How to Get Personal Workers Compensation Insurance

At Heaton Bennett Insurance, we understand the importance of protecting yourself as a self-employed individual or independent contractor. Personal workers’ compensation insurance offers a safety net for those who don’t qualify for traditional coverage.

This guide will walk you through the process of obtaining personal workers’ compensation insurance, helping you safeguard your income and health in case of work-related injuries or illnesses.

What Is Personal Workers Compensation Insurance?

Definition and Purpose

Personal workers’ compensation insurance provides coverage for self-employed individuals and independent contractors who don’t have access to traditional employer-provided workers’ comp. This specialized insurance protects against financial losses due to work-related injuries or illnesses.

Target Audience

Self-employed professionals, freelancers, and independent contractors are the primary candidates for personal workers’ compensation insurance. If you run a one-person business or work as a contractor, you likely lack coverage under a company’s workers’ comp policy. This leaves you exposed to potential financial hardship if you sustain an injury on the job.

Differences from Traditional Coverage

Personal workers’ comp differs from traditional coverage in several ways:

- Purchase method: Individuals buy it directly, not employers.

- Customization: It’s tailored to cover unique risks faced by self-employed workers.

- Flexibility: Coverage can adapt to various professions (e.g., freelance photographers, self-employed carpenters).

Financial Protection

Personal workers’ compensation acts as a financial safety net by typically covering:

- Medical expenses related to work injuries

- Income replacement for work-related injuries or illnesses

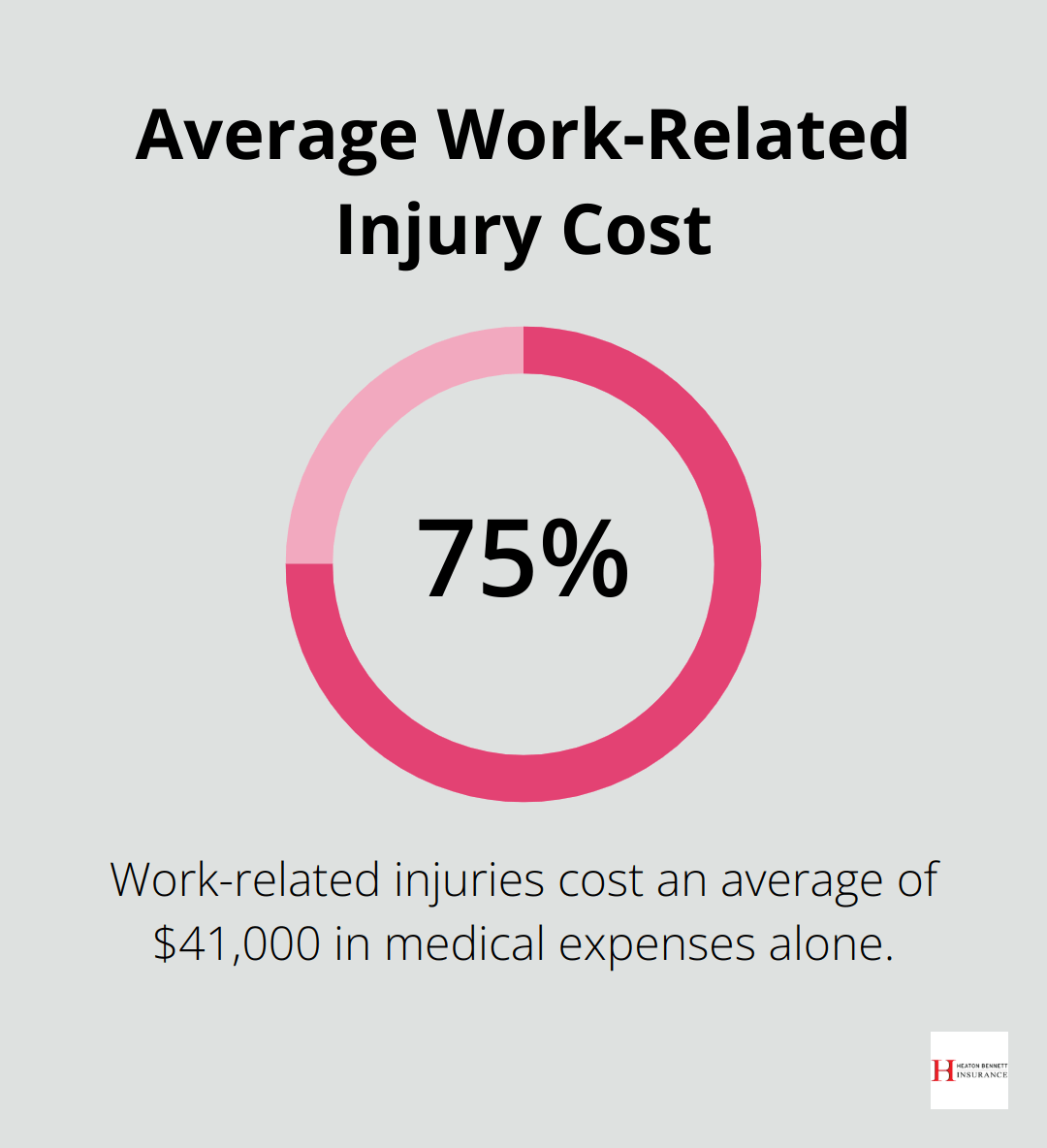

This protection is vital for self-employed individuals who might otherwise face substantial out-of-pocket expenses or income loss during recovery. The Bureau of Labor Statistics reports that the average cost of a work-related injury is $41,000 in medical expenses alone (a potentially devastating amount for a self-employed person).

Importance for Self-Employed Individuals

All self-employed individuals should consider personal workers’ compensation insurance. It’s not just about complying with state laws – it’s about safeguarding your livelihood and ensuring you can provide for yourself and your family, even in unexpected circumstances.

As we move forward, let’s explore the steps to obtain personal workers’ compensation insurance and ensure you have the right coverage for your unique needs.

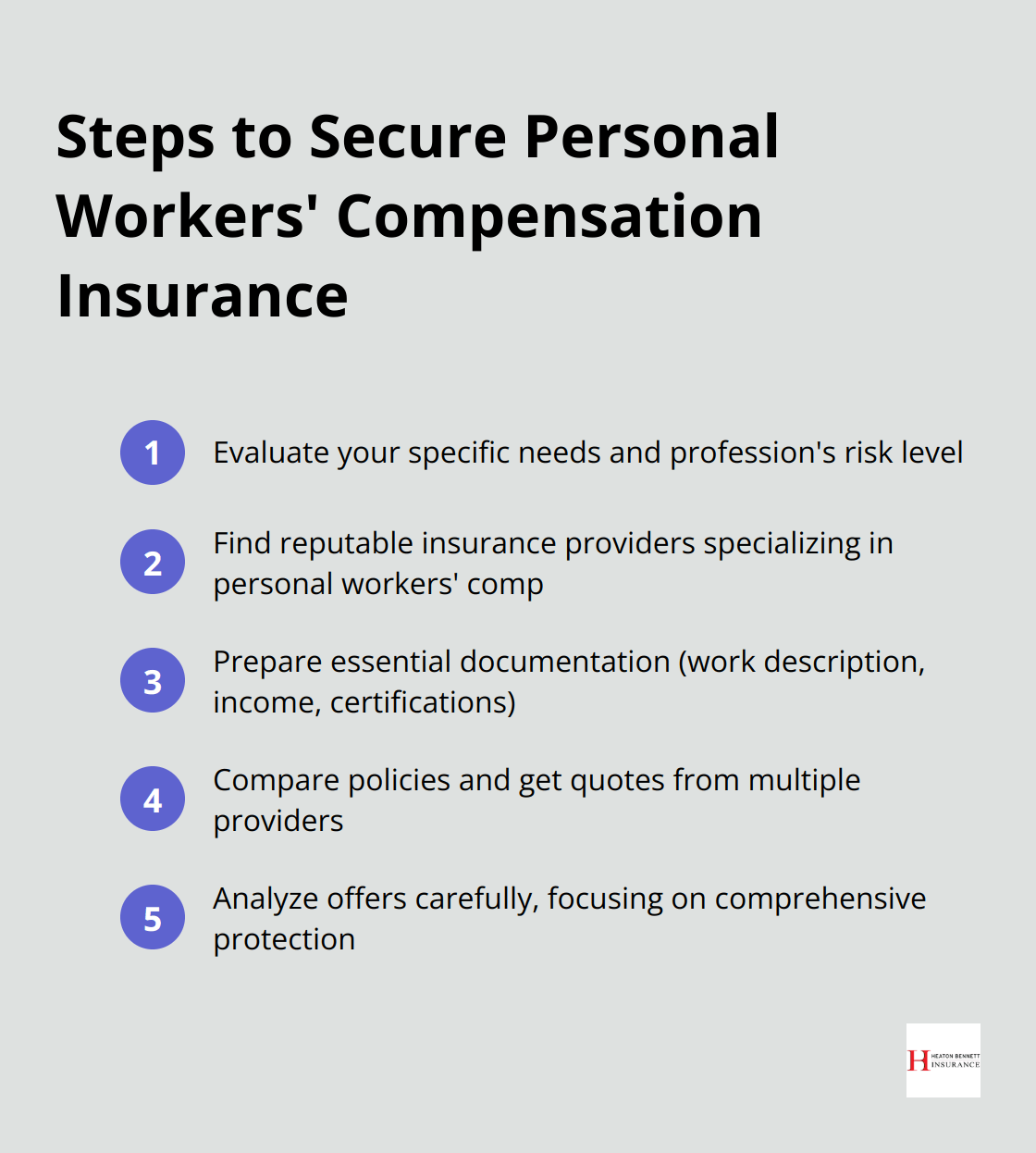

How to Secure Personal Workers Compensation Insurance

Evaluate Your Specific Needs

Start by assessing your profession’s risk level. A construction contractor faces different hazards than a freelance writer. Consider your work environment, tools used, and potential injuries. This evaluation helps determine the coverage amount you need.

Check your state’s requirements. Some states mandate personal workers’ comp for certain professions. Texas doesn’t require it for most self-employed individuals, but specific industries may have different rules.

Find Reputable Insurance Providers

Research insurance companies that specialize in personal workers’ compensation. Look for providers with experience in your industry. The National Association of Insurance Commissioners (NAIC) website offers valuable resources for checking an insurer’s reputation and financial stability.

Don’t overlook local independent agencies (like Heaton Bennett Insurance). They often have access to multiple carriers and can provide personalized guidance tailored to your specific situation.

Prepare Your Documentation

Gather essential information before you apply. This typically includes:

- Detailed description of your work activities

- Annual income or projected revenue

- Business license or professional certifications

- Any previous work-related injury history

Having this information ready streamlines the application process and ensures accurate quotes.

Compare Policies and Get Quotes

Request quotes from multiple providers. Don’t just focus on price – consider coverage limits, exclusions, and additional benefits. Some policies might offer extras like coverage for temporary disability or rehabilitation services.

Pay attention to the claims process. A straightforward, efficient claims procedure can be crucial when you’re injured and unable to work. Ask about average claim processing times and customer satisfaction rates.

Try to get at least three quotes to compare. Analyze these offers carefully, ensuring you understand the fine print and potential gaps in coverage.

The cheapest option isn’t always the best. Focus on finding a policy that provides comprehensive protection for your specific needs. With the right personal workers’ compensation insurance, you can work with confidence, knowing you’re protected against unforeseen work-related injuries or illnesses.

As you move forward in your search for the ideal personal workers’ compensation insurance, it’s important to consider several key factors that will influence your decision. Let’s explore these critical elements in the next section.

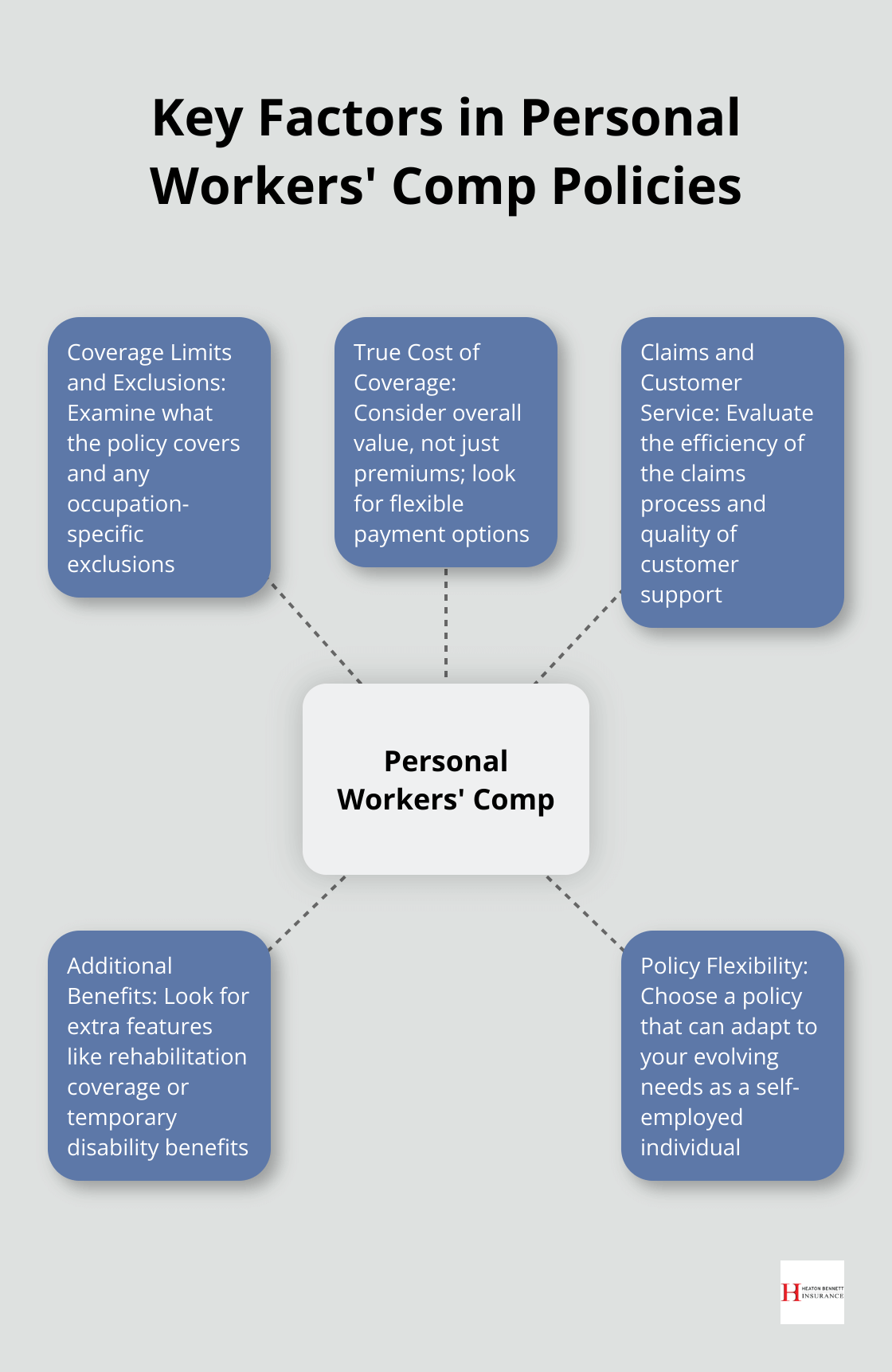

What Matters Most in Personal Workers’ Comp Policies?

Coverage Limits and Exclusions

The core of any workers’ comp policy consists of its coverage limits and exclusions. Low premiums should not distract you from examining what the policy actually covers. Some policies exclude certain injury types or cap medical expense reimbursements at levels that could leave you financially exposed.

A policy with a $100,000 medical expense limit might appear adequate, but severe injuries can quickly surpass this amount. The National Safety Council reports that the average cost of a disabling workplace injury is $39,000 (with more serious injuries potentially costing much more).

Focus on occupation-specific exclusions. Freelance photographers should ensure their policy covers injuries that could occur during on-location shoots. Contractors must verify coverage for falls from heights or injuries from power tools.

The True Cost of Coverage

Premium costs matter, but they shouldn’t be your sole focus. Examine the overall value proposition. A slightly higher premium might offer substantially better coverage or lower deductibles (potentially saving you thousands in the event of a claim).

Many insurers offer flexible payment options, including monthly installments or pay-as-you-go plans that adjust based on your actual income. These options can benefit freelancers with fluctuating earnings.

Consider long-term costs as well. Some policies offer discounts for maintaining a safe work record or completing safety training programs. These safety investments can lead to lower premiums over time.

Efficiency in Claims and Customer Service

The real test of an insurance policy occurs when you file a claim. A streamlined claims process can mean the difference between focusing on your recovery and battling bureaucracy while injured.

Search for insurers with dedicated claims teams for self-employed individuals. Ask about their average claim processing times and whether they offer 24/7 claim reporting. Some providers now offer mobile apps for easy claim submission and tracking.

Customer service quality holds equal importance. Check reviews and ratings from other self-employed professionals in your industry. The National Association of Insurance Commissioners (NAIC) provides a complaint index that can give you insight into an insurer’s customer service record.

Additional Benefits and Riders

Some personal workers’ comp policies offer extra benefits that can provide significant value. These may include:

- Rehabilitation coverage

- Temporary disability benefits

- Coverage for specialized equipment

Evaluate these additional features carefully. They might justify a slightly higher premium if they align with your specific needs and risks.

Policy Flexibility and Scalability

As a self-employed individual, your work situation may change over time. Choose a policy that can adapt to your evolving needs. Some insurers offer policies that can scale with your business growth or adjust coverage based on seasonal fluctuations in your work.

Workers’ compensation insurance acts as a safety net for self-employed professionals, covering medical expenses and lost wages if you suffer an injury or illness related to your work. It’s crucial to understand the specifics of your policy to ensure you have the protection you need.

Final Thoughts

Personal workers’ compensation insurance protects self-employed individuals from financial hardship due to work-related injuries. It fills the gap left by traditional employer-provided coverage and offers essential protection for independent contractors. We recommend you evaluate your specific needs, research reputable providers, and compare policies to find the right coverage for your unique situation.

At Heaton Bennett Insurance, we understand the complexities of personal workers’ compensation insurance. Our team can guide you through the process and help you find the right coverage to protect your livelihood. We offer access to multiple carriers and can tailor a solution that meets your specific needs.

Visit our website to learn more about how we can help secure your future with personal workers’ compensation insurance. Investing in this type of insurance is a smart business decision that protects your income, health, and future. Take the time to research and consult with insurance professionals to ensure you have the right coverage in place.