Contractor Insurance Rates Texas: Budgeting for Risk

Contractor insurance rates in Texas vary wildly depending on your experience, the work you do, and your claims history. Getting this wrong means overpaying or worse-being underinsured when something goes wrong.

At Heaton Bennett Insurance, we help contractors understand exactly what drives their premiums and how to budget smartly. This guide walks you through the real factors that impact your costs and concrete ways to reduce them.

What Drives Your Contractor Insurance Costs in Texas

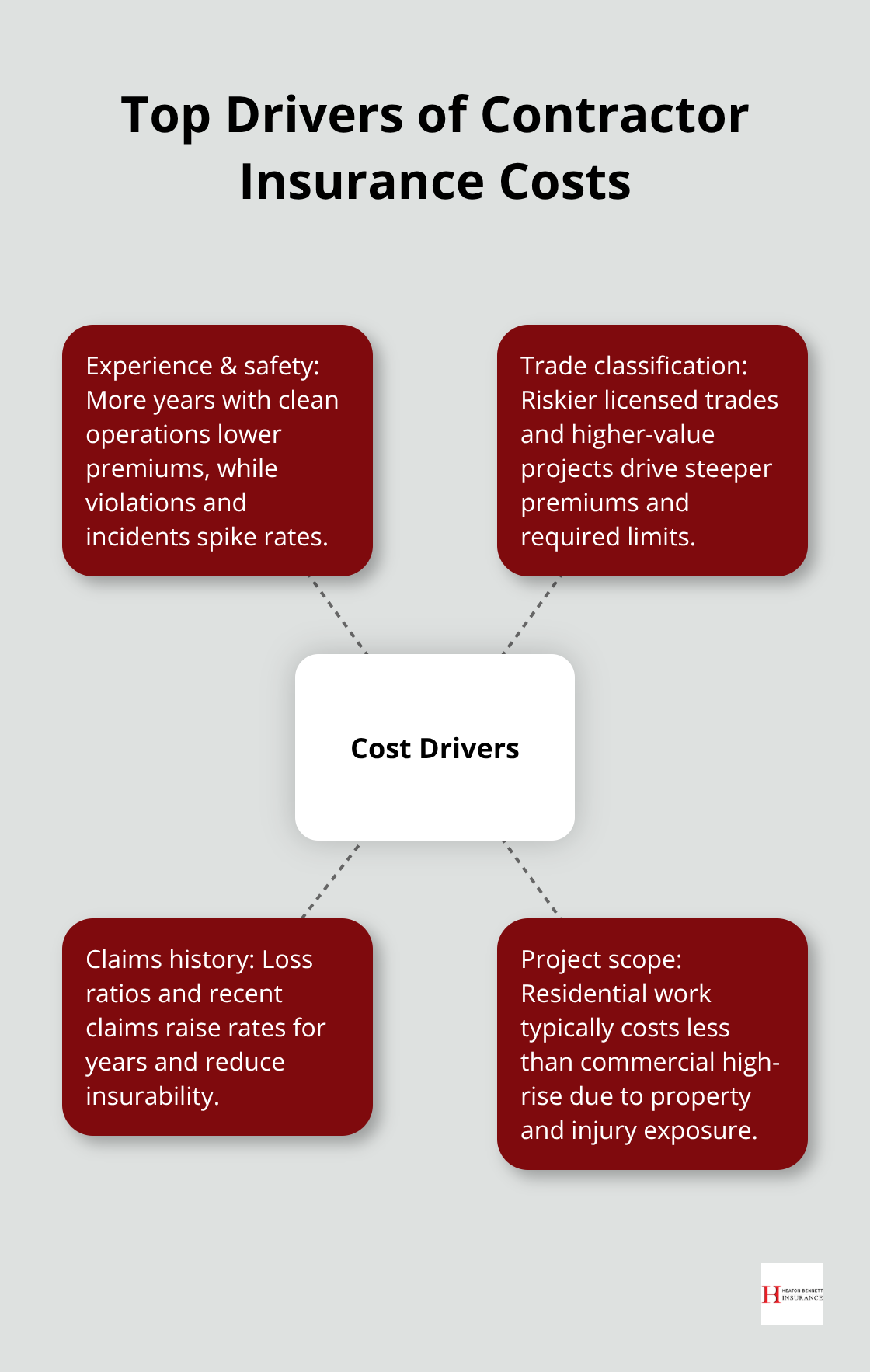

Experience and Safety Record Shape Your Premiums

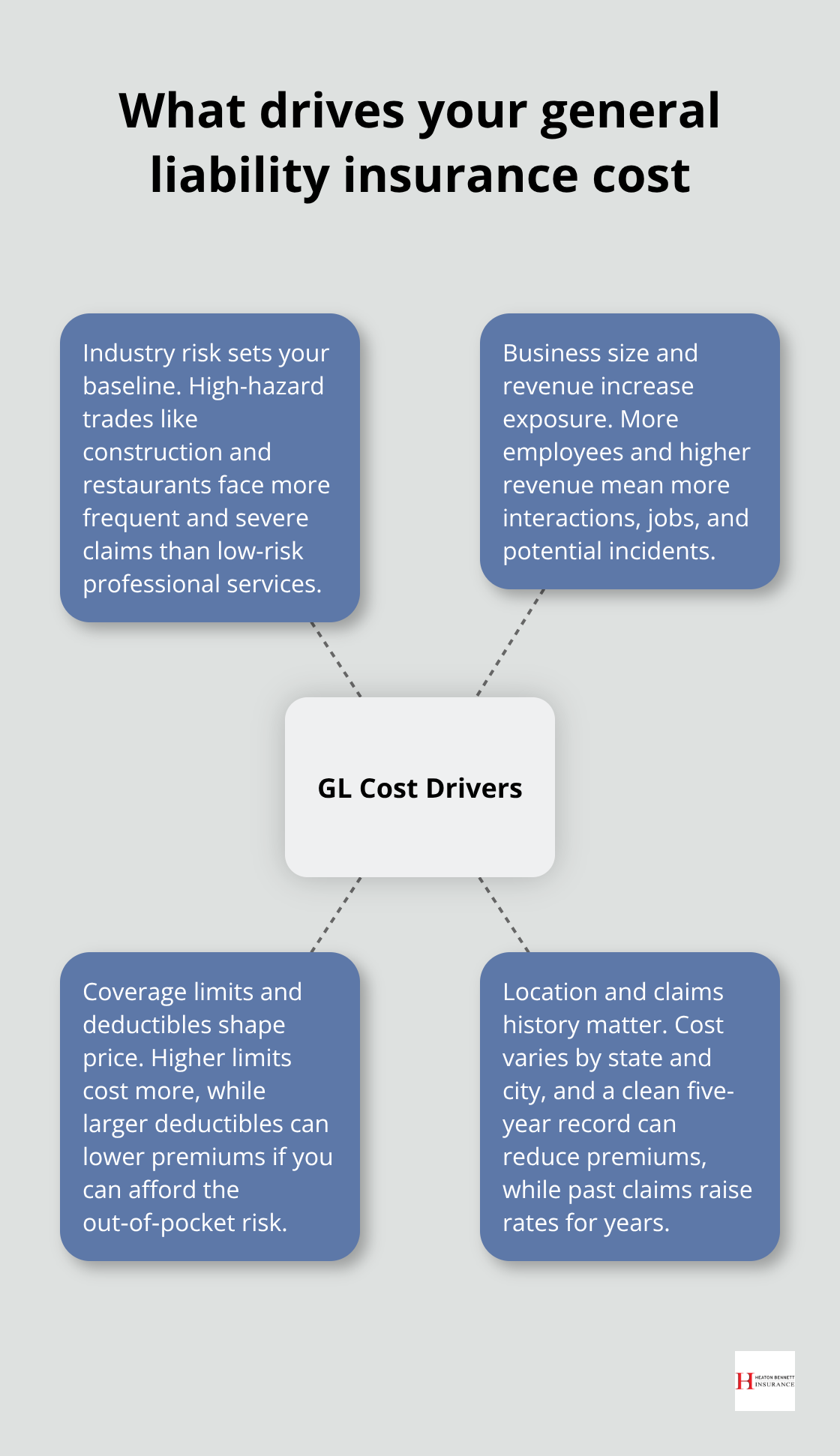

Your experience level and safety record are the first things insurers examine when pricing your policy. A contractor with 10+ years of clean operations pays significantly less than someone fresh to the trade. Insureon data shows that experience directly correlates with lower premiums because insurers see fewer claims from seasoned operators. If you’ve maintained zero incidents over five years, you’re in a strong negotiating position. Multiple claims or safety violations spike your rates dramatically. Texas contractors working in high-hazard trades like roofing, electrical, and HVAC face steeper premiums than general carpentry because injury risk is objectively higher. An electrician with a spotless safety record might pay around $3,020 annually for general liability coverage, while someone with claims on file could pay 40-60% more for the same limits.

Trade Classification Determines Your Risk Profile

Your specific trade classification determines which underwriting rules apply to you. Licensed trades in Texas fall under Texas Department of Licensing and Regulation oversight, which mandates minimum coverage limits. Electrical contractors must carry $300,000 per occurrence and $600,000 aggregate coverage, while HVAC Class A contractors need the same minimums but Class B requires only $100,000 per occurrence. Plumbing contractors need at least $300,000 in general liability. These aren’t suggestions-they’re legal requirements to maintain your license and perform work. Beyond statutory minimums, your actual premium depends on the scope of work you perform. A contractor handling only residential framing pays less than one performing commercial high-rise work because the property values and injury exposure differ substantially. Insureon data indicates estimated annual costs for a $1 million revenue contractor run about $30,706 for electricians, $36,170 for plumbers, and $30,800 for HVAC contractors when you bundle general liability, workers’ compensation, commercial auto, and inland marine coverage. These figures reflect the real cost structure across Texas and show why trade classification matters more than many contractors realize.

Claims History Predicts Your Future Rates

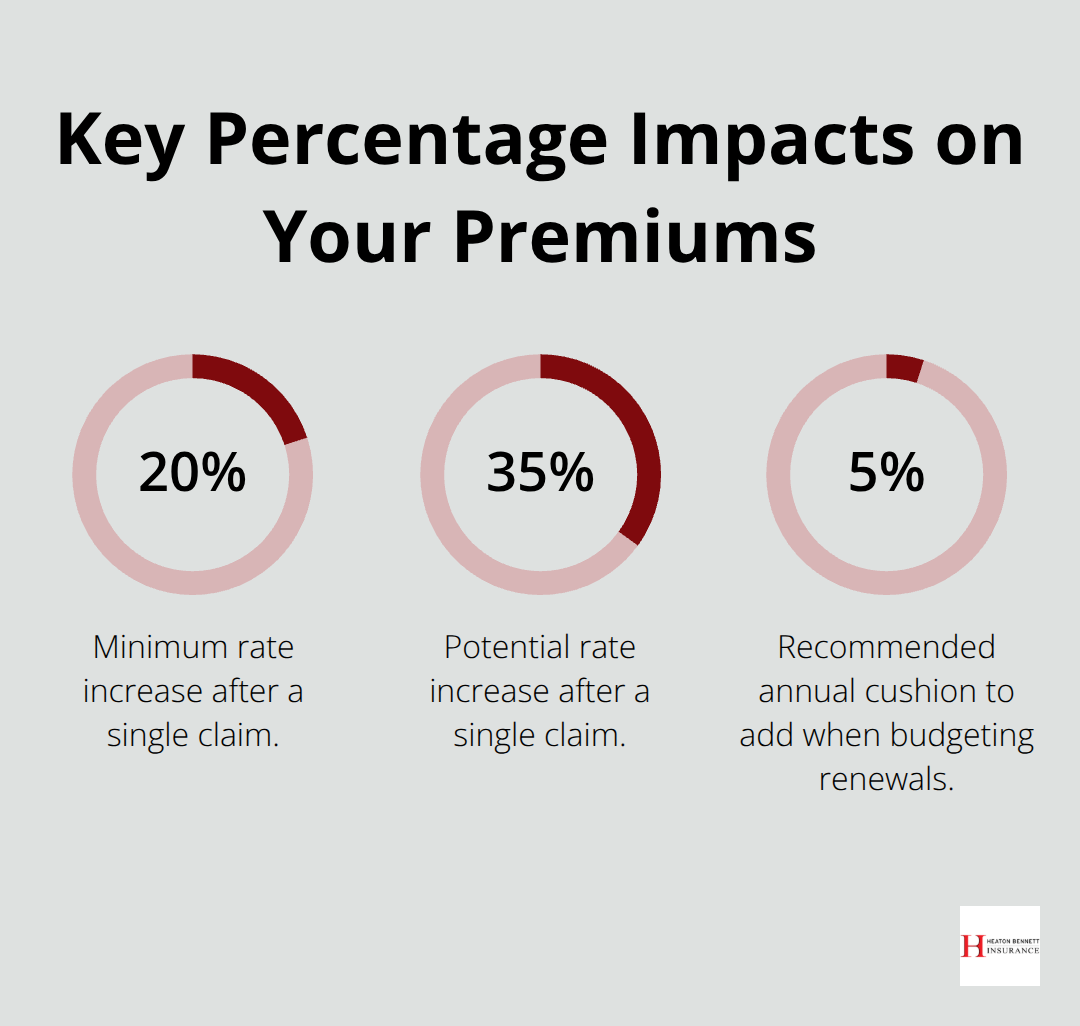

Your past claims history is the single strongest predictor of future premiums. One legitimate claim can increase your rates by 20-35% for the next three to five years. Two claims within five years makes you hard to insure at any reasonable rate. Insurers use loss ratios-the total amount you’ve claimed divided by premiums paid-to calculate your risk score. A contractor who’s claimed $15,000 over ten years while paying $60,000 in premiums has a 25% loss ratio, which is manageable. One who’s claimed $40,000 over the same period has a 67% loss ratio and looks like a liability to underwriters. The type of claim matters too. A property damage claim from a fire caused by faulty wiring looks worse than a minor slip-and-fall incident. Workers’ compensation claims carry particular weight because they signal workplace safety problems. If your business has filed multiple workers’ comp claims, underwriters assume your safety protocols are weak and price accordingly. Understanding these three factors-experience, trade classification, and claims history-puts you in control when you shop for coverage and negotiate rates with carriers.

How to Budget for Contractor Insurance in Texas

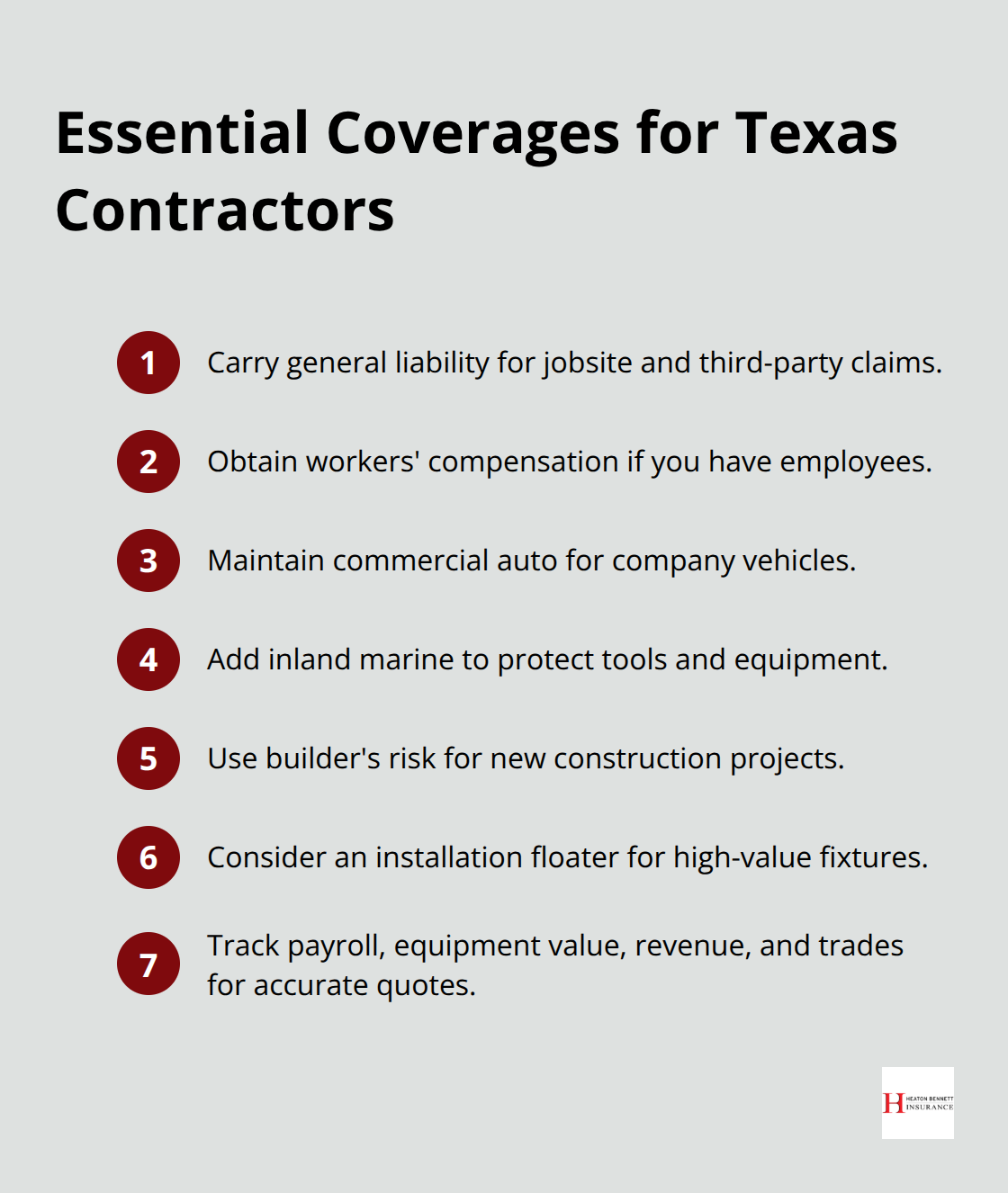

List Every Coverage Type You Actually Need

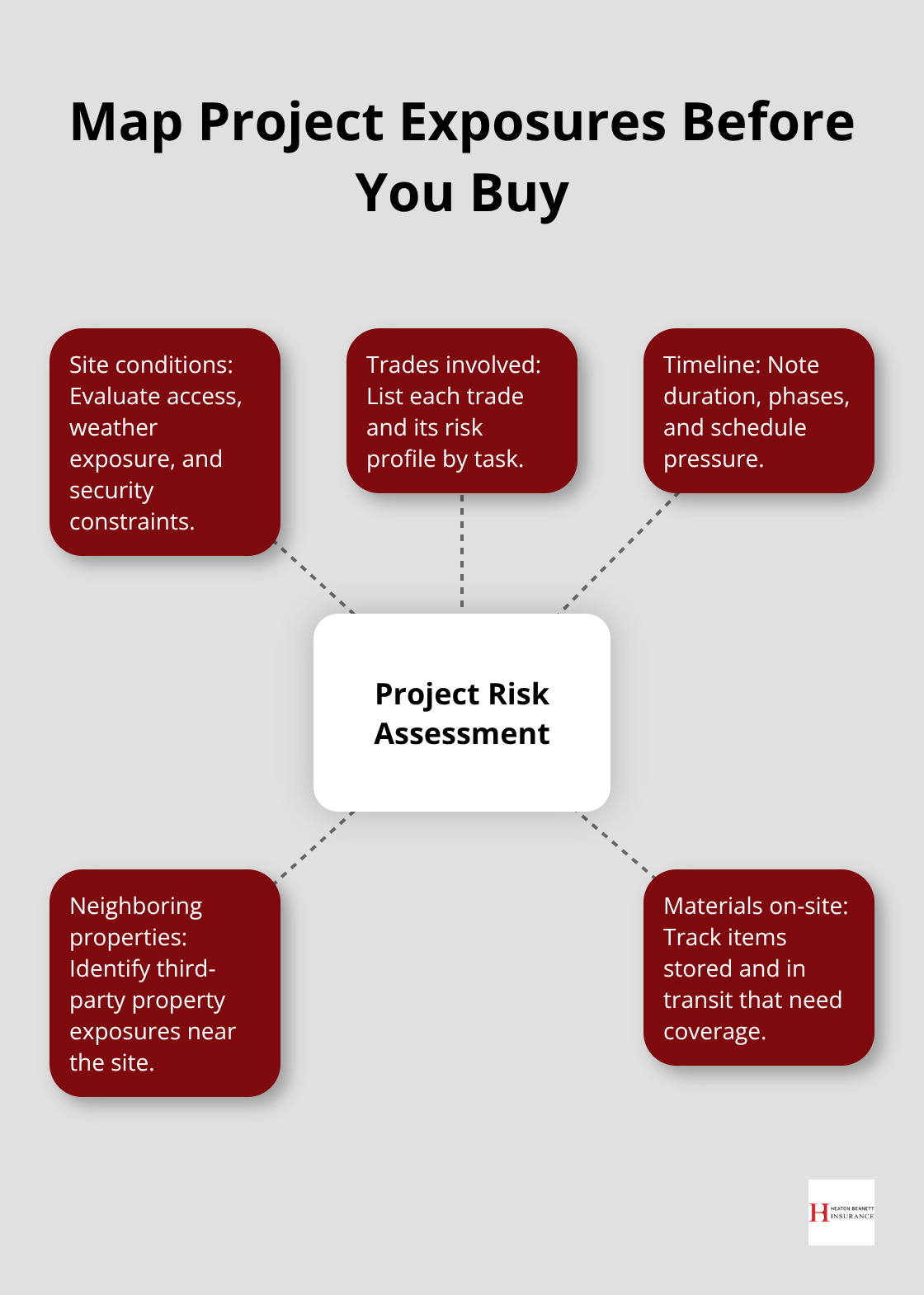

Start by listing every coverage type you actually need, not what you think sounds good. General liability is non-negotiable in Texas-most clients and permit offices require it before you step on a job site. Workers’ compensation is required if you have employees, and even if Texas law doesn’t mandate it for private employers, opting out exposes you to lawsuits that dwarf any premium savings. Commercial auto insurance is legally required for company vehicles.

Beyond these essentials, your budget depends on what you do. An electrician needs inland marine coverage for tools and equipment; a general contractor handling new builds needs builder’s risk insurance. A plumber installing high-value fixtures might need an installation floater. Write down your payroll, equipment value, annual revenue, and the specific trades you perform. Your insurance agent uses these numbers to calculate exposure.

Know Your Real Costs by Trade

According to Insureon data, a $1 million revenue electrician should budget roughly $30,706 annually across general liability ($3,020), workers’ compensation ($8,230), commercial auto ($18,256), and inland marine ($1,200). A plumber runs about $36,170, and an HVAC contractor about $30,800. These aren’t guesses-they’re median costs from actual Texas contractor data.

Underestimate your payroll or equipment value, and your policy won’t cover the full loss when something happens. Overstate it, and you pay for coverage you don’t need. Accuracy here determines whether your insurance actually protects you.

Compare Quotes from Multiple Carriers

General liability alone ranges from roughly $19 to $60 per month depending on your trade and history. That’s a significant difference over a year for the same coverage. Shop at least three carriers before committing. Many underwriters offer same-day quotes online-you answer questions about your business, crew size, and claims history, then compare.

When comparing quotes, check the details: per-occurrence limits, aggregate limits, deductibles, and exclusions. A low monthly quote with a $5,000 deductible and $300,000 per-occurrence limit looks cheap until you realize it won’t cover most commercial contracts requiring $1 million per occurrence.

Bundle Policies to Cut Costs

Bundling policies cuts costs significantly. A business owner’s policy combining general liability and commercial property averages about $121 per month according to Insureon, versus buying them separately. Add workers’ compensation and commercial auto to that bundle, and you lock in volume discounts that single-policy quotes won’t match.

Premiums typically rise 3–5% annually even with a clean claims record, simply because of inflation and increased payroll. If you budget today for next year, add at least 5% to your current premium estimate. This prevents sticker shock when your renewal notice arrives and helps you plan cash flow accurately.

Plan for Premium Growth and Contract Requirements

Your contract obligations often dictate coverage limits that exceed statutory minimums. A municipal project might require $2 million aggregate coverage, while a commercial lease could demand $1 million per occurrence with you named as additional insured. These contract-driven requirements shape your actual budget more than base rates do.

Once you’ve identified your coverage needs and compared quotes across carriers, the next step involves protecting those rates through the decisions you make on the job site. How you operate directly impacts whether your premiums stay stable or climb sharply at renewal.

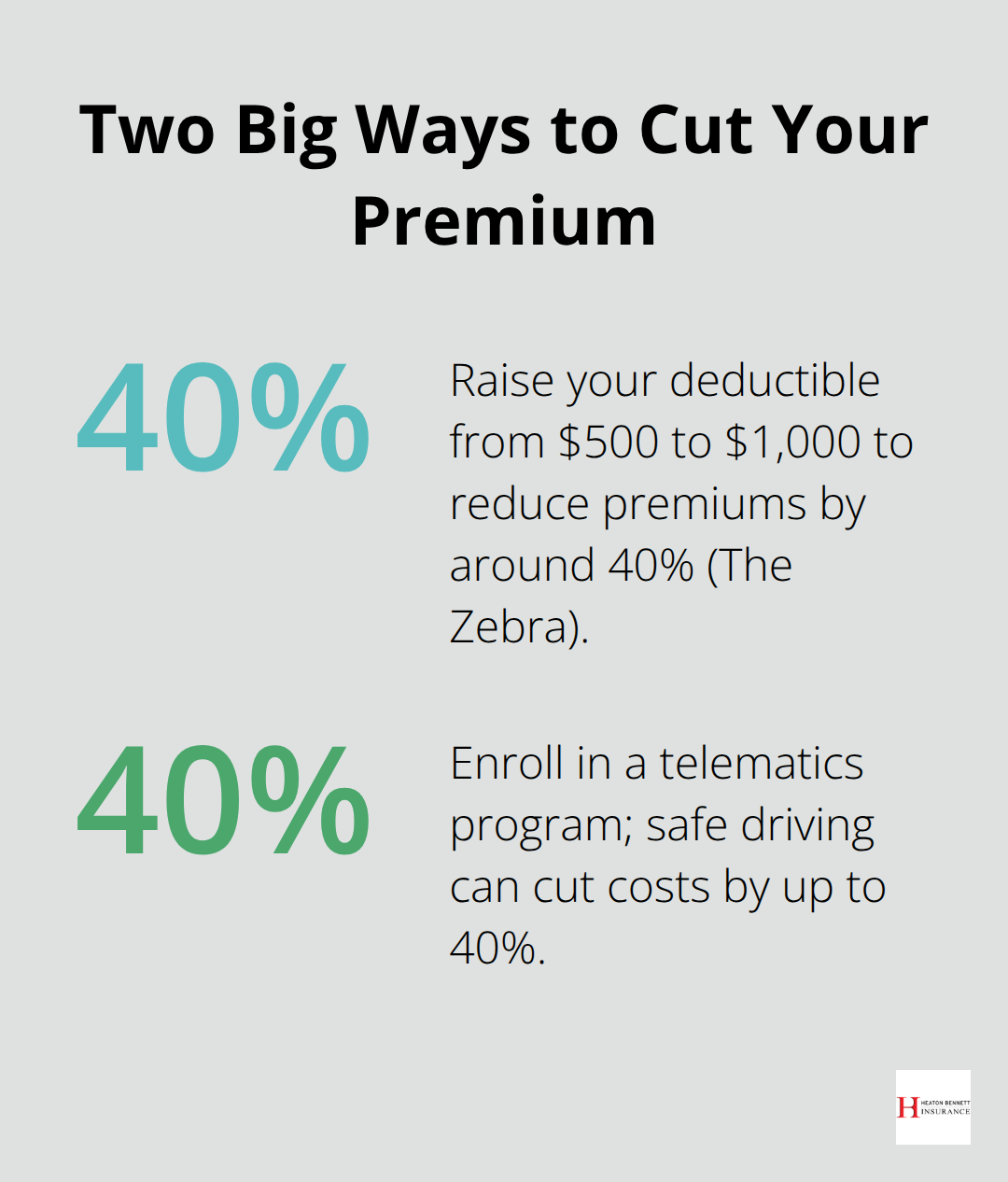

How to Actually Lower Your Premiums

Invest in Safety Programs That Underwriters Reward

Safety programs directly reduce your premiums when you document them properly. Carriers track your safety record closely, and contractors who implement formal training programs see measurable premium reductions. OSHA 30-hour certifications for supervisors, job-site-specific safety plans, and documented incident prevention protocols all signal to underwriters that you operate a tight ship. Licensed trades under Texas Department of Licensing and Regulation rules should document safety compliance meticulously because regulators scrutinize these trades more heavily.

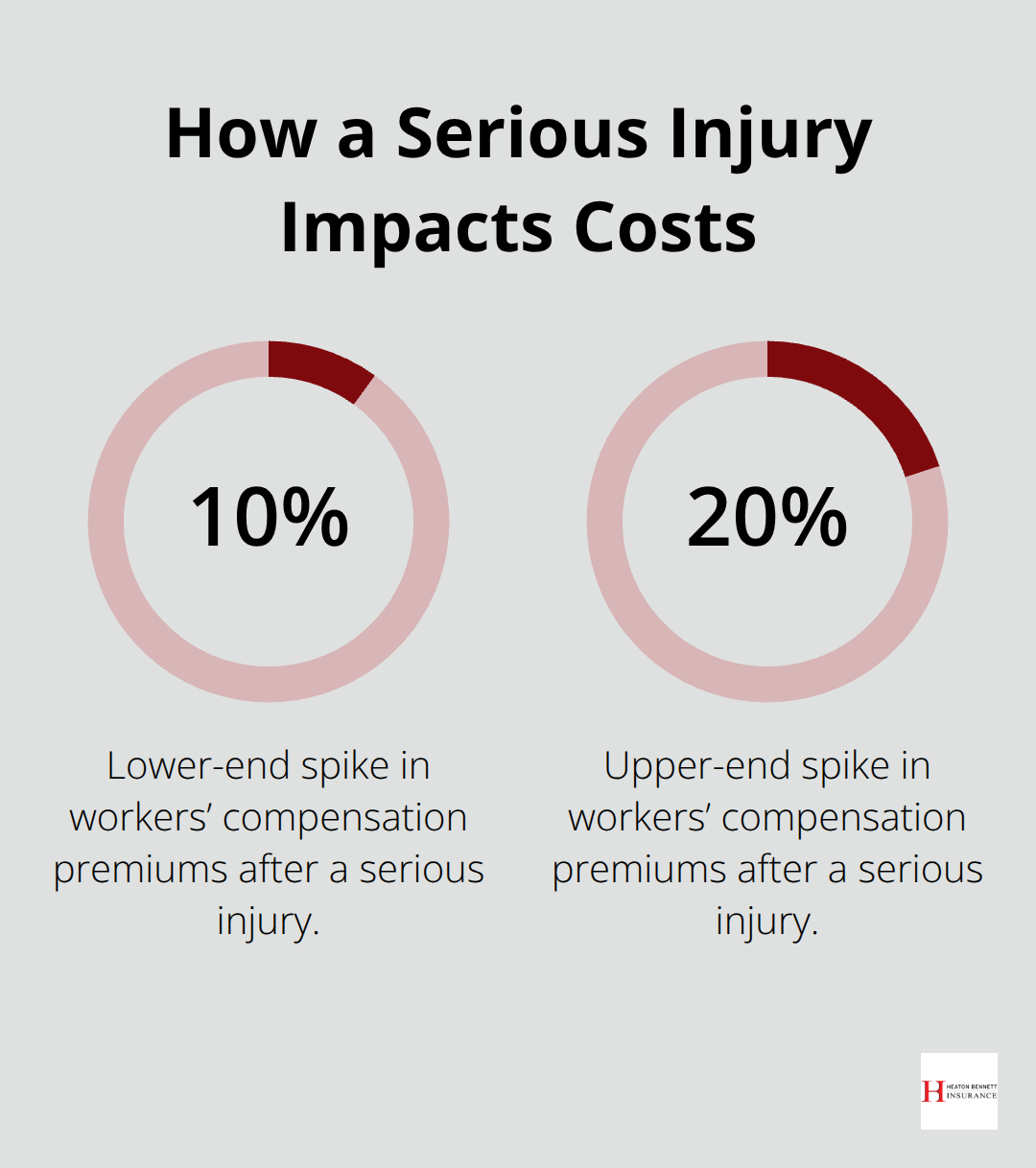

One Texas electrical contractor reduced their workers’ compensation premium by 18% over two years through weekly toolbox talks, job-site safety checklists, and mandatory OSHA training for all crew members. That represents real money returning to your business. Underwriters ask detailed questions about your safety practices during underwriting, so prepare documentation in advance. A contractor without documented safety measures pays significantly more-sometimes 40% or higher premiums for identical coverage.

Bundle Policies to Unlock Substantial Discounts

Bundling policies remains the single most effective cost reduction strategy available to you. General liability alone costs roughly $19 to $60 monthly depending on your trade, but combining general liability with commercial property, workers’ compensation, and commercial auto through a business owner’s policy cuts your overall cost substantially. Insureon data shows bundled coverage averages about $121 monthly compared to purchasing policies separately, which costs considerably more. The discount compounds when you add inland marine coverage for tools and equipment or professional liability for specialized work.

Carriers reward contractors who consolidate their insurance needs with one provider. You lock in volume discounts that single-policy quotes simply won’t match. This approach also simplifies your administrative burden-one renewal date, one point of contact, one consolidated bill instead of juggling multiple carriers and payment schedules.

Protect Your Claims History Above All Else

Your claims history shapes everything from this point forward, which is why protecting it matters more than any other decision you make. A single claim increases your rates 20 to 35 percent for the next three to five years, making prevention your most powerful cost control tool. Contractors who maintain clean records for five years build negotiating leverage at renewal time-some carriers offer loyalty discounts or rate freezes to long-term customers with zero claims.

Prevention protocols cost far less than the premium increases that follow a claim. Invest in safety equipment, proper training, and quality workmanship now rather than absorbing higher premiums later. That approach guarantees lower costs long-term and protects your ability to bid competitively on future projects.

Conclusion

Contractor insurance rates in Texas hinge on three factors you control: your experience and safety record, your trade classification and its regulatory requirements, and your claims history. Understanding these drivers lets you budget accurately instead of guessing at costs or discovering coverage gaps mid-project. The contractors who pay the least aren’t those with the cheapest initial quotes-they’re the ones who invest in documented safety programs, consolidate their insurance with one provider, and treat claims prevention as a business priority.

Proper budgeting starts with listing every coverage type your business actually needs, then comparing quotes across multiple carriers to find real savings. A $1 million revenue electrician budgets roughly $30,706 annually; a plumber around $36,170 (these reflect what Texas contractors actually pay, not theoretical numbers). Bundling policies cuts costs substantially, and maintaining a clean claims record protects your rates from climbing 20 to 35 percent after a single incident.

We at Heaton Bennett Insurance help Texas contractors navigate these decisions without guesswork. Contact Heaton Bennett Insurance to get quotes from top carriers and find the right coverage for your contracting business.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

![Vacation Rental Insurance for Owners [2025 Guide]](https://insureaustin.com/wp-content/uploads/emplibot/Vacation-Rental-Insurance-for-Owners-_2025-Guide__1766711421-180x180.jpeg)