Is Group Disability Insurance Worth It for Your Company?

Group disability coverage protects your employees’ income when illness or injury prevents them from working. Yet many business owners question whether the investment makes financial sense.

We at Heaton Bennett Insurance see companies struggle with this decision daily. The answer depends on your workforce size, budget, and employee retention goals.

What Group Disability Coverage Actually Includes

Group disability insurance divides into two distinct types that serve different purposes. Short-term disability covers temporary conditions that last three to six months, replaces 60% to 100% of salary with minimal wait periods. Long-term disability begins after 90 to 180 days and provides 50% to 60% of base salary for extended periods, sometimes until retirement age. The Social Security Administration reports that one in four 20-year-olds will experience a disability before retirement, which makes this distinction vital for workforce plans.

Coverage Amounts Follow Strict Formulas

Most group plans cap monthly benefits at $5,000 regardless of salary levels, which creates coverage gaps for high earners. The standard 60% income replacement drops to 35% to 40% after taxes when employers pay premiums. Companies with 10 or more employees typically qualify for group rates, which cost significantly less than individual policies. Premium costs range from $25 to $500 monthly (based on industry risk levels), with office-based businesses that pay substantially less than operations in manufacturing.

Group Plans Trade Flexibility for Affordability

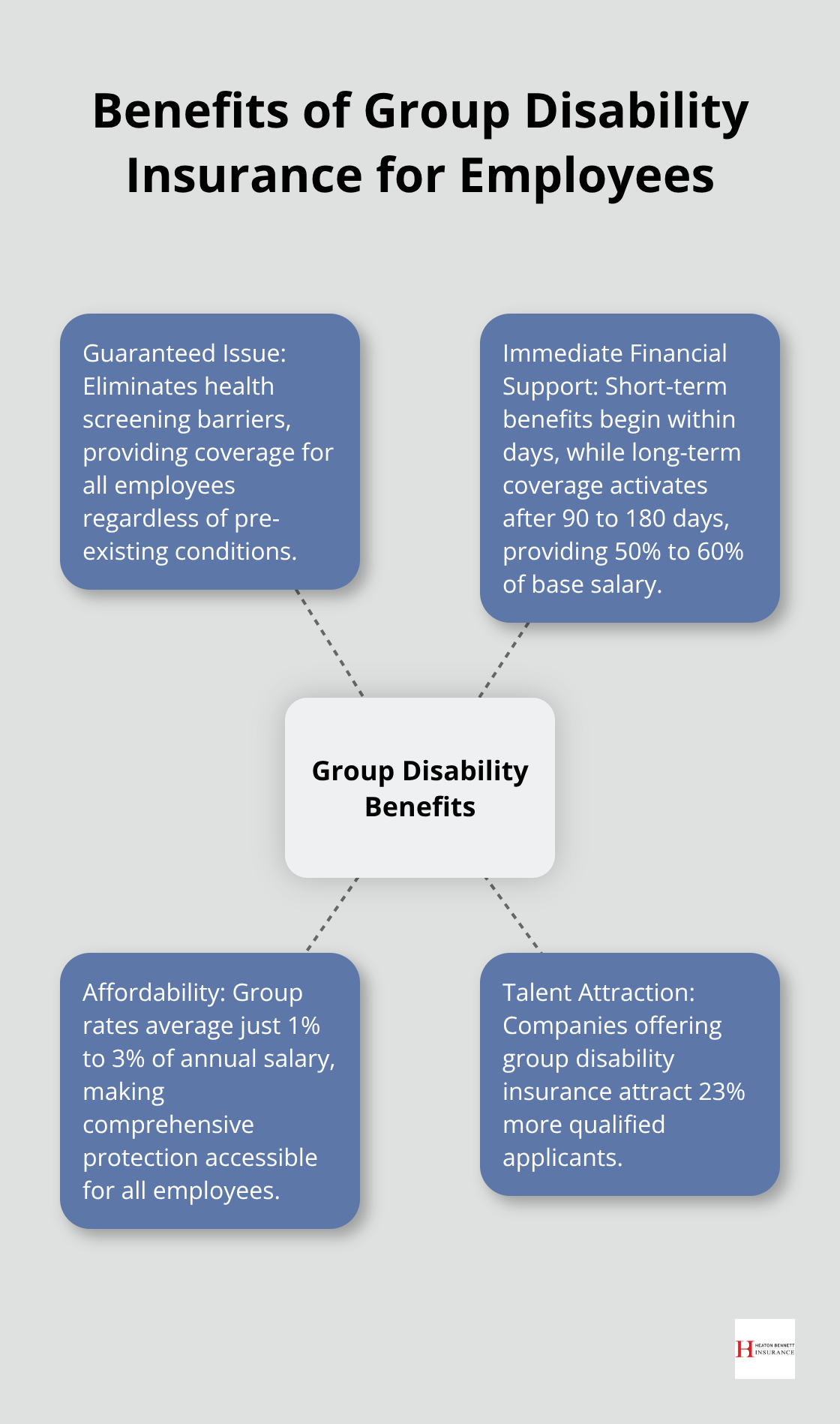

Group policies operate as guaranteed issue coverage, which means employees cannot face denial based on health conditions. However, this convenience comes with rigid benefit structures and limited portability when employees change jobs. Individual policies offer higher benefit caps, tax-free payouts when employees pay premiums, and stronger disability definitions. Group plans often require total disability for claims approval, while individual policies may cover partial disabilities or specific occupation limitations.

Premium Structure Affects Your Bottom Line

Employers have flexibility in premium payments through company coverage, employee contributions, or combination approaches. Pre-tax premiums can be tax-deductible for the business (which provides potential tax benefits for employers). However, benefits paid for employer-covered premiums may be taxed as income for employees, which reduces their net benefit value. This tax treatment significantly impacts the actual financial protection employees receive when they need benefits most.

Why Group Plans Save Money

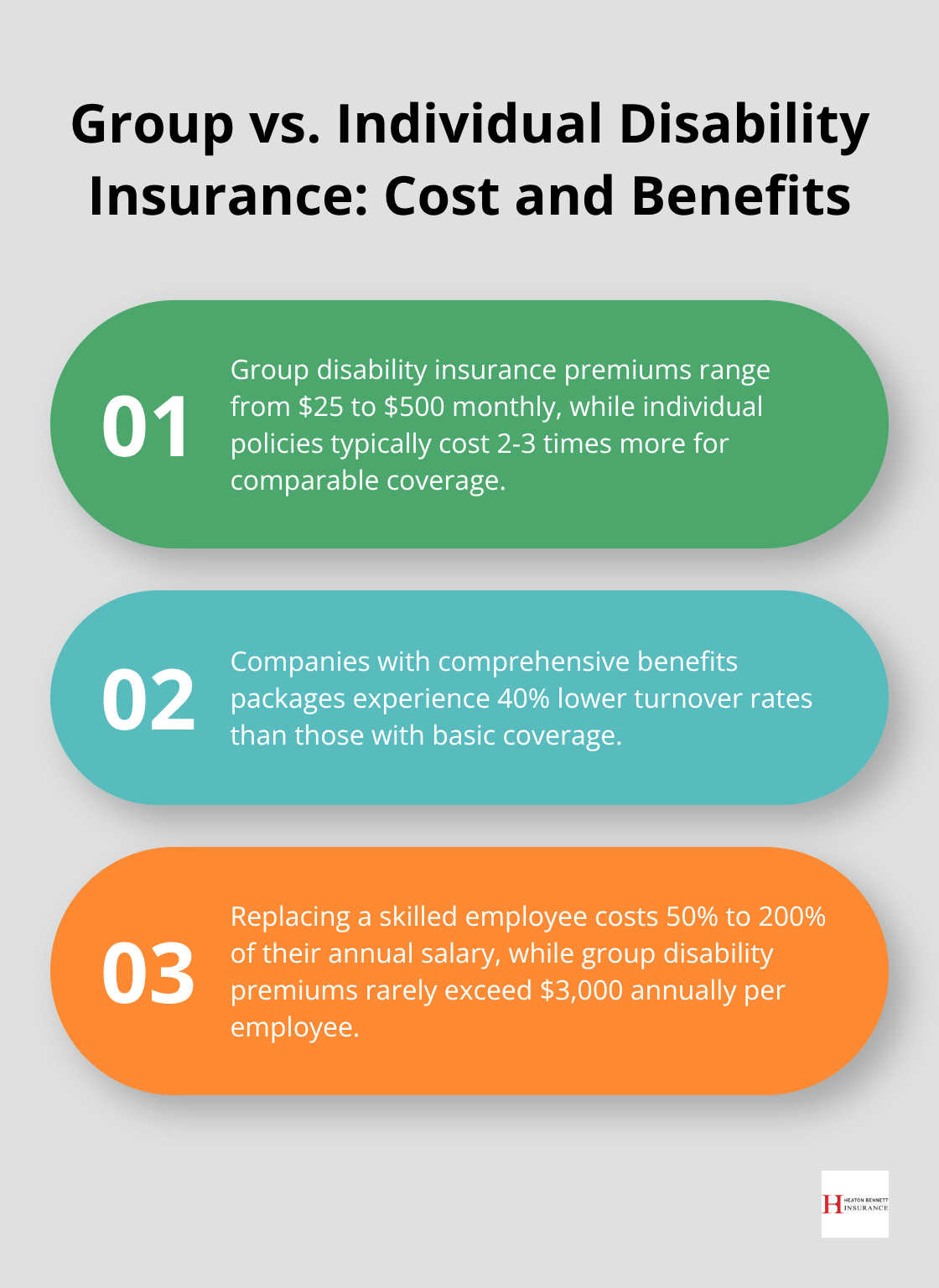

Group disability insurance delivers substantial cost advantages that individual policies cannot match. Premium costs for group coverage range from $25 to $500 monthly based on industry risk, while individual policies typically cost 2-3 times more for comparable coverage. Companies with office-based employees pay significantly less than manufacturing operations due to lower claim frequencies.

Administrative Costs Drop Dramatically

Group plans eliminate medical underwriting costs and administrative overhead that drive up individual policy expenses. The guaranteed issue feature means no employee faces denial, which reduces the administrative burden of managing multiple individual applications and approvals. Companies process one group application instead of dozens of individual submissions, cutting paperwork and processing time by 75%.

Tax Benefits Lower Your Real Costs

Premium payments for group disability insurance qualify as tax-deductible business expenses, which reduces your effective cost by your corporate tax rate. A company that pays 25% corporate tax effectively reduces their premium costs by that same percentage. However, when employers pay premiums, employee benefits become taxable income (reducing the net benefit employees receive). Companies can shift this tax burden by requiring employees to pay premiums with after-tax dollars, making their benefits tax-free.

Retention Benefits Exceed Premium Costs

The Hartford reports that companies with comprehensive benefits packages experience 40% lower turnover rates than those with basic coverage. Replacing a skilled employee costs 50% to 200% of their annual salary according to Society for Human Resource Management data. For a company that loses just two employees annually at $60,000 salaries, replacement costs reach $60,000 to $240,000. Group disability premiums rarely exceed $3,000 annually per employee, making the retention value clear.

These financial advantages create a compelling business case, but the real value lies in what this coverage means to your employees when they face unexpected health challenges.

What Do Employees Really Gain from Group Coverage

Group disability insurance transforms your employees’ financial security in ways that individual policies cannot match. When a construction worker at a mid-sized firm suffers a back injury that requires six months of recovery, group short-term disability immediately replaces 60% to 100% of their salary with just a 7-day wait period. Without this protection, that same employee would face impossible choices between medical bills and mortgage payments. The Society for Human Resource Management found that 69% of employees consider disability benefits extremely important when they evaluate job offers (ranking it higher than retirement contributions).

Coverage Reaches Every Employee

Group plans eliminate the health screening barriers that block high-risk employees from individual coverage. A diabetic office manager or a worker with a previous heart condition gains the same disability protection as their healthiest colleagues through guaranteed issue enrollment. Individual policies would either deny these employees outright or charge premiums that exceed $800 monthly for similar coverage. Group rates average just 1% to 3% of annual salary, which makes $50,000 employees pay roughly $500 to $1,500 yearly for comprehensive protection.

Benefits Packages Drive Talent Decisions

Companies that offer group disability insurance attract 23% more qualified applicants according to recent Bureau of Labor Statistics employment data. High-performing candidates specifically seek employers who demonstrate investment in long-term employee welfare beyond basic group health insurance. The guaranteed renewable feature means employees retain coverage stability regardless of health conditions they develop, unlike individual policies that may face cancellation or premium increases. This combination of affordability, accessibility, and employment-based stability creates a compelling value proposition that strengthens your position in competitive markets.

Financial Protection Starts Immediately

Short-term disability benefits begin within days of a qualifying condition, while long-term coverage activates after 90 to 180 days. Employees receive 50% to 60% of their base salary through long-term benefits (sometimes until retirement age). This immediate financial support prevents the devastating income loss that forces families into debt or bankruptcy when medical emergencies strike unexpectedly.

Final Thoughts

Group disability insurance provides measurable value when you compare premium costs against employee protection and retention benefits. Companies that spend $1,500 annually per employee on disability coverage often save $60,000 to $240,000 in replacement costs for each worker they retain. The guaranteed issue feature removes health screening barriers while it provides immediate financial protection that individual policies cannot match.

Your decision depends on workforce size, industry risk levels, and competitive position in talent markets. Businesses with 10 or more employees access group rates that cost significantly less than individual coverage. Manufacturing operations face higher premiums than office-based companies, but the protection value stays consistent across industries.

Companies that offer comprehensive disability coverage attract 23% more qualified applicants and experience 40% lower turnover rates than those with basic benefits (compared to businesses without these protections). We at Heaton Bennett Insurance help Austin businesses evaluate group disability options through our independent agency access to multiple carriers. Our team provides tailored coverage recommendations that fit your specific workforce needs and budget constraints.