![Vacation Rental Insurance for Owners [2025 Guide]](https://insureaustin.com/wp-content/uploads/emplibot/Vacation-Rental-Insurance-for-Owners-_2025-Guide__1766711421-1030x589.jpeg)

Vacation Rental Insurance for Owners [2025 Guide]

Vacation rental owners face a harsh reality: standard homeowners insurance won’t cover your guests or their belongings. Most policies explicitly exclude short-term rentals, leaving you exposed to significant financial risk.

At Heaton Bennett Insurance, we’ve seen too many owners learn this lesson the hard way. This guide walks you through the coverage gaps, your insurance options, and how to protect your investment properly.

Why Standard Homeowners Insurance Doesn’t Work for Vacation Rentals

Standard homeowners insurance policies are built for owner-occupied properties. The moment you rent your home to guests for short periods, you’ve fundamentally changed the risk profile in ways traditional policies simply don’t cover. According to the Insurance Information Institute, standard homeowners policies explicitly exclude rental activity without a dedicated endorsement, and most insurers won’t even add one for short-term rentals. Your policy was underwritten with the assumption that you and your family live there full-time. Guest turnover, unfamiliar people accessing the property multiple times monthly, and commercial activity transform the risk into something your homeowners insurer never agreed to protect.

The Liability Exposure Problem

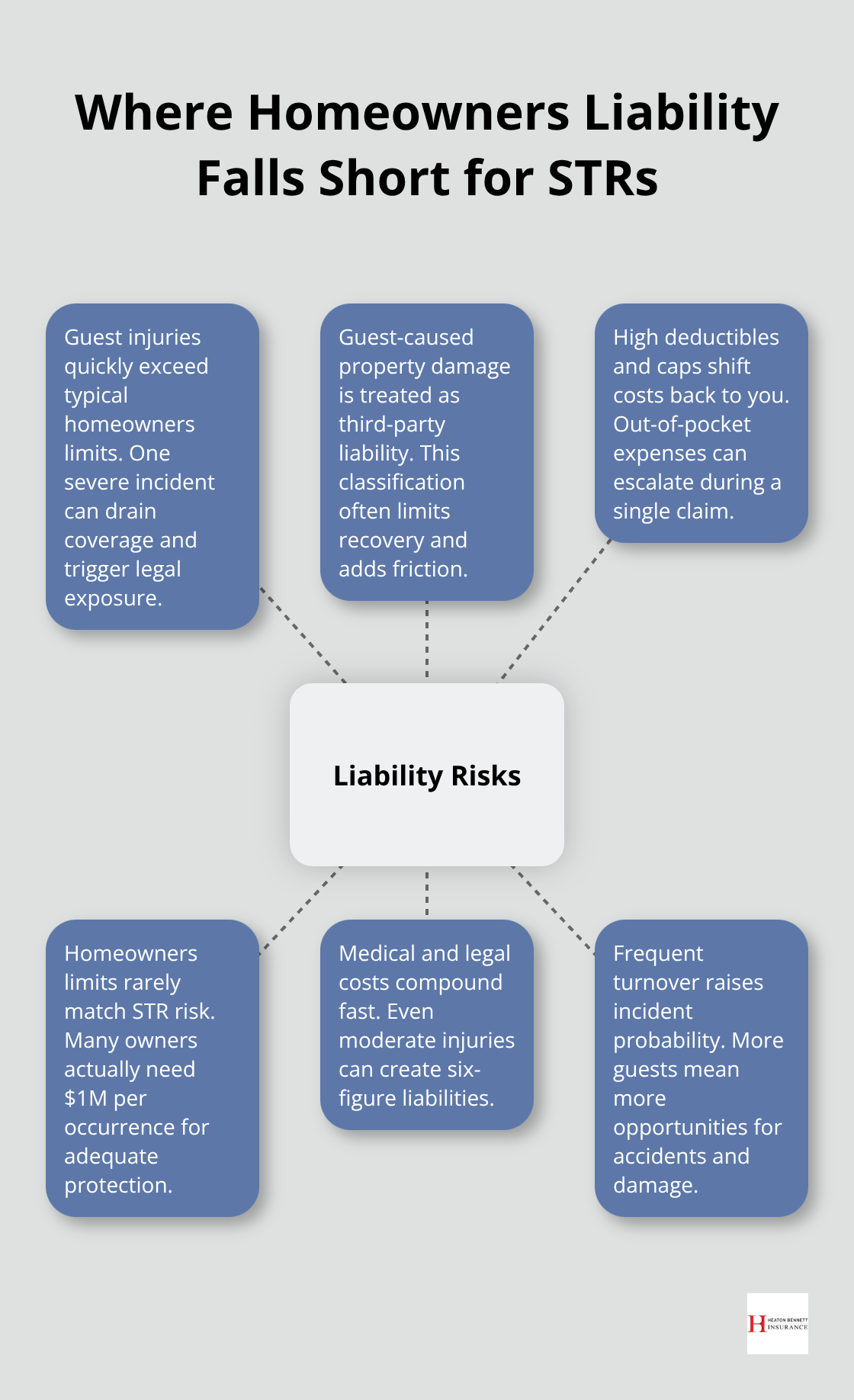

The liability exposure alone makes standard homeowners insurance inadequate. Your homeowners policy typically includes $100,000 to $300,000 in personal liability coverage, but vacation rental owners need $1 million per occurrence minimum, according to the Insurance Information Institute. When a guest slips on your stairs and requires emergency surgery, or their child drowns in your pool, your homeowners liability limit evaporates instantly. Beyond guest injuries, you face property damage claims from guests themselves. A guest causes a kitchen fire that damages cabinetry and appliances worth $15,000, or they destroy furniture and electronics during a wild party. Your homeowners policy treats guest-caused damage as third-party liability rather than property damage, which means deductibles and coverage limits work against you.

If your homeowners policy has a $2,500 deductible and a $300,000 liability limit, you’re personally responsible for everything above that threshold.

Why Business Income Protection Matters Most

Here’s what separates vacation rental owners from homeowners: your property generates revenue. When a covered event damages your rental, you lose income while repairs happen. Standard homeowners policies don’t include business interruption or loss-of-rent coverage. If a water pipe bursts and takes your property offline for 30 days during peak season, you lose $6,000 or $10,000 in bookings with zero protection. Dedicated vacation rental policies include actual loss sustained business income with no time limits, which means you recover the full income you would have earned during repairs. The Insurance Information Institute specifically recommends loss-of-rental income coverage as a core component for STR owners. Without it, a single claim can wipe out months of profit.

Property Damage Claims From Guests

Guest-caused damage represents a distinct risk that homeowners policies handle poorly. Your homeowners coverage treats damage caused by guests as a liability claim rather than property damage, which creates a coverage mismatch. A guest spills red wine on your hardwood floors, or they damage your HVAC system through misuse-your homeowners policy won’t cover these losses the way a vacation rental policy would. Dedicated vacation rental insurance covers guest-caused damage to the property itself, including accidental and intentional damage, with no sub-limits on theft or vandalism. This distinction matters enormously when you calculate the true cost of a claim. Your property’s revenue potential is a business asset that requires business insurance, not homeowners insurance, and the next section explores the specific coverage types that actually protect vacation rental owners.

Your Coverage Options Beyond Standard Homeowners

Why Platform Protection Falls Short

Platform host protection programs sound appealing until you read the fine print. Airbnb offers up to $1 million in Host Protection coverage, but this is not a comprehensive insurance policy-it’s a liability backstop with significant exclusions. The program covers guest injuries and third-party liability but leaves your property contents, building damage, theft, and business income unprotected. According to the Insurance Information Institute, platform protection should supplement your dedicated insurance, never replace it. These programs have annual aggregate caps and notable exclusions that create dangerous gaps. A guest steals $8,000 worth of electronics, or they cause $12,000 in water damage to your kitchen-platform protection won’t cover either scenario.

What makes this worse is that many owners believe platform coverage is sufficient and operate without a real policy. In 2024, roughly 2.4 million short-term rental listings were active in the United States, yet most owners rely on platform protection alone, leaving themselves dangerously exposed. Vrbo and other platforms have similar limitations. The data proves that platform programs alone cannot protect your investment adequately.

How Dedicated Vacation Rental Policies Work Differently

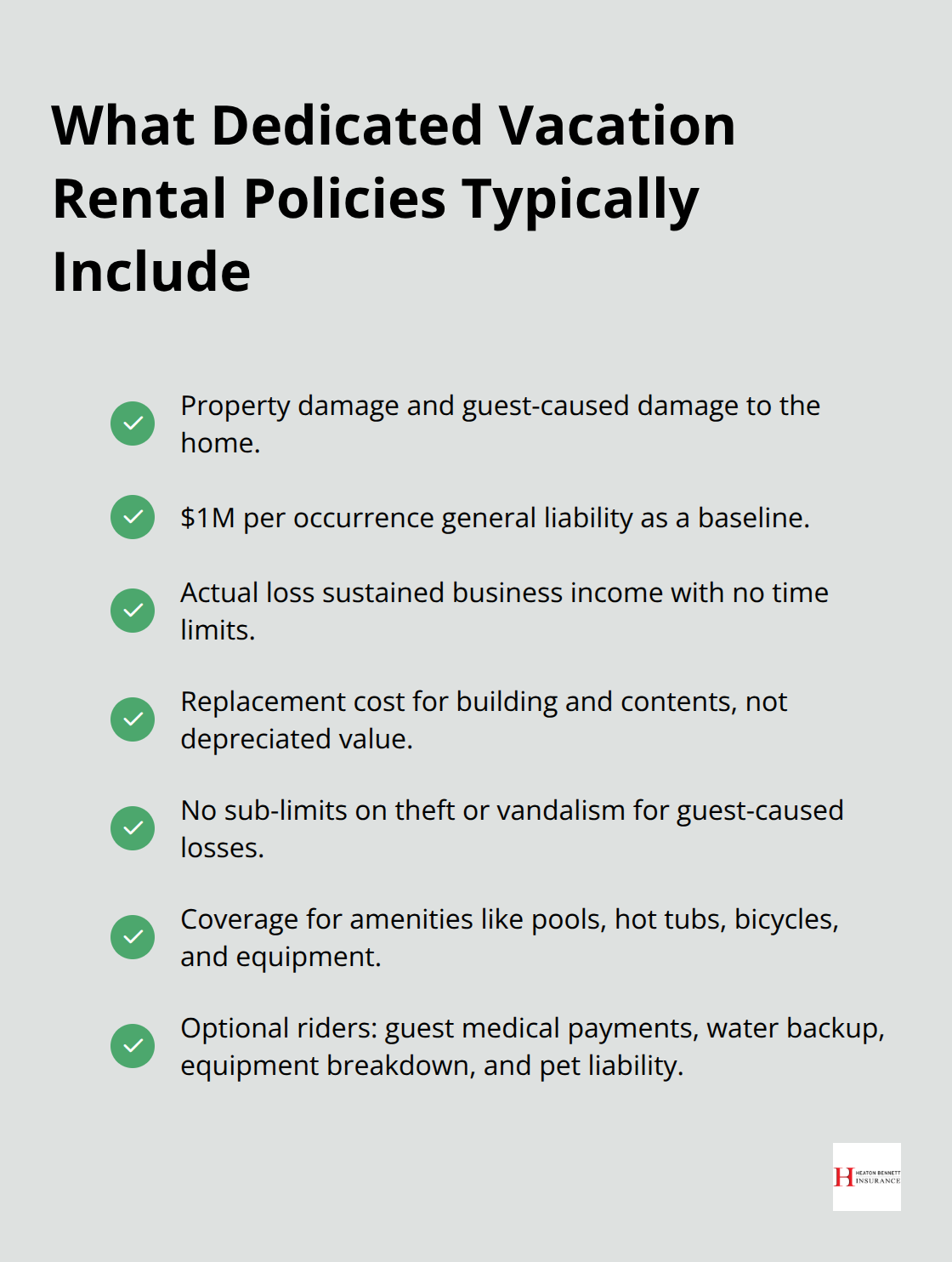

Dedicated vacation rental insurance policies are fundamentally different because they’re built for your business model. These policies cover property damage, guest-caused damage, general liability with $1 million per occurrence minimum, and actual loss sustained business income with no time limits. Unlike platform protection, dedicated policies include replacement cost valuation for building and contents, meaning your furniture and appliances are covered for what it costs to replace them new, not their depreciated value.

Coverage extends to amenities like pools, hot tubs, bicycles, and equipment with no sub-limits on guest damage or theft. Lloyd’s of London-backed providers have set the industry standard, covering over 100,000 owners and offering policies underwritten to commercial standards rather than homeowner standards. You can add riders for guest medical payments, water backup, equipment breakdown, and pet liability depending on your property’s specific risks.

Understanding Premium Costs and Coverage Variations

The cost varies significantly based on property value, occupancy rate, location, and amenities. Properties with 6 or more bedrooms showed 12.61% demand growth in 2025 according to AirDNA, which means higher replacement values and correspondingly higher premiums. A 3-bedroom property in a low-risk area might cost $800 annually, while a luxury 6-bedroom with a pool in a competitive market could run $3,500 or more.

If your rental includes a pool or hot tub, your liability exposure increases dramatically, and dedicated policies account for this with appropriate coverage and pricing. The key difference from platform protection is that dedicated policies actually transfer risk to an insurance company, whereas platform programs leave most risk on you.

Selecting the Right Provider for Your Needs

When you evaluate providers, verify that your chosen platform (Airbnb, Vrbo, or direct bookings) is explicitly covered under the policy, and confirm that the insurer offers quick claims processing-some providers settle claims within 4 business days, which matters enormously when you need income recovery during downtime. An independent insurance agent can help you compare multiple carriers and find the policy that matches your specific property type and business model, rather than forcing you into a one-size-fits-all solution.

Matching Coverage to Your Specific Rental Model

The single biggest mistake vacation rental owners make is purchasing generic coverage that doesn’t match how they actually operate. A luxury 5-bedroom beachfront property with a pool rented weekly at $400 per night faces entirely different risks than a modest 2-bedroom urban apartment rented to business travelers. Your coverage must reflect your actual exposure, which means starting with a brutally honest assessment of what you own and what guests do to it.

Property Value and Inventory Requirements

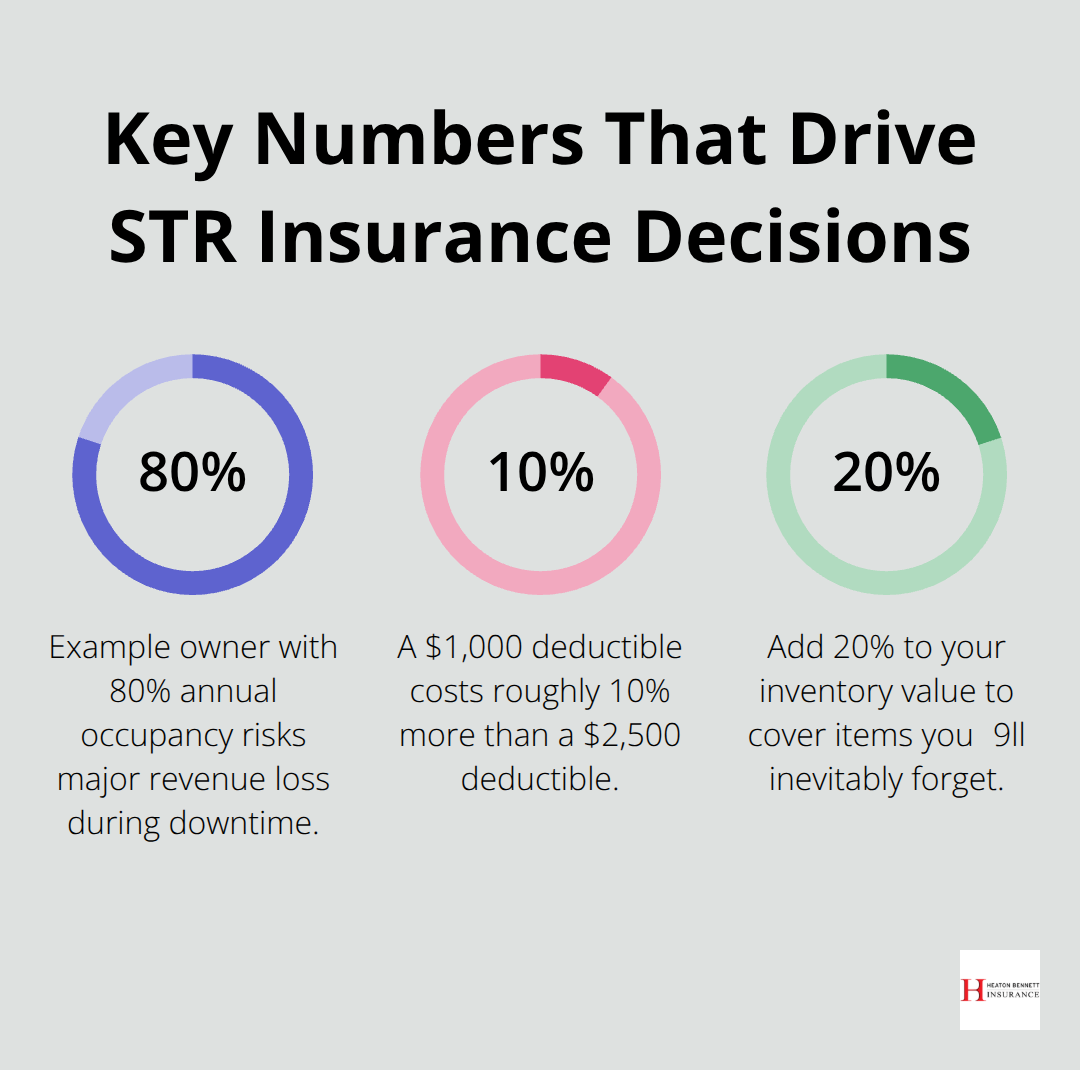

Property value matters enormously because it determines your replacement cost coverage needs. If your rental contains $45,000 worth of furniture, appliances, and fixtures, your contents limit must cover that amount in full. Most owners underestimate property value by 30 to 40 percent because they forget to include kitchen equipment, bedding, artwork, outdoor furniture, and electronics. Create a detailed inventory with photos and receipts, then add 20 percent to account for items you’ll inevitably forget. This inventory becomes your insurance baseline and your claims documentation if something happens.

Occupancy Rates and Business Income Coverage

Occupancy rate directly impacts your business income coverage needs. An owner with 80 percent annual occupancy in a market with $200 nightly rates loses roughly $48,000 per month during complete downtime. Your loss-of-rent coverage must reflect this reality, not some theoretical average. AirDNA data shows occupancy around 54.9 percent nationally in 2025, but your specific property and market will differ significantly.

Calculate your actual monthly revenue loss and verify your business interruption coverage matches that number. If you operate multiple properties, portfolio policies often deliver 15 to 25 percent lower combined premiums than insuring each property separately, which makes this a financial decision as much as a coverage decision.

Liability Limits and Amenity-Based Exposure

Your liability limits require matching your amenities and guest volume. The $1 million per occurrence standard exists because guest injuries happen frequently enough that lower limits get exhausted. A guest drowns in your pool, or they suffer a serious injury from falling on your stairs, and medical costs plus legal liability easily exceed $500,000. If you have a pool or hot tub, your liability exposure doubles, and some insurers will require $2 million per occurrence coverage for properties with water features.

Deductibles and Claims Frequency

Deductibles create a critical trade-off between premium cost and out-of-pocket expense. A $500 deductible costs roughly 15 to 20 percent more annually than a $1,000 deductible, but a $1,000 deductible costs roughly 10 percent more than a $2,500 deductible. The real question is how many claims you expect in a given year. High-turnover properties with frequent guest changes experience more damage claims, so lower deductibles make financial sense. A property with 40 guest turnovers annually will almost certainly have at least one claim, making a $500 deductible worth the extra cost.

Exclusions, Sub-Limits, and Platform Verification

Review policy exclusions with specific attention to what your property actually contains and how guests use it. Water damage, theft, and vandalism should have no sub-limits or exclusions. Pet damage requires explicit coverage if you allow animals, and the Insurance Information Institute recommends verifying coverage for theft and vandalism specifically because these exclusions create dangerous gaps. Ask carriers directly whether the policy covers intentional damage by guests, not just accidental damage, because this distinction determines whether a guest’s deliberate destruction gets covered. Confirm that your platform of choice appears explicitly in the policy language. Airbnb-specific exclusions exist with some carriers, and Vrbo coverage varies widely. A 3-minute quote before committing to a full application helps eliminate carriers that won’t cover your specific situation.

Final Thoughts

Vacation rental insurance for owners isn’t optional anymore. The market has matured, the risks are real, and the financial consequences of operating without proper coverage far exceed the cost of a dedicated policy. Standard homeowners insurance won’t protect you, platform protection leaves dangerous gaps, and the difference between adequate coverage and inadequate coverage often determines whether a single claim bankrupts your business or gets handled professionally.

Your next step is straightforward: obtain quotes from at least three carriers that specialize in vacation rental coverage. Ask each carrier specifically about your property type, your occupancy rate, and your platform of choice. Verify that guest-caused damage, theft, and vandalism are covered with no sub-limits, and confirm that business income protection includes actual loss sustained coverage with no time restrictions. Calculate your property’s replacement value honestly, then add 20 percent to account for items you’ll forget, and review deductibles against your expected claim frequency.

At Heaton Bennett Insurance, we understand that vacation rental owners need more than a generic policy. Contact us at Heaton Bennett Insurance to start your Security Snapshot process and get a clear picture of your actual coverage needs. Peace of mind comes from knowing your investment is protected by real insurance, not platform promises or wishful thinking.