How Much Does Tiny Home Insurance Cost?

Tiny home insurance cost varies dramatically based on your location, construction materials, and coverage choices. Most owners pay between $600 to $1,200 annually, but rates can swing much higher in disaster-prone areas.

We at Heaton Bennett Insurance see significant price differences between mobile and foundation-based tiny homes. Understanding these cost factors helps you budget effectively and find the right protection for your investment.

What Drives Tiny Home Insurance Costs

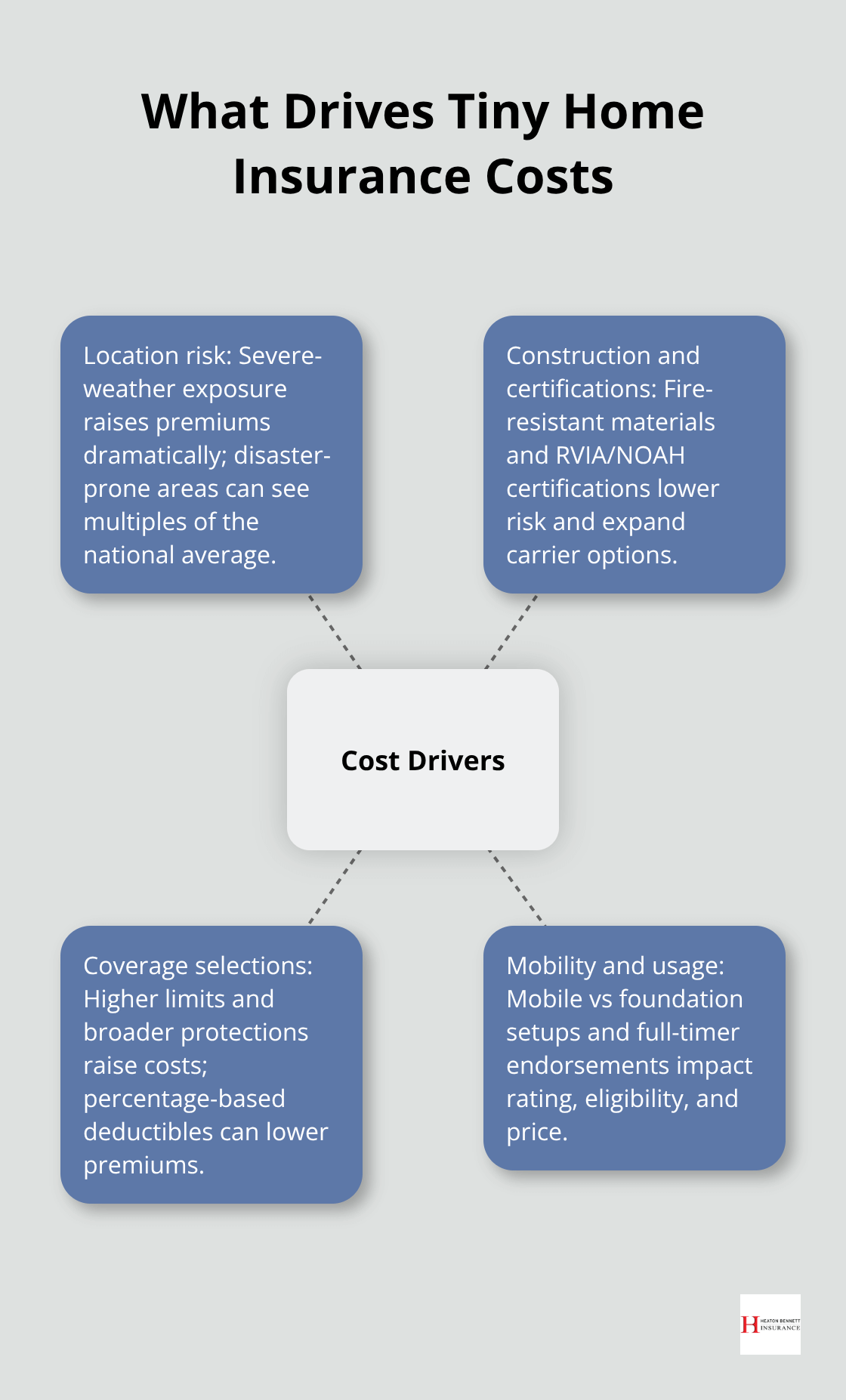

Your geographic location stands as the single biggest factor that determines tiny home insurance premiums. Oklahoma leads the nation at $1,974 annually according to recent industry data, while states like Kansas see rates around $1,521. The National Association of Insurance Commissioners reports that areas prone to tornadoes, hurricanes, and wildfires push premiums 200% above national averages. Clients in Austin pay significantly less than those in coastal hurricane zones or tornado alley regions.

Construction Standards Control Your Rates

Insurance companies examine building materials and construction quality closely when they set rates. RVIA-certified tiny homes typically qualify for standard RV insurance policies with lower premiums, while DIY builds often require specialty coverage at higher costs. Homes built with fire-resistant materials like metal roofing and fiber cement siding receive better rates than those with standard wood construction. Companies like Foremost require NOAH or RVIA certification before they offer coverage (making professional construction a smart financial choice).

Coverage Choices Control Your Premium

Your policy limits and coverage types directly control your annual costs. Basic liability coverage starts around $400 annually, while comprehensive protection that includes personal property and additional living expenses can reach $1,500. Percentage-based deductibles instead of fixed $500 amounts can reduce premiums by up to 19% in some states according to recent market analysis. Full-timer policies for mobile tiny homes cost more than seasonal coverage, but they provide year-round protection that standard RV policies exclude.

Mobile vs Foundation Homes Create Price Gaps

Mobile tiny homes on wheels face different rate structures than foundation-based units. RV insurance for mobile units typically costs less initially but require full-timer endorsements for permanent residence (which increases premiums substantially). Foundation-based tiny homes often need specialty homeowners policies that cost more upfront but provide broader coverage. The mobility factor alone can create a 30-40% difference in annual premiums between these two categories.

These cost factors work together to create your final premium, but smart choices in each area can lead to substantial savings when you explore your tiny home insurance coverage options.

Average Tiny Home Insurance Rates by State

Insurance rates for tiny homes vary wildly across the United States, with some states charging three times more than others. Oklahoma tops the cost charts at $1,974 annually, representing a staggering 242% above the national average according to industry data. Tennessee follows at $1,600 per year, while Kansas sits at $1,521 annually. States prone to natural disasters consistently show the highest premiums, with tornado-prone areas like Oklahoma and hurricane zones along the Gulf Coast pushing rates well above $1,500.

Weather Patterns Drive Regional Premium Differences

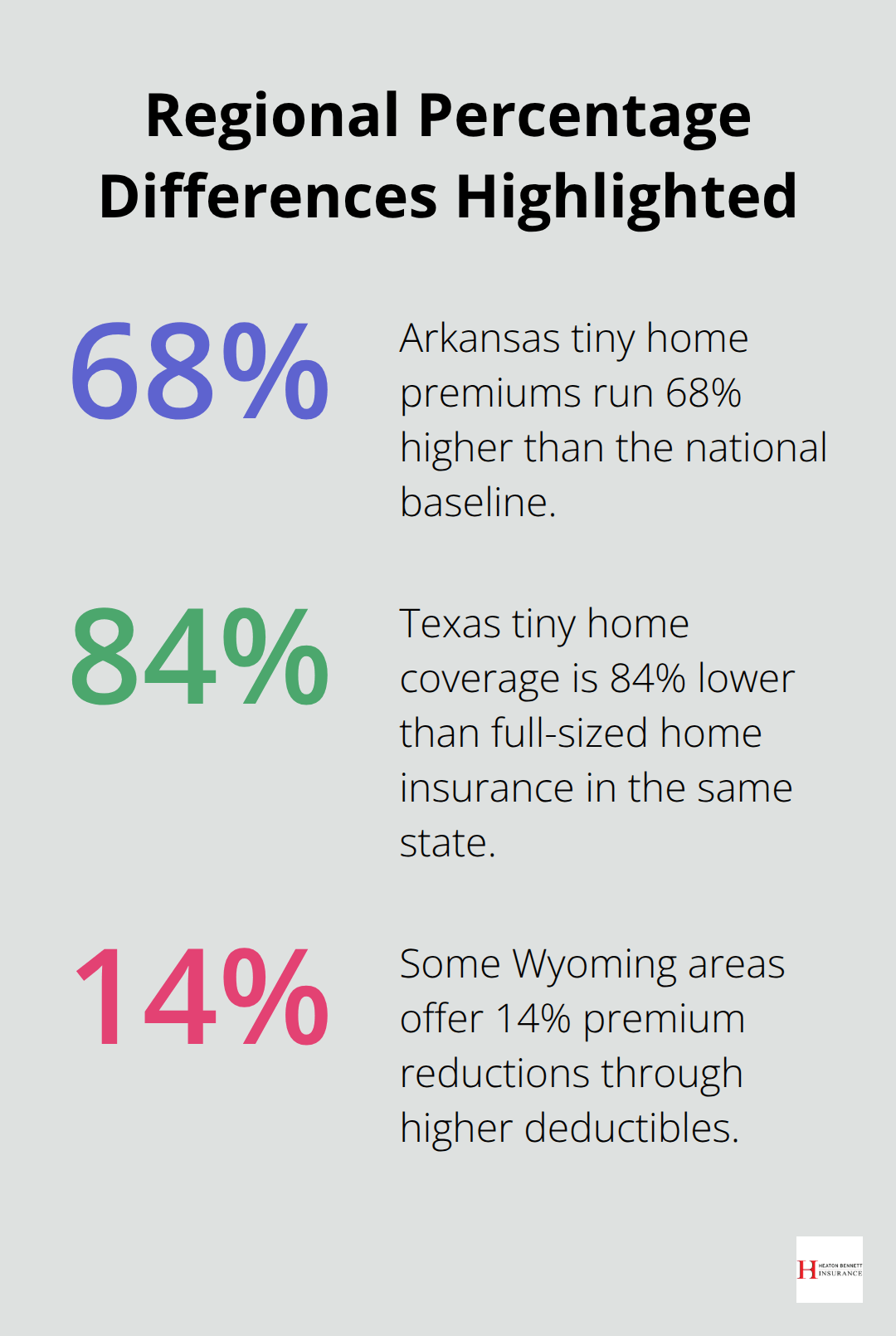

The National Association of Insurance Commissioners data shows that climate risks create the most dramatic price swings between states. Arkansas averages $1,177 annually but runs 68% higher than the national baseline due to severe weather exposure. Texas averages $1,387 for tiny home coverage, still 84% lower than full-sized home insurance in the same state. States with mild weather patterns like Wyoming offer significant discounts, with some areas providing 14% premium reductions through higher deductible options (making location choice a major cost factor).

High-Risk vs Low-Risk Geographic Areas

Natural disaster frequency determines premium levels more than any other factor. States in tornado alley see rates spike 200% above national averages, while coastal hurricane zones face similar increases. Alabama and Arkansas both experience rates around 68% higher than the national average due to climatic risks. Conversely, states with stable weather patterns maintain lower baseline rates, with some regions offering substantial savings for tiny home owners who choose their location strategically.

Foundation vs Mobile Homes Show Different State Rates

Mobile tiny homes face different rate structures depending on state regulations and RV registration requirements. Foundation-based units in low-risk states like South Carolina average around $800 annually, while the same structure in Oklahoma could cost $2,200. Mobile units registered as RVs typically start lower but require full-timer endorsements that can double premiums in high-risk states (particularly in disaster-prone regions). Some states mandate DMV registration for tiny homes on wheels, which affects both coverage options and final costs.

These state-by-state variations highlight why location research proves essential before you commit to a tiny home purchase, but several proven strategies can help reduce these premiums regardless of where you live. Policy holders who bundle auto insurance with homeowners coverage typically save 10-25% on combined premiums.

How Can You Cut Your Tiny Home Insurance Costs

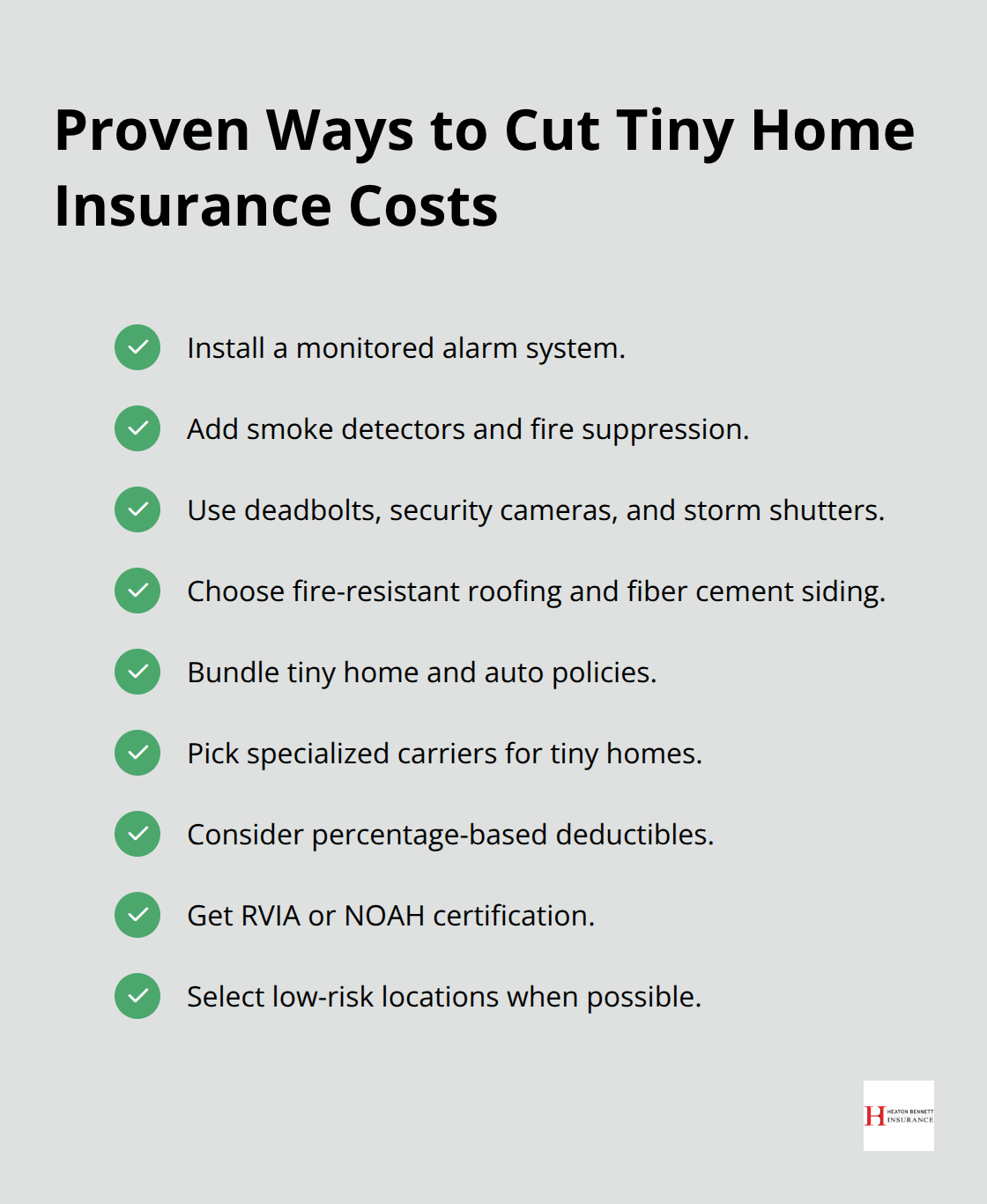

Smart security upgrades deliver immediate premium reductions that pay for themselves within two years. Monitored alarm systems typically reduce rates by 15-20%, while smoke detectors and fire suppression systems can cut premiums by another 10%. Progressive and American Family both offer substantial discounts for homes with deadbolt locks, security cameras, and storm shutters. Professional installation of fire-resistant materials like metal roofing and fiber cement siding creates long-term savings that compound annually.

Companies reward proactive safety measures because they reduce claim frequency (which makes these investments profitable for both owners and insurers).

Bundle Your Policies for Maximum Savings

Tiny home insurance combined with auto coverage through the same carrier generates automatic discounts of 10-25% according to industry standards. Clients save hundreds annually when they consolidate multiple policies under one provider. RV insurance bundled with auto coverage produces even higher discounts for mobile tiny homes, particularly with carriers like Farmers and American Family. Multi-policy discounts stack with safety feature reductions, which creates compound savings that can reduce total premiums by 35-40%. The key lies in choosing carriers that specialize in both coverage types rather than forcing incompatible policies together.

Choose Specialized Providers Over Generic Companies

Specialty insurers like Foremost and Strategic Insurance Agency understand tiny home risks better than traditional carriers, which leads to more accurate pricing and better coverage. These specialized providers offer percentage-based deductibles that save up to 19% annually compared to fixed $500 amounts. American Modern provides vacation home policies specifically designed for seasonal tiny homes, while companies like Insure My Tiny Home focus exclusively on this market segment. Generic insurance companies often misclassify tiny homes (resulting in coverage gaps and higher premiums). Independent insurance agencies who understand RVIA certification requirements and NOAH standards prevent costly mistakes that generic providers frequently make.

Final Thoughts

Tiny home insurance cost depends on three primary factors: your location, construction quality, and coverage choices. States like Oklahoma charge $1,974 annually while others like Kansas average $1,521. Weather risks drive these differences, with disaster-prone areas that see premiums 200% above national averages.

Smart buyers reduce costs through security upgrades that cut premiums by 15-20%, policy bundles for additional 10-25% savings, and specialized providers who understand tiny home risks. RVIA certification and professional construction materials create long-term savings that compound annually. Mobile homes require different coverage than foundation-based units, with RV policies that start lower but need full-timer endorsements for permanent residence (percentage-based deductibles save up to 19% compared to fixed amounts in many states).

We at Heaton Bennett Insurance help clients navigate these complex choices as an independent agency with access to multiple carriers. We find tailored insurance solutions that match your specific tiny home situation and budget requirements. Start with quotes from specialized providers, document your safety features, and consider your long-term plans when you choose between mobile and foundation coverage options.