Tiny Home Insurance Cost What to Expect

Tiny home insurance cost varies dramatically based on your home’s type, location, and coverage needs. Most owners pay between $600 to $1,800 annually, though mobile units often cost less than permanent foundations.

We at Heaton Bennett Insurance see many tiny home owners surprised by pricing differences compared to traditional homeowners policies. Understanding these costs upfront helps you budget effectively and find the right protection for your unique living situation.

How Much Do Tiny Homes Actually Cost to Insure

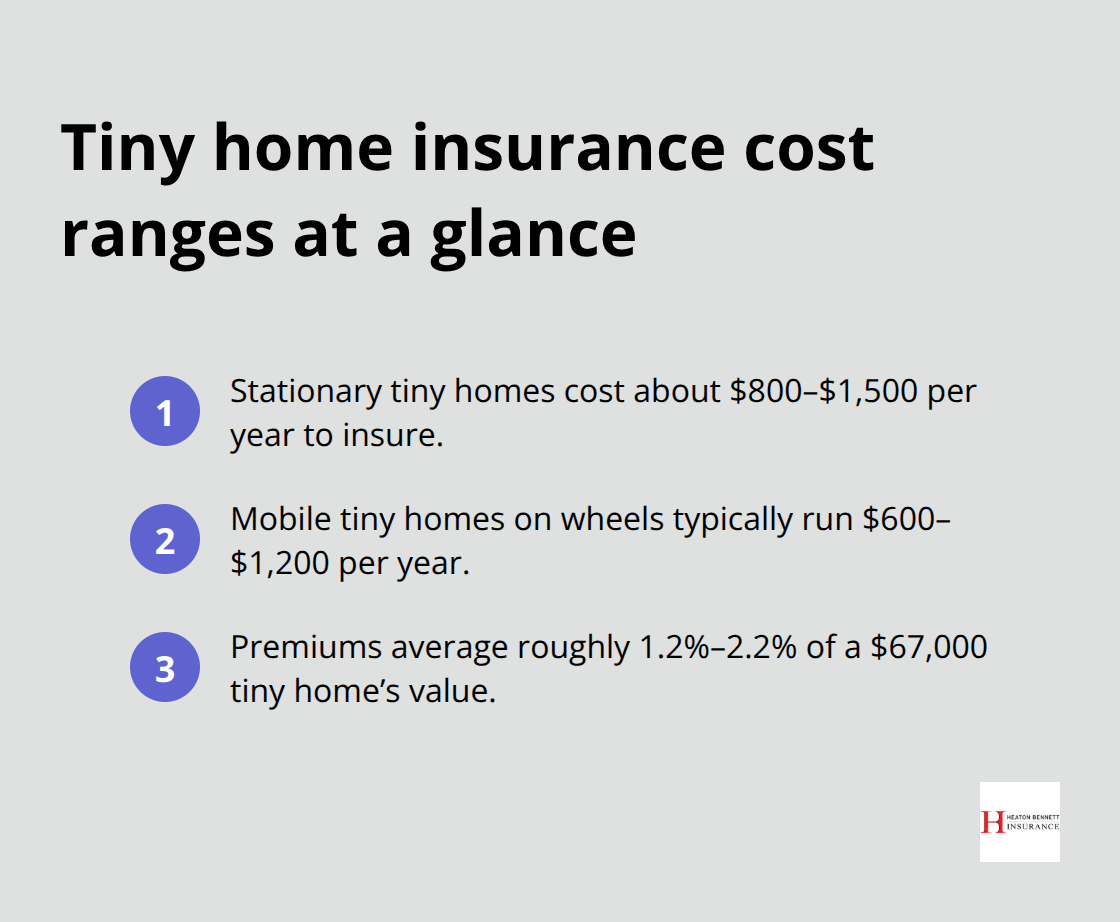

Stationary tiny homes on permanent foundations cost $800 to $1,500 annually to insure, while mobile tiny homes on wheels range from $600 to $1,200 per year. Factory-built certified tiny homes command lower premiums than DIY builds, with Progressive and Foremost Insurance offering competitive rates for NOAH-certified structures. RubyHome Real Estate data shows the average tiny home value reached $67,000 in 2024, making insurance premiums roughly 1.2% to 2.2% of home value.

Premium Differences Between Mobile and Stationary Units

Mobile tiny homes face higher transit risks but benefit from RV-style coverage options that cost significantly less than traditional homeowners policies. Stationary units require manufactured home insurance, which averages $1,200 annually compared to the $1,687 national average for standard homeowners coverage (according to 2024 industry data). Mobile units often qualify for specialized RV insurance that provides adequate protection at lower costs.

Regional Cost Variations Impact Your Budget

Southern states with hurricane exposure and western fire-prone areas drive premiums up substantially. Florida tiny home owners often pay double the national average, while Midwest locations like Ohio and Indiana offer the lowest rates. Texas and California tiny home owners pay 20-30% more than national averages due to weather risks and higher property values, while states like Montana and Wyoming offer premiums as low as $500 annually for basic coverage.

Insurance Provider Options Shape Your Costs

Strategic Insurance and American Modern Insurance provide state-specific rates that reflect local risk factors. Progressive requires factory construction and NOAH certification but offers competitive premiums for qualified homes. The Hartford provides builder’s risk insurance during construction phases, which protects your investment before standard coverage takes effect.

These cost factors directly connect to the specific elements that insurance companies evaluate when they calculate your premium, which we’ll examine next.

What Drives Your Tiny Home Insurance Premium

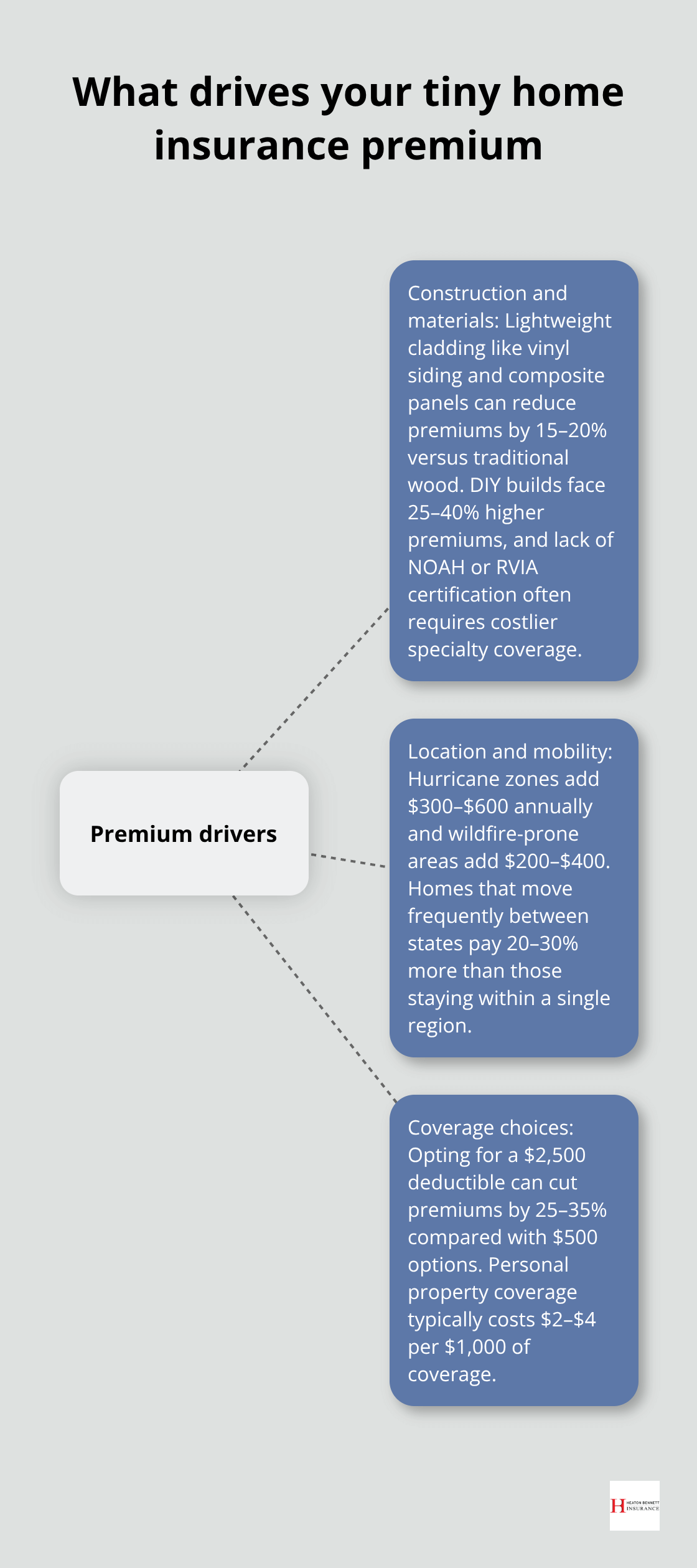

Insurance companies evaluate three primary factors when they calculate your tiny home premium. Construction materials create the biggest price variations, with lightweight materials like vinyl siding and composite panels reducing premiums by 15-20% compared to traditional wood construction. Steel framing increases costs due to higher replacement values. DIY builds face premium increases of 25-40% over factory-constructed homes because insurers view them as higher risk.

Homes that lack NOAH or RVIA certification often require specialty coverage that costs significantly more than standard policies.

Location Determines Base Risk Assessment

Weather exposure drives the most dramatic premium differences. Hurricane zones add $300-600 annually to base rates, while wildfire-prone areas increase costs by $200-400 per year. Mobile tiny homes face additional complexity because insurers evaluate both your primary parking location and travel patterns. Homes that move frequently between states pay 20-30% higher premiums than those that stay within single regions.

Zoning compliance affects rates substantially. Homes that violate local codes often require non-standard coverage that costs double traditional rates. Urban locations with better fire protection services reduce premiums by 10-15% compared to rural areas that lack professional fire departments.

Coverage Choices Control Your Final Premium

Deductible selection creates immediate cost impact. $2,500 deductibles reduce premiums by 25-35% compared to $500 deductibles, though this strategy only works if you maintain adequate emergency funds. Dwelling coverage limits should reflect your home’s actual replacement cost (underinsuring saves money upfront but creates devastating gaps during claims, while overinsuring wastes premium dollars without added protection).

Personal property coverage typically costs $2-4 per $1,000 of coverage. This makes it affordable protection that most owners should maximize rather than minimize to save small amounts.

Construction Quality Impacts Long-term Costs

Factory-built homes with proper certification consistently receive better rates than custom builds. Progressive and other major carriers prefer NOAH-certified structures because they meet standardized safety requirements. Homes built to NFPA 1192 or ANSI 119.5 standards qualify for preferred rates that can save hundreds annually.

These premium factors work together to create your final insurance cost, but smart owners can implement specific strategies to reduce these expenses significantly.

How to Cut Your Tiny Home Insurance Costs

Insurance companies reward customers who bundle multiple policies together, and tiny home owners can save 10-25% when they combine their coverage with auto, motorcycle, or other property insurance. Progressive offers the deepest discounts for customers who bundle tiny home coverage with their auto policies, often reducing total premiums by $150-300 annually. Independent agencies provide access to competitive rates from multiple insurers rather than limiting options to a single company, which allows clients to stack multiple discounts across carrier networks.

Security Features Deliver Immediate Premium Reductions

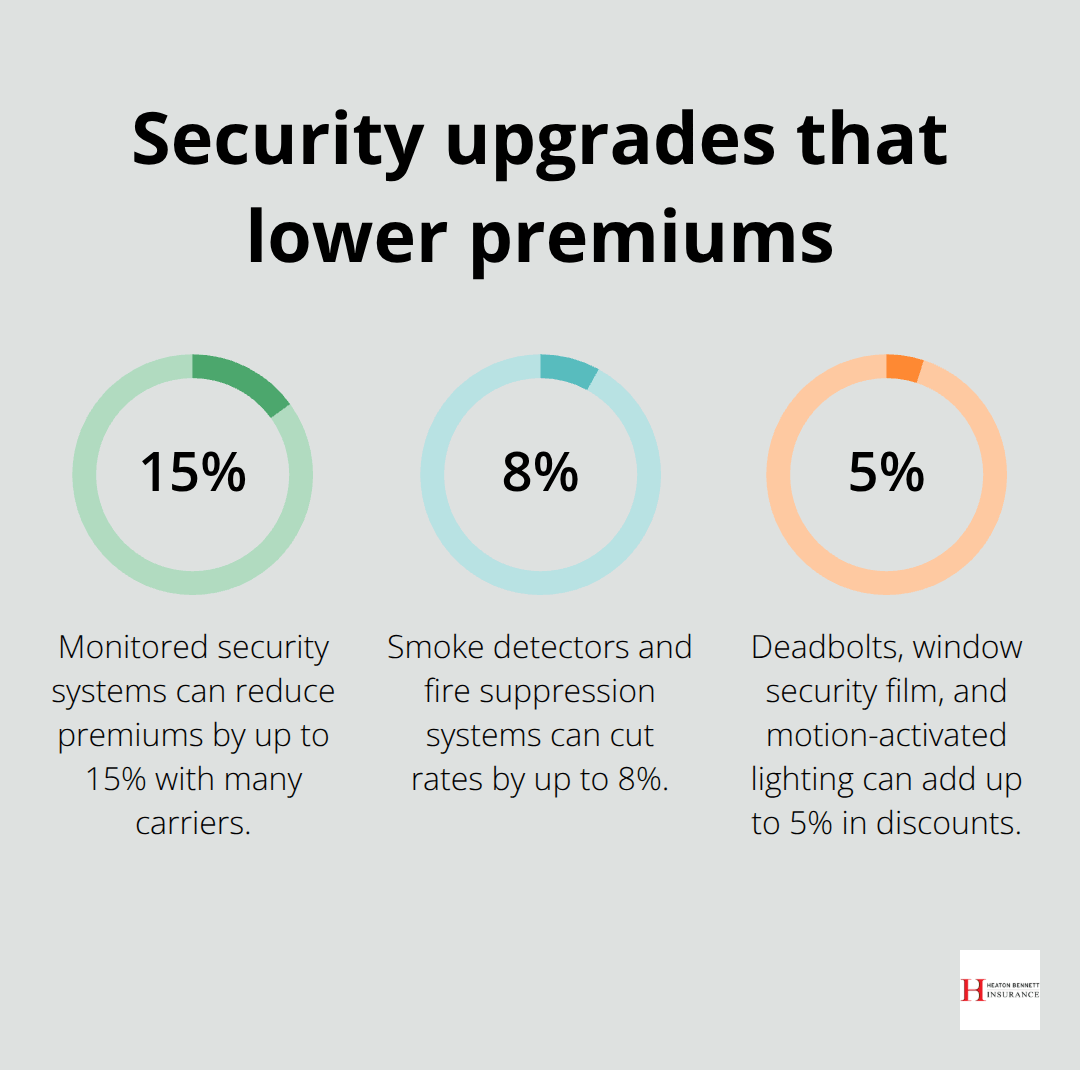

Monitored security systems reduce premiums by 5-15% with most carriers, while smoke detectors and fire suppression systems cut rates by another 3-8%. Strategic Insurance specifically rewards tiny homes equipped with cellular monitoring systems because remote locations often lack reliable landline connections. Deadbolt locks, window security film, and motion-activated lighting create additional 2-5% discounts that compound over time.

Hard-wired smoke detectors perform better than battery-operated units for insurance discounts, and professionally monitored systems outperform self-monitored alternatives.

Smart Deductible Strategies Maximize Savings

Higher deductibles instead of $500 options reduce annual premiums by 25-35%, saving most owners $200-400 yearly. This strategy works best when you maintain emergency funds equal to your deductible amount in easily accessible accounts (most financial experts recommend three months of expenses). Foremost Insurance offers the most competitive rates for higher deductible policies, particularly for mobile tiny homes. Coverage limits should match your actual replacement costs rather than arbitrary round numbers – a $45,000 tiny home insured for $60,000 wastes premium dollars without providing meaningful protection, while underinsurance creates catastrophic gaps during total loss claims.

Professional Installation Reduces Risk Premiums

Certified electricians and plumbers who install tiny home systems help qualify for preferred rates with major carriers. Homes that meet NFPA 1192 or ANSI 119.5 standards receive automatic discounts because these codes reduce fire and structural risks. Professional installation documentation proves compliance during underwriting reviews, which often results in 5-10% premium reductions compared to DIY installations.

Final Thoughts

Tiny home insurance cost typically ranges from $600 to $1,800 annually, with mobile units generally costing less than stationary homes on permanent foundations. Factory-built certified homes receive better rates than DIY builds, while location factors like hurricane zones or wildfire areas can increase premiums by $200-600 yearly. Smart strategies significantly reduce your insurance expenses through bundled policies, security systems, and higher deductibles.

Multiple carriers offer different coverage options since requirements vary dramatically between providers. Progressive prefers factory-built homes, while Strategic Insurance covers non-certified builds. Independent agencies provide access to competitive rates from multiple insurers rather than single company limitations (which often results in better coverage matches for unique tiny home situations).

We at Heaton Bennett Insurance help tiny home owners navigate these complex coverage decisions. Our independent agency status provides access to multiple carriers, allowing us to find tailored insurance solutions that match your specific tiny home situation. Contact us today to explore your coverage options and get personalized quotes for your unique living arrangement.