General Liability Contractors: What You Need to Know

One accident on a job site can derail your entire business. General liability for contractors isn’t optional-it’s the foundation that protects you from lawsuits, medical bills, and property damage claims that could otherwise bankrupt you.

At Heaton Bennett Insurance, we’ve seen contractors lose everything because they skipped this coverage. This guide walks you through what’s actually covered, why you need it, and how to pick a policy that fits your operation.

What General Liability Actually Covers

General liability insurance for contractors covers three core areas: bodily injury claims when someone gets hurt on your job site, property damage claims when your work damages a client’s building or belongings, and personal injury claims like slander or copyright infringement. The policy also covers your legal defense costs, which is where the real value sits. According to Insureon, the median monthly premium for general liability is about $82, but that protection extends far beyond the premium amount. When a lawsuit lands on your desk, the insurer pays your attorney fees, court costs, and settlements up to your policy limits.

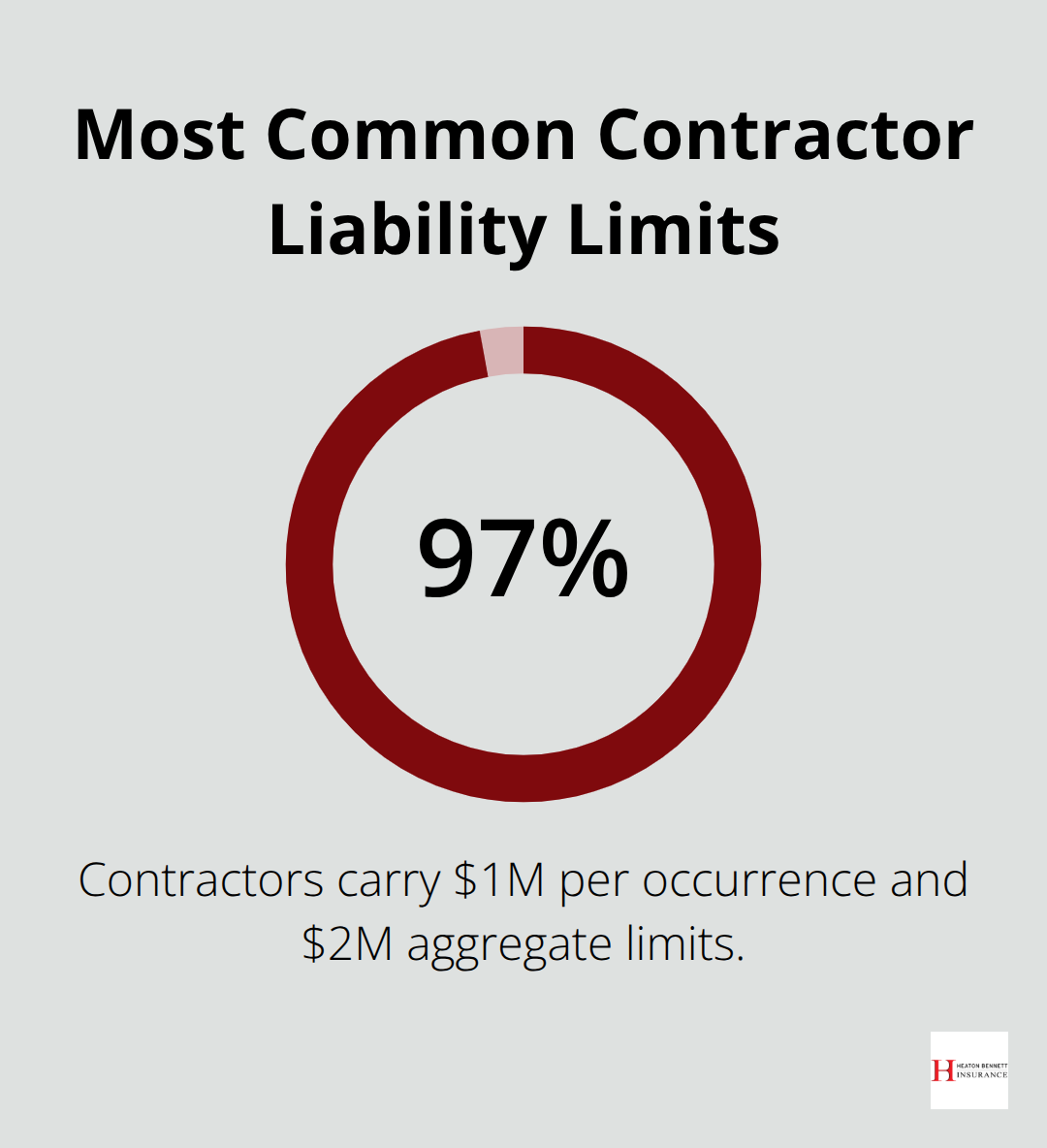

A typical contractor carries $1 million per occurrence and $2 million aggregate coverage-what about 97% of contractors purchase according to Insureon. That’s the coverage sweet spot because it handles most job site incidents without pushing premiums into territory that crushes your margins.

Bodily Injury Coverage Protects Your Wallet

If a homeowner trips on your equipment and breaks their arm, or a passerby gets hit by debris from your worksite, bodily injury coverage handles the medical bills, lost wages, and pain-and-suffering claims. Construction injury claims happen regularly, and without coverage, you’re writing personal checks for tens of thousands of dollars. Property damage coverage works the same way for physical damage-when your crew accidentally damages the client’s roof while installing siding, or a tool falls through a window, the policy covers repairs or replacement costs up to your limits.

Defense Costs Separate From Settlement Payouts

Most contractors underestimate the value of defense cost coverage. A single lawsuit costs $50,000 or more in legal fees before the case even settles, and that’s on top of any settlement amount. Your general liability policy covers these expenses separately from your per-occurrence limit, which means the insurer pays your lawyer while also covering the actual claim payout. This distinction is critical because it prevents a lawsuit from draining your business bank account just to defend yourself, even if you ultimately win the case.

Understanding what your policy actually covers sets you up to make smart decisions about limits and endorsements. The next section walks you through how to assess your specific business risks and choose coverage that matches your operation.

Why Your Business Needs General Liability Coverage

The Real Cost of Operating Without Coverage

A single incident on your job site transforms into a personal financial crisis without general liability insurance. Construction work exposes you to third-party claims constantly-someone gets injured, property gets damaged, and suddenly you face legal bills and settlement demands that exceed your annual revenue. According to Insureon, the average construction business pays around $82 per month for general liability coverage, yet a single lawsuit costs $50,000 or more in legal fees alone before any settlement gets paid. That math is straightforward: spending roughly $1,000 per year protects you from potential losses in the hundreds of thousands. Most contractors who skip this coverage believe it won’t happen to them, then discover too late that one accident wipes out years of profit. The Hartford reports that construction businesses average $1,351 per year for general liability, which remains trivial compared to what happens when you face a claim without coverage. Your business cannot afford to self-insure against catastrophic liability.

Clients and Lenders Demand Proof of Coverage

Clients and lenders won’t work with you without proof of coverage. Virtually every commercial client and most residential clients now require a Certificate of Insurance before allowing you on their property. If you can’t produce one, you lose the job-period. Banks and equipment lenders often require general liability as a condition of financing, meaning you cannot grow your business without it.

Additionally, many state licensing boards and local jurisdictions expect contractors to carry minimum coverage levels.

Why Coverage Matters for Your Business Stability

What separates successful contractors from those struggling is treating general liability as a non-negotiable business operating cost, not an optional expense. The coverage sits between your business and financial ruin. When you assess your specific business risks in the next section, you’ll discover exactly what coverage limits and endorsements protect your operation from the ground up.

Picking the Right Policy for Your Operation

Match Coverage Limits to Your Actual Work

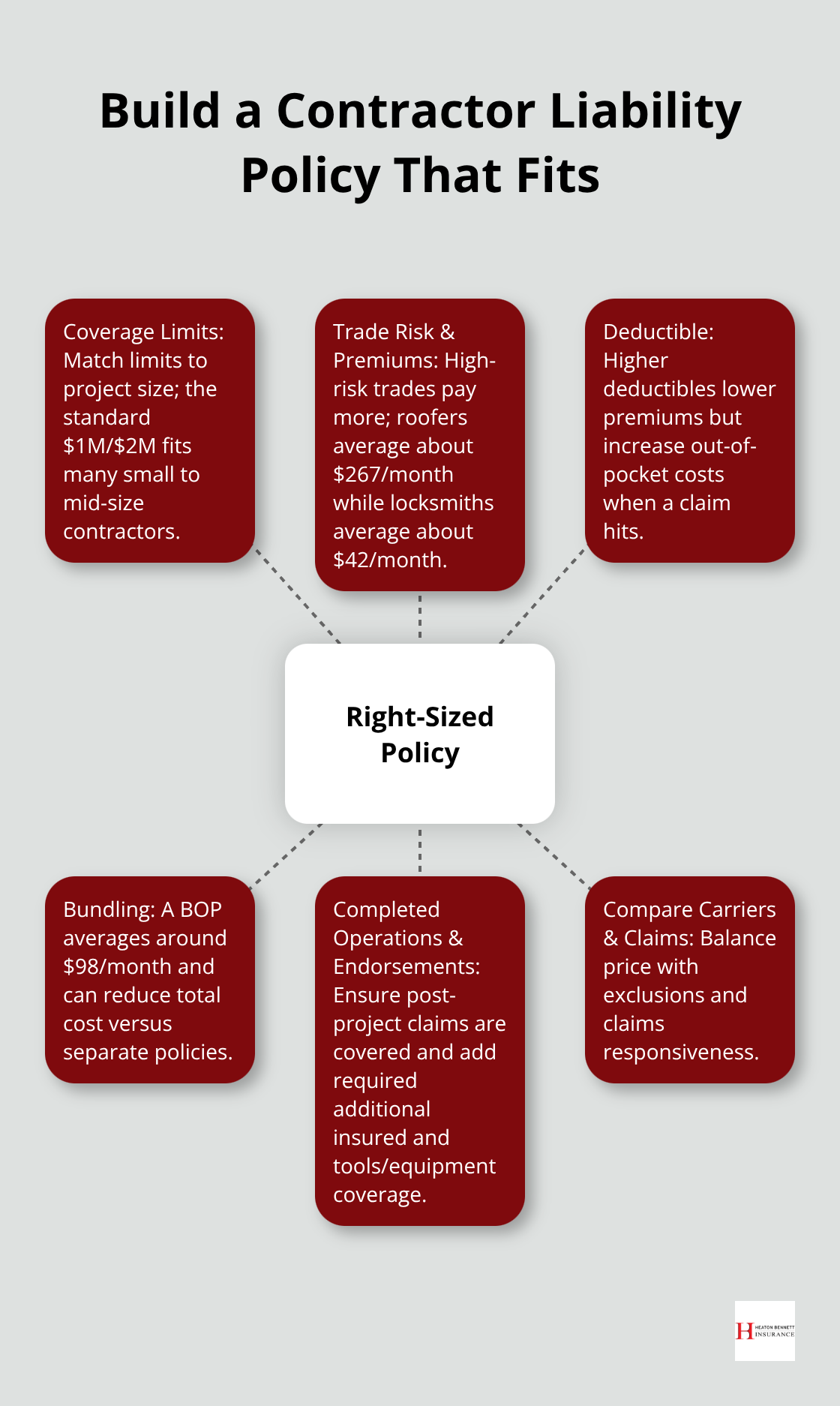

Start by mapping your actual job site exposure instead of guessing at coverage limits. A residential painter operating solo faces completely different risks than a general contractor running crews on commercial projects. According to Insureon, premiums for roofers average around $267 per month while locksmiths average about $42 per month, which reflects how dramatically risk profiles vary by trade. Your coverage limits should match the scope and dollar value of your projects. The standard $1 million per occurrence and $2 million aggregate works for most small to mid-size contractors, but if you handle larger commercial jobs or high-value renovations, those limits may leave you exposed. If you do small residential repairs, you might find better pricing with $500,000 per occurrence without sacrificing meaningful protection.

Adjust Your Deductible to Control Costs

Your deductible directly impacts your monthly premium. Choosing a $1,000 deductible instead of $500 lowers your costs, but you’ll pay that amount out of pocket when a claim hits. Talk to carriers about what specific work you do and where you operate, because location matters significantly-high-litigation states and urban areas cost more than rural regions.

Roofers, tree service operators, and general contractors often find themselves in the excess and surplus market because standard carriers view them as too risky, which means higher costs and more restrictive terms.

Bundle Policies to Save Money

Bundling your general liability with commercial auto coverage, workers’ compensation, or a Business Owner’s Policy typically saves money. Insureon reports that a BOP averages around $98 per month compared to purchasing policies separately. This approach reduces your total premium while simplifying management of multiple policies.

Evaluate Carriers on Claims Performance

When evaluating carriers, ask direct questions about claims handling speed and whether they’ve worked with contractors in your specific trade. Completed operations coverage is essential but often overlooked-this protection covers claims that arise after a project finishes, like when a roof leak shows up six months after completion. Confirm your policy includes this before signing. Ask about endorsements that fit your operation: tools and equipment coverage protects your own gear, and if clients require additional insured status, that endorsement must be available and affordable.

Compare Multiple Quotes and Coverage Details

Get quotes from multiple carriers and compare not just the monthly cost but what’s actually covered and what exclusions apply. An independent agency has access to multiple carriers and can match you with companies that understand contractor work, rather than locking you into one insurer’s approach. The cheapest quote isn’t always the best deal if the carrier denies claims or takes months to respond-your policy only matters when you need it.

Final Thoughts

Your coverage needs shift as your business grows and your project types change, so review your limits annually to stay protected without overpaying. Get quotes from multiple carriers, compare what’s actually covered beyond the monthly premium, and confirm that completed operations coverage and required endorsements are included in your policy. Ask carriers about their claims handling speed and whether they’ve worked with contractors in your specific trade, since a responsive carrier that understands construction work becomes invaluable when you file a claim.

We at Heaton Bennett Insurance work with contractors across Austin to build coverage that matches their actual operations and protects their bottom line. As an independent agency, we access multiple carriers, which means we match you with companies that understand general liability contractors coverage rather than locking you into one insurer’s approach. Our Security Snapshot process identifies gaps in your coverage and ensures you stay protected without paying for unnecessary extras.

A single incident without proper protection wipes out years of profit, while the right policy keeps your business standing. Stop treating insurance as an afterthought and start treating it as the foundation it actually is. Reach out to Heaton Bennett Insurance to discuss your specific needs and get a customized quote that protects your operation.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.