Why Is My Auto Insurance Premium So High?

Your auto insurance premium feels high because multiple factors work together to determine your rate. At Heaton Bennett Insurance, we’ve helped thousands of drivers understand what drives their costs up-and more importantly, how to bring them down.

The good news is that you have more control over your premium than you might think. This guide breaks down exactly what insurers look at and shows you concrete steps to lower what you pay.

What Really Drives Your Auto Insurance Premium

Your Driving Record Sets the Foundation

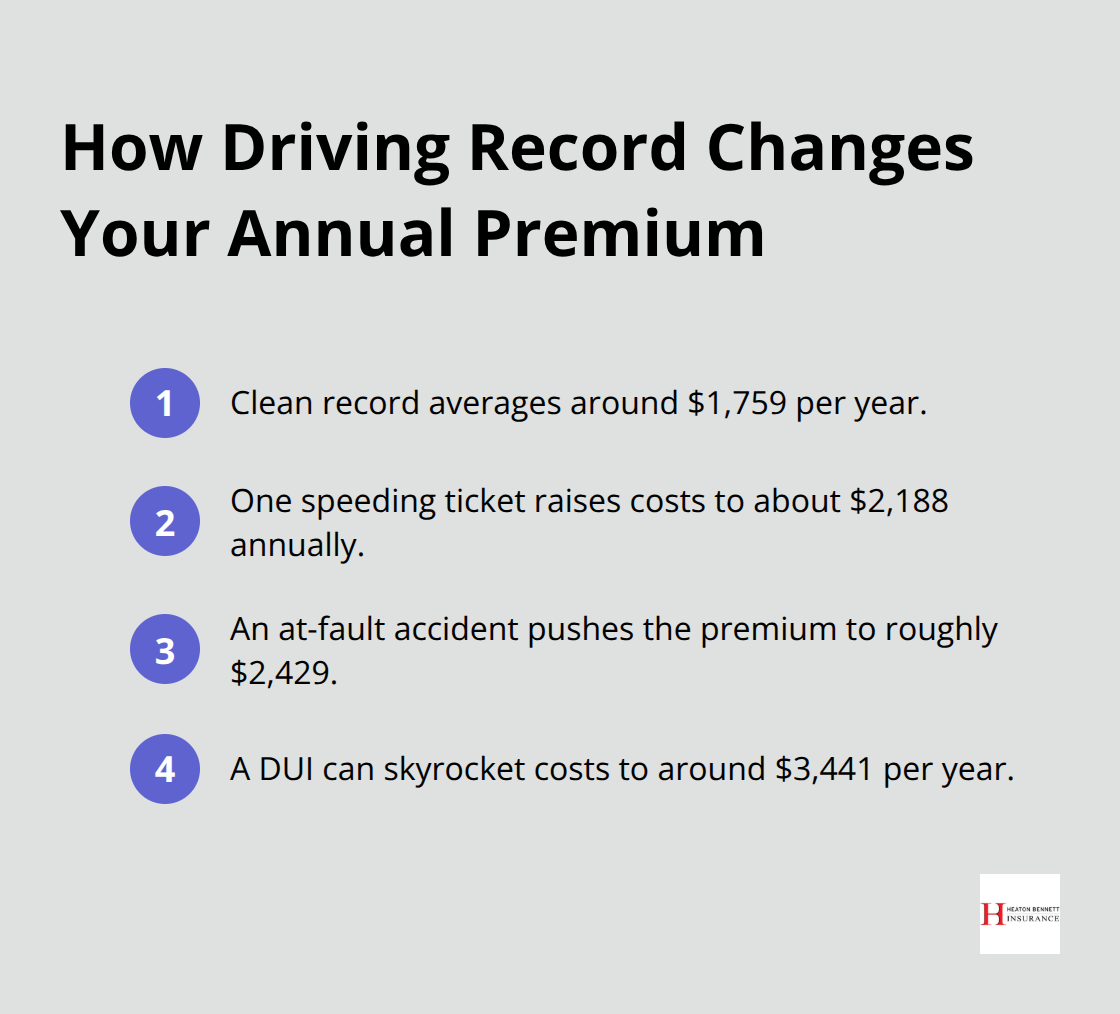

Your driving record is the single most important factor insurers examine, and the data proves it. According to The Zebra, a driver with no accidents or tickets pays around $1,759 annually, while one speeding ticket bumps that to $2,188, an accident pushes it to $2,429, and a DUI skyrockets the cost to $3,441. These aren’t small differences-they’re permanent reminders that your behavior behind the wheel directly determines what you pay. One bad decision can cost you thousands over the next three to five years.

If you’ve had violations, the best strategy is to drive cleanly going forward and watch your rates drop as those incidents age off your record. Your actions today shape your premiums for years to come.

Age and Gender: The Numbers Behind the Rates

Age matters far more than most people realize. Teenage drivers face premiums around $5,039 per year, while drivers in their 20s average $2,284, and those in their 50s drop to around $1,555, according to The Zebra. This isn’t discrimination-it’s math based on real crash data showing younger, less experienced drivers cause more expensive accidents. Your gender also influences rates, though the effect is smaller and primarily affects drivers under 25.

Vehicle Choice and Safety Features

The vehicle you choose to insure carries enormous weight in the calculation. Luxury cars and sports vehicles cost significantly more to insure because repair and replacement costs are higher. A Honda Civic costs far less to insure than a BMW or Tesla, and safety features matter too. Vehicles with strong safety ratings from the Insurance Institute for Highway Safety qualify for discounts that can meaningfully reduce your premium.

Credit Score and Location Impact

Your credit score might surprise you as a rating factor, but it’s real and substantial. Drivers with poor credit can pay over $1,500 more per year than those with excellent credit, according to The Zebra. Four states-California, Hawaii, Massachusetts, and Michigan-ban or limit credit-based scoring, but everywhere else, insurers use it extensively. This means maintaining good credit isn’t just about your financial health; it directly affects your insurance costs. Pay your bills on time and monitor your credit report for errors that could unfairly inflate your score.

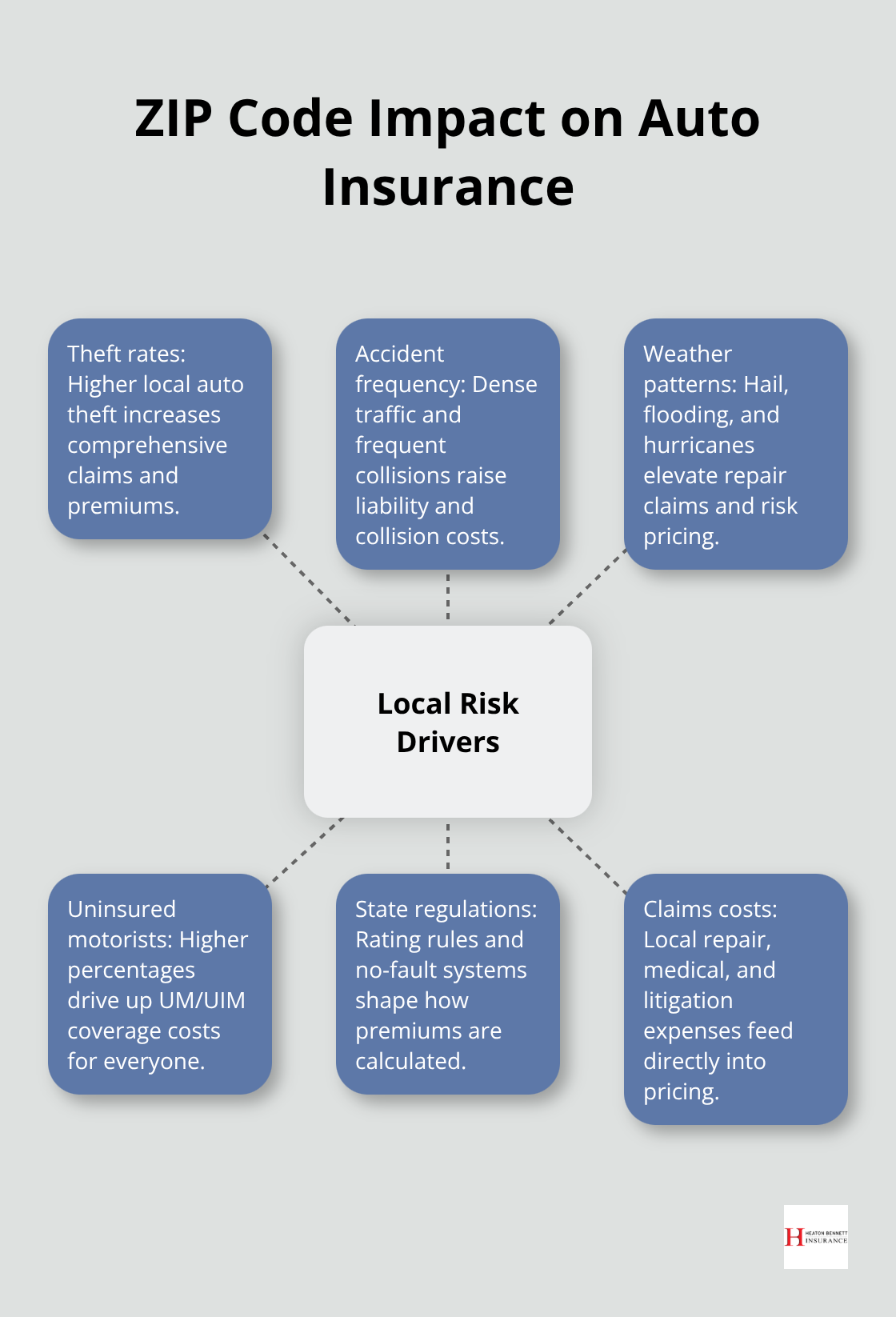

Location is another massive driver of premiums that catches people off guard. Moving to a different ZIP code, even within the same city, can trigger significant price changes because insurers use local risk data tied to theft rates, accident frequencies, and weather exposure. Michigan averages about $193 per month for full coverage while Ohio sits around $111, and Florida reaches about $253 due to high uninsured-driver rates and hurricane exposure.

Mileage and Risk Exposure

Your annual mileage also affects what you pay. Drivers who log under 7,500 miles yearly pay less than those driving 15,000 or more miles because exposure to risk increases with time on the road. If your commute changed after a move or your work situation shifted, your mileage profile likely changed too-and insurers will reprice your policy accordingly. Understanding these specific factors about your situation puts you in position to identify which ones you can actually control and which ones require a different approach, like shopping for better rates or adjusting your coverage strategy.

How Insurers Price Your Policy

Insurance companies use sophisticated risk assessment models that analyze hundreds of data points about you, your vehicle, and your location to predict the likelihood you’ll file a claim. The algorithms are proprietary and vary between carriers, which is why two people with identical driving records and vehicles receive wildly different quotes from different insurers. According to The Zebra, typical monthly premiums among major carriers range from USAA at around $114 to Allstate at around $201, illustrating just how much variation exists. Each company weights risk factors differently based on their own claims history and business model.

Some insurers heavily penalize young drivers while others use telematics data to reward safe driving habits. Some treat accidents from five years ago as serious red flags while others let them fade faster. The only way to know your actual price is to get quotes from multiple carriers, not just one or two. Shopping around isn’t optional if you want fair pricing-it’s the single most effective way to combat high premiums because you force competition to work in your favor.

Your ZIP Code Carries More Weight Than Your Driving Record

Your ZIP code determines more of your premium than you’d expect, sometimes outweighing your driving record entirely. Michigan drivers pay approximately $193 monthly for full coverage while Ohio drivers average around $111 for the same protection, according to The Zebra. That $82 monthly difference has nothing to do with individual driving skill and everything to do with state regulations, local claim costs, and risk exposure.

Even moving within the same metro area triggers repricing because insurers use detailed local data about theft rates, accident frequencies, weather patterns, and uninsured motorist percentages. When you update your address mid-policy, insurers reprice immediately, sometimes increasing your premium even if you relocate to what feels like a safer neighborhood. The new ZIP code’s rating territory, local traffic patterns, and claims history override your personal profile. A driver with a perfect record faces a premium jump simply from relocating.

State Regulations Create Massive Price Swings

Florida’s average of $253 monthly reflects high uninsured-driver rates and hurricane exposure that push costs upward for everyone in the state. California runs about 16 percent above the national average due to high living costs and congestion, while Hawaii sits roughly 38 percent below average thanks to strict rating limitations and fewer drivers. If you’re considering a move, calculate the insurance impact before signing a lease or mortgage because it can cost hundreds or thousands annually.

These state-level differences stem from regulatory frameworks that vary significantly. No-fault states require personal injury protection and have different claims processes, which affects premium structure and medical expense coverage. Four states-California, Hawaii, Massachusetts, and Michigan-ban or limit credit-based insurance scores in pricing, which shifts how insurers calculate premiums. Understanding your state’s rules helps explain why your neighbor in another state pays so differently for identical coverage.

How Different Carriers Weight the Same Information

Two insurers analyzing your exact same profile produce different numbers because they prioritize risk factors differently. One carrier might view a three-year-old accident as a major concern while another considers it largely resolved. One might charge heavily for young drivers while another offers competitive rates through telematics programs that track safe driving. This variation means the cheapest quote isn’t always the best value-you need to compare final premiums across multiple carriers to find what actually works for your situation. The carrier that offers the lowest rate for a 35-year-old with a clean record might charge significantly more for a 22-year-old with one speeding ticket. Shopping around reveals these differences and puts you in control of finding the rate that matches your actual risk profile rather than accepting the first number you receive.

How to Actually Lower Your Premium

Shop Around to Force Competition in Your Favor

The most direct way to lower your premium is to shop around, and this step matters more than almost anything else you can do. According to The Zebra, typical monthly premiums from major carriers range from USAA at $114 to Allstate at $201, meaning the same coverage costs you $1,044 more annually depending on which company you choose. You’re not powerless against high rates-you’re simply accepting whatever number appears on your renewal notice instead of forcing competition to work for you. Get quotes from at least three different carriers for identical coverage levels and deductibles, then compare the final premiums side by side. The cheapest option isn’t always the best value, but you’ll immediately see where your current insurer stands relative to the market. If you’re paying significantly more, switching carriers is often the fastest way to reduce what you owe without changing your driving habits or vehicle.

Bundle Policies and Adjust Your Deductible

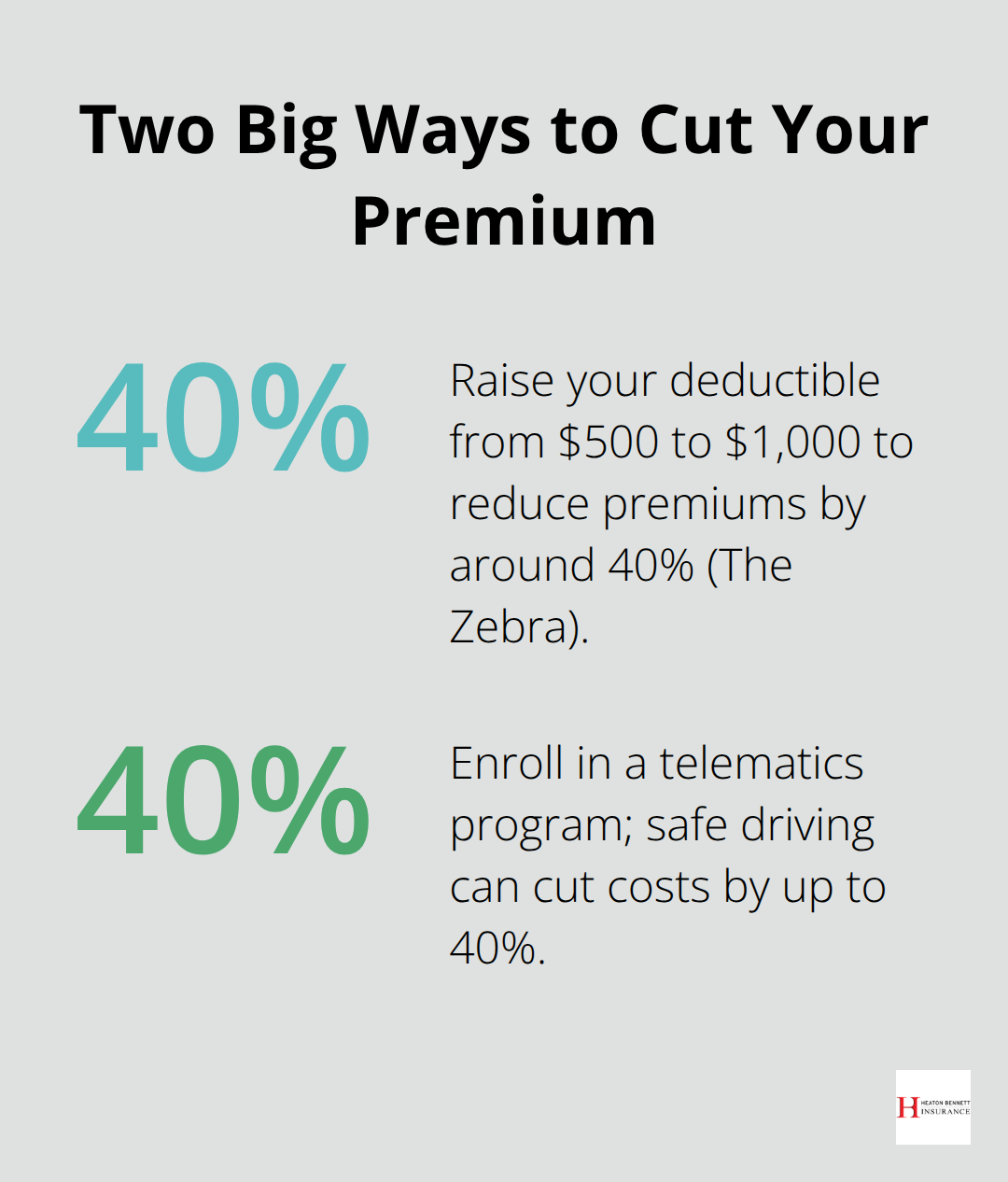

Bundling your auto policy with homeowners or renters insurance delivers measurable savings that compound quickly. Bundling typically cuts costs across both policies, and The Zebra data shows this remains one of the most effective discounts available. Raising your deductible from $500 to $1,000 can reduce your premium by 40 percent or more, according to The Zebra, but only make this move if you actually have $1,000 set aside to cover a claim. You control this lever completely-many drivers overlook this option because they assume deductibles are fixed.

Evaluate Your Coverage and Mileage Profile

On older vehicles worth less than ten times your annual premium, dropping collision and comprehensive coverage entirely makes financial sense. Use Kelley Blue Book or Edmunds to calculate your car’s actual value before deciding. Your annual mileage also influences your rate, so if you’ve shifted to working from home or carpooling, contact your insurer to update your mileage profile because some carriers offer low-mileage discounts for drivers under 7,500 miles yearly.

Leverage Telematics and Additional Discounts

Telematics programs that track your driving behavior can cut premiums by up to 40 percent for safe drivers, making this particularly valuable if you have a clean driving record. Defensive driving courses and good student discounts for those under 25 provide additional savings opportunities, though availability varies by state and insurer. The reality is that multiple small adjustments-bundling, higher deductibles, accurate mileage reporting, and discount hunting-combine to produce substantial savings, but none of these tactics matter if you shop with only one carrier because you’ll never know if you’re getting a competitive price in the first place.

Final Thoughts

Your auto insurance premium reflects dozens of factors working together, but you control more than you realize. Your driving record, age, vehicle choice, credit score, location, and mileage all influence what you pay, yet most drivers never question whether they’re getting a fair price. The answer to why your auto insurance premium is so high often comes down to one simple fact: you haven’t shopped around, which means you’re accepting whatever number appears on your renewal notice instead of forcing competition to work in your favor.

Start by obtaining quotes from at least three different carriers for the exact same coverage and deductibles. Next, evaluate your deductible level and coverage composition to ensure you’re not paying for protection you don’t need while maintaining adequate limits for your situation. Bundle your auto policy with homeowners or renters insurance if possible, update your mileage profile if your driving habits have changed, and explore telematics programs that reward safe driving with meaningful discounts.

We at Heaton Bennett Insurance understand that navigating these decisions alone feels overwhelming. As an independent agency in Austin, Texas, we have access to multiple carriers and can pull quotes from different companies to show you exactly where your current premium stands in the market. Visit Heaton Bennett Insurance to start your personalized quote process and discover how much you could actually save.