Key Person Insurance in Succession Planning Securing Your Company’s Future

Your company’s most valuable employees hold the keys to daily operations, client relationships, and future growth. When these key personnel leave unexpectedly, the financial impact can devastate even well-established businesses.

We at Heaton Bennett Insurance understand that effective succession planning requires more than just identifying replacements. Key person insurance provides the financial bridge your company needs during critical transitions.

What Key Person Insurance Actually Covers

Key person insurance delivers immediate cash when your most valuable employees die or become permanently disabled. The policy pays out tax-free proceeds directly to your business, not to the employee’s family. This money replaces lost revenue, covers recruitment costs, and keeps operations stable while you search for replacements.

The Financial Protection You Get

Unlike general liability or property insurance that protects against external risks, key person coverage addresses internal vulnerabilities that threaten your company’s survival. The policy compensates for revenue gaps, operational delays, and client relationship disruptions that occur when key personnel leave unexpectedly. Standard business insurance policies exclude these internal risks entirely.

The Real Cost of Personnel Loss

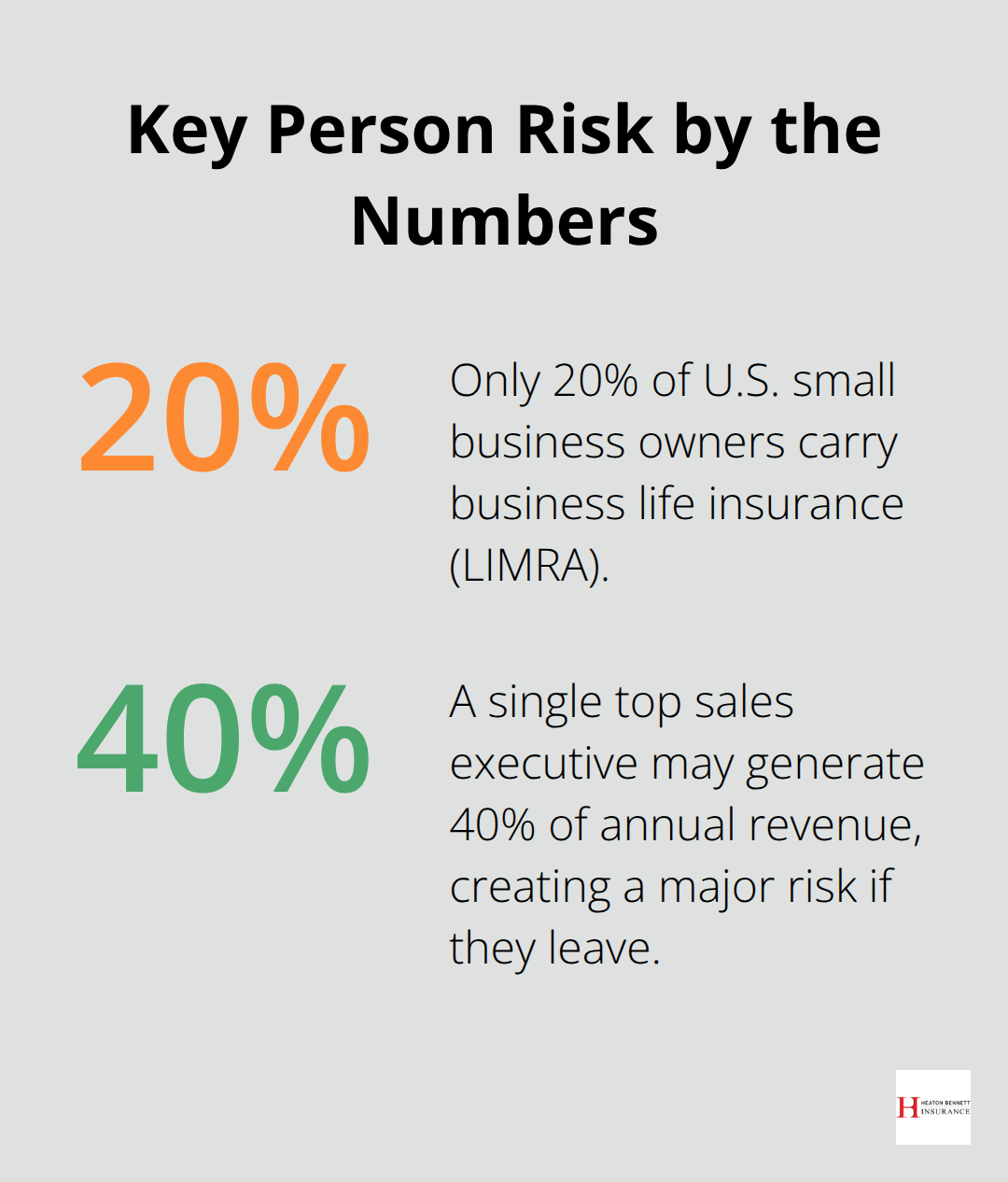

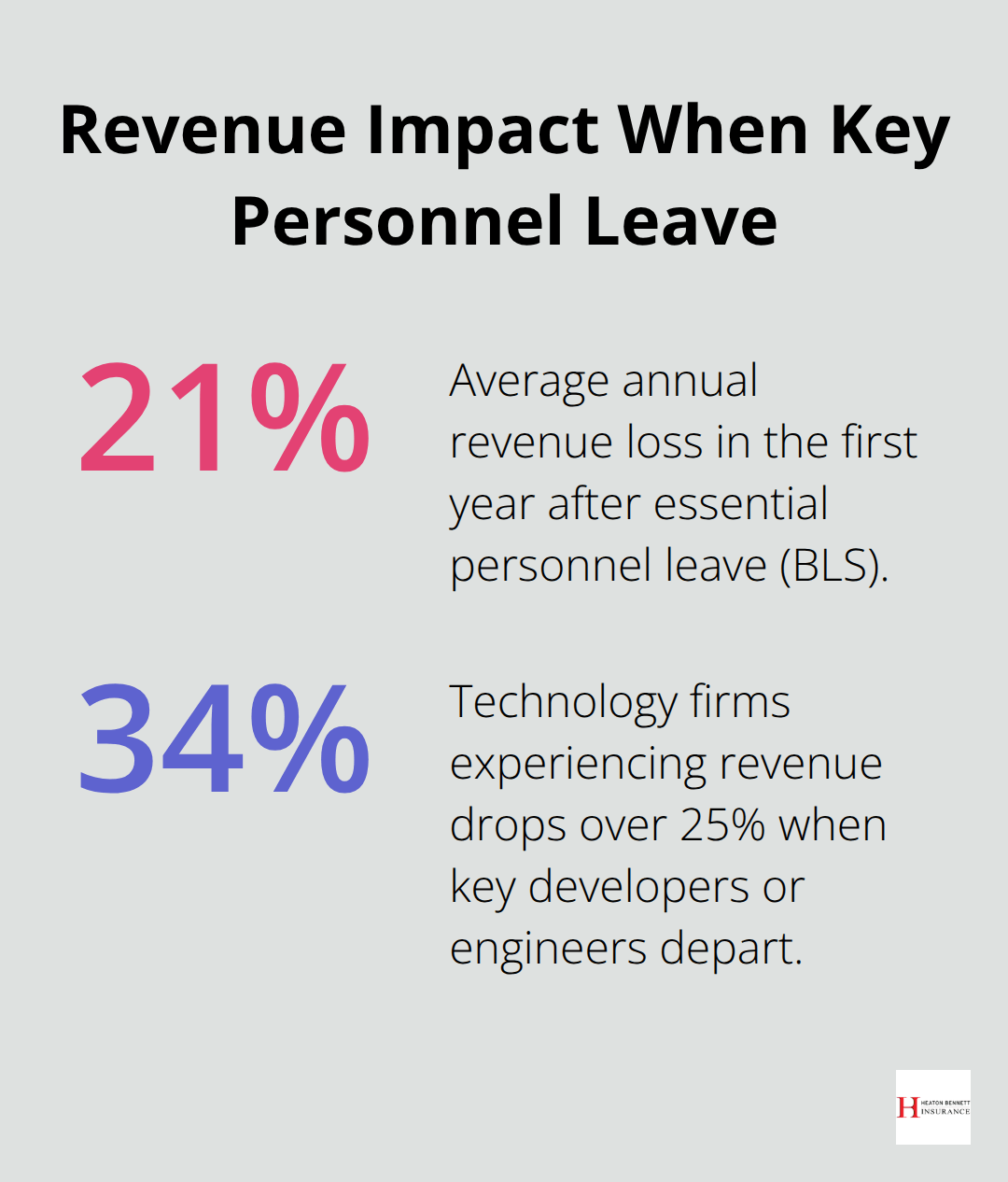

LIMRA research shows only 20% of small business owners carry business life insurance, yet companies face substantial financial hits when key employees leave. Recruitment and training expenses alone cost an average of 6 to 18 months of that person’s salary. Revenue losses compound this financial damage significantly.

A top sales executive who generates 40% of your annual revenue creates a massive gap when they leave unexpectedly. Key person insurance covers these direct losses plus the hidden costs of client defection, delayed projects, and operational disruptions (costs that standard business insurance ignores completely).

How This Differs From Employee Benefits

Standard group life insurance benefits the employee’s beneficiaries, while key person insurance protects your business interests. You own the policy, pay the premiums, and receive the death benefits. The coverage amount reflects the employee’s value to your company rather than their personal financial needs.

This fundamental difference makes key person insurance a business asset that strengthens your balance sheet. Lenders and investors often require this coverage before they approve business loans, as it demonstrates financial stability and risk management.

The next step involves identifying which specific employees qualify for this protection and calculating the appropriate coverage amounts.

Identifying Key Personnel and Assessing Coverage Needs

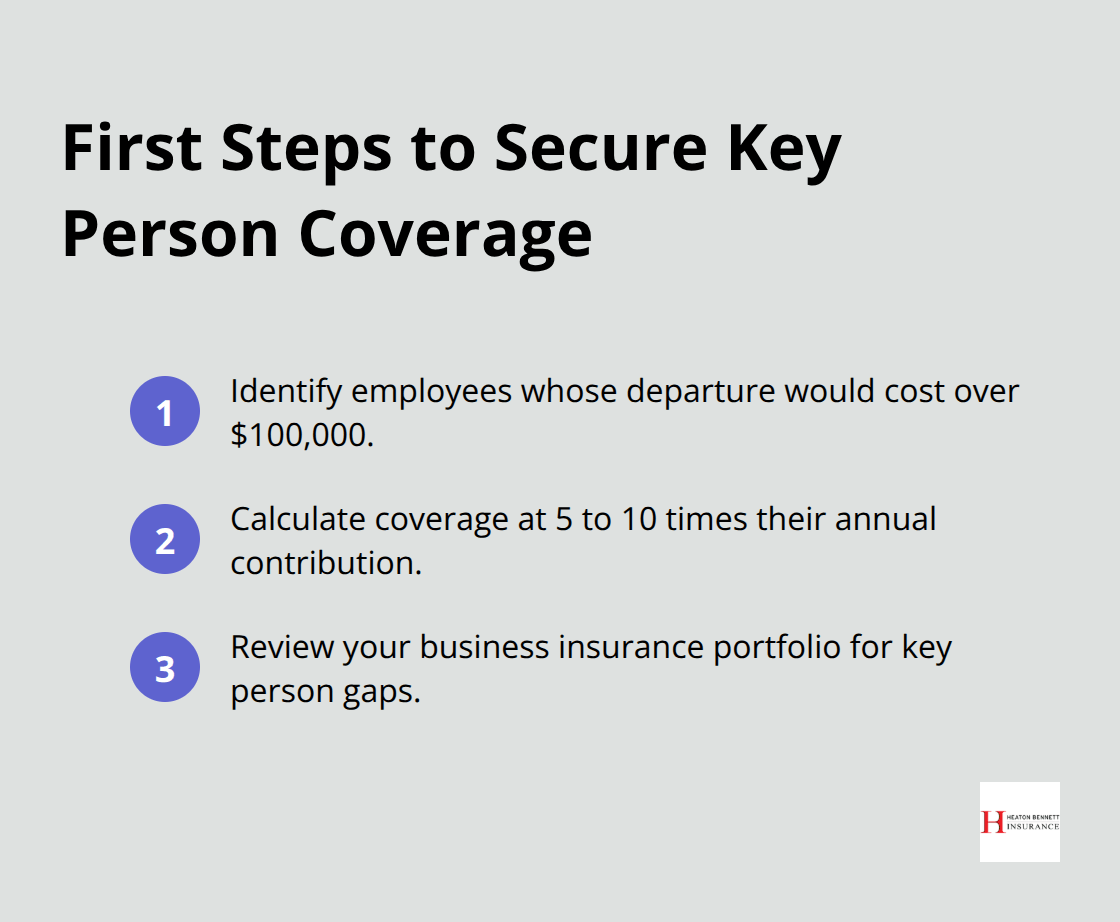

Your business depends on specific individuals who drive revenue, maintain client relationships, and possess irreplaceable knowledge. The founder who controls 60% of client relationships qualifies immediately. The software developer whose proprietary code powers your entire platform qualifies. The sales manager who personally handles your three largest accounts qualifies. Anyone whose sudden departure would create operational chaos deserves serious consideration.

Revenue Impact Assessment

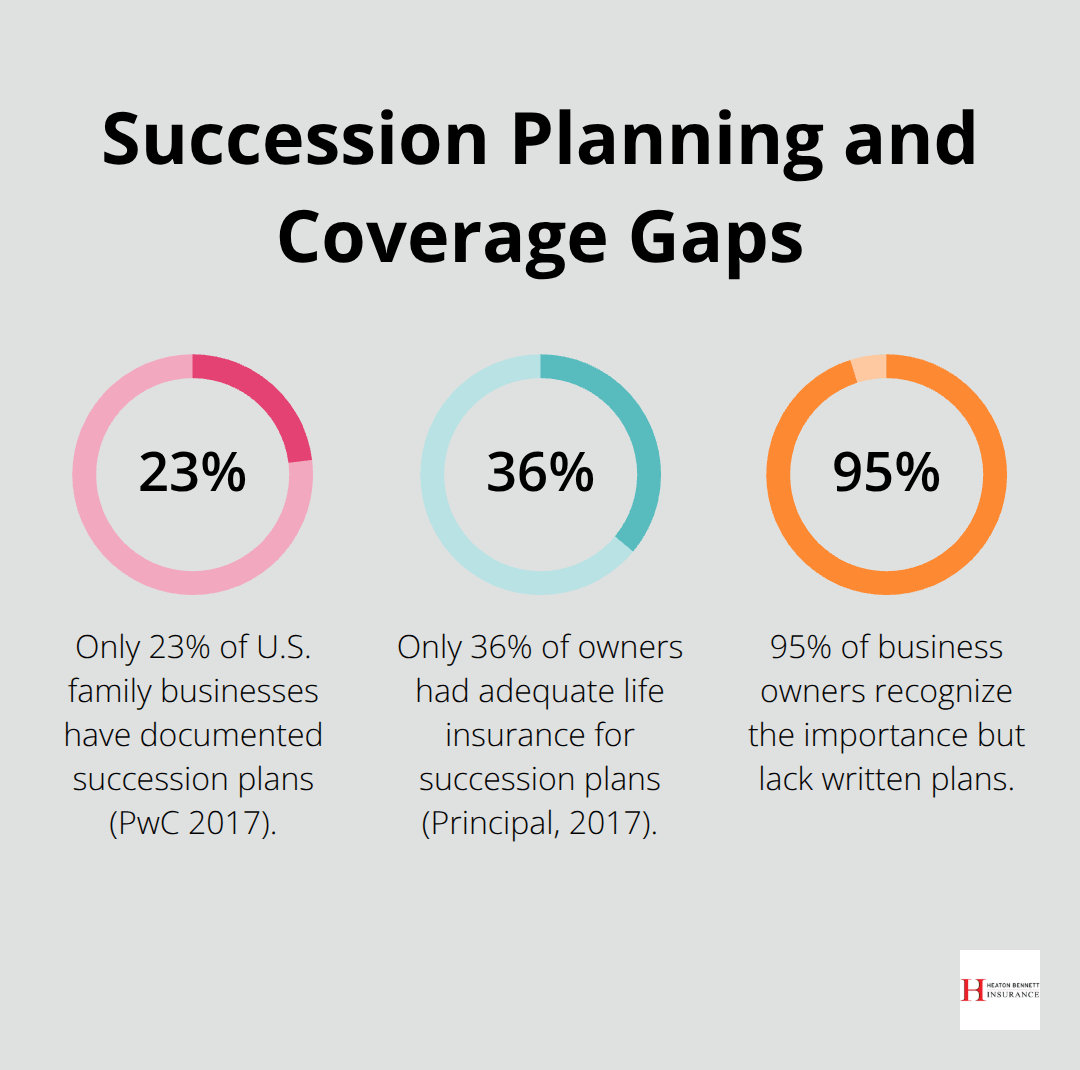

Calculate each employee’s direct revenue contribution through their sales figures, client relationships, and project leadership over the past 24 months. PwC’s 2017 U.S. Family Business Survey revealed that only 23% of family businesses maintain documented succession plans, yet these companies often stake their survival on one or two key individuals.

Multiply the employee’s annual compensation by 5 to 10 times to establish baseline coverage amounts. A $100,000 executive might require $500,000 to $1,000,000 in coverage based on their revenue impact and replacement timeline. This calculation provides the foundation for protection levels that match actual business risk.

Skills and Relationship Evaluation

Target employees with irreplaceable institutional knowledge, exclusive client relationships, or specialized technical skills that would take months to replace. The marketing director who personally knows every major client creates more risk than someone who simply manages campaigns. The engineer who designed your core product systems poses greater vulnerability than general programmers.

Document specific relationships, contracts tied to individuals, and knowledge that exists nowhere else in your organization (these factors often justify higher coverage amounts than pure revenue calculations suggest). The absence of these relationships can trigger client defections and operational breakdowns that extend far beyond immediate revenue loss.

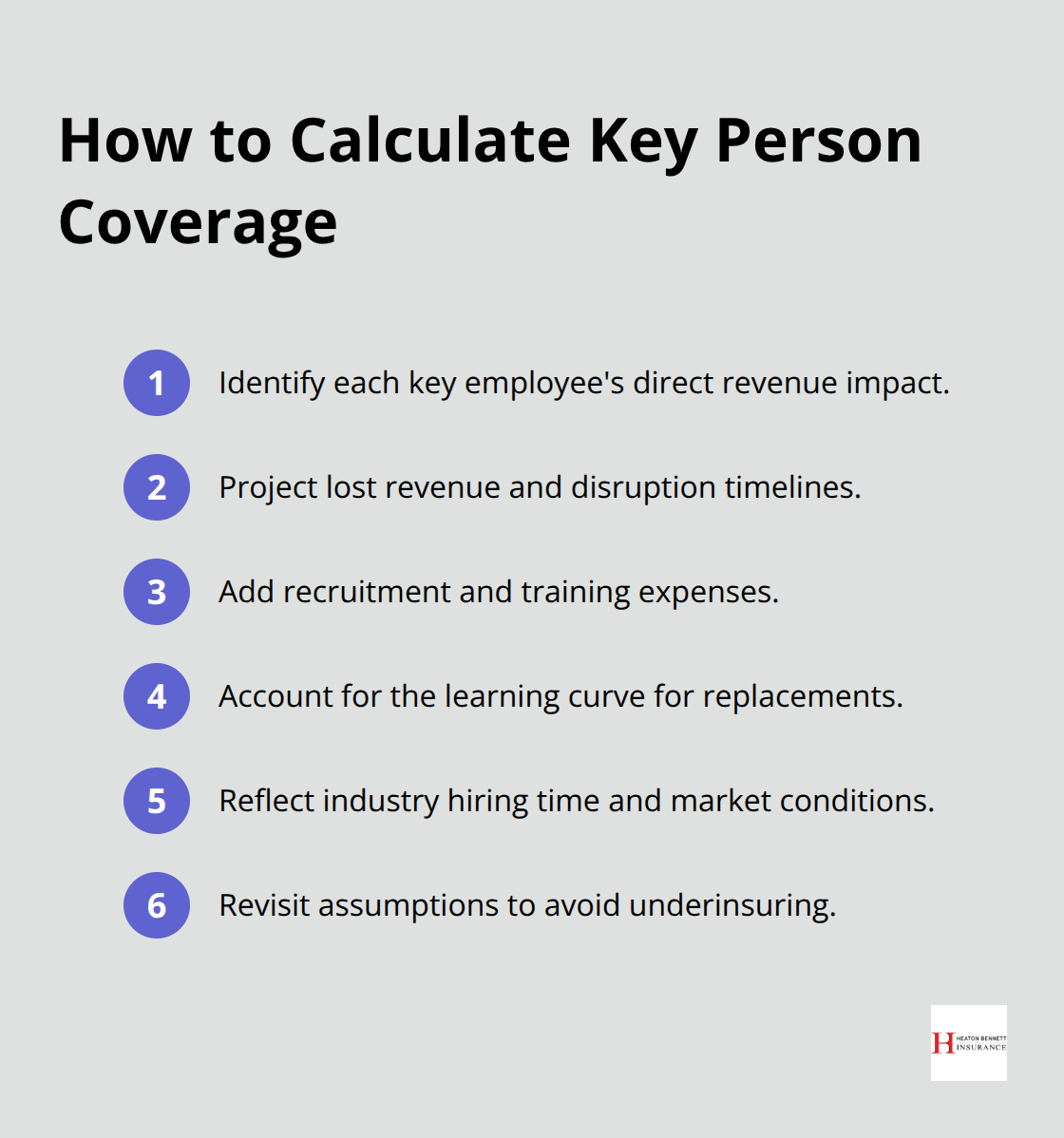

Coverage Amount Calculations

Base your coverage calculations on replacement costs, lost revenue projections, and business disruption timelines. Factor in recruitment expenses, training costs, and the learning curve new employees face when they join your organization. Most businesses underestimate these transition costs and purchase insufficient coverage as a result.

Consider the time required to find qualified replacements in your industry and geographic area. Specialized roles in competitive markets demand higher coverage amounts due to extended search periods and premium compensation packages needed to attract top talent.

We can assist you with assessing your insurance needs and provide you with some quotes from several of the top insurance companies to ensure your key person coverage aligns with your actual business risks.

The next phase involves structuring these policies to support your broader succession strategy and coordinate with existing business agreements.

Implementing Key Person Insurance as Part of Succession Strategy

Purchase Coverage Before You Need It

Buy key person insurance immediately after you identify critical personnel, not when succession discussions begin. The National Federation of Independent Business reports that many small business owners delay this coverage until retirement approaches, which creates dangerous protection gaps. Young, healthy employees qualify for lower premiums and better terms than older executives who face health issues. A 35-year-old key employee might pay 60% less in annual premiums than the same coverage purchased at age 55.

Structure Policies for Maximum Flexibility

Term life insurance works best for short-term succession scenarios where you plan to replace key personnel within 5-10 years. Universal life insurance provides permanent protection with cash value accumulation that supports long-term succession strategies. Split the coverage between both policy types to balance immediate protection with future flexibility (this approach gives you options as business needs change). Set the business as both owner and beneficiary to maintain complete control over policy proceeds and avoid complications with employee departures.

Coordinate Coverage with Business Agreements

Key person insurance must align with buy-sell agreement valuations and mechanisms. The Principal Financial Group found that only 36% of business owners had adequate life insurance for succession plans in their 2017 study. Structure policy amounts to match buy-sell agreement obligations exactly, which prevents shortfalls during ownership transitions. Update coverage amounts annually to reflect business growth and changes in key person responsibilities.

Link Policies to Succession Triggers

Connect policy proceeds to specific succession triggers like disability, retirement, or death to activate predetermined transition plans automatically. This connection streamlines the succession process and eliminates confusion about when coverage applies (clear triggers prevent disputes among stakeholders). Document these triggers in both the insurance policy and your succession plan to maintain consistency across all business agreements.

Final Thoughts

Key person insurance transforms succession planning from a risky gamble into a strategic advantage. The 95% of business owners who recognize succession planning’s importance but lack written plans expose themselves to unnecessary financial devastation. Your company cannot afford to join the 80% of businesses that operate without this protection.

The tax-free proceeds from key person policies provide immediate liquidity when your most valuable employees leave unexpectedly. This financial cushion covers recruitment costs, maintains client relationships, and prevents the operational chaos that destroys business value. Companies with proper key person coverage weather personnel transitions without compromising their competitive position or stakeholder confidence.

Document your key personnel today and calculate their revenue impact on your business. Purchase coverage while these employees remain healthy and premiums stay affordable (review policy amounts annually as your business grows and key roles evolve). We at Heaton Bennett Insurance specialize in tailored insurance solutions that protect your business interests and provide access to multiple carriers with personalized coverage options that align with your succession planning objectives.

![Annuities Explained The Ultimate Guide for Retirees [2025]](https://insureaustin.com/wp-content/uploads/emplibot/Annuities-Explained-The-Ultimate-Guide-for-Retirees-_2025__1760663225-180x180.jpeg)