Contractor Liability Coverage: Protecting Against Mistakes and Accidents

One mistake on a job site can cost your contracting business thousands in legal fees and settlements. Contractor liability coverage protects you when accidents happen, injuries occur, or property gets damaged during your work.

At Heaton Bennett Insurance, we know that most contractors underestimate their exposure to claims. This guide walks you through what this coverage actually protects, why it matters, and what claims contractors face most often.

What Contractor Liability Coverage Actually Protects

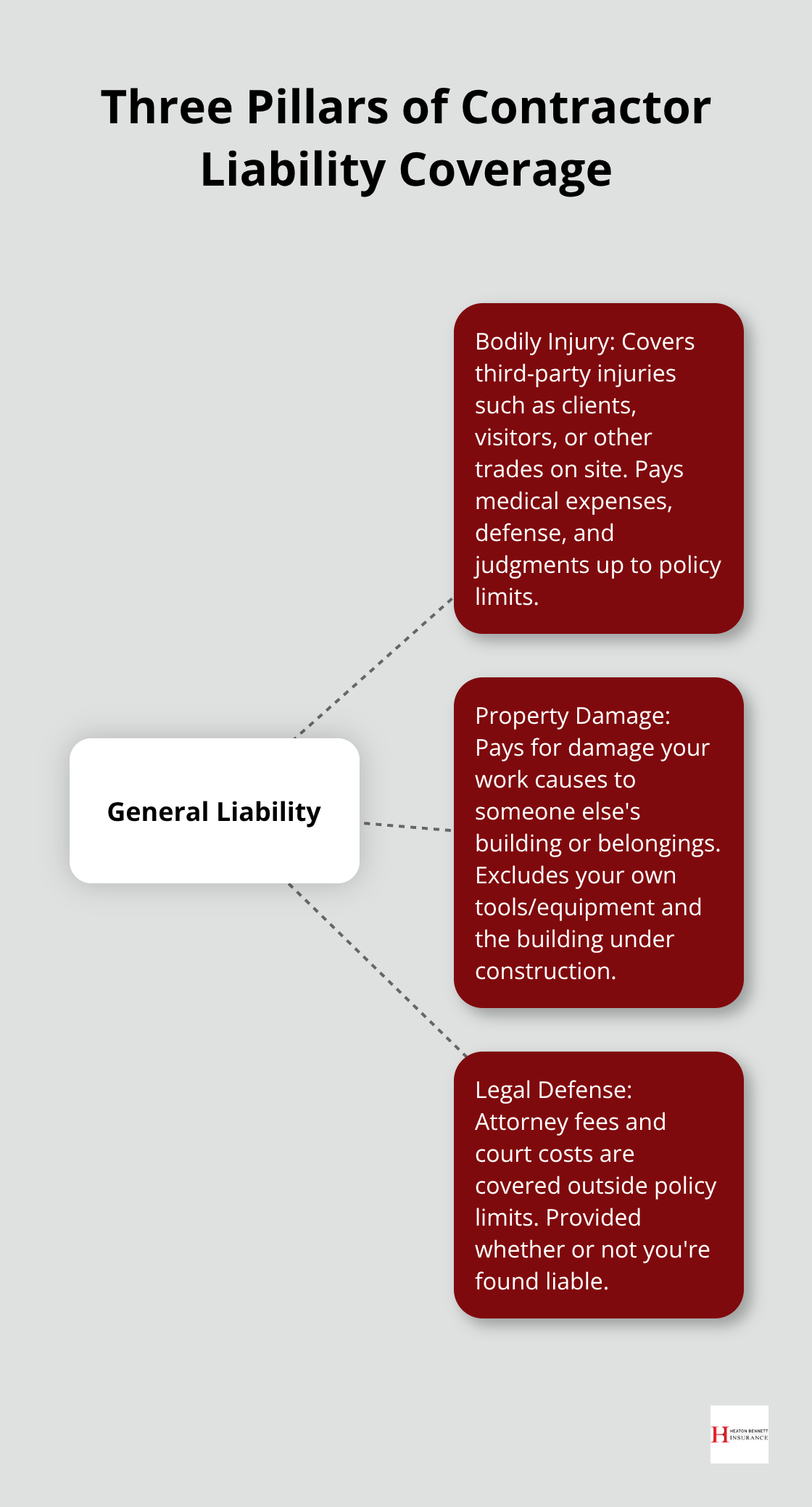

Contractor liability coverage addresses three distinct threats to your business: bodily injury claims, property damage liability, and legal expenses. The Insurance Information Institute notes that general liability policies typically include Coverage A for bodily injury and property damage, Coverage B for personal and advertising injury, and Coverage C for medical payments. Each covers different scenarios you’ll encounter on job sites. A client who trips over your equipment and breaks their leg falls under bodily injury protection. Damage to a homeowner’s flooring or walls during your work is property damage liability. The legal fees to defend yourself against either claim-whether you’re found liable or not-come from your policy’s legal defense component, which operates separately from your coverage limits.

These three elements work differently, and understanding the distinctions prevents nasty surprises when you file a claim.

Bodily Injury Claims Represent Your Biggest Exposure

Third-party bodily injury claims represent the highest-frequency liability exposure for contractors. This covers injuries to clients, their family members, employees of other trades on site, or passersby-essentially anyone except your own employees, whose injuries fall under workers’ compensation. A homeowner’s guest who slips on wet concrete you poured, a plumber’s helper who gets struck by falling materials from your scaffolding, or a neighbor injured by debris from your demolition work all trigger bodily injury coverage. The typical general liability limit in construction is $1 million per occurrence with a $2 million aggregate, according to the Insurance Information Institute. That sounds substantial until you face a catastrophic injury case where medical costs, lost wages, and pain-and-suffering awards exceed those limits-which is why many contractors carrying standard limits pursue umbrella policies for additional protection. Your policy covers medical expenses, legal defense, and judgments if you’re found liable, but the coverage only applies to legitimate third parties, not employees or your own injuries.

Property Damage Liability Covers Someone Else’s Assets

Property damage liability covers harm to someone else’s building, belongings, or land caused by your work. This includes permanent damage like stains on carpeting, broken windows, drywall holes, and structural damage, plus temporary issues like dust contamination or water intrusion. Here’s the critical distinction most contractors miss: this coverage does not protect your own tools, equipment, or materials. If your drill gets stolen from a job site or your truck bed gets damaged, that’s not covered under general liability-you need separate tools and equipment coverage or inland marine policies. Similarly, damage to the building under construction is covered by builder’s risk insurance, not general liability. Your property damage liability specifically protects against claims from the property owner or third parties when your actions cause financial loss to their assets. The distinction matters during underwriting and claims handling. If you submit a claim for your own property damage, it will be denied, which is why contractors need multiple insurance types working together on any project.

Legal Defense Costs Stand Apart From Coverage Limits

Your insurer pays legal defense costs regardless of whether you’re found liable, and these expenses don’t reduce your coverage limits-they’re separate. This means if you face a $500,000 claim and your policy limit is $1 million, your insurer covers your attorney’s fees and court costs in addition to any settlement or judgment up to that $1 million. Defense costs can easily reach $50,000 to $150,000 for contested construction claims, even before trial. Prompt notification to your insurer when an incident occurs is critical for maintaining coverage and controlling defense costs. Many contractors delay reporting because they hope claims won’t materialize, but this delay can jeopardize coverage or increase costs. Your policy requires you to notify the insurer promptly, provide incident details, document damages, and maintain thorough records-these actions directly affect whether your claim gets paid and how aggressively your insurer defends you. Waiting weeks or months to report an incident weakens your position and can result in coverage denial if the delay prejudices the insurer’s ability to investigate or defend the claim.

What Happens When You File a Claim

The moment an accident occurs on your job site, you must contact your insurer immediately. Contractors who wait to report incidents often find that their coverage gets denied or their defense becomes more expensive because the insurer couldn’t investigate while evidence was fresh. Your insurer needs specific information: the date and time of the incident, the names and contact information of injured parties or property owners, a detailed description of what happened, photos of the scene, and witness statements if available. Documentation matters more than most contractors realize. The insurer uses your initial report to assign a claims adjuster, open an investigation, and begin your legal defense if needed.

Delays in reporting or incomplete information can undermine your case and leave you exposed to costs your policy should have covered. The faster you act after an incident, the better your insurer can protect you and your business.

Why Contractors Actually Need Liability Coverage

One Accident Can Destroy Your Business

Without liability coverage, a single accident on your job site drains your business bank account faster than you’d expect. Construction ranks as the most dangerous industry in terms of workplace deaths according to the National Safety Council, and the risks extend far beyond your own employees to clients, their families, and bystanders. A homeowner’s guest who trips over your materials and fractures their spine, a neighbor whose property gets damaged during your work, or a subcontractor injured by your negligence can all file claims that exceed $100,000 in medical costs and legal fees alone.

Without coverage, you become personally liable for these amounts. Creditors pursue your business assets, your personal savings, and even future earnings through wage garnishment. Most contractors who face this situation discover too late that their personal homeowner’s insurance explicitly excludes business activities. Your business assets-equipment, vehicles, receivables, and goodwill-sit completely exposed. One catastrophic claim forces you to close your doors, sell your equipment at a loss, and spend years recovering financially.

Liability Coverage Transfers Risk to Your Insurer

Liability coverage transfers this risk to an insurance company, which means your business survives an accident that would otherwise destroy it. The financial protection operates as a safety net that keeps your personal and business assets intact when claims arise. Your insurer handles the legal defense, negotiates settlements, and pays judgments up to your policy limits. This protection allows you to focus on running your business instead of worrying about catastrophic financial exposure on every job.

Client Contracts Demand Proof of Insurance

Nearly every client contract requires proof of insurance before you start work, and many specify minimum coverage limits like $1 million per occurrence. Homeowners applying for mortgages often require contractors to carry liability coverage as a condition of the loan. Lenders view contractors without coverage as high-risk vendors and either disqualify bids or demand higher prices to compensate for the exposure.

General liability insurance costs between $69 and $113 per month for standard $1 million coverage according to industry data-a small price compared to losing a single job opportunity or facing an uninsured claim. Clients increasingly verify coverage before signing contracts, and having current certificates of insurance ready demonstrates professionalism and reduces friction during the bidding process.

Coverage Unlocks Access to Larger Projects

Without coverage, you face exclusion from larger projects, commercial work, and any client with a risk management department. Your business becomes confined to cash jobs from homeowners who don’t ask questions, which means lower project values, less stable revenue, and fewer opportunities to grow. Contractors with liability coverage access a much wider market of clients and projects that generate higher revenue and more predictable work pipelines.

The difference between insured and uninsured contractors shows up immediately in the types of jobs available to you. Residential remodeling companies, commercial builders, and property management firms all require proof of coverage before hiring subcontractors or awarding contracts. This requirement isn’t arbitrary-it reflects the real financial exposure these clients face when contractors cause damage or injuries. Your liability coverage signals that you take risk seriously and that you have the financial backing to handle claims professionally. Without it, you’re essentially locked out of the most profitable segments of the contracting market.

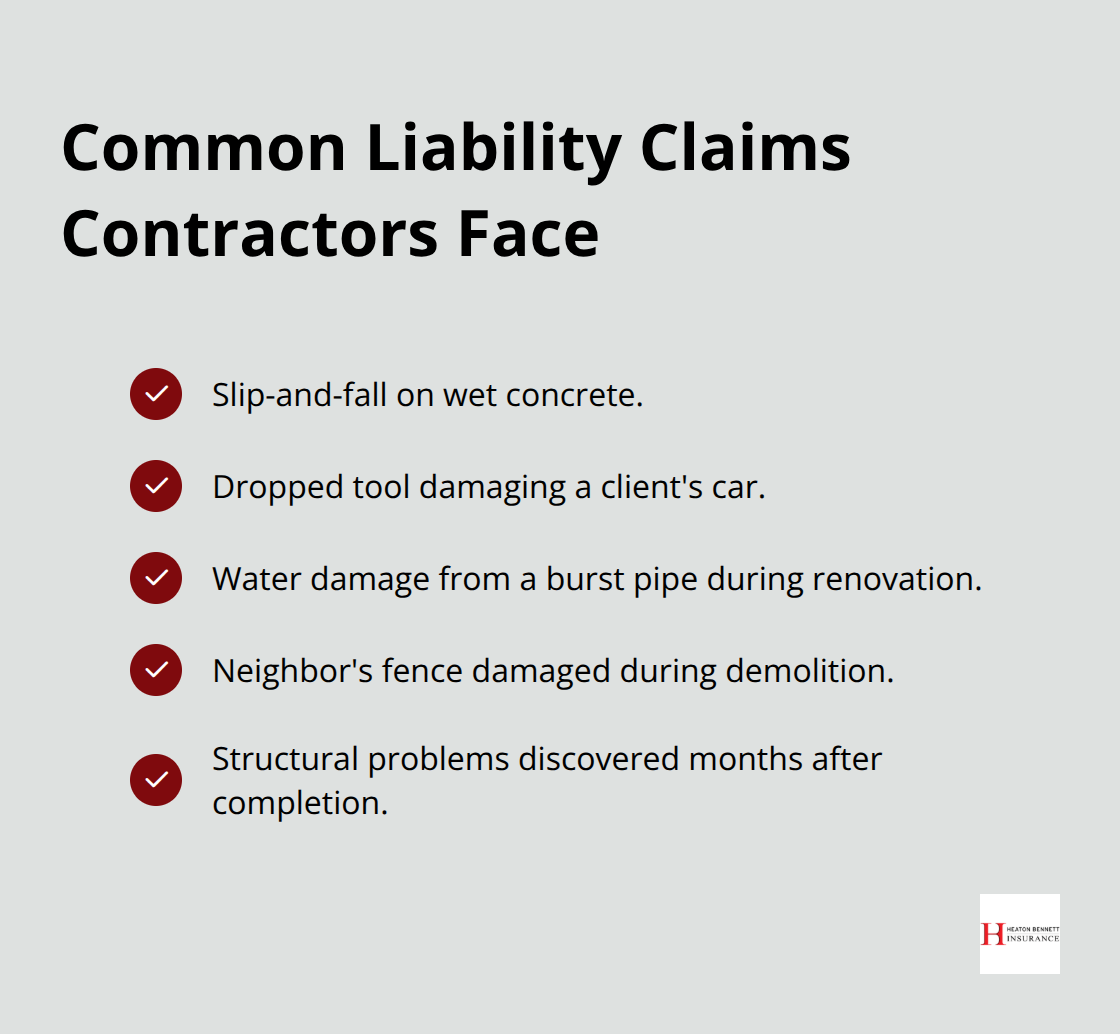

Common Claims Contractors Face

Slip-and-fall injuries on wet concrete, a dropped tool that damages a client’s car, water damage from a burst pipe during renovation work, a neighbor’s fence damaged during demolition, and structural problems discovered months after project completion happen constantly in construction. These situations represent the exact scenarios your liability coverage addresses. Most contractors focus on worst-case catastrophic injuries, but frequent, smaller claims drain contractor resources just as much.

Third-Party Injuries Cost More Than You Expect

A homeowner’s guest who trips over your equipment and requires emergency room treatment costs $8,000 to $15,000 in medical expenses alone. Your liability policy covers these costs immediately, preventing the homeowner from suing you personally for reimbursement. Job site accidents occur because construction work involves inherent risks-workers moving materials, equipment operating near pedestrians, temporary hazards like exposed nails or uneven surfaces, and clients or their family members moving through active work zones.

The National Safety Council ranks construction as the most dangerous industry, and while that statistic focuses on worker deaths, it reflects the overall hazard level contractors operate within daily. Your liability coverage protects you when third parties get hurt during your work, regardless of whether you bear direct responsibility. A client’s family member could trip over perfectly safe conditions you created, slip on water that accumulated unexpectedly, or get struck by something you didn’t see coming. Without coverage, you face the full cost of their medical treatment, lost wages, pain-and-suffering awards, and your legal defense.

Property Damage Claims Add Up Quickly

During a kitchen renovation, you accidentally damage the homeowner’s original hardwood flooring while removing cabinets-the cost to repair or replace exceeds $3,000 to $8,000 depending on the wood type and floor size. During plumbing work, a fitting fails and causes water damage to walls and personal property, creating repair costs of $5,000 to $20,000. During electrical work, you accidentally sever a wire inside the wall, causing a fire that spreads before the homeowner notices, resulting in tens of thousands in property damage.

Your liability policy covers all these scenarios because they stem from your work and damage someone else’s property. The critical detail most contractors miss is that completed operations coverage protects you after the project finishes. A homeowner discovers roof leaks six months after your roofing work concludes, or a tile installation fails and cracks appear weeks after you complete the job.

Post-Completion Failures Create Hidden Exposure

These post-completion failures trigger completed operations liability claims, which are covered separately under your general liability policy but only if your policy explicitly includes this protection. Many contractors assume their coverage ends when they leave the job site, but problems discovered later can still generate expensive claims. Prompt notification to your insurer when you learn about post-completion issues is essential because the longer you wait, the harder it becomes to investigate the root cause and defend your position.

Final Thoughts

Contractor liability coverage protects your business when accidents happen on job sites, and without it, a single incident can force you to close your doors permanently. Your business assets, personal savings, and future earnings sit exposed to claims that easily exceed $100,000 or more. Liability coverage transfers that financial risk to an insurance company, allowing you to focus on running your business instead of worrying about catastrophic exposure.

Most contractors discover too late that they lack proof of insurance and face exclusion from the most profitable work available. Homeowners applying for mortgages, commercial property managers, and lenders all require coverage before hiring you, and the cost of contractor liability coverage-roughly $69 to $113 monthly for standard $1 million coverage-is negligible compared to losing job opportunities. Having the right protection in place gives you genuine peace of mind, knowing that your business survives whatever accidents come your way.

Contact Heaton Bennett Insurance today to discuss your contractor liability coverage needs and get a quote from an insurance professional who understands contractor risks. We work with multiple carriers to find coverage that matches your specific business needs and budget. Our team guides you through the process, helping you understand exactly what your policy covers and where gaps might exist.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.