Contractor Insurance Austin TX: Local Regulations and Options

Running a contracting business in Austin means navigating specific insurance requirements that protect both your operations and your clients. Contractor insurance in Austin TX isn’t one-size-fits-all-different contractor types face different mandates.

We at Heaton Bennett Insurance help contractors understand what coverage they actually need versus what’s optional. This guide walks you through Texas state requirements, Austin-specific regulations, and how to pick the right coverage for your business.

What Insurance Must You Have as an Austin Contractor

Registration and General Liability Basics

Texas does not require a statewide general contractor license, which surprises many contractors moving to the state. Instead, Austin governs its own licensing through the Austin Build + Connect portal, and you must register your contracting business there before starting work-the registration itself is free. However, free registration does not mean you are covered legally. General Liability Insurance is the non-negotiable foundation. Most Austin projects demand a current Certificate of Insurance before you step foot on site, and clients will not negotiate on this. A standard General Liability policy covers bodily injury, property damage, and legal fees if something goes wrong during your work.

Understanding Your Premium Costs

In 2024, the median monthly cost for new Progressive customers was $60, though rates ranged up to $85 depending on your specific risk profile. Your actual premium depends on the type of work you do-roofers and excavation contractors pay significantly more than interior finish carpenters because the physical risk is higher. Location matters too. Austin’s density and construction activity mean rates tend to sit on the higher end compared to rural Texas areas. The work you perform, your safety track record, and the number of employees all influence what you ultimately pay each month.

State-Licensed Trades and Workers Compensation

For trades requiring state licensure, Texas demands additional insurance proof before you can legally operate. Electricians, plumbers, and HVAC technicians must register with the Texas Department of Licensing and Regulation, and many government or commercial projects will not hire you without Workers Compensation Insurance in place. Texas is an opt-out state for workers comp, meaning you are not legally required to carry it unless you have employees or a contract mandates it-but that is a dangerous gamble. If an employee gets injured and you do not have coverage, you face a direct lawsuit with no insurance protection. Projects on public land or with major general contractors almost always require it.

Additional Coverage You Cannot Ignore

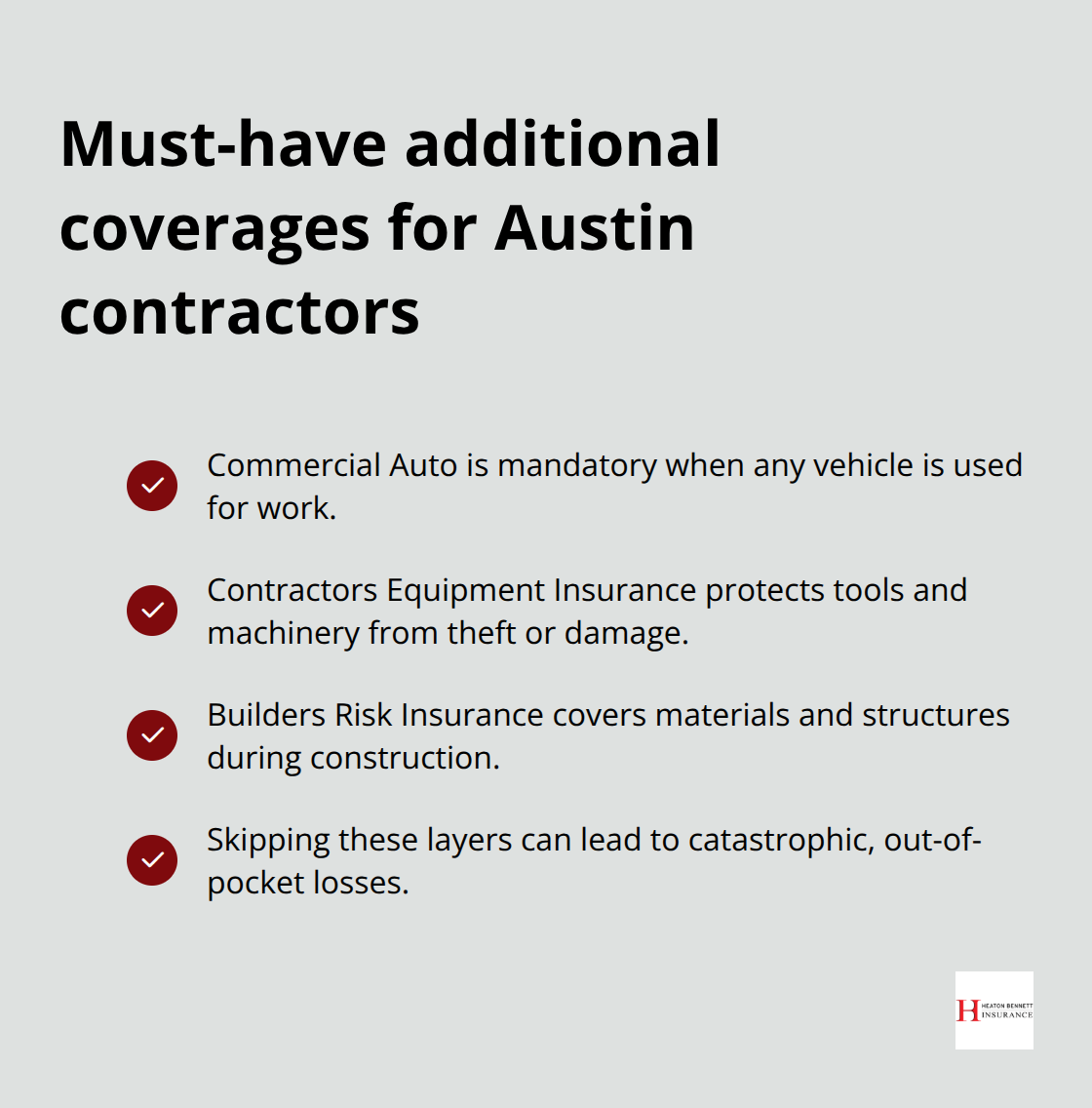

Beyond these basics, your specific situation determines what else you need. If you operate a company vehicle for work, commercial auto insurance is mandatory because personal auto policies explicitly exclude business use.

If you own tools worth more than a few thousand dollars, Contractors Equipment Insurance protects against theft or damage on job sites and in transit. Builders Risk Insurance becomes essential when you are responsible for materials and structures during construction. Many Austin contractors underestimate their exposure by skipping these layers, then face catastrophic losses they could have prevented for a few hundred dollars a year.

The right combination of coverage transforms your insurance from a compliance checkbox into genuine protection. Understanding which policies apply to your specific trade and project type sets the stage for selecting the right provider who can tailor coverage to your actual operations.

What Coverage Actually Protects Your Austin Contracting Business

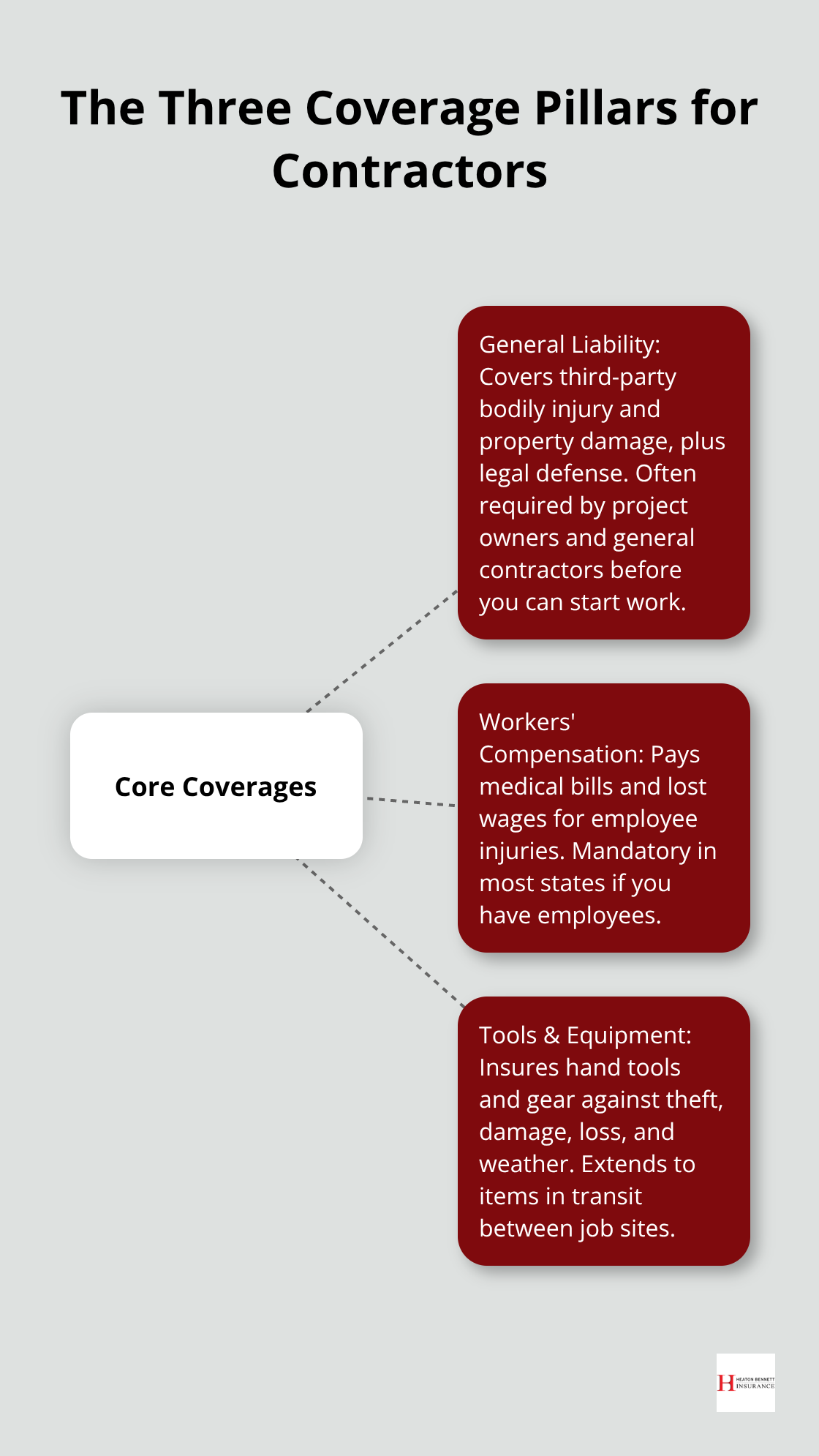

General Liability: Your First Line of Defense

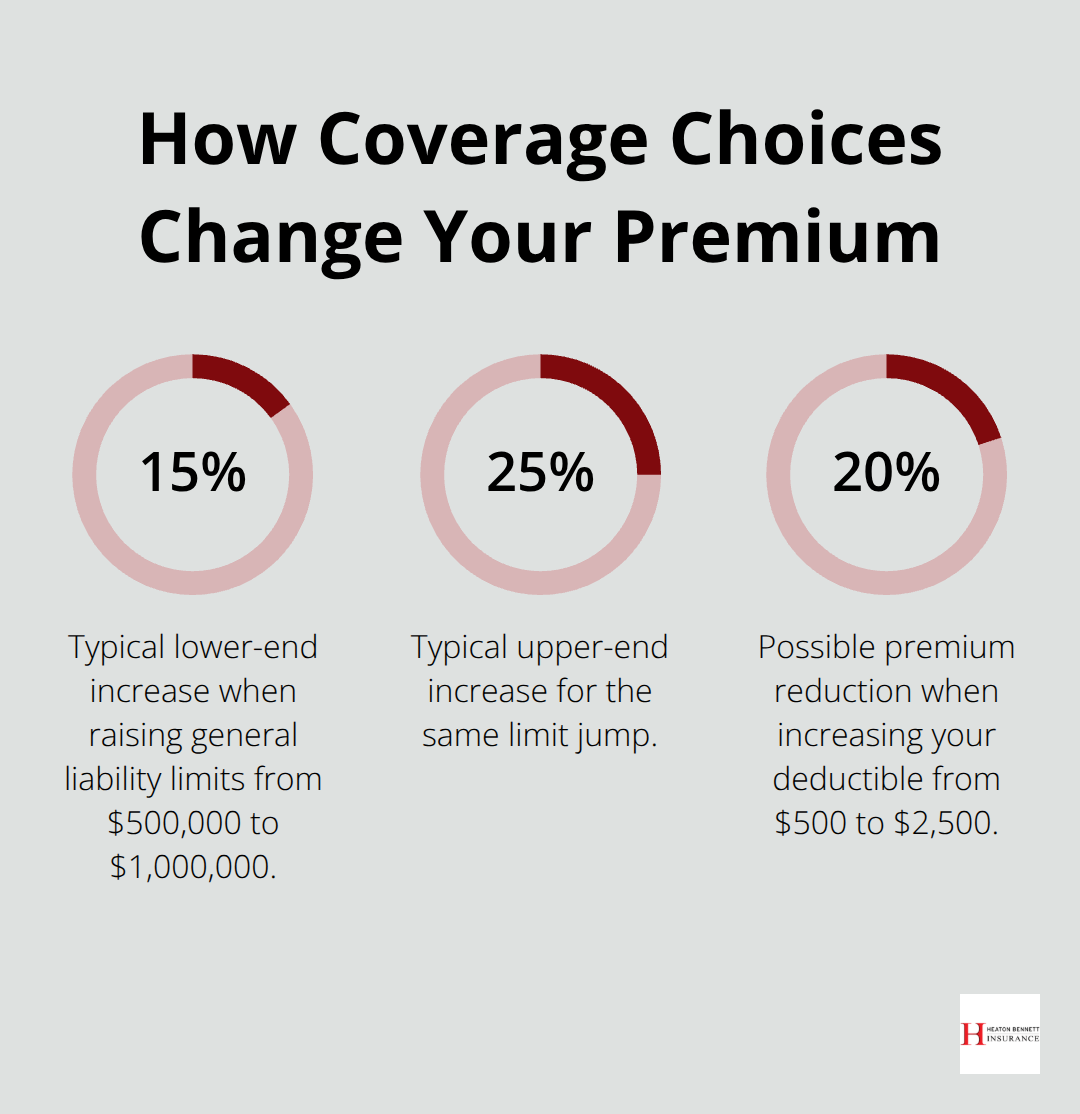

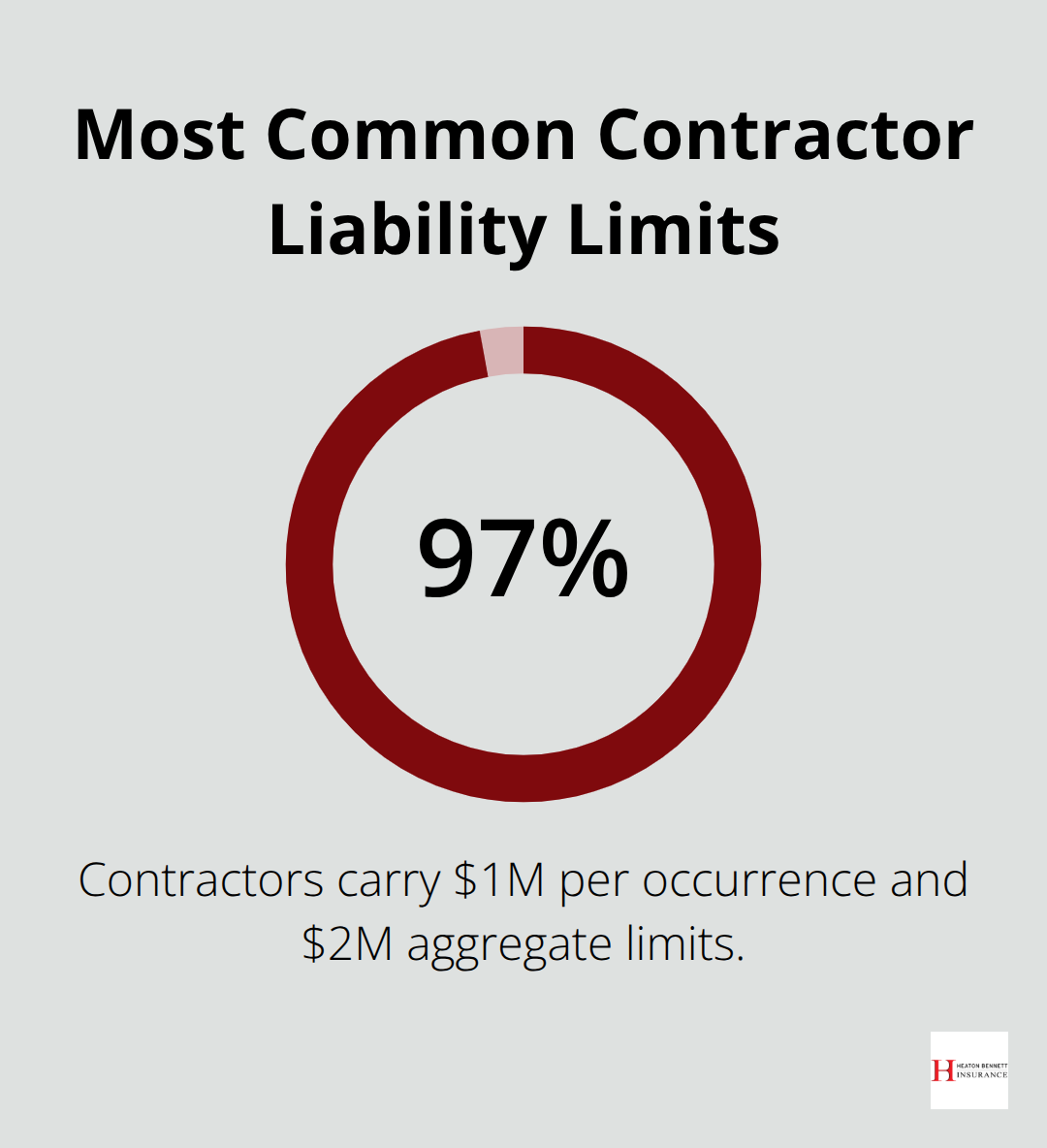

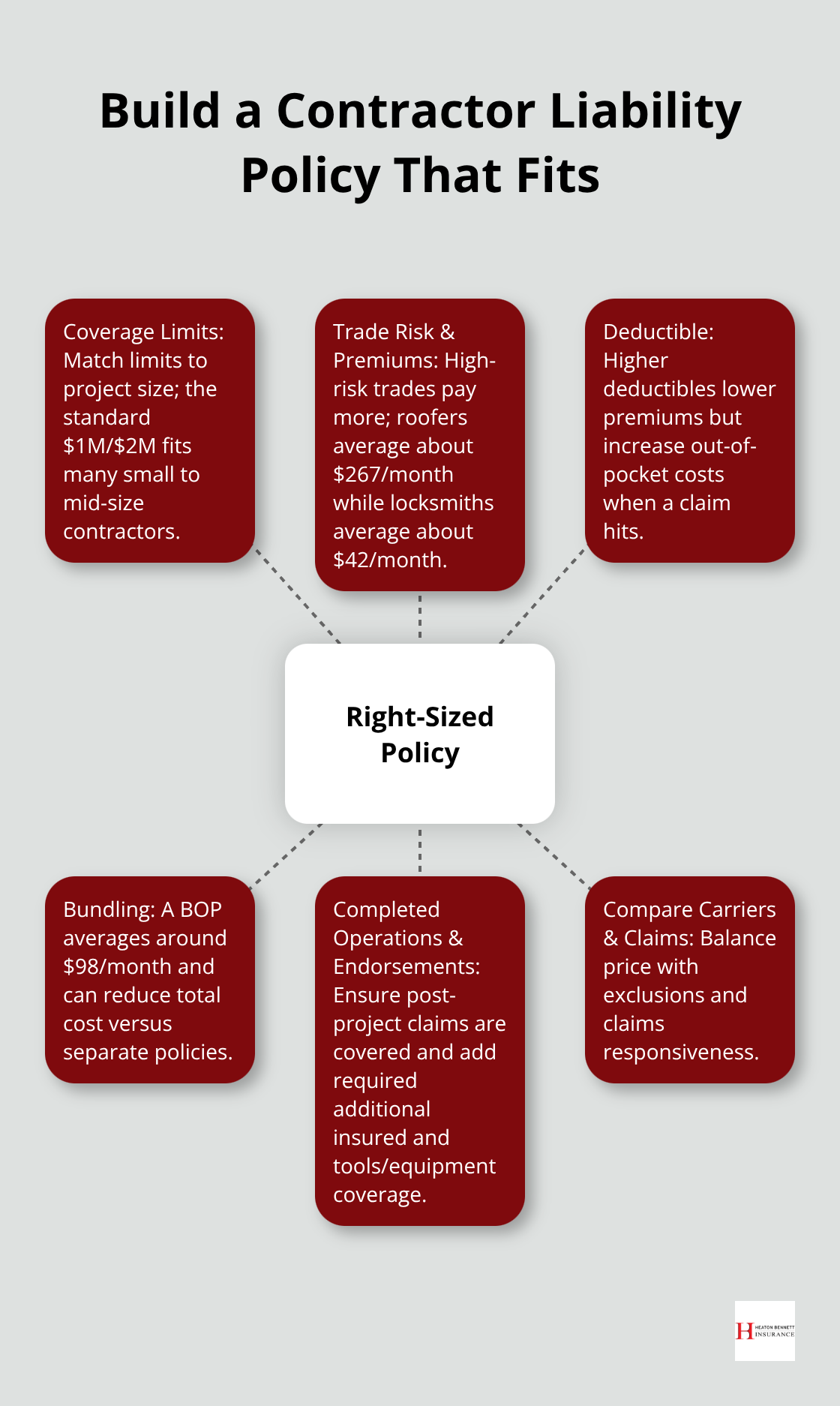

General Liability covers bodily injury and property damage claims, but it does not cover your own faulty workmanship-that gap is where many Austin contractors get burned. If you install a roof and it leaks three months later, General Liability will not pay to fix it. That exposure belongs to you. However, when a visitor trips on your equipment and breaks an arm, or your crew accidentally damages a client’s fence, General Liability steps in. Most Austin projects require at least $1,000,000 per occurrence in coverage limits. Larger commercial jobs or public sector work demand $2,000,000 or higher. The cost difference between $1M and $2M limits is usually modest-often $15 to $25 monthly-so paying for adequate limits makes financial sense.

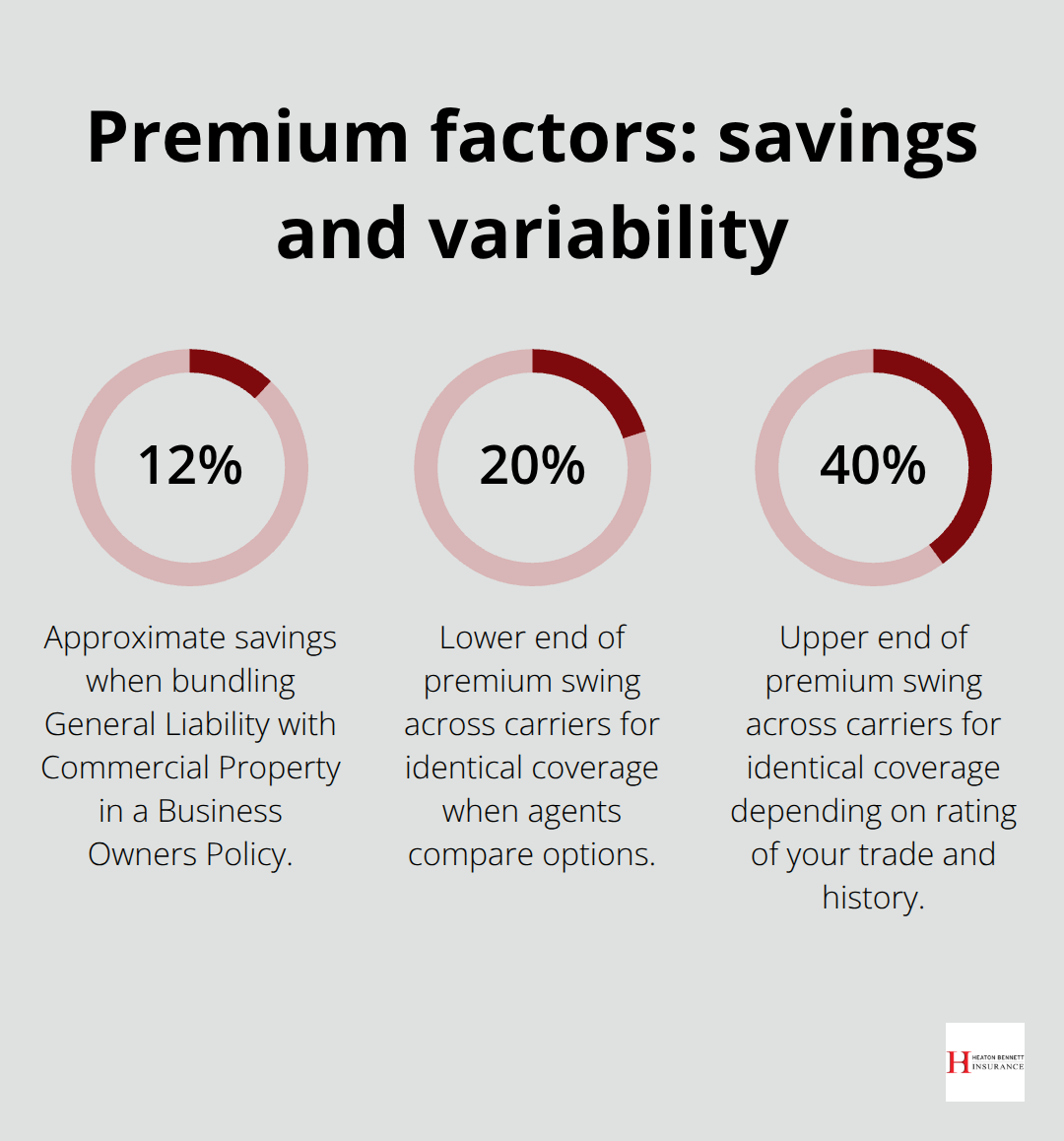

If you have a physical shop or office, a Business Owners Policy bundles General Liability with Commercial Property coverage for roughly 12% savings compared to buying them separately. Many Austin projects also require an additional insured endorsement, which extends your liability protection to the general contractor or property owner at no extra cost to add to your policy.

Workers Compensation: The Coverage You Cannot Skip

Workers Compensation in Texas remains optional unless you have employees or a contract mandates it, but that loophole has destroyed contractors who faced lawsuits after injuries. Texas Mutual has insured over 80,000 Texas businesses for workers comp and offers competitive premiums plus a dividend history that can offset costs. If you operate alone, the math might seem simple-skip it to save money. The reality is brutal: one serious employee injury without coverage creates personal liability exposure that can bankrupt you.

Commercial Auto and Equipment Protection

Commercial Auto is non-negotiable if you use any vehicle for work. Personal auto policies explicitly exclude business use, meaning your insurer will deny claims if you transport tools, travel between job sites, or conduct any business activity. Contractors Equipment Insurance protects tools and machinery from theft or damage. A single theft of $5,000 in equipment can wipe out months of savings; for Austin contractors with $10,000 or more in tools, this coverage costs roughly $300 to $500 annually and pays for itself after one loss.

Builders Risk and Flood Coverage

Builders Risk Insurance protects materials, fixtures, and structures you are responsible for during construction-fire, theft, wind, and hail are covered until project completion. Who purchases Builders Risk should be spelled out in your contract; if the client buys it, confirm coverage limits match your exposure. Central Texas flood risk demands separate flood insurance because standard policies exclude water damage. Flash flooding in Austin has caused significant losses, and coverage gaps leave contractors exposed.

Understanding these coverage types positions you to make informed decisions about which policies fit your specific operations. The next step involves finding a provider who can tailor these options to your actual business model and project scope.

Finding the Right Insurance Partner for Your Austin Contracting Business

National Carriers vs. Local Expertise

Selecting an insurance provider matters more than most contractors realize, because the wrong partner leaves you scrambling when you need coverage most. National carriers like Progressive offer competitive rates-the 2024 median of $60 monthly for new customers is attractive on the surface-but they operate through standardized underwriting that often misses the specific risks Austin contractors face. Local and regional carriers understand Central Texas flood exposure, the construction activity density around I-35 and MoPac, and project-specific requirements that national algorithms cannot capture. Texas Mutual has built trust across over 80,000 Texas businesses by offering workers compensation premiums plus a dividend history that returns money to policyholders, but they specialize in one coverage type.

Why Independent Agents Win on Comparison and Service

Independent agents in Austin have access to multiple carriers and can compare quotes across 5 to 10 options instead of locking you into a single company’s rates and terms. This matters because premium differences for identical coverage can swing 20 to 40 percent depending on how each carrier rates your specific trade and loss history. An independent agent also handles the administrative burden-issuing certificates of insurance same-day when a project deadline hits, adding additional insured endorsements without delays, and advocating for you if a claim dispute arises. Direct online insurers cut out the agent entirely and offer lower prices on standardized policies, but they cannot negotiate custom terms or provide guidance when your situation falls outside their standard boxes.

How to Request and Compare Quotes Effectively

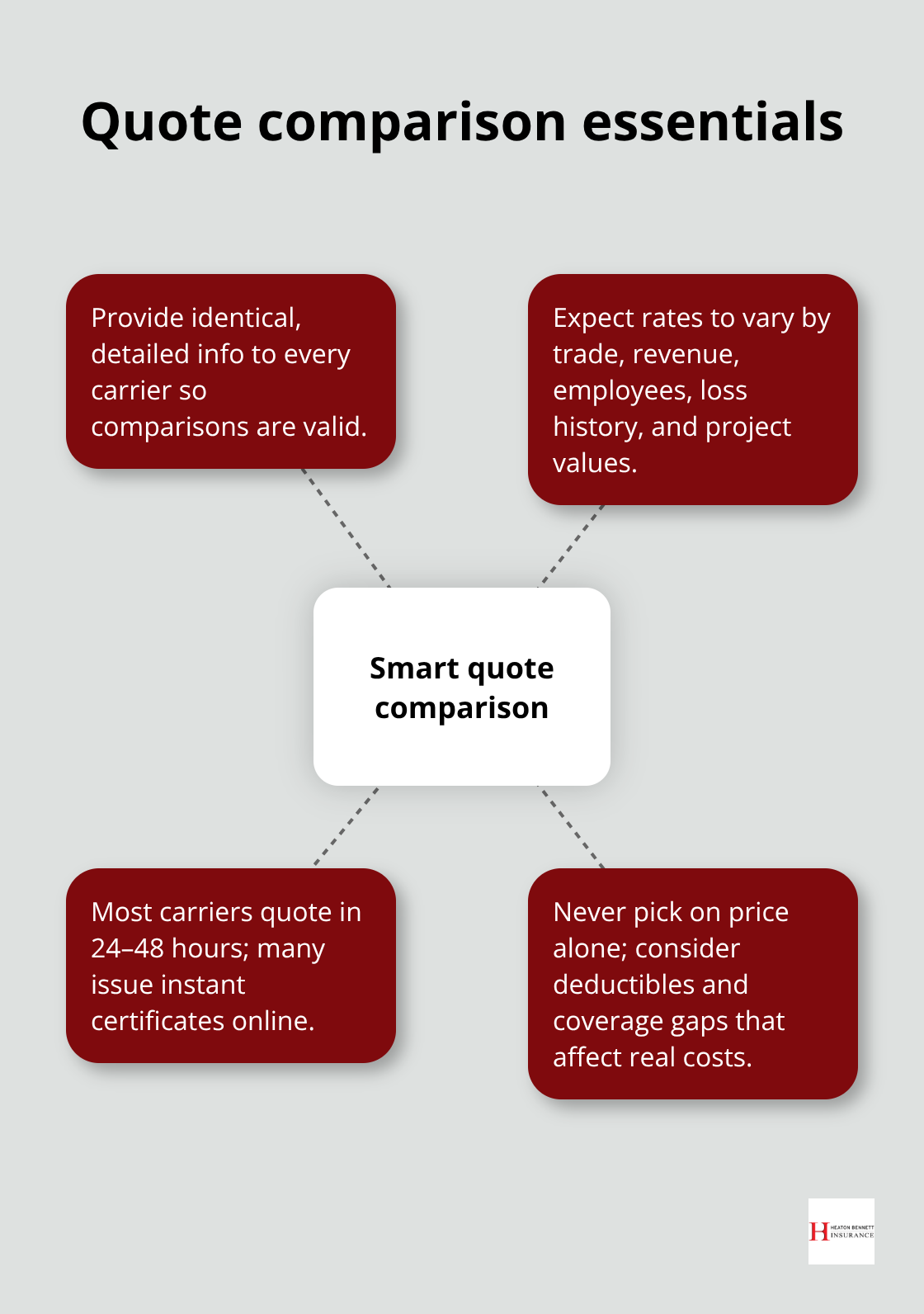

When you request quotes, always provide the same detailed information to each carrier-your specific trade, annual revenue, number of employees, loss history, and the typical project values you handle. Rates vary significantly based on these factors, and incomplete information produces misleading comparisons. Most carriers issue quotes within 24 to 48 hours, and many provide instant certificates of insurance that you can download immediately. Do not choose based solely on price; a $40 monthly policy with a $5,000 deductible and incomplete coverage creates false savings when a claim hits your deductible or falls outside your limits.

Evaluating Total Cost of Ownership

Instead, evaluate the total cost of ownership-monthly premium plus deductible exposure plus coverage gaps-across your likely project pipeline over the next 12 months. An independent agency in Austin provides access to multiple carriers with local expertise, meaning they understand Austin Build + Connect requirements and the nuances of project-specific coverage that protects your actual operations rather than a generic contractor profile.

Final Thoughts

Contractor insurance in Austin TX protects your business from financial ruin, but only when you select coverage that matches your actual operations rather than a generic contractor template. General Liability forms the foundation that every Austin project demands before you start work, while Workers Compensation, Commercial Auto, and equipment protection fill gaps that many contractors overlook until a loss forces them to pay out of pocket. State licensing requirements for electricians, plumbers, and HVAC technicians add another layer of mandatory coverage that varies by trade, and skipping these protections exposes you to direct lawsuits with no insurance backing.

The real decision comes down to finding a provider who understands Austin’s specific environment-Central Texas flood risk, local permitting through Austin Build + Connect, and project-specific endorsements that protect your actual exposure. National carriers offer competitive pricing, but they apply standardized underwriting that misses the nuances Austin contractors face on a daily basis. An independent agency gives you access to multiple carriers, meaning you compare quotes across different risk assessments instead of accepting a single company’s evaluation.

We at Heaton Bennett Insurance work with Austin contractors to build coverage that matches their specific trade, project pipeline, and risk tolerance. Start by gathering your business details-your trade, annual revenue, number of employees, and typical project values-then request quotes from multiple carriers using identical information so comparisons hold real meaning. Contact Heaton Bennett Insurance to discuss your situation and receive quotes that reflect your actual operations, not a generic profile.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.