How Much Does Liability Insurance Cost for Small Business?

Small business owners face a common question: how much does liability insurance cost for a small business? The answer varies significantly based on multiple factors.

We at Heaton Bennett Insurance see costs ranging from $400 to $3,000 annually, depending on your industry, business size, and coverage needs. Understanding these variables helps you budget effectively and find the right protection for your company.

What Drives Your Liability Insurance Costs

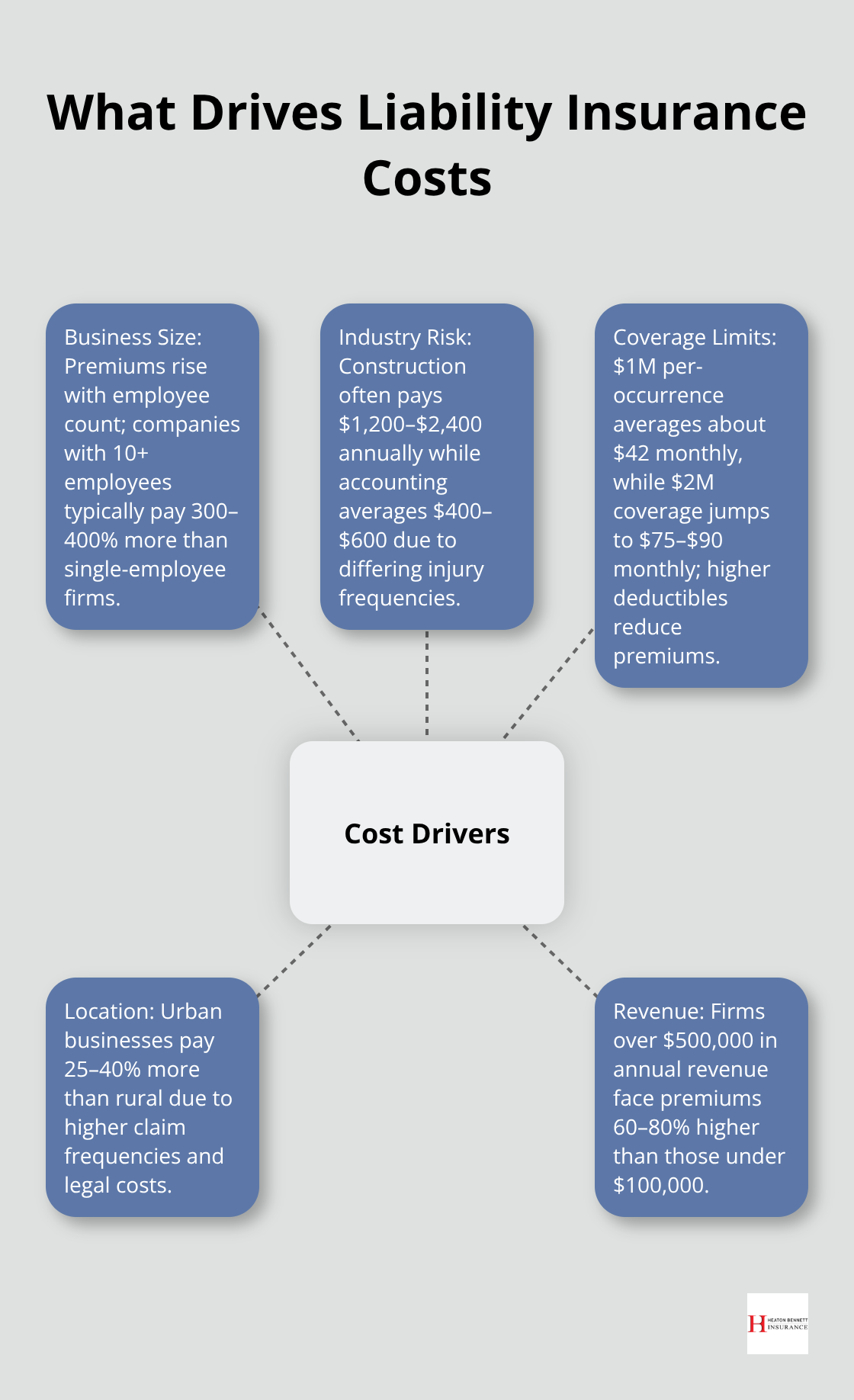

Business Size Determines Premium Structure

Your business size directly impacts premium calculations. Companies with one employee pay approximately $45 monthly for workers’ compensation, while multi-employee operations face exponentially higher costs. The Hartford data shows businesses with 10+ employees typically pay 300-400% more than single-employee companies.

Your annual revenue affects rates significantly. Businesses that earn over $500,000 face premiums 60-80% higher than those under $100,000 in revenue. This revenue-based calculation reflects the increased exposure and potential claim sizes that larger operations face.

Industry Risk Classifications Set Base Rates

Your industry classification determines your base premium rate. Construction companies pay $1,200-2,400 annually for general liability coverage, while accounting firms average just $400-600. Progressive Insurance reports that tree trimmers and contractors face the highest premiums due to injury frequency, while financial advisors enjoy the lowest rates.

Manufacturing businesses fall into high-risk categories, with premiums often exceeding $2,000 annually. Service-based businesses like consulting typically pay 50-70% less than product-based companies. These classifications reflect historical claim data and risk assessments specific to each industry type.

Coverage Limits Control Your Budget

Your policy limits dramatically affect costs. A $1 million per-occurrence policy averages $42 monthly, while $2 million coverage jumps to $75-90 monthly. Most Insureon customers choose $1 million limits with $500 deductibles (the most popular combination among small businesses).

Higher deductibles reduce premiums by 15-25%. Raising your deductible from $250 to $1,000 can save $200-400 annually. Aggregate limits matter too: $2 million aggregate coverage costs 20-30% more than $1 million aggregate limits.

Location Impacts Premium Calculations

Urban businesses pay 25-40% more than rural counterparts due to higher claim frequencies and legal costs. Metropolitan areas present increased liability exposure through higher population density and elevated litigation rates.

Natural disaster zones also affect rates significantly. Businesses in flood-prone or earthquake-active regions face additional premium adjustments that reflect these environmental risks. These location-based factors combine with your other risk characteristics to create your final premium structure, which leads us to examine the specific costs across different liability insurance types.

What Does Each Liability Insurance Type Actually Cost

General Liability Insurance Sets the Foundation

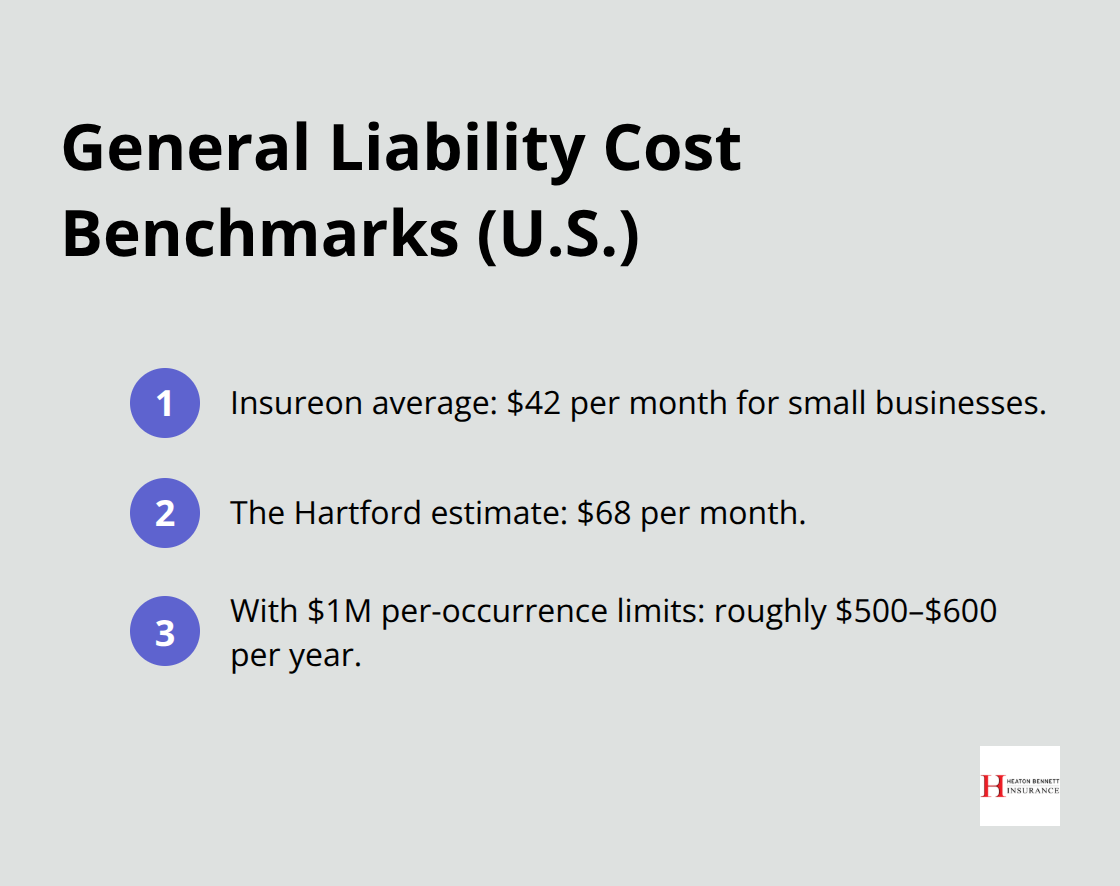

General liability insurance forms the base protection layer for most businesses, with small companies paying an average of $42 monthly according to Insureon data. The Hartford reports slightly higher figures at $68 monthly, while businesses that select $1 million per-occurrence limits typically see costs around $500-600 annually.

Professional service companies like accounting firms pay the lowest rates at $400-600 yearly. Construction businesses face premiums of $1,200-2,400 annually due to elevated injury risks. This wide range reflects the direct correlation between industry risk levels and premium calculations.

Professional Liability Insurance Commands Higher Rates

Professional liability insurance costs significantly more than general coverage, with most service-based businesses paying $50-61 monthly. Medical professionals and technology consultants face the steepest rates, often exceeding $200 monthly due to high-value claim potential.

Legal and financial advisory firms typically pay $75-150 monthly, which reflects the substantial financial exposure these professions carry. Newer businesses without established track records pay 20-30% more than established companies with clean claims histories (a factor that insurance carriers weigh heavily in their underwriting process).

Product Liability Insurance Shows Maximum Variation

Product liability coverage demonstrates the widest cost variation among liability types. Food manufacturers and supplement companies face premiums of $150-400 monthly due to contamination risks and FDA regulations. Electronics manufacturers typically pay $100-250 monthly, while clothing and textile businesses see rates of $75-150 monthly.

Companies that manufacture children’s products or medical devices face the highest premiums, often exceeding $500 monthly. Import businesses add another complexity layer, with international product liability often doubling domestic rates due to supply chain risks and foreign manufacturing standards.

These varying costs across liability types highlight why businesses need strategic approaches to manage their insurance expenses effectively.

How Can You Cut Your Liability Insurance Costs

Bundle Policies for Maximum Savings

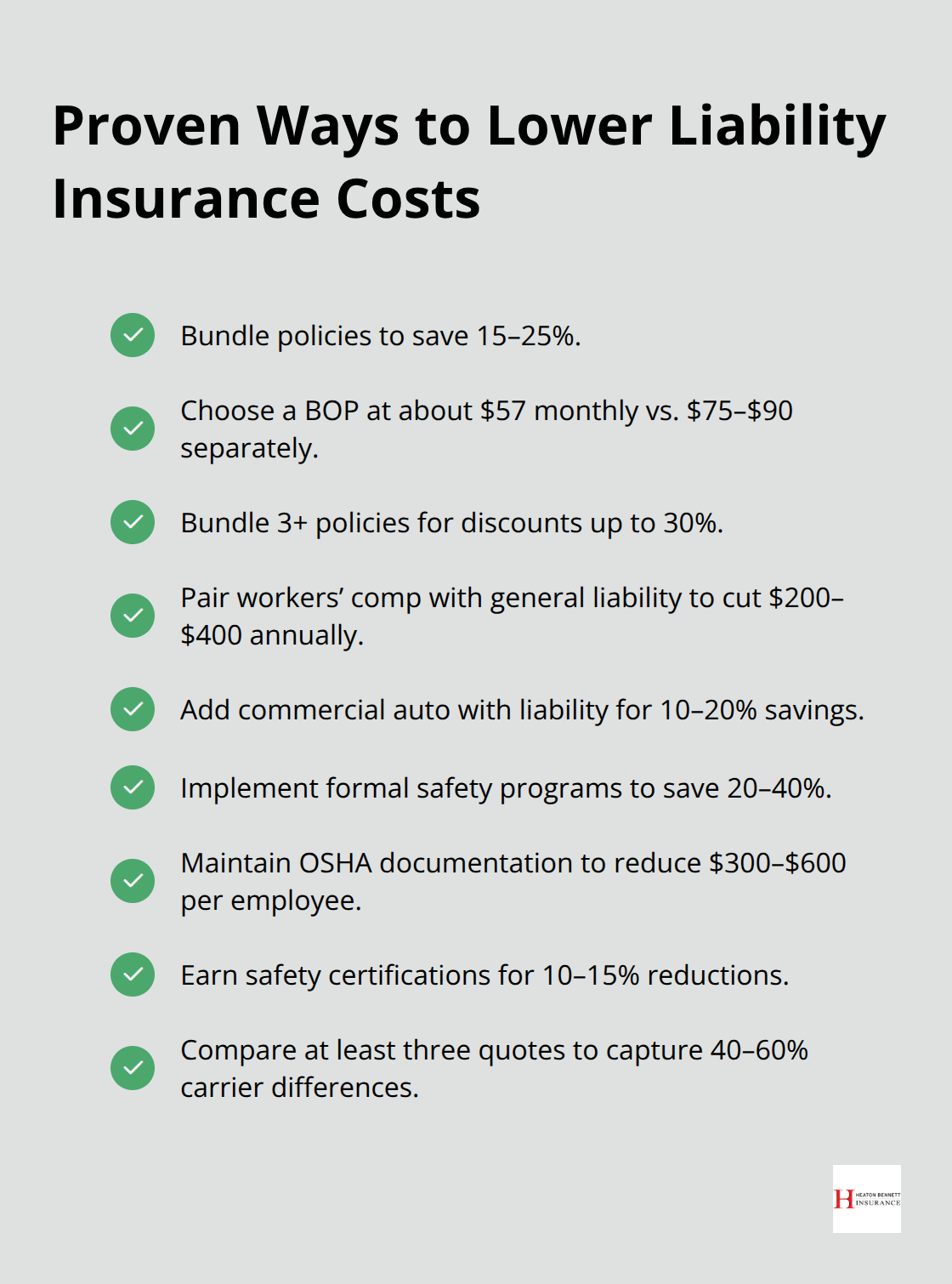

Business owners who combine multiple insurance types with one carrier see immediate cost reductions of 15-25%. A Business Owner’s Policy that bundles general liability with commercial property insurance costs $57 monthly on average, compared to separate purchases at $75-90 monthly. Progressive Insurance data shows that businesses that combine three or more policies receive discounts up to 30%.

Workers compensation paired with general liability typically reduces total premiums by $200-400 annually. Commercial auto insurance bundled with liability coverage delivers additional savings of 10-20% according to The Hartford’s structure. These combinations create substantial cost advantages while simplifying your insurance management process.

Document Safety Programs for Premium Reductions

Companies with formal safety programs pay 20-40% less for liability coverage than businesses without risk management protocols. OSHA compliance documentation reduces workers compensation premiums by an average of $300-600 annually per employee. Security systems, employee training programs, and incident logs demonstrate proactive risk management to insurers.

Businesses that complete safety certifications through industry associations see premium reductions of 10-15%. Regular safety audits and documented maintenance schedules for equipment further reduce rates. The National Association of Insurance Commissioners confirms that insurers reward businesses that actively minimize their risk exposure through measurable safety initiatives.

Compare Carriers for Best Rates

Premium variations between carriers for identical coverage reach 40-60% according to Insureon’s market analysis. Three quotes minimum should be your standard practice (some businesses see cost differences exceeding $1,000 annually between highest and lowest bids). Independent agents access multiple carriers simultaneously, which streamlines this comparison process while providing expertise on coverage nuances.

Established businesses with clean claims histories have the strongest position and should leverage this advantage when they request quotes. Annual policy reviews become essential since carrier strategies shift regularly, and your current provider may no longer offer the most competitive rates for your risk profile.

Final Thoughts

Small business owners who ask “how much does liability insurance cost for a small business” must consider multiple factors that directly impact premiums. Business size, industry risk level, coverage limits, and location create the foundation for insurance costs, with annual premiums that range from $400 to $3,000. The data reveals clear patterns: construction companies pay significantly more than accounting firms, businesses with multiple employees face higher costs than single-employee operations, and urban locations command premium increases of 25-40% over rural areas.

Proper liability coverage protects business assets and future income from potentially devastating lawsuits. The modest cost of adequate insurance coverage becomes insignificant when compared to the financial destruction that one uninsured claim could cause. Smart business owners recognize this protection as an investment rather than an expense (particularly when considering the average claim costs in their industry).

We at Heaton Bennett Insurance recommend that business owners obtain quotes from multiple carriers to find competitive rates for their specific situation. Our team provides access to numerous insurance companies, which allows us to compare coverage options and pricing structures that match business needs. Contact Heaton Bennett Insurance to start your coverage evaluation and secure the protection your business requires.