How to Choose the Best Business Medical Insurance Plan?

Selecting the right business medical insurance plans can make or break your company’s healthcare strategy. Poor choices lead to unhappy employees and budget overruns.

We at Heaton Bennett Insurance see businesses struggle with this decision daily. The good news is that with the right approach, you can find coverage that works for both your team and your bottom line.

What Insurance Plan Types Should You Consider?

Four Main Plan Types Shape Your Options

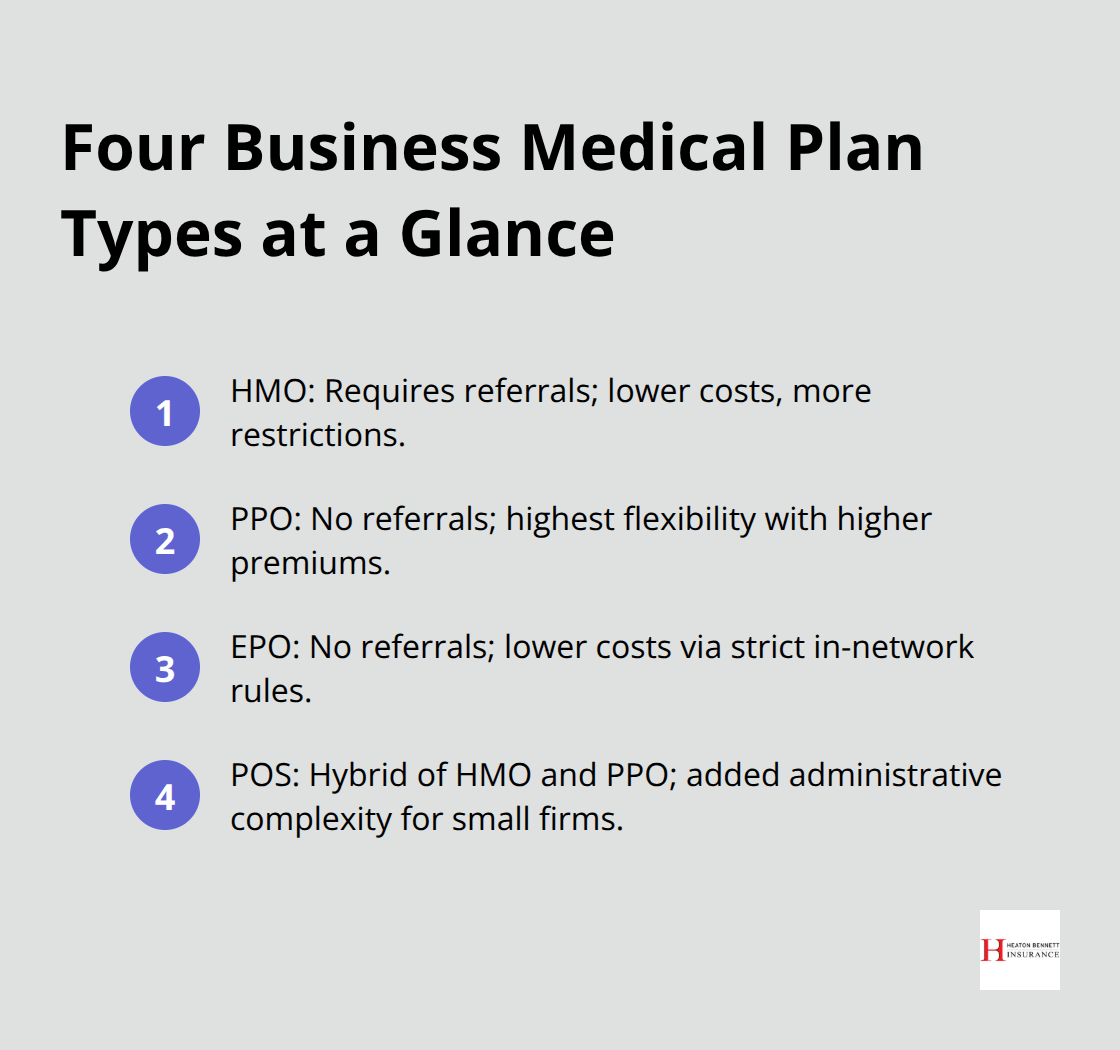

The four main business medical insurance plan types serve different business models and employee needs. Health Maintenance Organization plans cover 13% of workers according to the Kaiser Family Foundation and require referrals for specialists, which makes them cost-effective but restrictive. Preferred Provider Organization plans offer maximum flexibility without referrals but cost significantly more, with average employer contributions reaching $7,729 annually compared to $6,644 for HMOs.

Exclusive Provider Organization plans eliminate referral requirements while they maintain lower costs through strict network limitations. Point of Service plans blend HMO and PPO features but create administrative complexity that most small businesses avoid.

Coverage Components That Drive Real Value

Small businesses must prioritize specific coverage elements over flashy add-ons. Preventive care benefits generate measurable returns through reduced long-term costs and healthier workforces. Mental health coverage has become non-negotiable as telehealth services address provider network limitations effectively. Prescription drug benefits vary dramatically between carriers, with formulary restrictions that affect employee satisfaction more than premium differences. The average deductible for single coverage reached $1,787 in 2024 (making out-of-pocket maximums a critical protection for employees who earn modest wages).

Compliance Requirements You Cannot Ignore

The Affordable Care Act mandates that businesses with over 50 full-time employees provide minimum essential coverage or face penalties in 2025. Small employers with fewer than 50 employees avoid these mandates but miss tax credit opportunities worth up to 50% of premiums through the Small Business Health Options Program marketplace. Employers typically must contribute at least 50% of employee premiums to maintain group coverage eligibility. The No Surprises Act adds transparency requirements that affect plan administration costs and employee protection standards.

Once you understand these plan fundamentals and compliance requirements, you need to evaluate how they align with your specific business circumstances and workforce demographics.

How Do You Match Insurance Plans to Your Workforce

Start With Hard Numbers About Your Team

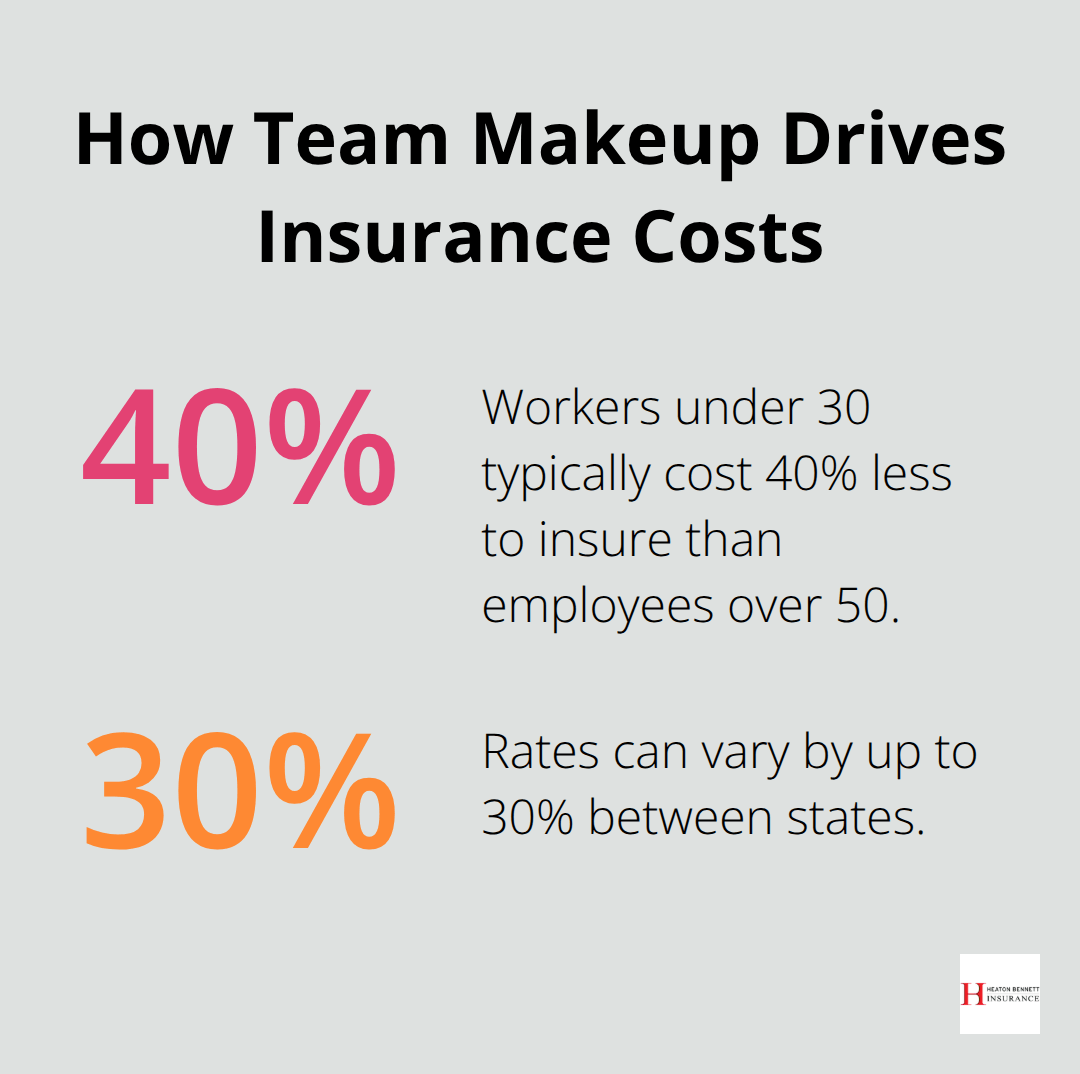

Employee demographics drive insurance costs more than any marketing brochure suggests. Workers under 30 typically cost 40% less to insure than employees over 50, while family coverage averages $25,572 annually compared to $8,951 for single coverage according to the Kaiser Family Foundation. Geographic location affects rates by up to 30% between states (which makes your Austin headquarters advantageous compared to high-cost markets like New York or California).

Track your current workforce composition: age ranges, family status, and chronic conditions through anonymous health risk assessments. Companies with predominantly younger, single employees should prioritize lower-premium, higher-deductible plans, while businesses with older workers or families need comprehensive coverage despite higher costs.

Budget Reality Beats Wishful Thoughts

Small businesses spend an average of $612 per employee monthly on health insurance, but this figure misleads without context about your specific situation. Employers must contribute at least 50% of employee premiums to maintain group eligibility, which means a 10-employee company faces minimum monthly costs of $3,060 for basic coverage. Premium increases average 5-8% annually and require budget plans that account for compound growth over three-year periods. The Small Business Health Care Tax Credit reduces costs by up to 50% for eligible employers with fewer than 25 full-time employees and average wages below $64,000 (which makes SHOP marketplace enrollment financially advantageous despite administrative complexity). Calculate total cost of ownership and include administrative time, broker fees, and employee turnover costs from inadequate coverage.

Network Strength Determines Employee Satisfaction

Provider networks vary dramatically between carriers, with narrow networks that reduce costs by 15-20% while potentially create access problems that drive employee complaints. Verify that your employees’ current doctors participate in prospective plan networks, as forced provider changes generate more dissatisfaction than premium increases. The National Committee for Quality Assurance rates health plans on network adequacy and clinical quality and provides objective comparisons beyond premium costs. Regional carriers often provide superior local networks compared to national insurers, particularly in specialized markets like Austin where local hospital systems maintain preferred relationships with specific carriers.

These workforce and budget assessments set the foundation for evaluating specific plan features that will make or break your employees’ healthcare experience.

What Plan Features Matter Most for Your Business

Premium Costs Hide the Real Financial Picture

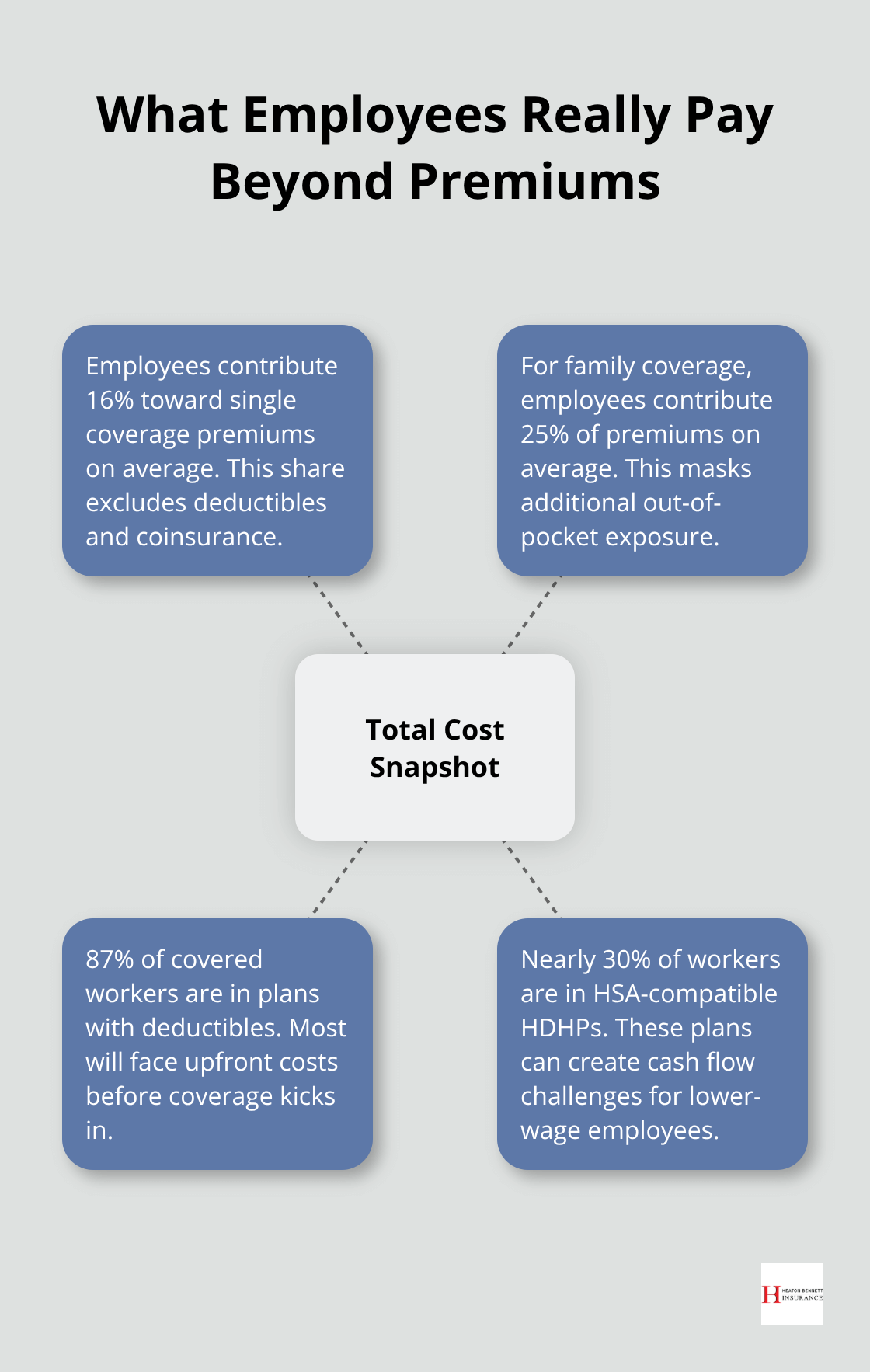

Premium costs represent only 60-70% of your total healthcare expenses, while out-of-pocket costs devastate employee budgets and drive turnover. Workers contribute an average of 16% toward single coverage premiums and 25% for family coverage according to the Kaiser Family Foundation, but these percentages mislead because they ignore deductibles and coinsurance. Lower-wage workers spend nearly 10% of their income on premiums and out-of-pocket costs combined, which makes high-premium, low-deductible plans more valuable than spreadsheet calculations suggest. The average deductible reached $1,787 for single coverage in 2024, with 87% of covered workers enrolled in plans that require deductibles.

High-deductible health plans paired with Health Savings Accounts cover almost 30% of workers but create cash flow problems for employees who earn under $50,000 annually and cannot afford upfront medical expenses.

Network Quality Trumps Premium Savings Every Time

Provider networks determine whether your insurance investment delivers actual healthcare access or expensive frustration. Narrow networks reduce premiums by 15-20% but force employees to change doctors, travel longer distances, or pay out-of-network penalties that exceed premium savings. The National Committee for Quality Assurance rates network adequacy based on appointment availability and geographic access (with top-rated networks that show 90% specialist availability within 30 days compared to 60% for bottom-tier networks). Regional carriers often provide superior local networks in Austin compared to national insurers, particularly for specialized services like cardiology and orthopedics. Verify that major local hospital systems like Dell Seton Medical Center and St. David’s participate in your prospective plan networks, as emergency care costs skyrocket when employees use out-of-network facilities during medical crises.

Deductible Structures Impact Employee Financial Health

Deductible amounts directly affect whether employees seek necessary medical care or delay treatment due to cost concerns. Plans with deductibles above $2,000 for single coverage create barriers that lead to postponed preventive care and emergency room visits for routine problems. Family deductibles often reach $4,000-6,000 annually (which represents 10-15% of median household income for many employees). Health Savings Account eligibility requires minimum deductibles of $1,600 for individuals and $3,200 for families in 2024, but these thresholds exceed what most workers can comfortably afford without financial stress. Consider how employee demographics affect deductible timing and cash flow, as January medical expenses hit hardest when holiday spending has depleted savings accounts.

Final Thoughts

Business medical insurance plans demand careful evaluation of premium costs, network quality, and employee demographics. The data reveals that premium savings become meaningless when employees cannot access their doctors or afford deductibles above $2,000 annually. Companies with younger workforces can explore higher-deductible options, while businesses with older employees need comprehensive coverage despite higher costs.

Provider network strength matters more than premium differences in most cases. Narrow networks save 15-20% on premiums but create access problems that drive employee dissatisfaction and turnover. The average small business spends $612 per employee monthly on health insurance, yet total healthcare costs include deductibles and out-of-pocket expenses that affect employee financial stability (and ultimately impact your bottom line through reduced productivity).

Quality coverage reduces turnover costs and improves productivity through better employee health outcomes. The Small Business Health Care Tax Credit can reduce premiums by up to 50% for eligible employers through the SHOP marketplace. We at Heaton Bennett Insurance help Austin businesses navigate these decisions through our independent agency approach, which provides access to multiple carriers and personalized coverage solutions that match your workforce needs and budget requirements.