Contractor Tool Coverage: A Practical Guide for Small Contractors

Your tools are your livelihood. When a drill goes missing from a job site or a truck gets broken into, you lose money fast.

Most standard business insurance won’t cover contractor tool coverage the way you need it to. That’s why we at Heaton Bennett Insurance created this guide to help you understand your options and protect what matters most to your business.

What Contractor Tool Coverage Actually Protects

Contractor tool coverage is inland marine insurance designed specifically for tools and equipment that move between job sites. Unlike standard business property insurance, which only covers items at a fixed business address, this coverage travels with your gear-whether that’s hand tools in your truck, power equipment at a client’s home, or machinery stored off-site. The policy reimburses you for repair or replacement costs when tools are stolen, damaged by impact or weather, or vandalized. For small contractors in construction, landscaping, electrical work, plumbing, and painting, this distinction matters enormously because your tools aren’t sitting safely in one location. They’re exposed to loss every single day on multiple job sites.

Why Standard Insurance Leaves You Exposed

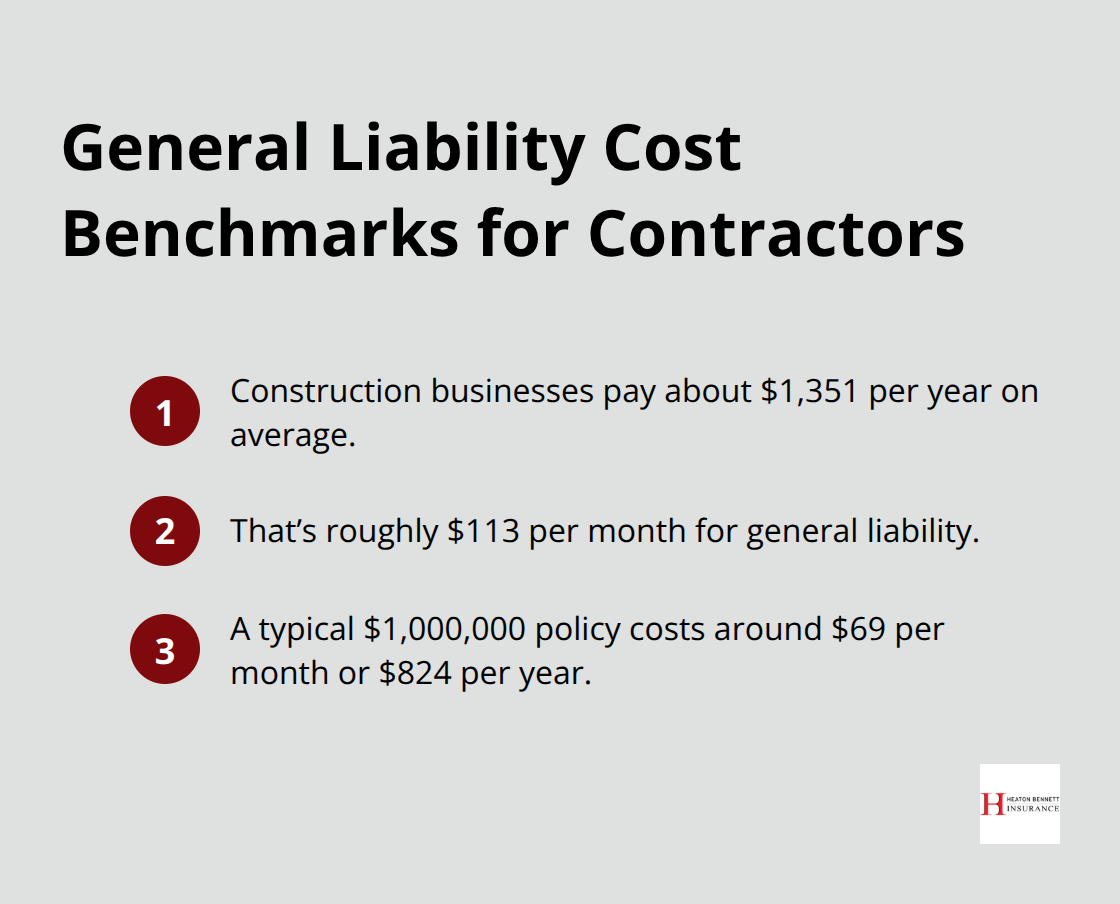

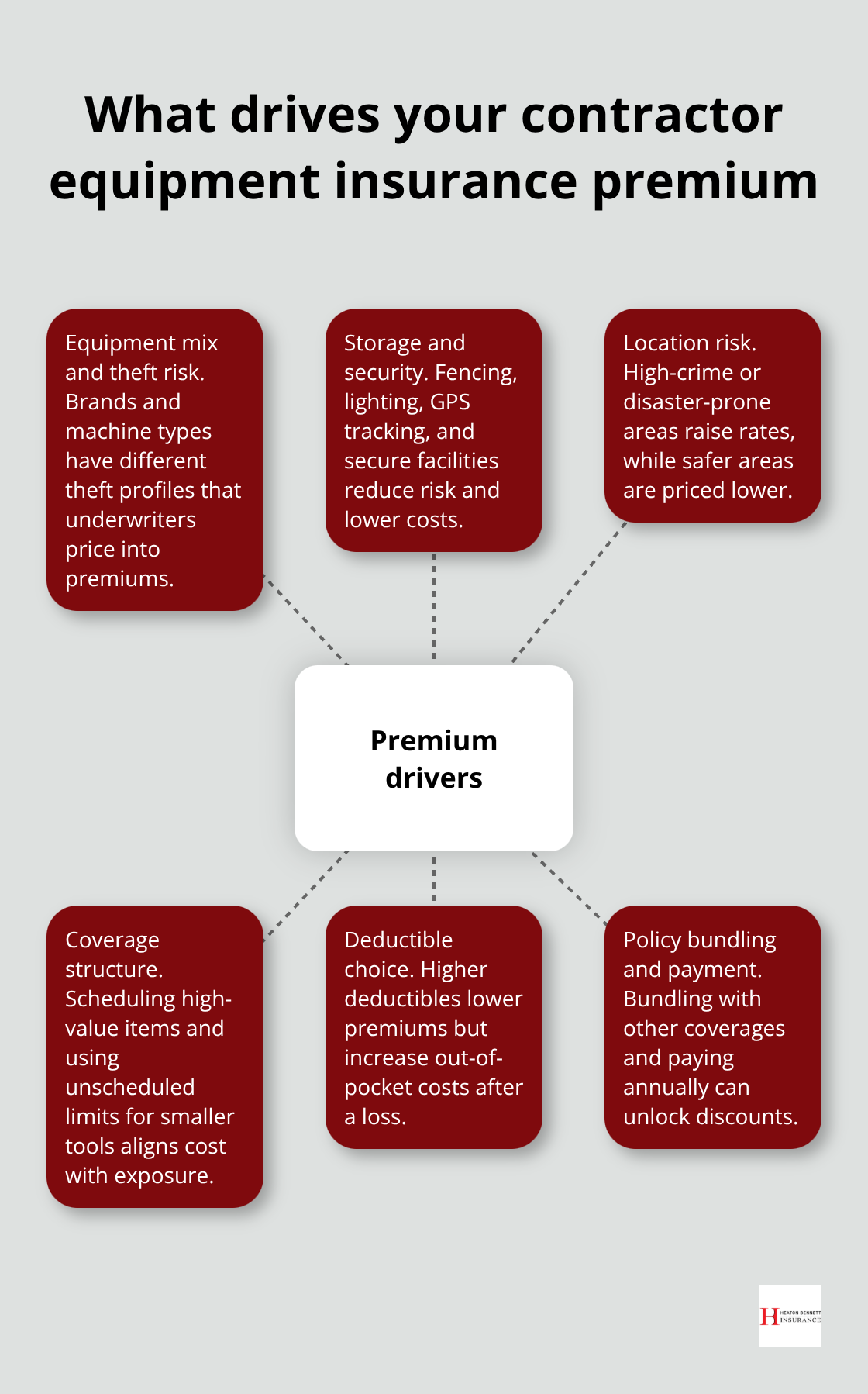

Your general liability policy covers damage you cause to someone else’s property or their injuries on your job site. Your business property coverage protects items at your shop or office. Neither of these policies covers your own equipment when it’s in transit or stored temporarily at a client’s location. A stolen cordless drill, a damaged laser level, or a broken compressor means immediate lost income because you can’t work until you replace it. According to industry data, the average premium for tools and equipment insurance for small businesses runs about $14 per month or roughly $170 annually-cheap compared to replacing even one mid-range power tool. Contractors without this coverage often absorb thousands in losses before they realize the gap in their protection.

What Actually Gets Covered and What Doesn’t

Property and equipment coverage protects hand tools, power tools, saws, laptops, work clothing, safety gear, and other portable equipment valued under $10,000. Covered events include theft from a job site or vehicle, accidental damage from drops or impacts, and vandalism. Items over $10,000 typically require separate inland marine coverage because of their higher value. What’s explicitly not covered is normal wear and tear, rust, corrosion, intentional damage, and equipment older than five years. Natural disasters like earthquakes and floods are excluded unless you add an endorsement to your policy. Coverage is triggered by sudden, unexpected loss-not gradual deterioration.

Calculating Your Coverage Needs

You need to assess your total tool inventory value and replacement costs to determine whether this policy makes sense for your business. If you carry $15,000 to $25,000 in equipment across multiple sites, the annual premium becomes a straightforward investment in avoiding catastrophic loss. The coverage limits and deductibles you select directly affect both your premium and your out-of-pocket costs when a loss occurs. Higher deductibles lower your monthly payments but increase what you pay when you file a claim. Lower deductibles cost more upfront but protect you better when theft or damage happens. Understanding this trade-off helps you pick limits that match your financial situation and risk tolerance.

Moving Forward with Protection

The right tool coverage depends on your specific equipment, how you transport it, and where you store it between jobs. Once you understand what standard business insurance won’t cover, you can see why contractors in high-risk trades need this protection. The next step is to explore the different types of tool coverage available and match them to your actual operations.

Types of Contractor Tool Coverage Available

Contractor tool coverage comes in distinct flavors, and understanding which type matches your operation is essential for avoiding gaps when loss happens. The coverage you need depends on where your tools spend most of their time and what threats pose the biggest risk to your bottom line. A painter who carries hand tools in a truck faces different exposures than a landscaper with expensive equipment stored at multiple job sites. Start by mapping where your tools actually live during a typical week, then match coverage to those specific locations and scenarios.

On-Site Tool and Equipment Coverage

On-site tool protection covers equipment while you work actively at a client’s location, whether that’s a residential home, commercial building, or renovation project. This coverage reimburses you when tools are stolen from a job site, damaged by weather or accidental impact, or vandalized during the workday. Contractors in construction, electrical, plumbing, and painting trades rely heavily on this component because tools disappear constantly from job sites, especially on larger projects where multiple crews work simultaneously.

Tools in Transit and Off-Site Protection

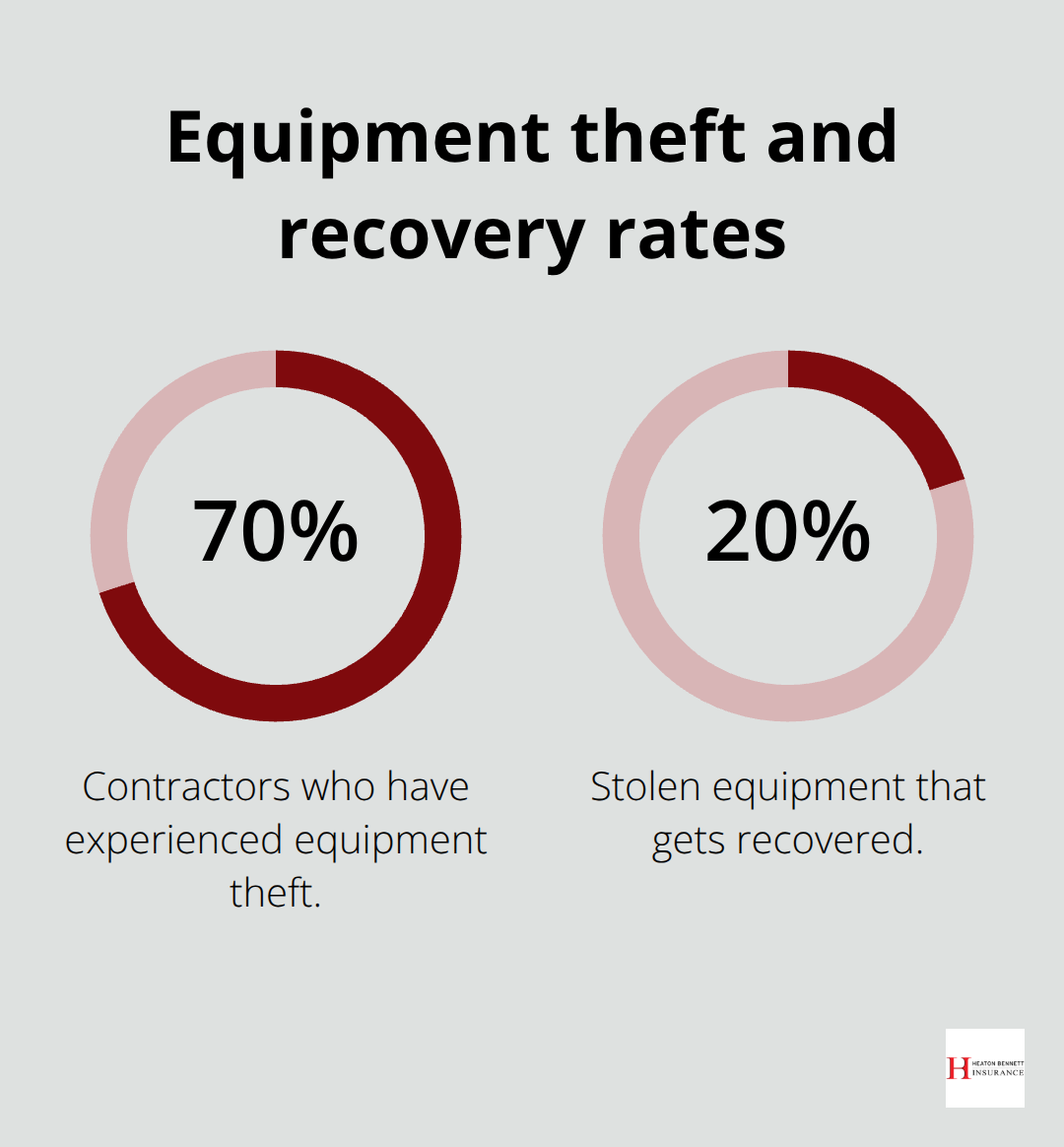

Tools in transit and off-site storage address the exposure that occurs between jobs. Your cordless drill in the truck bed, your power tools locked in a storage unit, or your equipment staged at a client’s property before work begins all fall under this protection. Theft from vehicles represents a major loss driver for contractors. According to Insureon, stolen tools (including those in transit or at client sites) represent a significant claim category. The coverage reimburses replacement or repair costs regardless of whether the loss occurred at 2 p.m. on a busy job site or at midnight in a parking lot.

Theft and Damage Coverage Options

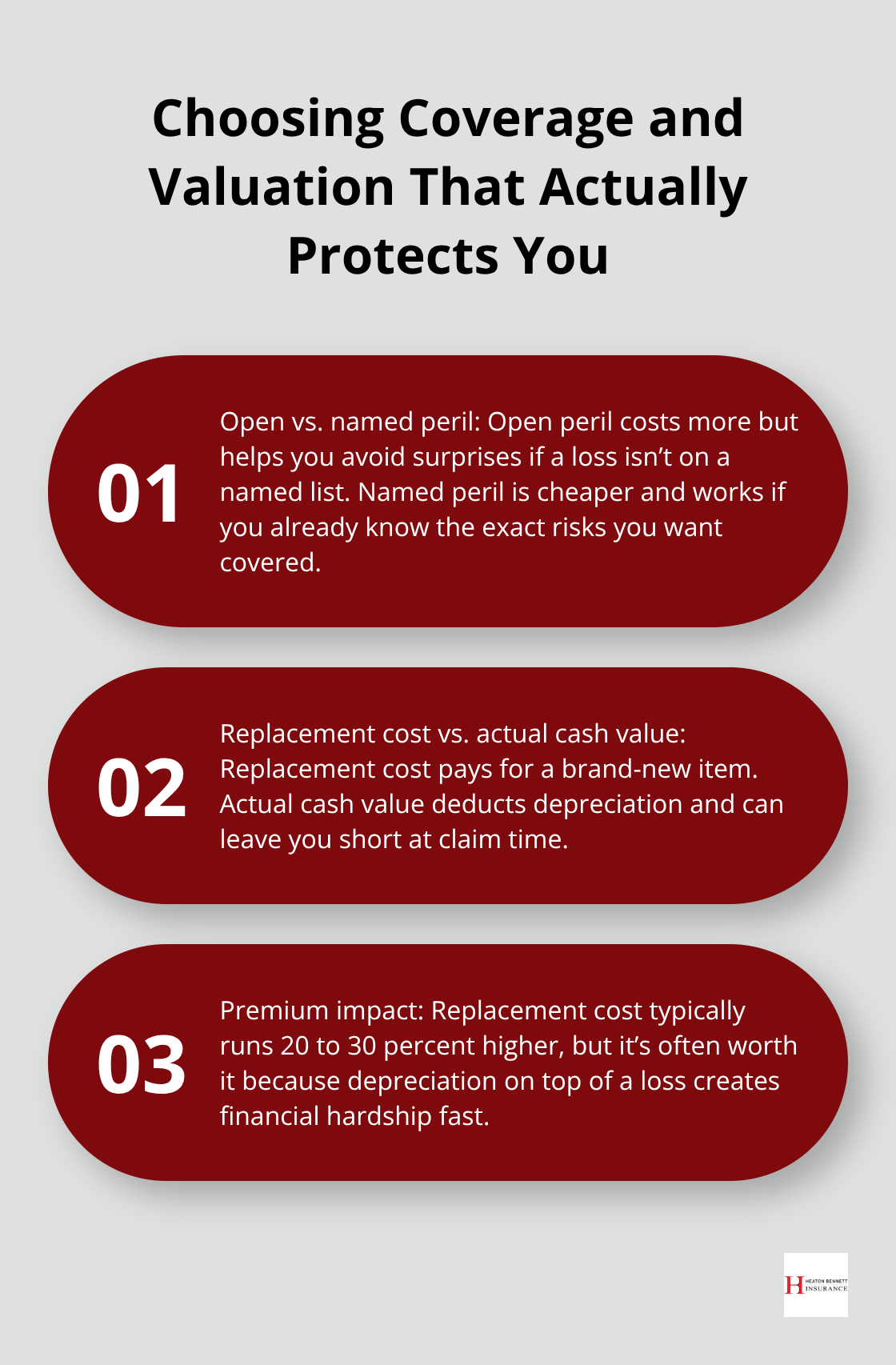

Theft and damage coverage options split into two main approaches: named peril policies that cover specific events you list, and open peril policies that protect against all sudden losses except those explicitly excluded. Open peril coverage costs more but protects you from unexpected events you might not have anticipated. Named peril coverage is cheaper and works well if you’ve already experienced losses and know exactly what to protect against. A contractor in a high-crime area might choose open peril protection as insurance against unpredictable theft, while someone in a lower-risk location might save money with named peril coverage focused on impact damage and vandalism.

Selecting Coverage Limits and Valuation Methods

Your coverage limits should reflect what you’d actually need to replace. Items under $10,000 fit comfortably in standard tools and equipment policies, but anything above that threshold usually requires separate inland marine coverage because of valuation and administration complexity. Replacement cost coverage pays to replace a stolen or damaged item with a new one, while actual cash value coverage deducts depreciation. A three-year-old impact driver worth $400 new might only be worth $240 under actual cash value, so the difference between these two approaches directly impacts your reimbursement. Replacement cost costs more upfront but leaves you whole when loss occurs. Most contractors choose replacement cost protection because the premium difference is modest compared to the financial hit of absorbing depreciation on top of a loss.

Once you understand these coverage types, the next critical step involves assessing your specific tools and equipment inventory to determine which combination of protections actually fits your business operations and budget constraints.

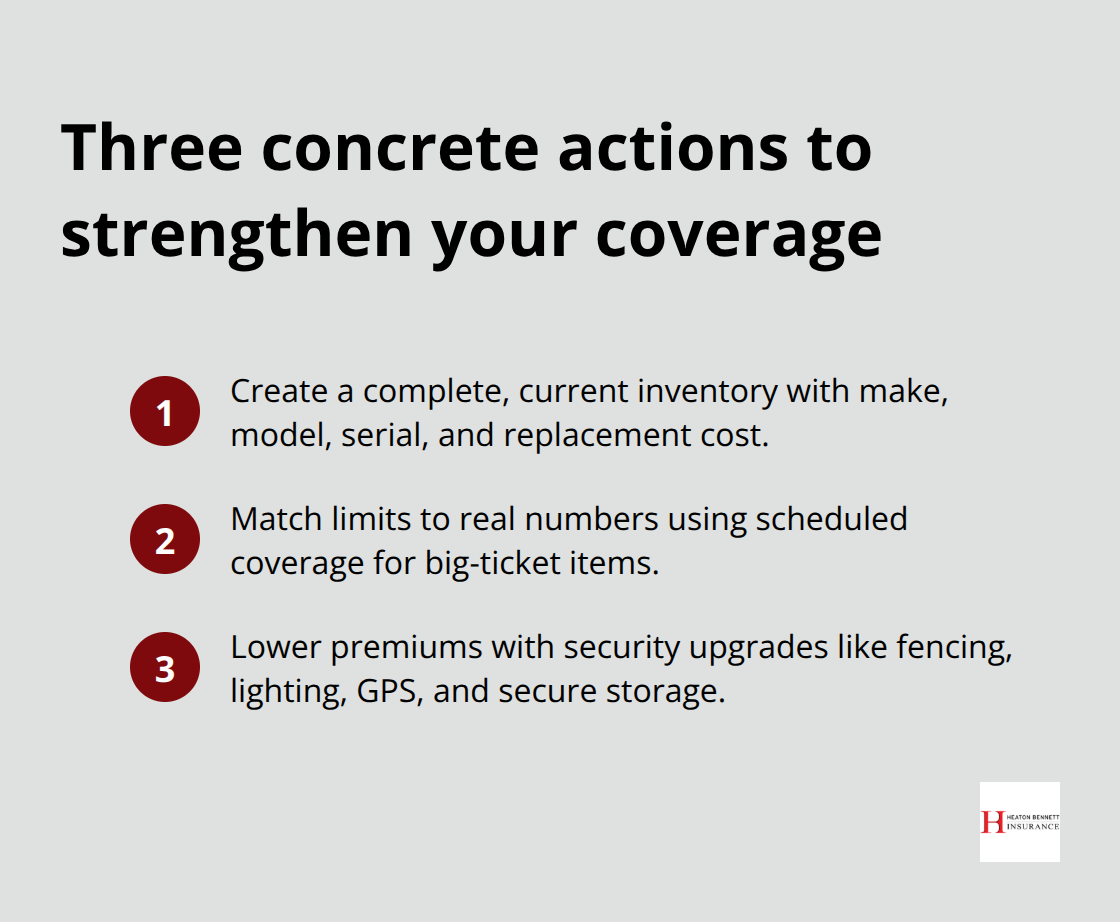

Matching Your Tools to the Right Coverage

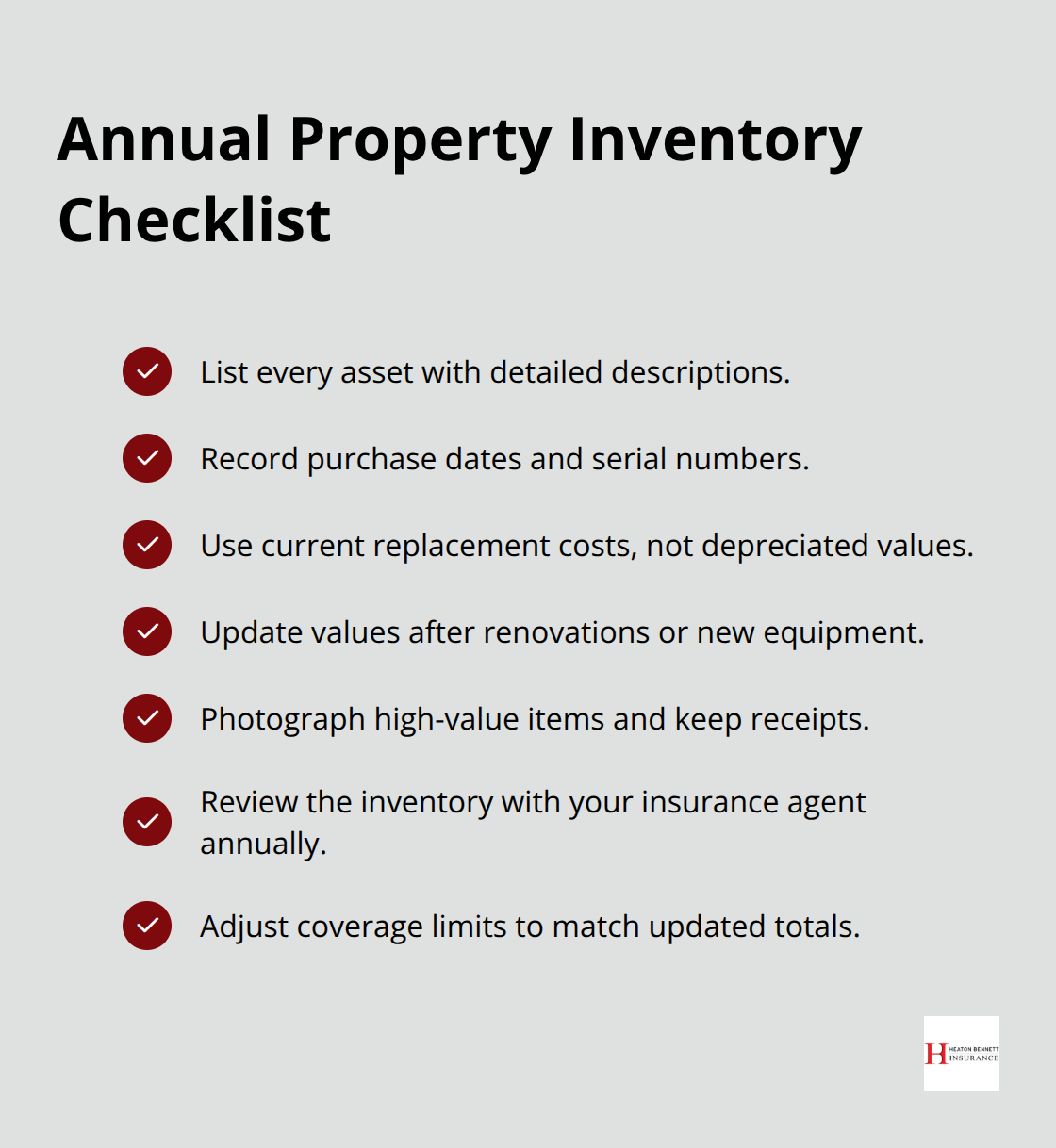

Create a Real Inventory of Your Equipment

Start with an actual list of what you carry to job sites and what you store off-site. Write down each tool’s make, model, age, and replacement cost-not what you paid three years ago, but what it costs to buy new today. A cordless drill that cost $150 in 2022 might run $180 now. A used laser level you picked up for $200 might need $350 to replace. This exercise takes two hours maximum and becomes your foundation for every coverage decision that follows. Many contractors skip this step and end up either underinsured or paying for limits they don’t need.

Categorize Tools by Location and Value

Separate tools into categories: items you carry daily in your truck, equipment stored at your shop, and expensive gear you own but use infrequently. Items under $10,000 fit standard tools and equipment policies, which average about $14 per month or $170 annually according to Insureon. Anything above $10,000 typically requires inland marine coverage with different underwriting and higher premiums. Once you know your total equipment value and where each item lives during the week, you can calculate whether the annual premium makes financial sense. If you carry $20,000 in tools across five job sites weekly, a $170 annual premium is negligible against even one stolen compressor or damaged power saw.

Choose a Deductible You Can Actually Afford

Deductibles matter far more than most contractors realize because they directly affect both your monthly payment and your real-world financial exposure. A $250 deductible policy costs roughly 15 to 20 percent more than a $1,000 deductible policy, but that difference disappears the first time you file a claim on a $400 stolen tool. Choose a deductible you can actually afford to pay out of pocket without disrupting operations, because a deductible you can’t pay is worthless protection. A contractor with tight cash flow might choose a $500 deductible and accept slightly higher premiums, while an established operation with reserves might comfortably absorb $1,000 and save on monthly costs.

Set Coverage Limits with a Buffer

Coverage limits should reflect your replacement costs plus a 20 percent buffer for unexpected equipment upgrades or newly acquired tools. If your current inventory totals $18,000, set limits at $22,000 rather than exactly $18,000. The small premium increase costs nothing compared to discovering mid-claim that you’ve outgrown your coverage.

Select Between Named Peril and Open Peril Coverage

Named peril coverage covers specific events like theft, vandalism, and impact damage, while open peril coverage protects against all sudden losses except those explicitly excluded. Open peril costs more but eliminates the risk of discovering your particular loss wasn’t on the named list.

Replacement cost coverage reimburses you for a brand-new replacement, while actual cash value deducts depreciation and leaves you short. Replacement cost typically runs 20 to 30 percent higher in premium but is worth the cost because depreciation on top of a loss creates financial hardship fast.

Final Thoughts

Contractor tool coverage protects your equipment from theft, damage, and loss-the three threats that hit your bottom line hardest. Standard business insurance won’t cover tools in transit or at client sites, coverage limits should match your actual replacement costs, and the annual premium of roughly $170 for small businesses costs far less than replacing even one mid-range power tool. The real work happens when you sit down with your actual equipment inventory, assign replacement costs to each item, and decide whether named peril or open peril protection fits your risk profile and budget.

Gather your tool list with make, model, and replacement costs, then calculate your total equipment value across all locations where tools spend time during a typical week. Decide on a deductible you can actually afford to pay out of pocket without disrupting operations, and choose between replacement cost and actual cash value coverage, knowing that replacement cost leaves you whole but costs more upfront. Contact an independent insurance agent who can compare quotes from multiple carriers and customize a policy that matches your specific operations.

We at Heaton Bennett Insurance understand that contractor tool coverage isn’t a one-size-fits-all decision. Our team works with multiple carriers to find coverage that protects your equipment without forcing you into unnecessary limits or exclusions, and we tailor solutions that fit your actual business whether you’re a solo painter or a construction company managing equipment across multiple job sites. Visit us to start a conversation about protecting your tools and your livelihood.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.