How Much Does Small Business General Liability Insurance Cost?

Small business general liability insurance cost varies dramatically depending on your industry, location, and coverage choices. At Heaton Bennett Insurance, we’ve seen premiums range from under $500 annually for low-risk service businesses to several thousand dollars for contractors and manufacturers.

Understanding what drives these costs helps you make smarter decisions about your coverage and budget.

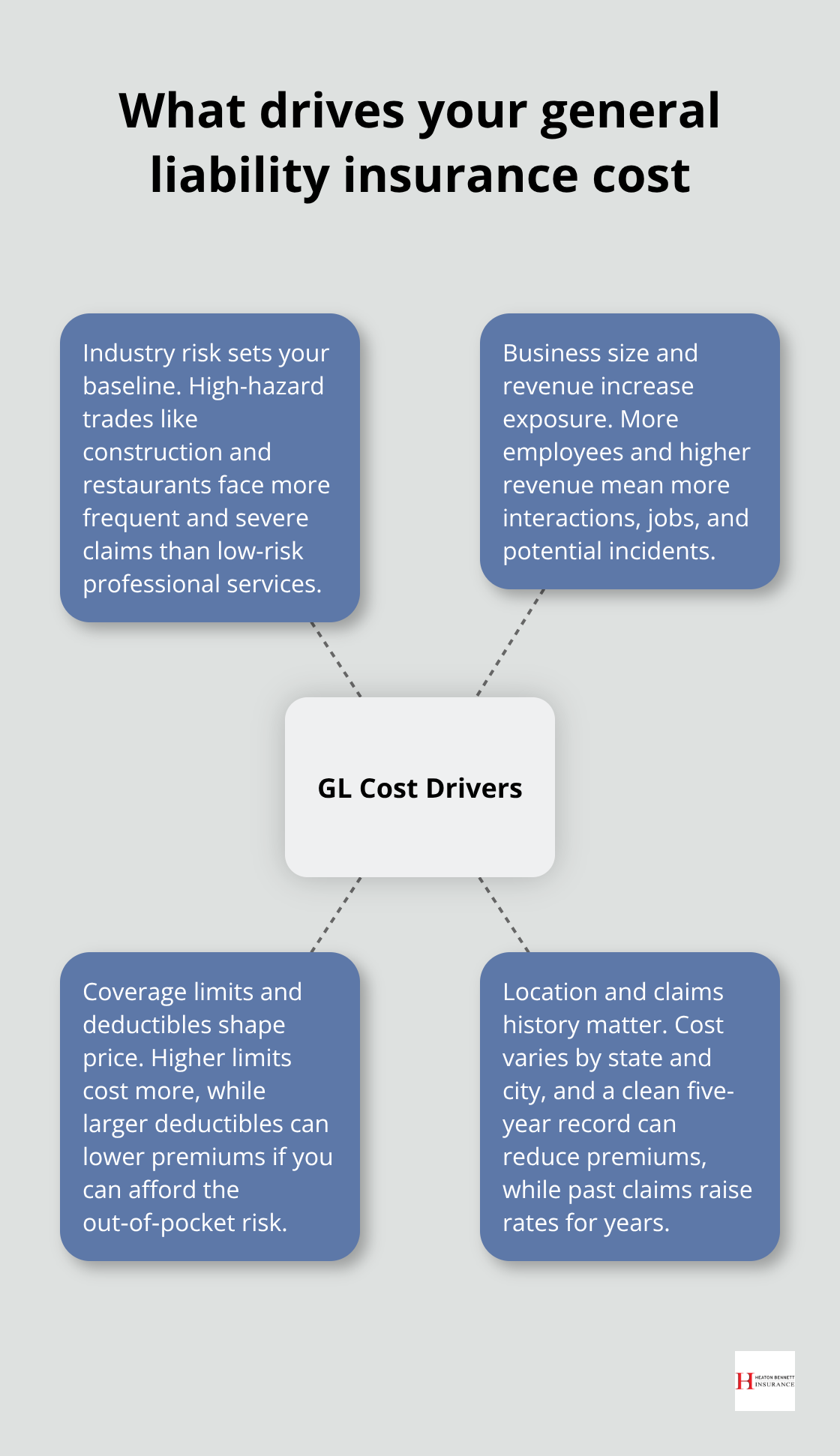

What Actually Drives Your General Liability Insurance Cost

Industry type creates the biggest price gap

Your industry type creates the biggest price difference in general liability premiums. Construction businesses pay roughly $108 per month on average, while accountants pay around $25 per month according to Next Insurance data. This gap exists because construction work exposes you to serious injury and property damage claims constantly. A painter working at heights faces different risks than a consultant working from an office. Electricians average $63 monthly, landscapers $50 monthly, and restaurants $108 monthly. The Hartford’s data shows restaurants paying approximately $2,408 annually while accounting firms pay around $675 per year.

Business size and revenue shape your premium

Your business size and revenue directly affect premiums because larger operations create more exposure to potential claims. A one-person consulting firm with $50,000 in annual revenue pays substantially less than a 15-person construction company with $1.2 million in revenue. Insureon’s analysis of 40,000 small business customers shows 53 percent operate with less than $100,000 in annual revenue, and these smaller operations typically secure lower premiums. Each additional employee increases your premium across all policy types because more staff means more client interactions and higher accident potential.

Coverage limits and deductibles set your baseline cost

The standard $1 million per occurrence and $2 million aggregate structure costs roughly $42 to $59 monthly nationally based on Insureon and Progressive data. Doubling your limits to $2 million per occurrence and $4 million aggregate adds approximately $5 to $20 monthly depending on your industry and location. Choosing a $500 deductible versus $1,000 cuts your premium by roughly 10 to 15 percent, though you must actually afford that deductible when a claim happens.

Location and claims history round out the picture

Location influences your costs through state-specific medical expenses, litigation costs, and crime rates. Colorado businesses average $49 to $52 monthly while Indiana averages $43 monthly. Dense urban areas and disaster-prone regions push premiums higher than rural locations. Your claims history matters for years afterward-past claims increase rates for 3 to 5 years, while maintaining zero claims for five years can reduce your premium by roughly 12 percent according to industry benchmarks. Understanding these four factors positions you to evaluate quotes accurately and identify where you can control costs most effectively.

What You’ll Actually Pay by Industry and Location

Industry type creates massive cost differences

General liability premiums swing wildly depending on what you do for work. Insureon’s analysis of 40,000 small business customers reveals accountants pay around $25 monthly while general contractors hit $108 monthly-a four-fold difference driven purely by industry risk. Next Insurance data confirms this pattern, showing electricians at $63 monthly, landscapers at $50 monthly, and restaurants at $108 monthly. The Hartford’s annual benchmarks paint the same picture: restaurants average $2,408 yearly, retail stores $696, and accounting firms $675. These aren’t theoretical ranges-they represent actual median costs paid by real businesses. Your specific premium within these ranges depends on your exact location and how you structure your coverage limits and deductibles.

Geography pushes your costs up or down

Location matters far more than most business owners realize. Colorado businesses average $49 to $52 monthly while Indiana averages $43 monthly, reflecting different state medical costs and litigation environments. Virginia sits around $36 monthly while California reaches $42 monthly according to state-level data. Dense urban areas consistently cost more than rural locations because higher population density means more foot traffic, more potential claims, and steeper medical costs when injuries occur. A restaurant in downtown Austin faces different pricing than one in a small Hill Country town.

Payment timing affects your annual expense

The annual payment versus monthly payment decision directly impacts your bottom line. Paying your full premium upfront typically saves 10 to 15 percent compared to monthly installments. If your annual premium runs $804, paying monthly costs around $67 to $70 monthly, but paying annually costs roughly $67 monthly on average. That difference compounds across years. Most small businesses find that committing to annual payment forces better budgeting discipline anyway.

Now that you understand what drives your costs and what you’ll actually pay, the real opportunity lies in identifying which cost-reduction strategies work best for your specific situation.

How to Cut Your General Liability Insurance Costs

Bundle policies to capture immediate savings

Combining your general liability policy with other coverage types delivers the most immediate savings. A Business Owner’s Policy that merges general liability with commercial property insurance costs around $57 monthly according to Insureon’s data from 40,000 customers, compared to purchasing those policies separately. That bundling discount ranges from 10 to 15 percent in most cases, and some insurers offer even steeper reductions when you add three or more policies together. If you also carry workers’ compensation, commercial auto, or cyber insurance, consolidating everything with one carrier often produces additional discounts that stack on top of your bundled rate. Request bundle quotes specifically rather than accepting individual policy quotes. Many business owners leave thousands of dollars on the table simply because they never asked about multi-policy discounts.

Invest in safety programs to reduce your premium

Documented risk management practices directly reduce your premium because insurers reward businesses that prevent claims from happening. OSHA-compliant safety protocols, employee training programs, and documented procedures signal to insurers that you take risk seriously. A construction company with a formal safety program and zero claims for five years can achieve roughly a 12 percent premium reduction compared to similar businesses without that track record. The Hartford and other carriers specifically mention that robust risk management practices qualify you for better rates. This means investing in safety equipment, spill cleanup protocols, security systems, and employee training isn’t just smart business-it’s profitable insurance strategy. Document everything you do. When you renew your policy, provide your insurer with evidence of your safety investments and clean claims history. Carriers want to see concrete proof that you’ve reduced your exposure.

Review your coverage annually to eliminate waste

Your needs change as your business grows, yet most business owners set their coverage limits once and forget about them. Reviewing your policy annually against your current revenue, employee count, and client contracts prevents you from paying for excessive coverage you don’t need or carrying insufficient limits that expose you to personal liability. If your revenue doubled since last year, your exposure increased and you might need higher limits. Conversely, if you’ve shifted your business model or reduced your customer-facing operations, you might qualify for lower premiums. This review takes roughly an hour and can identify $200 to $500 in annual savings through adjusting your deductible, eliminating unnecessary endorsements, or removing coverage riders that no longer apply to your operations.

Final Thoughts

Your small business general liability insurance cost ultimately reflects four primary factors: your industry type, business size, coverage limits, and location. Construction and restaurant businesses pay roughly $108 monthly while accountants pay around $25 monthly, reflecting the dramatic risk differences across industries. Most small businesses operate with $1 million per occurrence and $2 million aggregate limits, paying between $42 and $59 monthly nationally.

Reducing your costs requires action on three fronts. First, bundle your general liability policy with commercial property, workers’ compensation, or other coverage types to capture 10 to 15 percent savings immediately. Second, invest in documented safety programs and employee training because insurers reward businesses that prevent claims from happening-a clean five-year claims history can reduce your premium by roughly 12 percent. Third, review your coverage annually to eliminate unnecessary endorsements and adjust your deductible based on what you can actually afford in a claim.

A business owner who bundles policies, maintains a safety program, and pays annually can reduce their total insurance costs by 25 to 30 percent compared to someone purchasing individual policies with minimal risk controls. Getting a personalized quote takes roughly 15 minutes and reveals exactly what your specific situation costs. Heaton Bennett Insurance works with multiple carriers to compare rates and find coverage that matches your actual risk profile and budget.