Why Does My Auto Insurance Premium Keep Increasing?

Auto insurance premiums have surged 26% nationwide over the past two years, leaving drivers asking “why does my auto insurance go up” every renewal period.

Multiple factors drive these increases, from inflation hitting repair costs to changing risk patterns across the industry. We at Heaton Bennett Insurance see clients grappling with these rising costs daily, often without understanding the underlying causes.

What Forces Drive Your Premium Higher

Vehicle repair costs have jumped 37% since 2020 according to the Bureau of Labor Statistics, and insurers pass these increases directly to policyholders. Modern vehicles contain advanced safety technology, backup cameras, and collision avoidance systems that cost significantly more to repair than older models. A simple fender-bender that once required basic bodywork now demands recalibration of sophisticated sensors and replacement of expensive electronic components. Parts shortages have extended repair times and inflated costs further, with some repairs now taking weeks longer than pre-pandemic levels.

Claims Cost More and Happen More Often

The Insurance Information Institute reports that collision claims now average $5,992, up 36% from 2019 levels. Medical costs from auto accidents have risen even faster, with personal injury protection claims up 40% in three years. Weather-related claims have intensified dramatically, with hail damage alone costing insurers $2.5 billion more annually than five years ago. Distracted drivers cause more accidents despite awareness campaigns, while uninsured motorist claims force covered drivers to pay higher premiums.

Risk Assessment Models Have Changed

Insurance companies now analyze your habits through telematics and smartphone apps, and they’ve discovered that pandemic-era changes created new risk profiles. Urban drivers who switched to suburban commutes face different accident patterns, while work-from-home arrangements altered traditional risk calculations. Credit-based insurance scoring has become more sophisticated (with frequent credit checks that reveal financial stress correlating with claim frequency). ZIP code risk assessments now factor in local crime rates, weather patterns, and infrastructure quality more precisely than ever before.

These broad market forces affect every driver, but your personal circumstances play an equally important role in determining your specific premium increases.

How Your Personal Choices Impact Your Rates

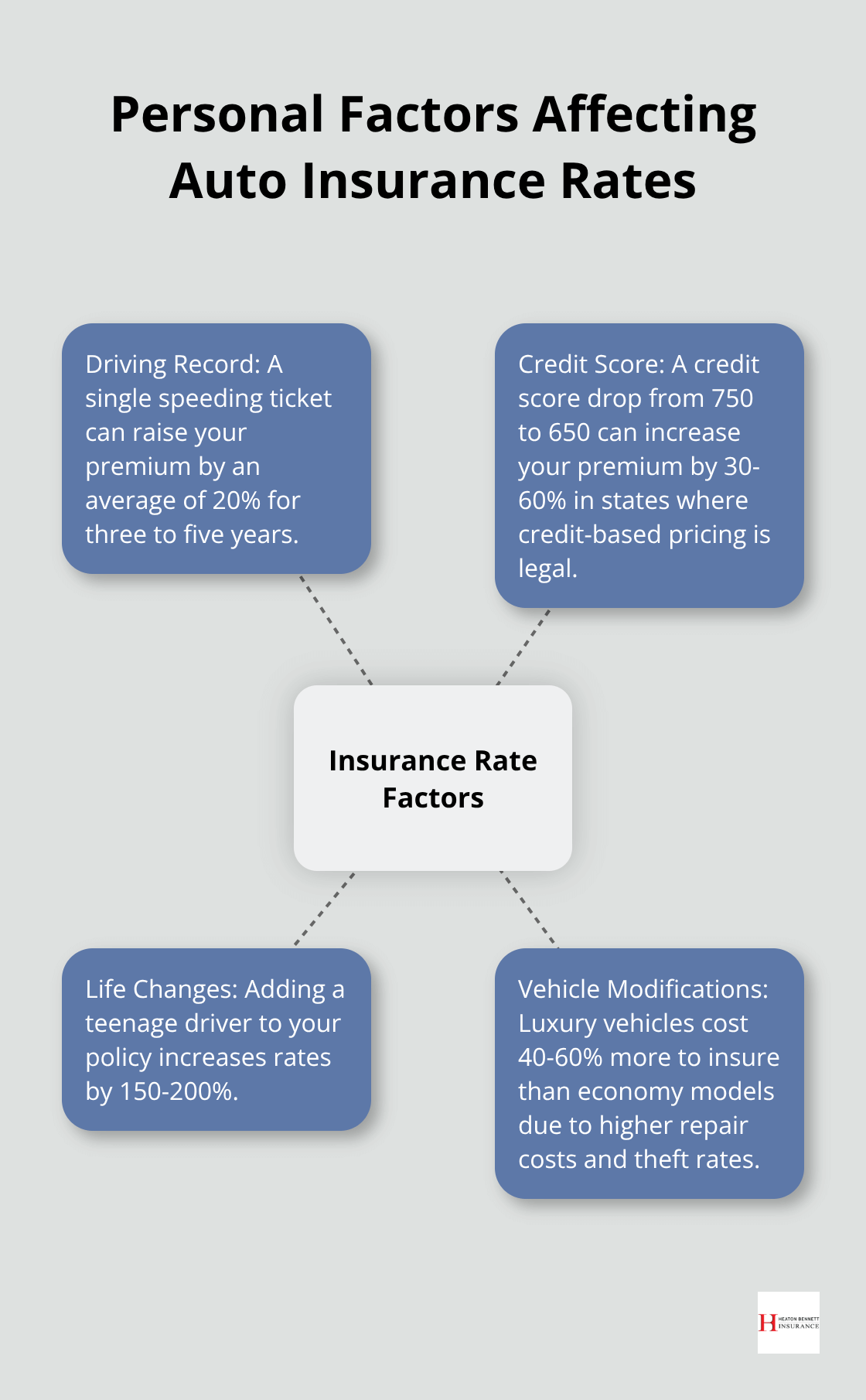

Your driving record creates a permanent trail that insurers scrutinize with mathematical precision. A single speeding ticket raises your premium by an average of 20% for three to five years, while at-fault accidents trigger increases of 40-50% according to industry data from the National Association of Insurance Commissioners. Minor claims like windshield replacements or hit-and-run incidents signal higher risk to insurers, who track your claim frequency rather than dollar amounts. Drivers who file two claims within three years face premium increases of 25-35%, regardless of fault determination.

Credit Score Changes Hit Hard

Insurance companies check your credit score at renewals because data shows drivers with lower credit scores file 40% more claims than those with excellent credit. A credit score drop from 750 to 650 can increase your premium by 30-60% in states where credit-based pricing remains legal. Late payments, maxed-out credit cards, and new debt all trigger rate increases at renewal time. Divorce, job loss, or medical debt that damages your credit score directly translates to higher auto insurance costs within six months.

Life Changes That Cost You Money

Adding a teenage driver to your policy increases rates by 150-200% because drivers under 25 cause accidents at twice the rate of experienced drivers. Moving from rural areas to cities with higher crime rates and traffic density can double your premiums overnight. Marriage typically reduces rates by 5-15% as insurers view married couples as more stable risks, while divorce reverses these savings. Retirement often increases rates despite reduced mileage because insurers classify senior drivers over 70 as higher-risk categories (with premiums rising 10-25% annually after age 75).

Vehicle Modifications and Coverage Changes

The car you drive directly affects what you pay. Luxury vehicles cost 40-60% more to insure than economy models due to higher repair costs and theft rates. Sports cars with powerful engines face surcharges of 25-50% compared to sedans. Adding comprehensive coverage to an older vehicle might seem unnecessary, but removing it can leave you vulnerable to theft or weather damage. Coverage limit changes also impact rates-increasing liability limits from state minimums to $100,000/$300,000 typically adds $200-400 annually but provides essential protection.

These personal factors interact with broader market forces that operate completely outside your control, creating a complex web of influences on your premium costs.

What Market Forces Push Your Rates Higher

Insurance companies operate on razor-thin profit margins, with the industry’s combined ratio hitting 101.3% in 2023 according to AM Best data. This means insurers paid out more in claims than they collected in premiums. When companies like State Farm report $6.7 billion in losses or Allstate posts $2.8 billion in losses, they respond by raising rates across entire regions to restore profitability. Reinsurance costs have spiked 35% since 2022 as global catastrophe losses exceeded $100 billion annually, which forces primary insurers to pass these increases directly to consumers through higher premiums.

Weather Disasters Cost Everyone More

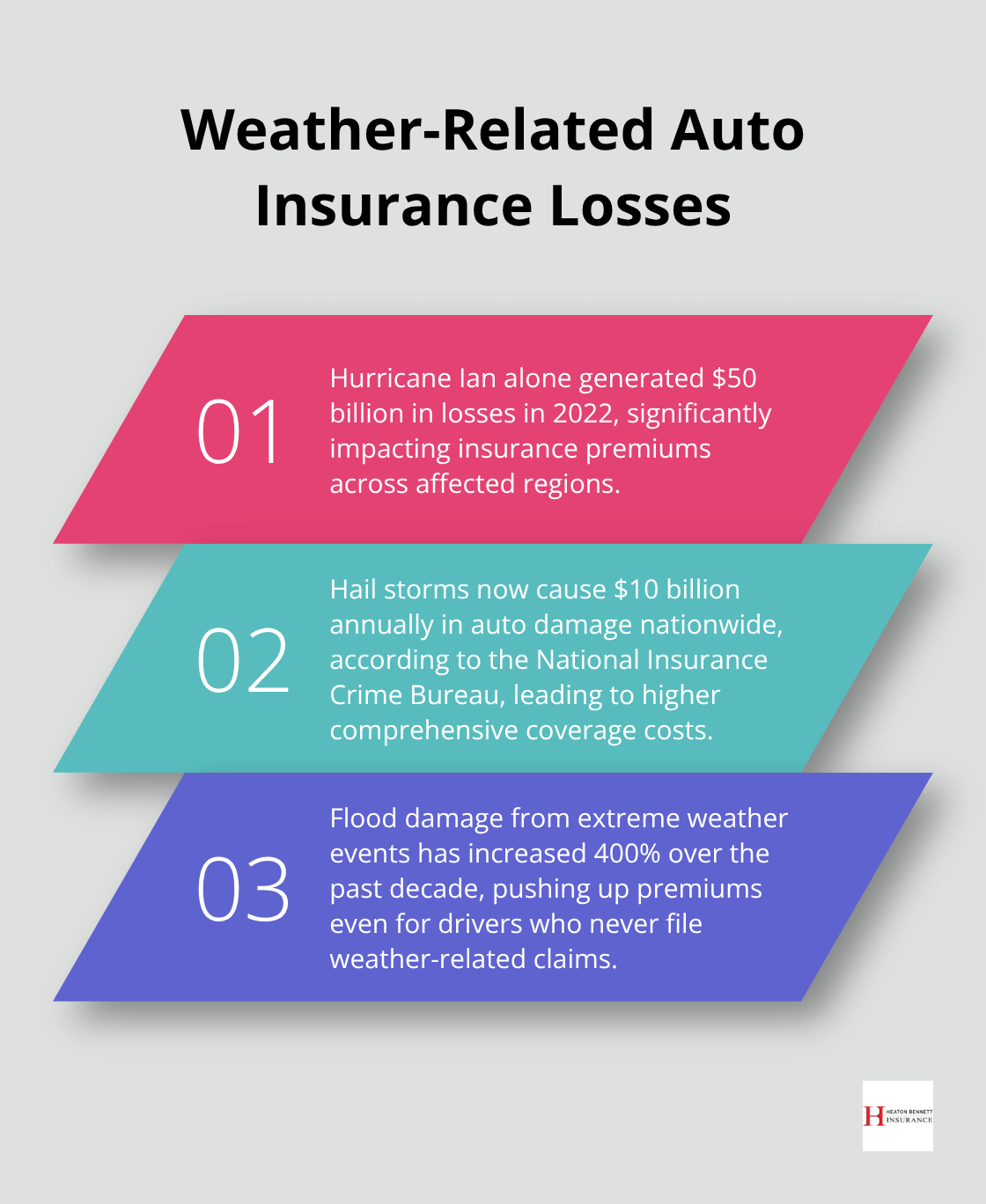

Hurricane Ian alone generated $50 billion in losses in 2022, while hail storms now cause $10 billion annually in auto damage nationwide according to the National Insurance Crime Bureau. Texas drivers face automatic rate increases after major storms regardless of personal claims because insurers spread catastrophic losses across all policyholders in high-risk zones. Wildfire-prone areas like California see 15-25% annual increases as insurers exit entire counties, which leaves companies to absorb concentrated risks. Flood damage from extreme weather events has increased 400% over the past decade (pushing comprehensive coverage costs higher even for drivers who never file weather-related claims).

State Regulations Force Rate Changes

Florida’s no-fault insurance requirements cost drivers $1,200 more annually than tort states, while Michigan’s unlimited personal injury protection mandate created the nation’s highest premiums until recent reforms. New York’s requirement for motorist coverage adds $300-500 to every policy, regardless of your record. When states modify minimum coverage requirements or eliminate credit scores for insurance, companies adjust base rates to compensate for changed risk calculations. California’s Proposition 103 requires insurers to justify rate increases publicly (creating 18-month delays that force companies to implement larger increases when finally approved).

Market Competition Affects Your Options

Insurance companies exit unprofitable markets regularly, which reduces competition and drives up rates for consumers. When major carriers like Farmers or GEICO reduce their presence in high-risk states, fewer options remain for drivers. Independent agencies like Heaton Bennett Insurance provide access to multiple carriers, which helps clients find competitive rates even when market conditions tighten. Consolidation in the insurance industry has eliminated smaller regional carriers that once offered competitive alternatives to national companies.

Final Thoughts

Auto insurance premiums rise due to complex interactions between market forces, personal factors, and industry dynamics. Repair costs climb while claim severity increases, and catastrophic weather events drive baseline rate increases that affect every driver. Your personal record, credit score changes, and life circumstances create additional premium variations that compound these broader trends.

Smart drivers take proactive steps to manage these costs. Drivers who raise deductibles from $500 to $1,000 reduce premiums by 15-20% while they maintain essential protection. Policy holders who bundle auto insurance with homeowners or renters coverage typically save 10-25% on combined premiums (and regular policy reviews help identify unnecessary coverage on older vehicles or missed discount opportunities).

Drivers must shop for better rates when their current insurer implements significant increases. Independent agencies like Heaton Bennett Insurance provide access to multiple carriers and allow you to compare options without single company restrictions. The question “why does my auto insurance go up” has multiple answers, but proactive management helps you balance cost control with adequate protection needs.