 million increments for high-risk trades like roofing and electrical work.

Establish minimum insurance requirements in every subcontract with specific dollar limits tied to actual project risk, implement a formal tracking system that monitors renewal dates and flags coverage gaps, and make insurance maintenance a material contract condition that gives you grounds to suspend work immediately if coverage lapses. Contact our team in Austin to review your current contractor subcontractor insurance strategy and identify gaps before they become claims.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.