Contractor Liability Insurance Texas: What Builders Should Know

Running a construction business in Texas means managing serious liability risks every single day. One accident on a job site can cost you thousands in medical bills, property damage, or legal fees-money that could shut down your operation.

Contractor liability insurance in Texas isn’t optional if you want to protect your business. We at Heaton Bennett Insurance help builders understand exactly what coverage they need and why it matters.

What Contractor Liability Insurance Covers

The Foundation of Your Protection

Contractor liability insurance protects your business from the financial fallout of accidents, injuries, and damage that occur on job sites. When a worker gets hurt, a client’s property sustains damage, or someone files a lawsuit against you, this coverage pays medical bills, repair costs, and legal defense fees. Without it, you face personal responsibility for these expenses, which can drain your business bank account faster than a major project delay. In Texas, more than 80 percent of clients require proof of liability insurance before they hire you, making this coverage essential just to bid on most projects.

What the Policy Actually Covers

The policy covers bodily injury claims when someone gets hurt because of your work, property damage when you accidentally damage a client’s building or belongings, and third-party liability when someone sues you for negligence. General liability forms the foundation, but your specific trade may require additional protection. Professional liability applies if you offer design or consulting services, workers’ compensation covers employee injuries, and specialized coverage like pollution liability protects you on environmental work.

The Real Cost of Going Uninsured

Texas doesn’t legally mandate contractor liability insurance for all businesses, but the market does. A lawsuit in construction costs anywhere from $54,000 to $91,000 depending on complexity, and that’s before any settlement or judgment. A single on-site injury claim or property damage incident triggers medical costs, legal defense fees, and potential settlements that would devastate an uninsured operation.

Premium Costs and What Influences Them

The average annual premium for a Texas contractor with $1 million in coverage runs about $500 to $1,500, influenced by your trade, project size, claims history, and safety practices. This cost varies significantly based on risk-an electrician’s premium differs from a roofer’s. Your certificate of insurance becomes your proof of protection when clients demand it before work starts, and having it ready means faster approvals and stronger client relationships.

Finding the Right Coverage for Your Business

Identifying the right coverage limits and types based on your specific work helps you avoid both underinsurance and overpaying for coverage you don’t need. The next section examines the specific types of coverage every Texas contractor should consider, from general liability to workers’ compensation and specialized protections that match your trade.

Types of Coverage Every Texas Contractor Needs

General Liability: Your First Line of Defense

General liability forms the foundation of contractor protection, but it covers only third-party bodily injury and property damage claims. When a client’s employee trips over your equipment and breaks an arm, or you accidentally damage their building, general liability pays medical costs and legal fees. However, this policy does not cover your own employees-that responsibility falls to workers’ compensation. Understanding this distinction prevents costly coverage gaps that leave your operation exposed.

Workers’ Compensation: Protecting Your Crew and Your Business

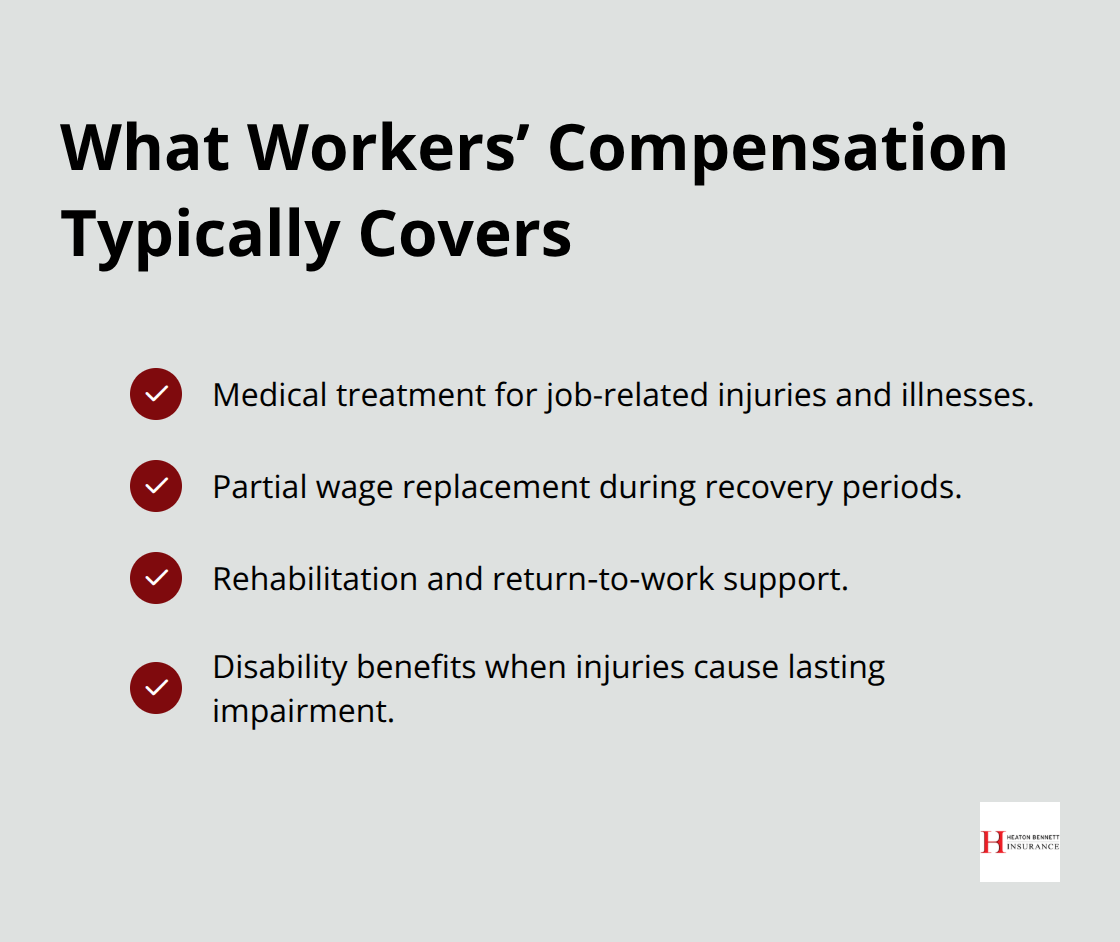

In Texas, workers’ compensation is mandatory for most contractors with employees. It covers medical treatment, lost wages, rehabilitation, and disability benefits when your crew gets hurt on the job. OSHA reports that roughly one in ten construction workers sustain injuries annually, making this coverage non-negotiable if you have staff.

The cost varies by trade and payroll, but it protects both your employees and your business from lawsuits that could otherwise drain your finances.

Tools and Equipment Coverage: Safeguarding Your Investment

Tools and equipment coverage protects your investment in job site gear against theft, vandalism, and weather damage. A single incident on the job site can wipe out thousands in tools before you finish a project. Many contractors absorb these losses personally, which eats into profit margins faster than project delays. This coverage prevents that drain on your bottom line.

Matching Coverage to Your Specific Trade

An electrician’s risk profile differs sharply from a roofer’s, and your premium reflects that reality. Electrical work carries higher professional liability exposure if you design systems, while roofing faces severe weather and fall risks that drive higher general liability costs. Start by documenting exactly what work you perform, what equipment you own, and how many employees you have. Then discuss these specifics with an insurance professional who understands Texas contractor risks. Request a detailed quote that breaks down each coverage type and shows how premiums reflect your specific trade and claims history. This transparency helps you understand what you’re buying and why each component matters to your operation.

The right coverage stack protects your operation without overpaying for unnecessary limits. Once you understand what each policy covers, the next step involves recognizing which claims actually trigger your protection and how that coverage responds when accidents happen on your job sites.

Common Claims and How Contractor Liability Insurance Protects You

Construction claims test your coverage in unpredictable ways. A worker steps on a nail and needs emergency surgery. A contractor accidentally damages electrical wiring in a client’s building during renovation. A third party sues because they claim your crew caused an injury weeks after work finished.

These situations reveal whether your insurance truly protects your operation or leaves you exposed. Contractor liability insurance responds differently depending on the claim type, the coverage you carry, and the specific circumstances on the job site. Understanding how your policy responds to real situations prevents nasty surprises when you need protection most.

Property Damage Claims on Job Sites

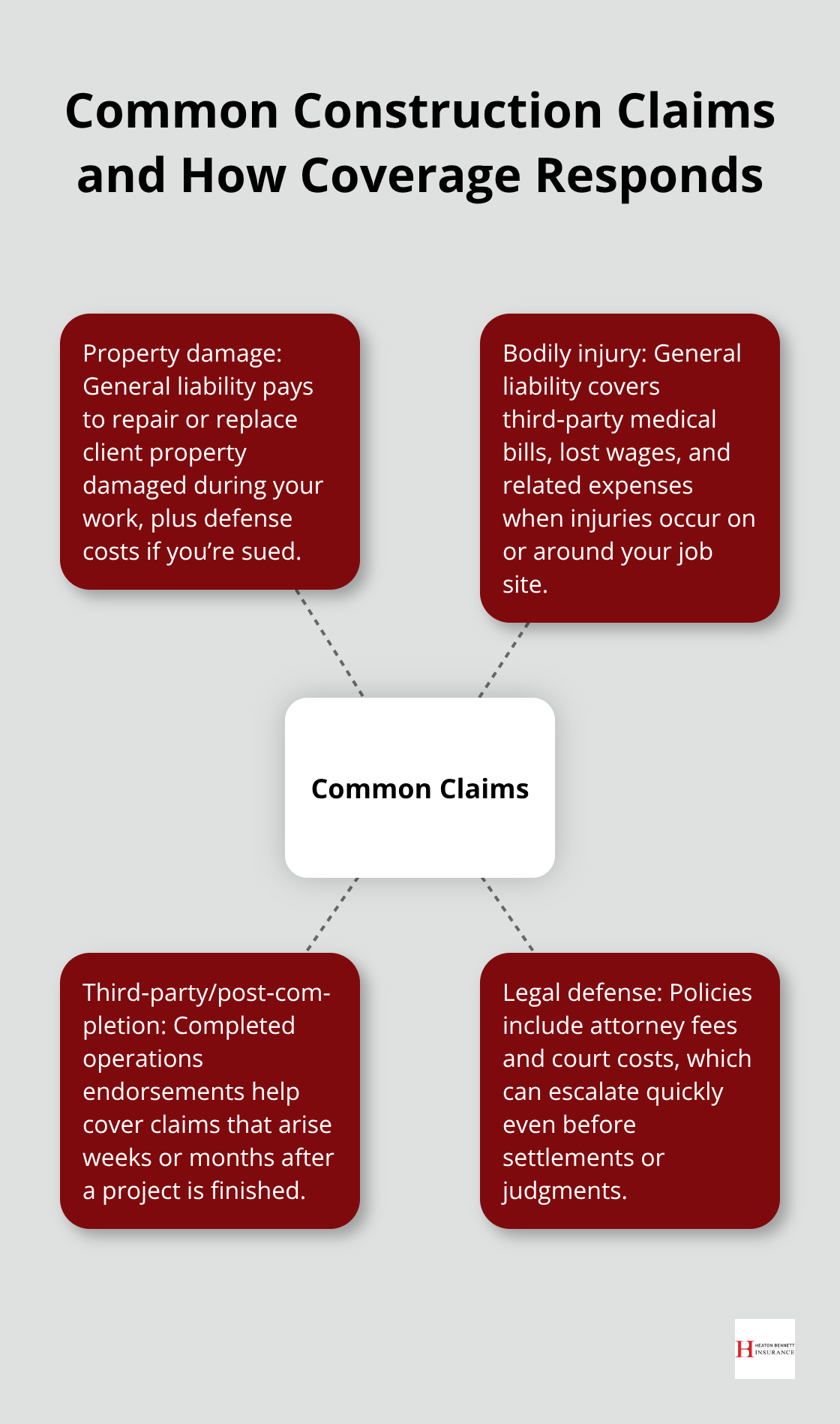

Property damage claims represent the most frequent liability exposure for Texas contractors. When you accidentally damage a client’s building, equipment, or belongings during work, general liability covers the repair costs and legal defense fees. A roofer installs new shingles and punctures the client’s HVAC unit below. A plumber cuts into drywall and hits copper piping. A painter spills materials on expensive flooring. These incidents trigger property damage claims that general liability covers. The policy pays to repair or replace the damaged property, plus your legal defense costs if the client sues. Without this coverage, you absorb the full cost yourself.

Bodily Injury Claims and Medical Expenses

Bodily injury claims follow a similar pattern but carry higher financial exposure. OSHA data shows roughly one in ten construction workers sustain injuries annually across the industry, but third-party injuries on your job sites create liability exposure beyond your crew. A client’s employee trips over your equipment and fractures their leg. A homeowner gets burned by hot materials your crew left unattended. A neighbor gets injured by debris from your work site. General liability covers medical treatment, emergency care, lost wages, rehabilitation costs, and legal settlements or judgments. These claims often exceed $10,000 quickly once hospital bills and lost income accumulate.

Third-Party Liability and Post-Completion Exposure

Third-party liability scenarios create the most unpredictable claims because they involve people outside your direct control and often surface months or years after work finishes. A client claims your electrical work created a fire hazard that caused property damage weeks later. A neighboring business sues because your crew damaged their building during construction. A homeowner discovers structural defects in work you completed and claims negligence. These claims test whether your coverage extends to post-completion exposure. General liability covers some post-completion claims, but completed operations endorsements strengthen this protection by explicitly covering claims that arise after you finish a project. Without this endorsement, your coverage may exclude the exact scenario that causes the largest loss.

Final Thoughts

Contractor liability insurance in Texas protects your business from the financial devastation that follows accidents, injuries, and property damage on job sites. The coverage you carry determines whether a single claim drains your bank account or gets handled by your insurer, and more than 80 percent of clients require proof of this protection before they hire you. General liability covers third-party bodily injury and property damage, workers’ compensation protects your employees, and specialized endorsements like completed operations coverage shield you from claims that surface months after work finishes.

Document your trade, the types of projects you undertake, your equipment investment, and your employee count to assess your specific risks accurately. Request detailed quotes that break down each coverage type and explain how premiums reflect your actual risk profile, then start with general liability as your foundation and add workers’ compensation if you have employees. Layer in specialized coverage that matches your trade and project scope, and keep your certificate of insurance ready to accelerate client approvals and strengthen relationships.

We at Heaton Bennett Insurance understand the unique risks Texas contractors face and work with multiple carriers to build tailored contractor liability insurance coverage that protects your operation without overpaying for unnecessary limits. Contact Heaton Bennett Insurance today to discuss your specific needs and get a quote that reflects your business.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.