Restaurant Property Coverage: Insuring Your Venue and Inventory

Your restaurant is one of your biggest investments, and protecting it requires more than just a standard business policy. Restaurant property coverage shields your building, equipment, and inventory from the losses that hit hardest-fire, weather, theft, and more.

At Heaton Bennett Insurance, we help restaurant owners understand exactly what they need to protect their operations. The right coverage limits make the difference between a temporary setback and a financial crisis.

What Restaurant Property Coverage Actually Protects

Restaurant property coverage protects three critical areas that directly impact your ability to operate. Your building structure comes first-whether you own the space or lease it, coverage protects the walls, roof, foundation, and permanent fixtures from fire, weather damage, theft, and vandalism.

If you lease, you need coverage for leasehold improvements like custom ventilation systems or kitchen build-outs you’ve installed. Commercial property insurance should extend to all inside assets including equipment, appliances, chairs, tables, and dishware. Many restaurant owners underestimate the cost of these improvements and face significant out-of-pocket expenses when damage occurs.

Equipment and Inventory Protection

Your equipment and furniture represent the second layer of protection. Commercial kitchen equipment, POS systems, dining furniture, and bar fixtures all need coverage against damage and loss. Equipment breakdown coverage pays for repairs or replacement when critical devices like coolers or refrigeration units fail unexpectedly, and it covers lost income when essential equipment stops working. Food spoilage coverage protects your high-value perishable inventory during extended power outages or mechanical failures-a relatively affordable protection compared to the losses you’d face without it.

Inventory and stock form the third essential component. Your coverage should protect ingredients, finished products, and supplies from theft, fire, and damage in transit. Business personal property coverage protects movable items from damage or theft, ensuring you recover the full replacement value of everything inside your restaurant.

Setting Coverage Limits That Match Your Reality

Setting the right coverage limits determines whether you recover quickly or face a financial crisis. Most restaurants fail to account for seasonal inventory fluctuations-your stock value in December differs dramatically from January, yet many owners choose a single coverage limit year-round. You need coverage that reflects your highest inventory value during peak seasons.

Building value assessment requires calculating the cost to rebuild your restaurant from scratch, not just the market value of the property. Older buildings or wood-framed structures cost more to rebuild due to stricter modern building codes, so your coverage limit should reflect reconstruction costs, not the original purchase price. A licensed insurance agent who understands restaurant operations can set appropriate limits and help you avoid underinsurance, which leaves you paying out-of-pocket for losses exceeding your policy limits.

Common Risks Restaurants Face and How Coverage Addresses Them

Fire and Smoke Damage

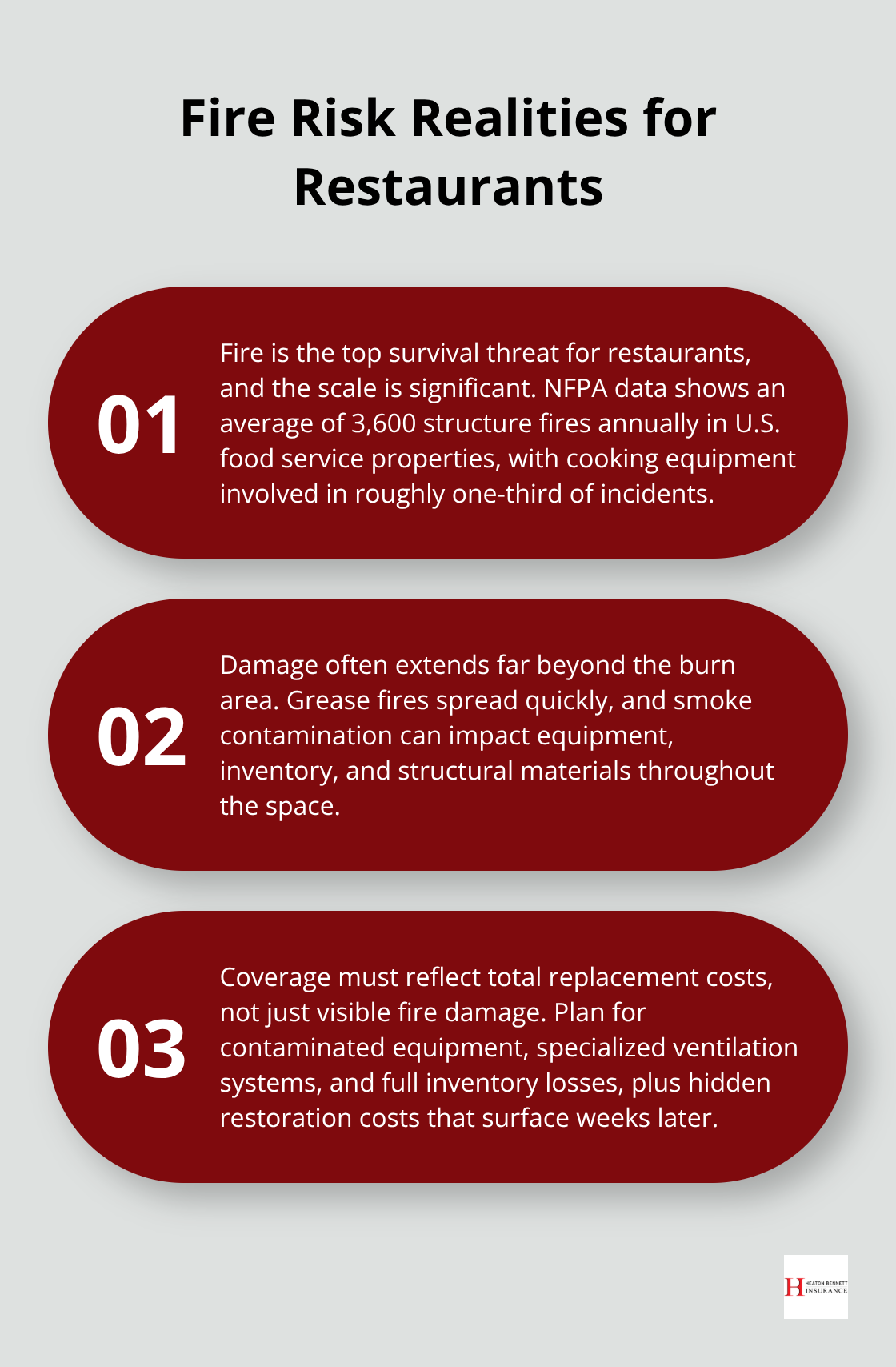

Fire remains the single greatest threat to restaurant survival, and the statistics back this up. The National Fire Protection Association reports that structure fires in food service properties cause an average of 3,600 fires annually in the United States, with cooking equipment involved in roughly one-third of all reported restaurant fires.

Grease fires spread faster than most restaurant owners anticipate, and smoke damage extends far beyond the immediate burn area, contaminating equipment, inventory, and structural materials throughout your space.

Property coverage protects against fire and smoke damage, but the real challenge lies in ensuring your coverage limit reflects the total replacement cost of everything affected. Many owners discover after a fire that their coverage falls short because they failed to account for the cost of replacing contaminated equipment that cannot be salvaged, specialized ventilation systems, or the full inventory lost to smoke exposure. Your property policy should cover not just the obvious fire damage but also the hidden costs of restoration and replacement that emerge weeks after the initial incident.

Weather-Related Damage and Natural Disasters

Heavy rain, hail, and flooding damage refrigeration units, spoil inventory, and compromise structural integrity, yet many restaurant owners carry inadequate weather coverage or skip flood insurance entirely because they assume their location will not be affected. According to data from insurance industry sources, weather-related business interruptions cost restaurants an average of $10,000 to $50,000 in lost revenue during closure periods, making business interruption coverage essential alongside property protection.

Your property coverage should explicitly address the specific weather threats in your region. Restaurants in flood-prone areas need separate flood insurance, as standard property policies exclude flood damage. Those in hail-prone regions should verify that their coverage includes hail damage to roofs and exterior equipment. Working with an insurance agent who understands your local climate risks helps you avoid gaps in protection that could leave you exposed when severe weather strikes.

Theft and Vandalism

Theft and vandalism target restaurants specifically because they contain high-value portable items like copper piping, outdoor equipment, and technology. Criminals know restaurants operate during predictable hours and often have limited security measures in place. Outdoor seating areas, loading docks, and storage spaces present particular vulnerability, and theft coverage protects not just the stolen items but also covers the cost of emergency replacements needed to keep operations running.

Your property coverage should explicitly include theft protection for equipment, inventory, and fixtures. Work with your insurance agent to identify which outdoor or exposed assets need additional specialized coverage based on your specific location and layout. Once you understand which risks threaten your restaurant most, determining the right coverage limits becomes the next critical step in protecting your investment.

How to Determine the Right Coverage Limits for Your Restaurant

Rebuild Costs, Not Market Value

Setting coverage limits requires far more precision than most restaurant owners invest. The fundamental mistake happens when owners use their property’s purchase price or current market value as their coverage limit. That approach fails completely because rebuilding costs exceed market value dramatically, especially in older buildings subject to modern building codes. A restaurant in a 1970s structure with wood framing costs significantly more to rebuild than an identical operation in a newer steel-frame building because updated fire codes, electrical systems, and structural requirements drive reconstruction expenses higher.

You need to calculate the actual cost to rebuild your restaurant from the ground up, including all structural components, mechanical systems, and finishes. A licensed insurance agent who understands restaurant construction can provide a detailed replacement cost analysis that reflects your specific building type, age, and local construction costs. This analysis forms the foundation for setting appropriate coverage limits that actually protect you when disaster strikes.

Account for Seasonal Inventory Swings

Inventory valuation demands attention to seasonal patterns that most owners overlook entirely. Your December inventory value during holiday service differs dramatically from your January inventory after the post-holiday slowdown, yet many restaurants select a single annual coverage limit that leaves them underinsured during peak seasons or paying unnecessary premiums during slow periods. Document your highest inventory value during your busiest season, then work with your insurance agent to establish a coverage limit that reflects that peak value.

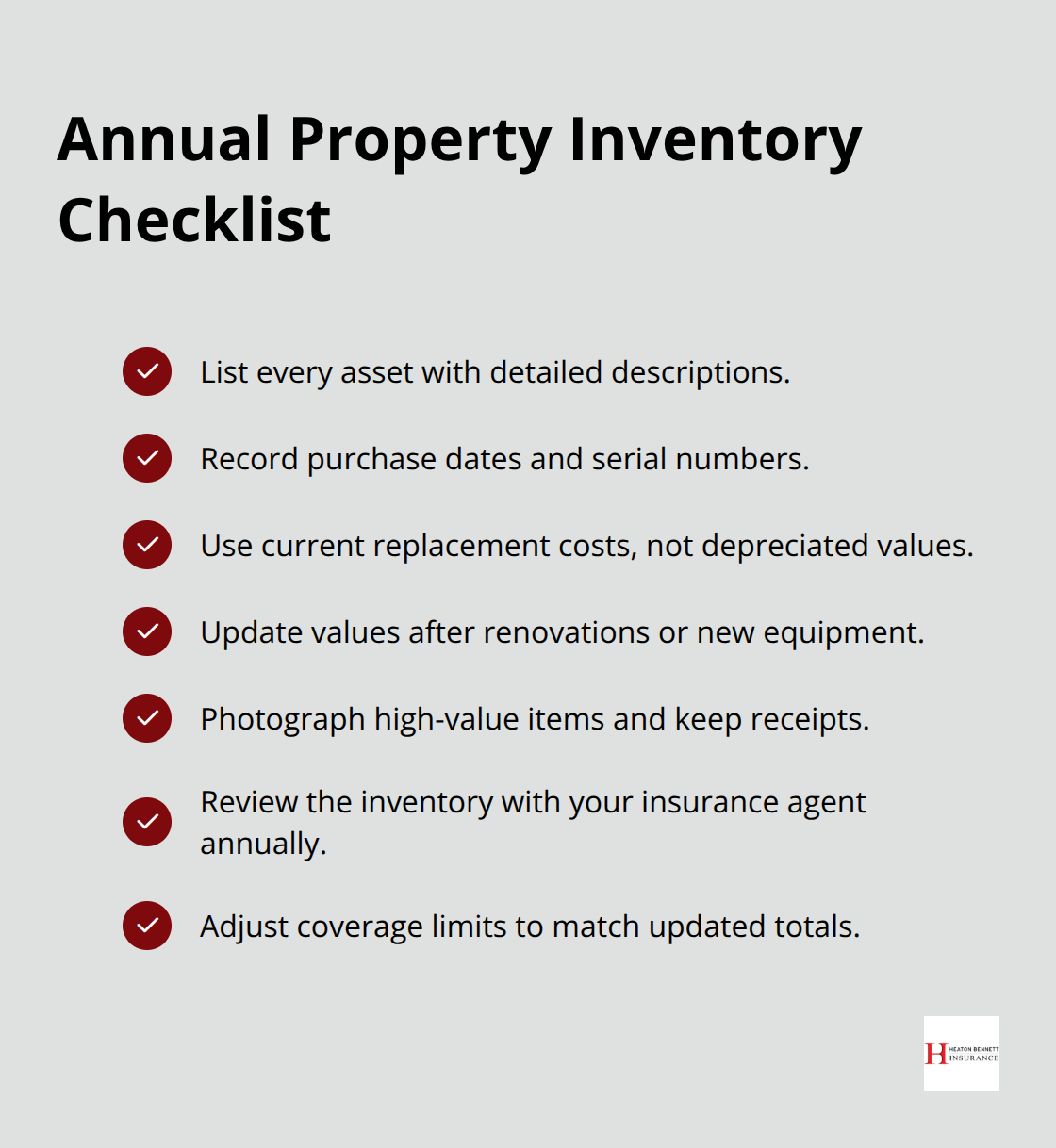

Equipment values matter equally, so catalog every piece of kitchen equipment, technology, furniture, and fixture with current replacement costs rather than depreciated values. Many restaurant owners discover after a loss that their coverage falls thousands of dollars short because they failed to account for the true replacement cost of specialized equipment like commercial-grade refrigeration or custom hood ventilation systems.

Update Your Asset Inventory Annually

Conduct a complete asset inventory annually, updating values as you add equipment or modify your space, then adjust your coverage limits accordingly to stay aligned with your actual property value. This practice prevents the common scenario where restaurants operate with outdated coverage limits that no longer match their current assets. Your inventory should include detailed descriptions, purchase dates, and current replacement costs for every item your restaurant depends on to operate.

When you work with an insurance agent to review this inventory, you establish coverage limits grounded in reality rather than guesswork.

Final Thoughts

Restaurant property coverage protects your most valuable business asset, but only when you set limits that match your actual exposure. The mistakes happen quietly-underestimating rebuild costs, ignoring seasonal inventory swings, or assuming your current policy still reflects what you own. These gaps between what you think you’re covered for and what you actually need create financial disasters when fires, weather, or theft strike.

Pull together your most recent property inventory, document your peak season inventory value, and calculate what it would cost to rebuild your restaurant from scratch. Compare those numbers against your current coverage limits, and if you discover gaps, you’re not alone-most restaurant owners find their restaurant property coverage falls short of their actual needs once they complete this exercise. An independent insurance agent who understands restaurant operations will walk you through the details that matter: building age, equipment values, seasonal fluctuations, and local risks.

Contact Heaton Bennett Insurance to review your current coverage and identify what you’re missing. Our team guides you through the specifics of your operation rather than forcing you into a one-size-fits-all package, and we help you build protection that matches your investment. The cost of getting this right is far less than the cost of being underinsured when disaster strikes.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.