HOA Insurance Requirements for Condos Explained

Condo ownership comes with unique insurance challenges that many residents don’t fully understand. HOA insurance requirements for condo buildings create coverage gaps that can leave individual owners financially exposed.

We at Heaton Bennett Insurance see countless condo owners who assume their HOA’s master policy protects everything. This misconception leads to expensive surprises when claims arise and coverage falls short.

What Does Your HOA Master Policy Actually Cover?

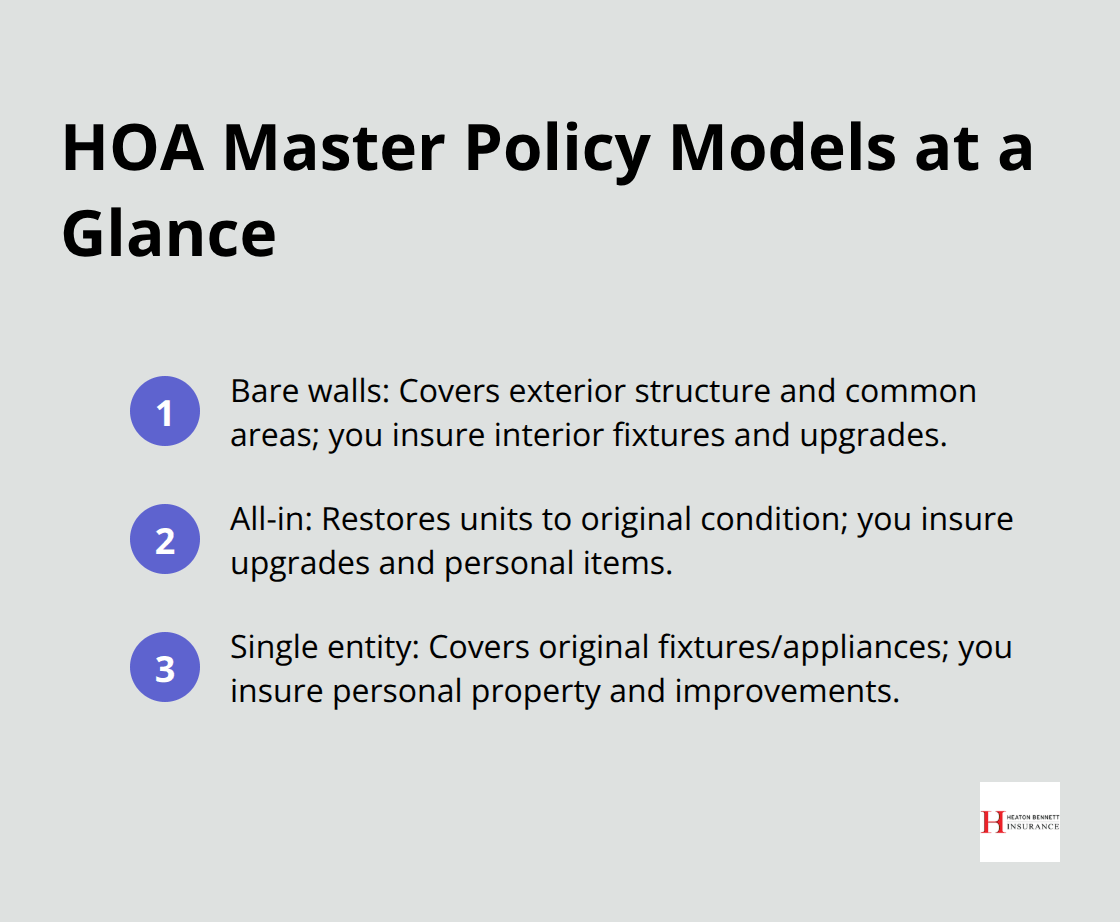

Most condo owners operate under dangerous assumptions about their HOA’s master insurance policy. The Insurance Information Institute reports that over 50% of condo owners remain unaware of their specific coverage requirements, which creates massive financial vulnerabilities. HOA master policies typically follow one of three coverage models that determine your personal insurance needs.

Bare Walls Coverage Leaves You Exposed

Bare walls policies cover only the building’s exterior structure and common areas. Your unit’s interior fixtures, appliances, floors, and personal improvements fall outside this coverage. The National Association of Insurance Commissioners emphasizes that this model places significant responsibility on individual owners. Water damage that destroys your hardwood floors or custom kitchen cabinets won’t receive coverage from the HOA policy.

This coverage type requires the most comprehensive personal condo insurance to fill gaps.

All-In Policies Create Different Risks

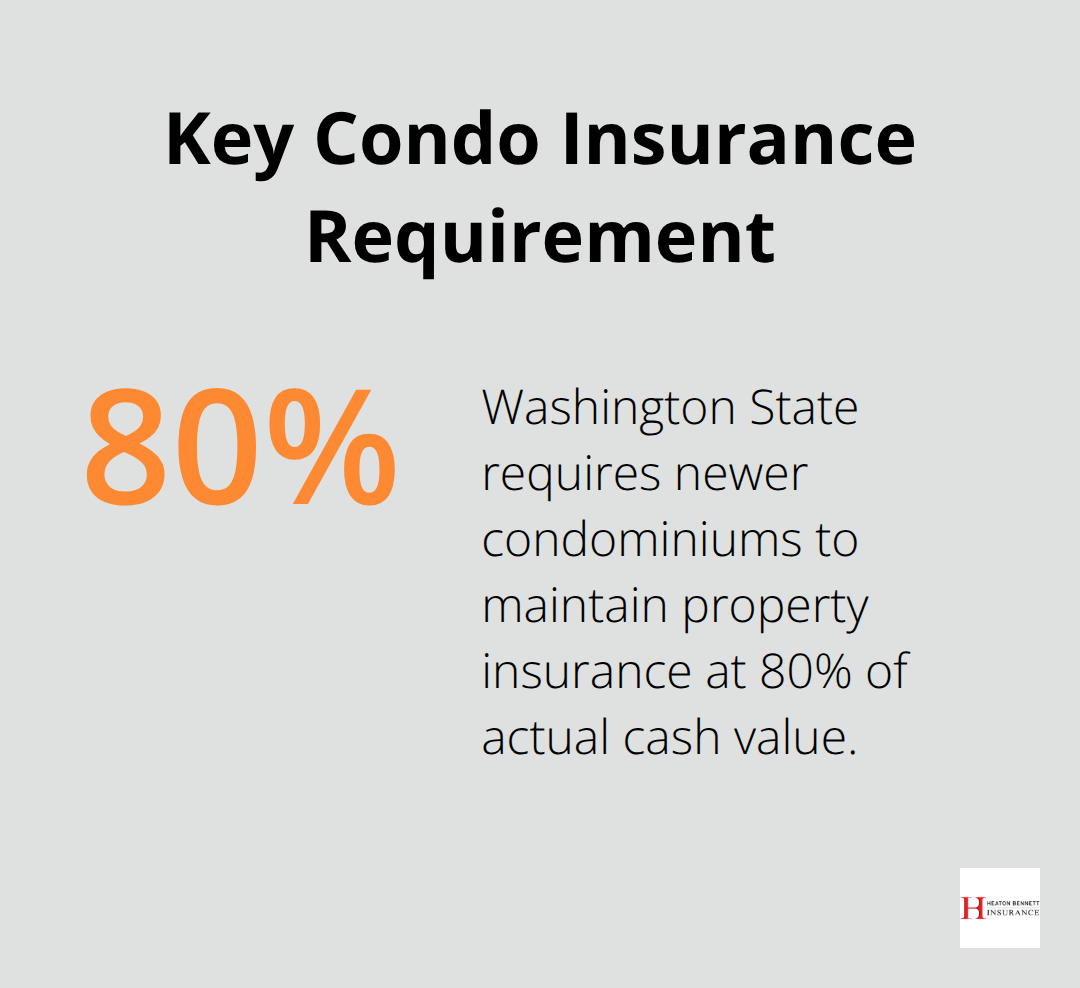

All-inclusive coverage policies restore units to their original condition, which includes fixtures and appliances that the developer installed. However, personal upgrades and improvements remain your responsibility. Washington State’s RCW 64.90.470 requires newer condominiums to maintain property insurance at 80% of actual cash value, but this doesn’t guarantee full replacement costs for your personal investments. Many associations choose this model to reduce individual owner insurance burdens, yet coverage disputes frequently arise over what constitutes original versus upgraded features.

Single Entity Policies Split Responsibilities

Single entity coverage falls between bare walls and all-in policies and covers original fixtures and appliances but excludes personal property and improvements. This model creates the most confusion when claims occur because the determination of original versus upgraded items becomes contentious. Your HOA’s declaration documents require annual review to understand which coverage model applies to your building (this directly impacts your personal insurance requirements and potential out-of-pocket expenses when claims arise).

These coverage gaps between HOA policies and individual needs create specific insurance requirements that every condo owner must address through personal policies.

What Personal Insurance Do Condo Owners Actually Need?

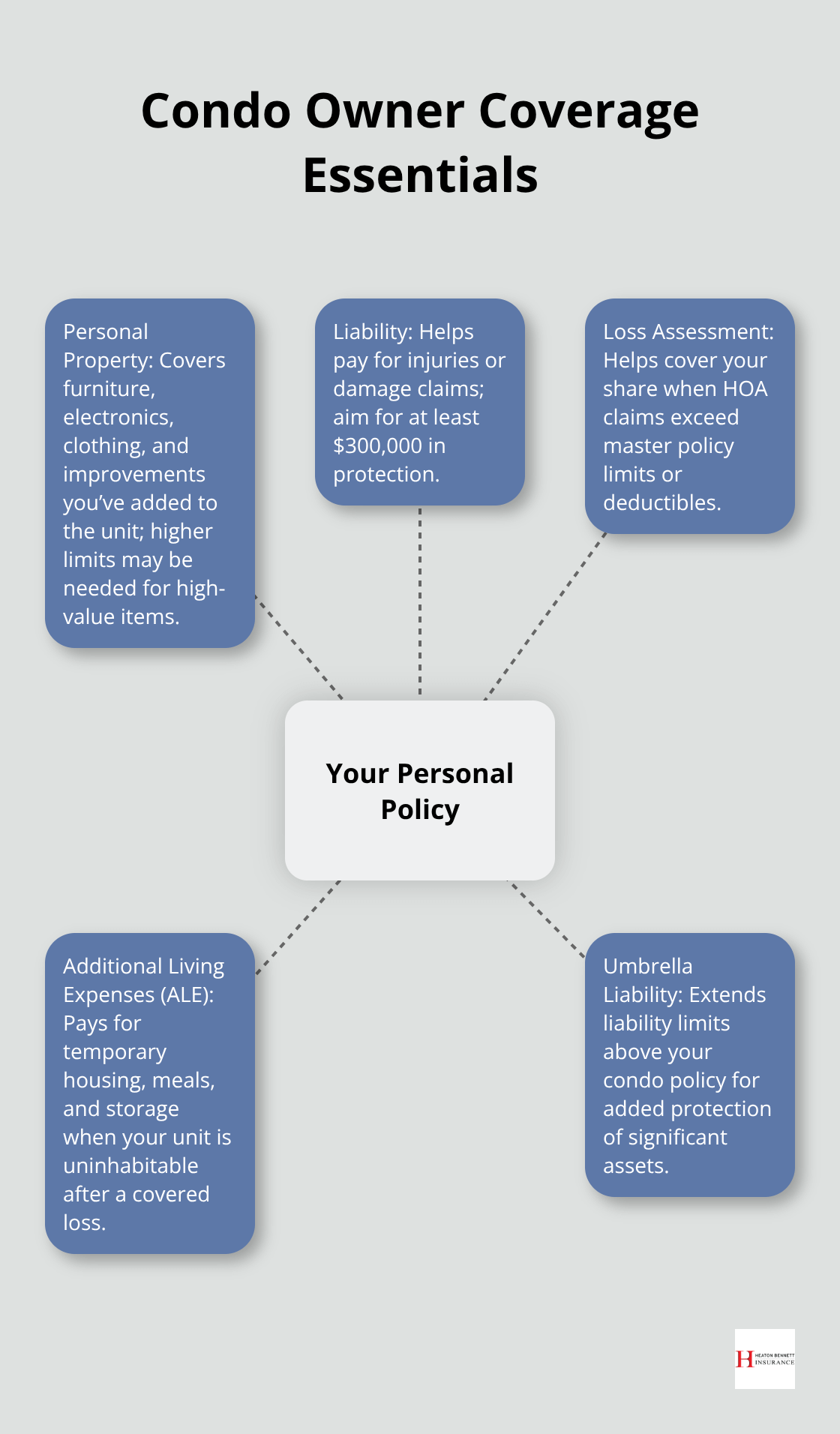

Personal Property Protection Fills Critical Gaps

HOA master policies leave substantial coverage gaps that require strategic personal insurance decisions. The American Association of Insurance Services reports that condo insurance costs between $300 to $800 annually, yet many owners purchase inadequate coverage that fails to protect their actual financial exposure.

Personal property coverage becomes your primary defense against losses that HOA policies exclude. This includes furniture, electronics, clothing, and personal improvements you’ve made to your unit. Standard policies start at $100,000 for personal possessions, but owners with valuable items need higher limits based on detailed property inventories (complete with photographs and receipts for verification).

Liability Coverage Protects Against Lawsuits

Personal condo policies protect against lawsuits when accidents occur inside your unit. The Insurance Information Institute recommends minimum limits of $300,000 for adequate protection against potential claims.

Water damage ranks as the most common condo insurance claim, which makes liability protection essential when your actions cause damage to neighboring units. Personal umbrella policies extend liability coverage beyond standard limits and become necessary for owners with significant assets.

Loss Assessment Coverage Handles Special Assessments

Loss assessment coverage represents the most overlooked protection that covers unexpected special assessments when HOA claims exceed policy limits or deductibles. This coverage protects you when your HOA faces major repairs that trigger assessments distributed among all unit owners.

Additional living expenses coverage pays for temporary housing when your unit becomes uninhabitable after covered damage (hotel costs, restaurant meals, and storage fees add up quickly during extended displacement periods).

These personal insurance requirements become even more complex when coverage disputes arise between HOA policies and individual owner policies.

How Coverage Disputes Impact Condo Owners

Inadequate Coverage Creates Financial Disasters

Statistical data from the National Association of Insurance Commissioners shows that many condo associations carry insufficient liability coverage, which directly exposes individual owners to increased financial risk. HOAs frequently purchase minimum required coverage to reduce association fees, but this approach creates expensive consequences when major claims occur.

Associations with inadequate limits face special assessments that can reach thousands of dollars per unit when catastrophic events exceed policy limits. The Champlain Towers South collapse in 2021 demonstrated how insufficient coverage transforms into massive financial burdens for unit owners who faced assessments for legal costs and victim compensation.

Special Assessments Strike Without Warning

HOA deductibles on master policies typically range from $10,000 to $100,000 per claim, and these costs get distributed among unit owners through special assessments. Water damage claims represent the most frequent trigger for assessments because they often affect multiple units simultaneously and exceed deductible thresholds quickly.

Washington State law requires newer condominiums to maintain property insurance at 80% of actual cash value, yet many associations choose higher deductibles to reduce premium costs and shift financial responsibility to owners. These unexpected assessments can devastate household budgets when owners haven’t prepared for sudden expenses.

Policy Conflicts Create Coverage Battles

RCW 64.34.352 and RCW 64.90.470 establish that HOA master policies provide primary coverage while individual unit policies serve as secondary coverage, but this hierarchy creates disputes over which insurer pays first. Insurance companies frequently argue over coverage responsibility, which delays repairs and leaves owners with out-of-pocket expenses.

Unit owners must file claims with their personal insurers even when HOA policies should provide coverage because secondary insurers often refuse payment until primary coverage disputes resolve. Prompt claim submission to both insurers prevents delays, but owners need documented evidence of what each policy covers to avoid prolonged battles between insurance companies (these disputes can extend for months while damage worsens).

Final Thoughts

HOA insurance requirements for condo ownership protect you from devastating financial surprises that can destroy your household budget. Your HOA’s master policy creates coverage gaps that demand strategic personal insurance decisions to avoid expensive out-of-pocket costs when claims arise. Document your personal property with detailed inventories and photographs to support future claims when disasters strike.

Review your HOA’s declaration documents annually to understand which coverage model applies to your building and affects your personal insurance needs. Purchase adequate personal liability coverage with minimum limits of $300,000 and add loss assessment coverage to protect against special assessments. Verify that your personal policy coordinates properly with your HOA’s master coverage to prevent disputes between insurers (these battles can delay repairs for months while damage worsens).

Work with experienced insurance professionals who understand the complexities of condo coverage requirements and can identify potential gaps in your protection. We at Heaton Bennett Insurance help navigate these complex coverage requirements and provide access to multiple carriers. Our independent agency creates tailored insurance solutions that address your specific condo ownership risks without gaps in protection.