Foodservice Insurance Texas: Protecting Your Dining Operations

Running a restaurant, café, or bar in Texas means managing countless moving parts. One critical piece many operators overlook is having the right foodservice insurance Texas coverage.

At Heaton Bennett Insurance, we’ve seen firsthand how the wrong insurance gaps can derail a business. This guide walks you through the coverage types your dining operation actually needs.

Why Your Restaurant Needs More Than Basic Coverage

Restaurants operate in one of the riskiest business environments. A slip-and-fall incident in your dining room costs $15,000 to $50,000 in medical bills and legal fees. A kitchen fire destroys your equipment and inventory, wiping out months of profit. An employee injured while prepping food creates immediate wage replacement obligations and potential workers’ compensation claims. Standard business insurance does not cover these specific exposures, which is why specialized foodservice coverage tailored to your operation’s actual risks matters.

The Real Cost of Liability Incidents

General liability incidents happen constantly in restaurants. According to the National Restaurant Association, slip-and-fall claims represent one of the most frequent lawsuits against dining establishments. Beyond immediate medical costs, you face legal defense expenses, settlements, and reputation damage that affects customer traffic for months. A customer who suffers food poisoning from improper handling can pursue product liability claims exceeding $100,000 when multiple patrons are affected.

If you serve alcohol, liquor liability exposure intensifies dramatically. Texas dram-shop laws hold establishments responsible for injuries caused by intoxicated patrons, meaning a single incident involving an over-served customer generates claims for property damage, medical expenses, and even criminal liability. Commercial general liability insurance specifically designed for restaurants covers these third-party bodily injury and property damage claims, but only if your policy includes proper liquor liability endorsements when alcohol is served.

Equipment and Inventory Protection Demands Precision

Your kitchen equipment represents 40 to 60 percent of your startup costs. A walk-in cooler failure spoils $3,000 in inventory without warning. A grease fire damages your hood system, requiring $8,000 to $15,000 in repairs and forcing temporary closure. Standard property insurance covers the building structure but leaves your equipment and inventory exposed unless specifically added.

Protect your restaurant from equipment breakdowns with comprehensive coverage that keeps kitchens running smoothly and avoids costly downtime. Business interruption coverage replaces your lost income during forced closures, covering rent, payroll, and utilities while you cannot operate. Without these riders, a three-week kitchen closure costs $12,000 to $20,000 in unrecovered expenses.

Employee Coverage Protects Your Bottom Line

OSHA data shows restaurant workers suffer injuries at rates 18 percent higher than the national average. A kitchen burn requiring hospitalization, a slip on wet floors causing broken bones, or repetitive strain injuries create immediate financial and legal obligations. While Texas does not mandate workers’ compensation for all employers, carrying coverage costs $300 to $3,000 annually and shields your business from direct liability.

Employment practices liability insurance addresses wrongful termination claims, discrimination allegations, and harassment complaints-risks that have grown substantially as labor dynamics shift in Texas hospitality. A single wrongful termination lawsuit costs $25,000 to $75,000 in legal defense alone, making EPLI a practical investment for any operation with employees. Understanding which coverage types apply to your specific situation requires a detailed review of your operation’s actual exposures and Texas regulatory requirements.

Coverage Types Your Restaurant Actually Needs

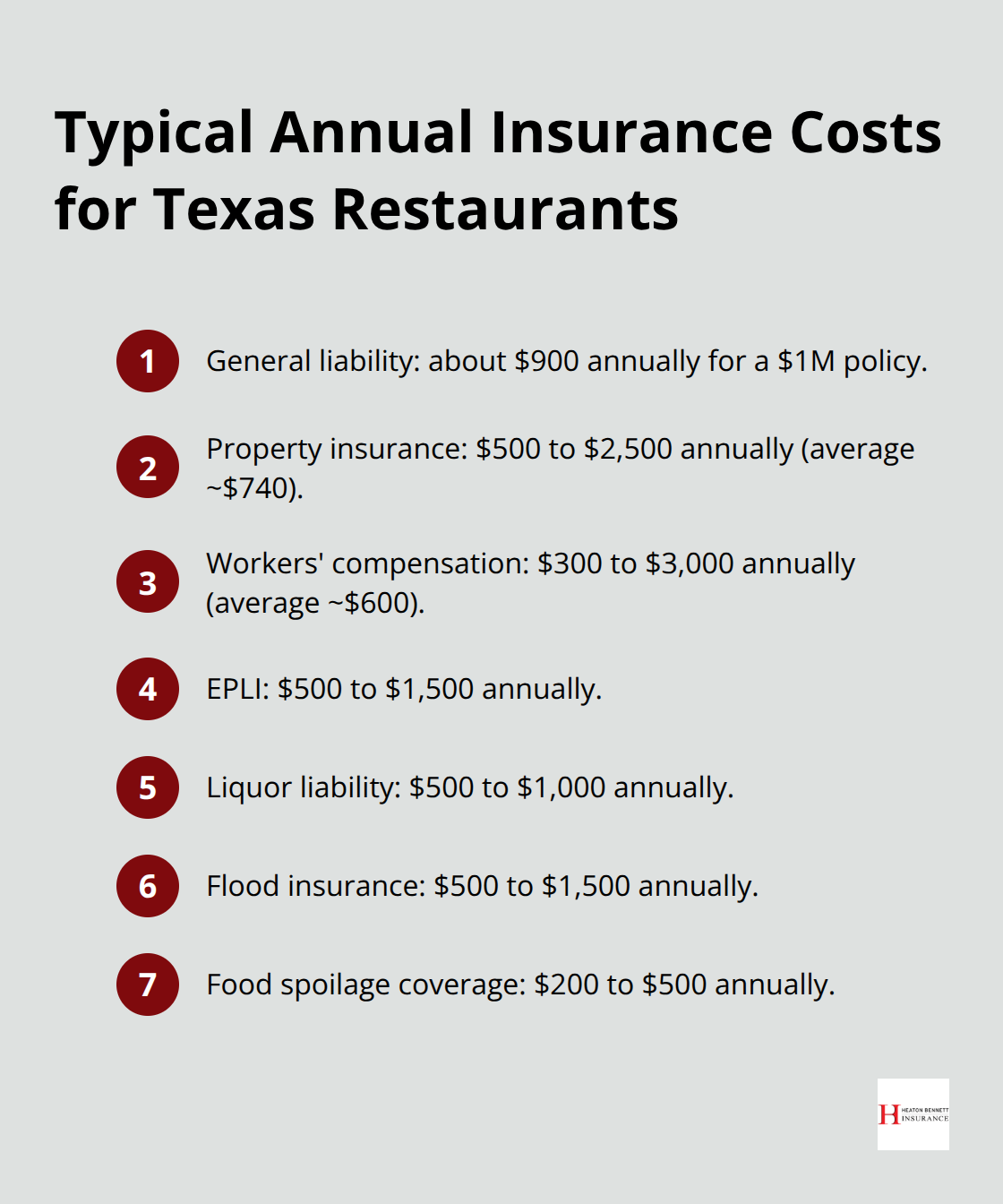

Commercial general liability insurance forms the foundation of restaurant protection, covering third-party bodily injury and property damage claims that arise from your operations. This covers slip-and-fall incidents in your dining room, customer injuries from food service, and damage to customer property. A $1 million general liability policy costs approximately $900 annually in Texas, though urban locations like Dallas and Houston pay 10 to 15 percent more than rural areas due to higher litigation risk. The policy does not cover employee injuries, damage to your own property, or claims related to alcohol service-those require separate endorsements or policies. If you operate a food truck or mobile operation, general liability still applies but requires additional vehicle coverage since your exposure changes with location.

What Your Property Coverage Actually Protects

Commercial property insurance safeguards your building, kitchen equipment, furniture, inventory, and point-of-sale systems. Most restaurant operators drastically underestimate their equipment values. A standard commercial kitchen with walk-in coolers, cooking equipment, and ventilation systems costs $40,000 to $80,000 to replace. Property coverage typically runs $500 to $2,500 annually with an average around $740 for standard protection, but this baseline excludes flood damage entirely. Coastal Texas areas like Galveston see property premiums 20 to 25 percent higher because of hurricane and flood risk, according to NOAA 2024 data. You need separate flood insurance costing $500 to $1,500 annually if you operate in a flood zone, which most Texas restaurants do not carry despite the exposure.

Food spoilage coverage protects against losses from power outages or equipment failures, costs $200 to $500 annually, and prevents catastrophic inventory losses during equipment breakdowns or weather events.

Employee Injuries and Workplace Claims Demand Serious Coverage

Workers’ compensation coverage costs $300 to $3,000 annually depending on payroll size and operation type, with an average around $600. Texas does not mandate this coverage for all employers, but OSHA data shows restaurant workers suffer injuries 18 percent above the national average, making coverage a practical necessity rather than optional. A kitchen burn requiring hospitalization or a slip injury on wet floors creates immediate wage replacement obligations and medical expenses that workers’ comp absorbs. Employment practices liability insurance protects against wrongful termination, discrimination, and harassment claims-exposures that have intensified as labor dynamics shift in Texas hospitality. A single wrongful termination lawsuit costs $25,000 to $75,000 in legal defense alone, making EPLI coverage at $500 to $1,500 annually a smart investment for any operation with employees.

Liquor Liability Stands Apart From General Liability

If you serve alcohol, liquor liability insurance is non-negotiable because standard general liability explicitly excludes alcohol-related claims. Texas dram-shop laws hold establishments responsible for injuries caused by intoxicated patrons, meaning a single incident involving an over-served customer generates claims for property damage, medical expenses, and potentially criminal liability. Liquor liability coverage costs $500 to $1,000 annually and covers legal fees, medical costs, and property damage resulting from incidents involving intoxicated patrons. Fine dining establishments and steakhouses pay significantly more than casual bars because their higher revenue and customer base create greater exposure. A Fort Worth steakhouse might pay $5,500 annually for full coverage including liquor liability, while a San Antonio taco stand without alcohol service pays around $2,000. Understanding which coverage types apply to your specific situation requires a detailed review of your operation’s actual exposures and Texas regulatory requirements.

What Texas Really Requires for Restaurant Insurance

Workers’ Compensation: Optional but Financially Essential

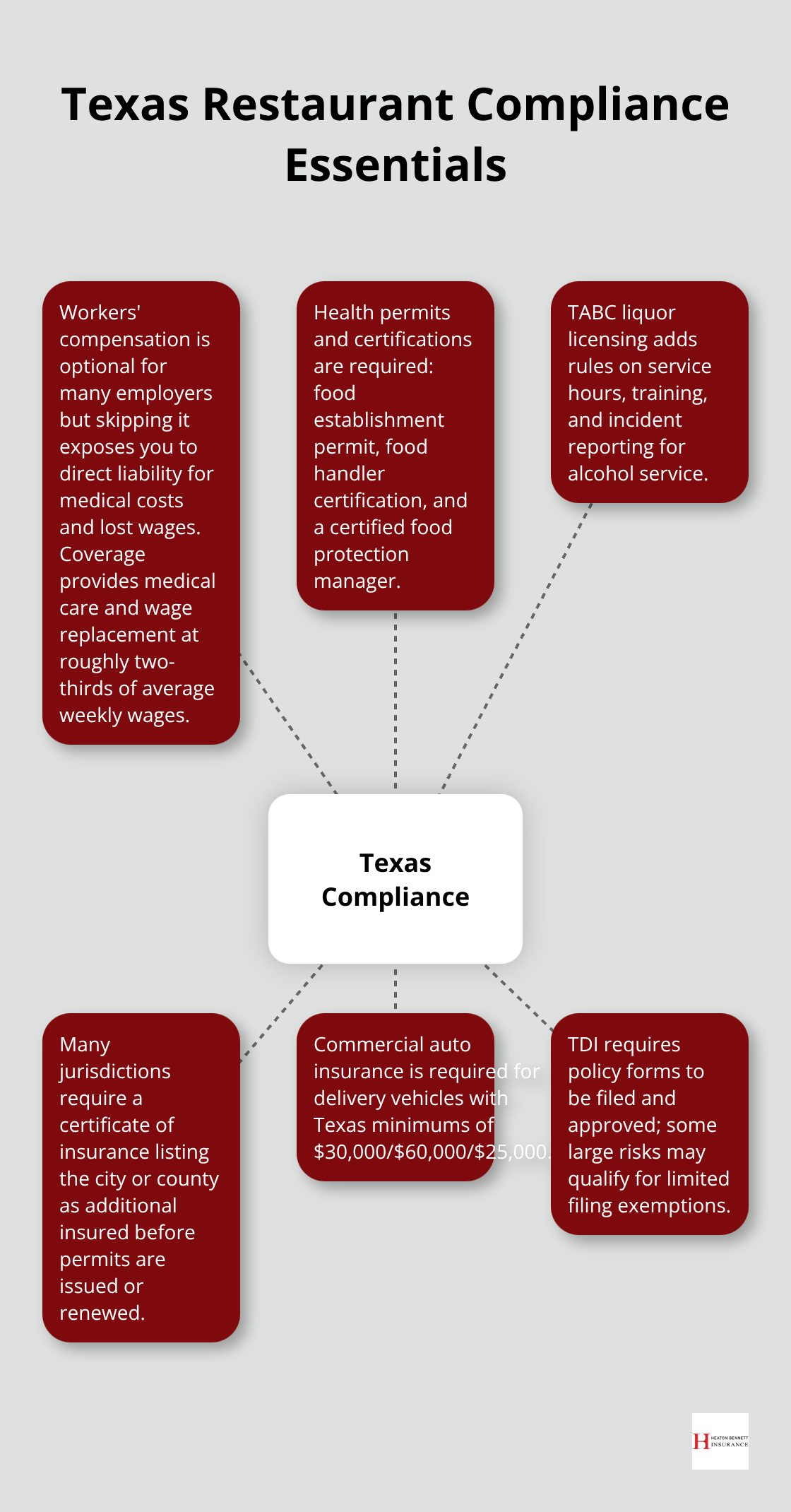

Texas treats workers’ compensation differently than most states-it’s not mandatory for all employers, but that doesn’t mean you should skip it. The state allows employers to opt out, yet carries serious consequences for doing so. If you operate without coverage and an employee gets injured, you face direct liability for all medical costs, lost wages, and potential punitive damages that can reach six figures. The Texas Workers’ Compensation Act covers medical treatment, wage replacement at two-thirds of average weekly wages, rehabilitation costs, and death benefits for employee families. Carrying coverage costs $300 to $3,000 annually depending on your payroll and operation type, making it far cheaper than absorbing a single serious injury claim yourself.

OSHA data shows restaurant workers suffer injuries 18 percent above the national average, so this isn’t theoretical risk-it’s daily operational reality in Texas kitchens. A kitchen burn requiring hospitalization or a slip on wet floors creates immediate wage replacement obligations and medical expenses that workers’ comp absorbs. Beyond workers’ comp, you need employment practices liability insurance to handle wrongful termination, discrimination, and harassment claims that have multiplied as labor disputes intensify across Texas hospitality. A single wrongful termination lawsuit costs $25,000 to $75,000 in legal defense alone, making EPLI coverage at $500 to $1,500 annually a practical necessity rather than optional protection.

Local Health Departments and Licensing Requirements

Local health departments and licensing authorities add another layer of requirements that vary by city and county. Texas restaurants need a food establishment permit from your local health department, food handler certification for staff, a food protection manager certification from someone on your team, and a sales tax permit from the Texas Comptroller. If you serve alcohol, the Texas Alcoholic Beverage Commission issues liquor licenses with strict compliance rules around service hours, training, and incident reporting.

Many jurisdictions require proof of insurance-specifically a certificate of insurance listing the city or county as additional insured-before issuing or renewing permits. You’ll also need commercial auto insurance if you operate delivery vehicles, with Texas minimum limits of $30,000 per person, $60,000 per accident, and $25,000 property damage per accident. Mobile food operations, catering services, and special events each trigger different permit requirements and insurance expectations.

Texas Department of Insurance Compliance

The Texas Department of Insurance requires all commercial general liability, liquor liability, and related policy forms to be filed and approved before use, with filings due at least 60 days before implementation. This regulatory framework exists to protect public health and safety, but it directly impacts your insurance requirements-your policy forms must comply with TDI standards or your coverage becomes invalid. Large foodservice operations with total insured property values reaching $5 million or more, annual gross revenues of $10 million or more, or premiums exceeding defined thresholds may qualify for a Large Risk exemption, meaning some forms or rates become exempt from filing.

Cost Reduction Strategies That Actually Work

Industry best practices in Texas emphasize annual policy reviews to catch coverage gaps as your operation grows. Bundling general liability, property, and business interruption into a business owner’s policy saves 10 to 15 percent on premiums compared to purchasing policies separately; a Lubbock diner reduced costs from $4,200 to $3,500 through bundling. Texas Restaurant Association membership unlocks 3 to 5 percent discounts with participating insurers, and many operators overlook this advantage despite representing real savings on annual premiums.

Safety and maintenance measures reduce future claims and premium increases-staff safety training cuts injury claims by about 25 percent per OSHA standards, and regular equipment maintenance yields 5 to 10 percent discounts from insurers who recognize lower risk. A clean claims history matters enormously; a single claim within 3 to 5 years can raise premiums by 15 to 25 percent, so investing in prevention pays dividends through stable insurance costs over time.

Final Thoughts

Your restaurant, café, or bar operates in a high-risk environment where a single incident threatens your entire business. Commercial general liability, property protection, workers’ compensation, and liquor liability when applicable form the foundation of responsible operations in Texas. Without these protections, you absorb the full financial impact of slip-and-fall claims, equipment failures, employee injuries, and alcohol-related incidents that cost tens of thousands of dollars.

Foodservice insurance Texas isn’t one-size-fits-all because your operation’s specific risks depend on your location, whether you serve alcohol, your equipment value, your payroll size, and your service model. A food truck faces different exposures than a fine dining establishment, and a catering business needs coverage that a sit-down café doesn’t. This is where working with an insurance partner who understands your actual operation matters most.

At Heaton Bennett Insurance, we specialize in tailoring coverage to your specific foodservice operation. As an independent agency, we access multiple carriers rather than pushing you toward a single provider, meaning your policy reflects your real needs and budget. Contact Heaton Bennett Insurance to discuss your foodservice insurance needs and receive a personalized quote that protects your margins and your peace of mind.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.