How Much Does Vacant Property Insurance Cost?

Vacant property insurance costs vary wildly depending on where your building sits and what shape it’s in. We at Heaton Bennett Insurance see premiums swing from a few hundred dollars annually to several thousand, and the difference often comes down to factors you can actually control.

This guide breaks down the real numbers behind vacant property insurance pricing and shows you concrete ways to reduce what you’re paying.

What Really Drives Up Your Vacant Property Insurance Costs

The price you pay for vacant property insurance reflects factors that insurers view as direct risk indicators. Your property’s condition matters enormously-a well-maintained home with updated electrical systems, a solid roof, and functioning plumbing costs far less to insure than an older structure showing signs of neglect. Insurers know that deteriorating properties attract more theft and suffer faster damage from undetected leaks or pest intrusion.

How Property Age and Condition Shape Your Premium

A 50-year-old house with outdated wiring will command significantly higher premiums than a 15-year-old home in comparable condition. Older homes consistently cost more to insure as vacant properties because they present genuine risk. An 80-year-old house with knob-and-tube wiring or galvanized plumbing poses fire and water damage threats that newer construction avoids. Insurers price these risks accordingly.

Properties showing visible deterioration-missing shingles, boarded windows, overgrown yards-signal to underwriters that maintenance has been neglected, making damage detection harder. A well-kept property with maintained landscaping, functioning systems, and regular inspections costs 20% to 30% less to insure than a neglected one.

Location’s Direct Impact on Your Rate

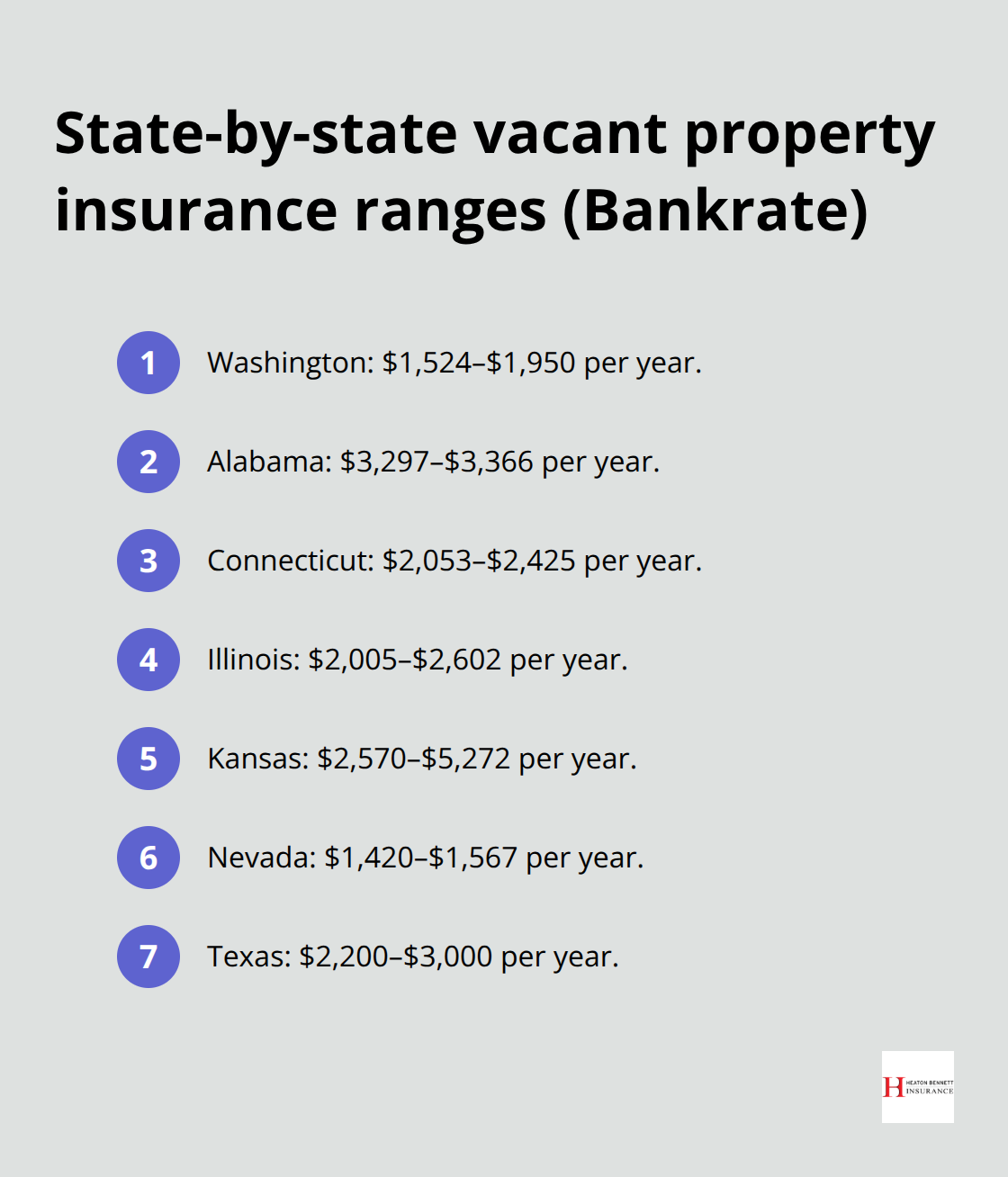

Geographic location functions as a primary cost driver. Washington state residents pay roughly $1,524 to $1,950 annually for vacant coverage, while Alabama residents face $3,297 to $3,366, according to Bankrate. These differences reflect local crime rates, building code standards, and disaster frequency.

Safe neighborhoods with strong police presence and lower theft statistics enjoy lower premiums. High-crime areas automatically cost more because the risk is statistically higher. Properties in high-crime neighborhoods face theft and vandalism rates that push premiums up by 30% to 40% compared to safe areas. Coastal regions and areas prone to wildfires add their own surcharges due to natural disaster exposure.

Your Coverage Choices Control Remaining Costs

Selecting appropriate coverage limits prevents you from overpaying for protection you don’t need. A modest home doesn’t require the same dwelling coverage limit as a luxury property. Choosing a $1,000 deductible instead of $250 can reduce your annual premium by 15% to 25%. This strategy works if you have emergency funds available to cover the deductible after a loss.

Your coverage choices directly impact what you’ll pay each month. Choosing a higher deductible-say $2,500 instead of $500-lowers your annual premium noticeably, though it means you absorb more cost if damage occurs. Coverage limits matter too; insuring a $400,000 structure costs substantially more than protecting a $200,000 property, which is simply mathematical reality based on potential loss exposure.

Understanding these three pillars-property condition, location, and coverage selections-positions you to make informed decisions about your vacant property protection. The next section reveals specific strategies that reduce what you actually pay while maintaining the coverage your property needs.

What Vacant Property Insurance Actually Costs Across America

Vacant property insurance premiums shift dramatically across state lines, and understanding regional pricing helps you anticipate what you’ll actually pay. According to Bankrate, Washington state residents spend $1,524 to $1,950 annually for vacant coverage, while Alabama residents face $3,297 to $3,366-more than double in some cases. Connecticut runs $2,053 to $2,425, Illinois ranges from $2,005 to $2,602, Kansas spans $2,570 to $5,272, and Nevada costs $1,420 to $1,567. These numbers reflect each state’s specific risk profile, from hurricane exposure in coastal regions to theft rates in urban areas.

Texas Pricing in the National Context

Texas property owners typically pay $2,200 to $3,000 annually for vacant coverage, positioning the state roughly in the middle of the national spectrum. This pricing makes Texas more affordable than northeastern states but pricier than western alternatives. If you own property across multiple states, these variations significantly impact your total insurance budget.

How Building Age Drives Premium Increases

A property’s age determines premium increases more reliably than almost any other factor. A 20-year-old vacant home costs substantially less to insure than a 70-year-old structure with the same square footage in the same neighborhood. Insurers charge more for older buildings because electrical fires, plumbing failures, and structural deterioration present genuine hazards that newer construction avoids.

An 80-year-old house with original wiring might cost 40% to 50% more annually than a 2005-built home, according to underwriting standards across major carriers. This age premium applies regardless of condition-even a meticulously maintained older property faces higher rates because the underlying systems themselves carry greater risk. Every decade beyond 50 years typically adds 8% to 12% to your annual premium.

The Financial Case for Property Updates

Property renovation before vacancy makes financial sense. Updating electrical systems, plumbing, or roofing can reduce your insurance costs by 15% to 25% and often pays for itself within three to five years through premium savings alone. These improvements lower your risk profile in the eyes of underwriters, directly translating to lower rates.

The cost differences between states and the impact of building age create a clear picture: your location and property condition control most of what you’ll pay. The next section reveals specific actions you can take right now to reduce these costs without sacrificing the protection your vacant property needs.

How to Cut Your Vacant Property Insurance Costs

Install Security Systems That Reduce Theft Risk

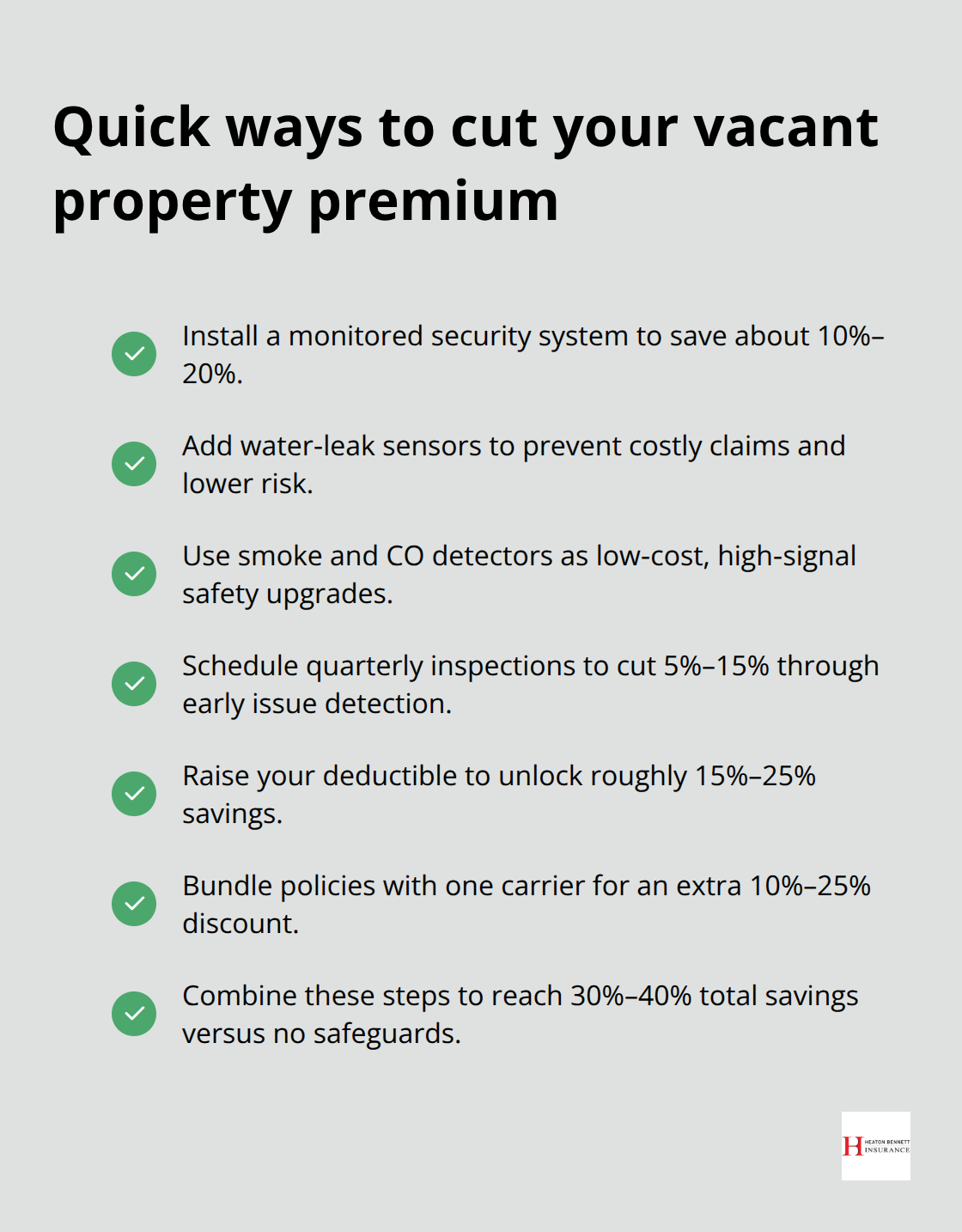

Security systems deliver measurable premium reductions that justify their upfront cost within months. Motion-sensor lights, burglar alarms, and security cameras signal to insurers that your property faces lower theft and vandalism risk, typically reducing premiums by 10% to 20% according to underwriting guidelines across major carriers. A $500 security system installation pays for itself in three to four months if it cuts your annual premium from $3,000 to $2,550. Water leak detection systems carry similar weight with underwriters because they catch pipe failures before they cause thousands in damage-a $200 sensor can prevent $15,000 in water damage claims. Smoke and carbon monoxide detectors cost under $100 combined but signal property awareness to insurers, making them an easy win. The most effective approach combines visible deterrents like alarm company signs with actual functioning systems; fake signs fool thieves but not insurance underwriters who verify system installation during the underwriting process.

Maintain Your Property to Lower Risk Signals

Property maintenance directly correlates with lower premiums because neglect signals higher risk. Mowing the lawn, cleaning gutters, and keeping the yard maintained makes the property appear occupied, which deters theft and vandalism. Arranging quarterly inspections by a neighbor or property manager costs $50 to $150 per visit but reduces your premium by 5% to 15% because regular monitoring catches problems early-a small roof leak discovered in week two costs far less than one discovered in month six. Setting thermostats to 55°F prevents frozen pipes during winter vacancy, eliminating a major damage source that drives premium increases.

Bundle Policies to Access Hidden Discounts

Bundling your vacant property policy with auto, homeowners, or business insurance through the same carrier typically yields 10% to 25% discounts on your total premium, making it worth shopping for carriers that write multiple lines of coverage. Independent agencies specializing in assembling coverage across multiple carriers mean you access discounts that single-company policies cannot match. The combination of security investments, regular maintenance checks, and multi-policy bundling can reduce your total annual cost by 30% to 40% compared to an unprotected property with no bundling strategy.

Final Thoughts

Your vacant property insurance cost ultimately reflects three controllable factors: property condition, location, and your coverage selections. A well-maintained property with security systems in a safe neighborhood costs substantially less to insure than a neglected building in a high-crime area, and building age adds another layer since older structures command higher premiums regardless of condition. The financial gap between states is real and significant, with Alabama residents paying double what Nevada residents pay for comparable coverage.

The strategies that reduce your premiums work because they address what insurers actually fear: theft, vandalism, undetected damage, and liability exposure. Installing motion sensors and burglar alarms cuts premiums by 10% to 20%, while arranging quarterly property inspections and maintaining your yard reduces costs by another 5% to 15%. Bundling your vacant property policy with auto or homeowners coverage through the same carrier yields 10% to 25% additional savings, and combined, these actions can lower your total annual cost by 30% to 40%.

Getting an accurate quote requires contacting multiple carriers and comparing the same coverage limits and deductibles across each quote. Your current homeowners insurer may offer a vacant property endorsement that qualifies for bundling discounts, making it worth checking before shopping elsewhere, and contact us at Heaton Bennett Insurance to discuss your vacant property insurance needs and receive a personalized quote that reflects your property’s actual risk profile.