Restaurant Liability Coverage: Key Protections for Foodservice

Running a restaurant means facing real liability risks every single day. From foodborne illness claims to slip-and-fall accidents, one incident can threaten your business financially.

At Heaton Bennett Insurance, we know that restaurant liability coverage isn’t optional-it’s essential protection. This guide walks you through the risks you face, what coverage actually protects you, and how to choose the right policy for your operation.

What Liability Risks Threaten Your Restaurant Most

Slip-and-Fall Injuries Lead Restaurant Claims

Slip-and-fall injuries rank as the leading cause of restaurant liability claims, according to data from Inszone Insurance. Wet floors, cluttered aisles, uneven surfaces, and poor lighting create constant hazards in front-of-house areas. A single slip-and-fall lawsuit costs $15,000 to $50,000 in legal defense alone, even if you win the case. Daily safety walks through dining areas matter far more than most restaurant owners realize. You need documented incident logs and routine maintenance schedules to show you took reasonable precautions.

Foodborne Illness Claims Surface Weeks Later

Foodborne illness claims present a different threat because they often surface weeks after a customer dines at your restaurant, making the connection harder to trace. The FDA Food Code emphasizes strict handwashing protocols and prohibits bare-hand contact with ready-to-eat foods, yet violations remain common in kitchens operating under pressure. Temperature control failures and inadequate time-temperature logs create liability exposure that extends far beyond a single meal service.

Kitchen Fires Cause Property and Income Loss

Kitchen fires represent another significant risk, with the National Fire Protection Association reporting over 7,000 restaurant fires annually. Grease buildup in hood and duct systems drives most of these fires, yet many restaurants fail to follow NFPA 96 cleaning schedules. A kitchen fire triggers both property damage claims and business interruption losses that devastate cash flow.

Third-Party Injuries Beyond Your Premises

Third-party bodily injury claims extend beyond your premises. If a delivery driver working for your restaurant causes a car accident, you face hired and non-owned auto liability exposure even if that driver uses their own vehicle. Liquor liability presents acute risk if you serve alcohol, since courts often hold establishments liable for injuries caused by visibly intoxicated patrons. A single alcohol-related claim exceeds $100,000 according to industry data, making this coverage non-negotiable if you pour drinks.

Back-of-House Injuries Affect Your Insurance Profile

Back-of-house injuries from knives, slicers, and fryers happen frequently in foodservice environments. The National Safety Council reports that workers suffer injuries on the job every 7 seconds in this sector. These employee injuries fall under workers’ compensation, not general liability, but they still represent real operational costs and claims history that insurers examine when pricing your policies. Understanding which coverages address each risk type helps you build a protection strategy that actually fits your operation.

Coverage That Actually Protects You

General Liability Forms Your Foundation

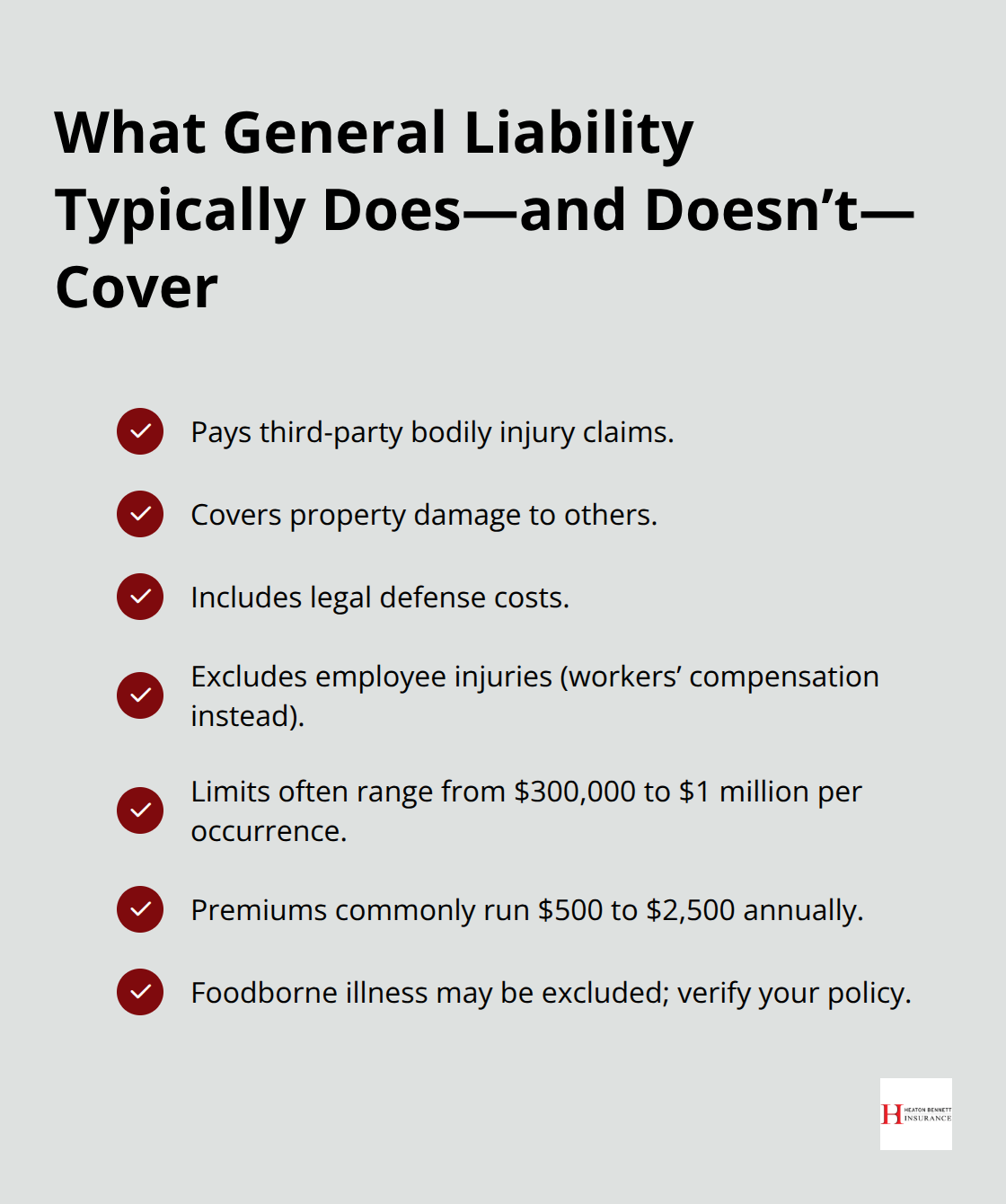

General liability insurance forms the foundation of restaurant protection, but it doesn’t cover everything you face. This coverage pays for third-party bodily injury claims like slip-and-fall medical bills and legal defense costs, plus property damage you cause to someone else’s belongings. However, general liability explicitly excludes employee injuries, which fall under workers’ compensation instead. The policy also has limits, typically ranging from $300,000 to $1 million per occurrence depending on your restaurant’s size and risk profile. Annual premiums for general liability run $500 to $2,500 based on location, square footage, and claims history. If you operate a high-traffic establishment with a bar, expect the upper end of that range. One critical point: general liability doesn’t automatically cover foodborne illness claims.

Some policies treat food poisoning as bodily injury and cover it; others exclude it entirely. You must verify this in your policy language before you need it.

Product Liability Covers Food-Related Claims

Product liability specifically covers claims arising from food you served that allegedly caused illness, including medical costs and settlements. Foodborne illness claims create extended liability exposure because illness surfaces weeks after service, expanding the window during which customers can file claims. This means a contamination event in January could trigger a lawsuit in March or April. The FDA Food Code emphasizes strict handwashing protocols and prohibits bare-hand contact with ready-to-eat foods, yet violations remain common in kitchens operating under pressure. Temperature control failures and inadequate time-temperature logs create liability exposure that extends far beyond a single meal service.

Liquor Liability Protects Against Alcohol-Related Incidents

Liquor liability insurance protects you from injuries caused by intoxicated patrons you served, and courts frequently hold establishments liable for serving visibly intoxicated customers. Annual premiums for liquor liability range from $400 to $3,000 depending on your operation’s size and alcohol volume. A single alcohol-related claim routinely exceeds $100,000 according to industry data, making this coverage absolutely essential if you pour any drinks whatsoever. If you serve alcohol at all-even beer and wine only-you need this protection in place.

Hired and Non-Owned Auto Liability Covers Delivery Risks

If you operate a delivery business or food truck, you also need hired and non-owned auto liability to cover accidents involving drivers using their personal vehicles for work. Many restaurant owners overlook this exposure entirely, assuming their general liability covers delivery accidents. It doesn’t. A delivery driver accident creates auto liability exposure that your general liability policy explicitly excludes, leaving you exposed to significant financial loss. Understanding which coverages address each risk type helps you build a protection strategy that actually fits your operation, and the next step involves assessing your specific business risks to determine which combination of policies you truly need.

Matching Coverage to Your Restaurant’s Real Risks

Document Your Actual Operation, Not Industry Averages

Start by writing down your annual revenue, square footage, number of employees, hours of operation, whether you serve alcohol, how you prepare food, and whether you deliver. This data matters because generic quotes miss the real exposures you face. A high-traffic casual restaurant with a bar faces different risks than a small takeout shop or a catering operation. Inszone Insurance’s 2025 data shows that quick-service restaurants with delivery face higher hired and non-owned auto exposure, while full-service establishments with bars show greater slip-and-fall and liquor liability claims. Your operational details drive the coverage limits you actually need.

Calculate Worst-Case Scenarios Specific to Your Business

Work backward from realistic incident scenarios rather than arbitrary industry benchmarks. If you operate a 2,000-square-foot dining room with 40 seats turning tables five times during dinner service, you face far more slip-and-fall exposure than a 500-square-foot takeout counter. A single slip-and-fall lawsuit costs $15,000 to $50,000 in legal defense alone, so starting with the industry minimum of $300,000 general liability coverage makes no sense if you run high-volume operations. What would a multi-case foodborne illness outbreak cost your business in medical claims, legal fees, and lost revenue? What if a delivery driver caused a serious injury accident? These calculations should drive your coverage limits.

Balance Deductibles Against Premium Costs

Deductibles between $1,000 and $2,500 strike the right balance between affordable premiums and manageable out-of-pocket costs when claims happen. A lower deductible reduces your financial pain during a claim but raises annual premiums significantly. A higher deductible cuts premiums but forces you to absorb more cost when incidents occur. Most restaurants should target the $1,500 to $2,000 range unless your claims history is spotless and your cash reserves are substantial.

When comparing quotes, never compare one restaurant’s premium to another’s because your risks differ fundamentally. Instead, compare quotes for your specific operation across multiple providers. Restaurant-specialist carriers like The Hartford and Berkshire Hathaway GUARD understand foodservice exposures better than generic commercial insurers and often price more competitively once they understand your actual risk profile. Ask each potential insurer for five referrals from similar restaurants and contact those references to verify their claims experience and coverage quality. This step matters more than premium shopping because a $200 annual savings means nothing if the insurer denies your claim or responds slowly when you need help.

Bundling policies into a Business Owners Policy combining general liability and property coverage can reduce costs, but verify that bundled coverage provides equivalent limits and exclusions to standalone policies. Some bundled packages reduce coverage limits to hit a lower price point, creating false savings that leave you underprotected.

Identify Exclusions and Expand Coverage With Endorsements

Read the policy exclusions section before signing anything because that’s where coverage gaps hide. Most general liability policies exclude employee injuries, which fall under workers’ compensation instead. Many policies also exclude foodborne illness claims or restrict coverage to specific circumstances. Some exclude liquor liability entirely, forcing you to purchase a separate policy. Product liability coverage might exclude claims arising from allergen contamination if you don’t document your allergen handling procedures.

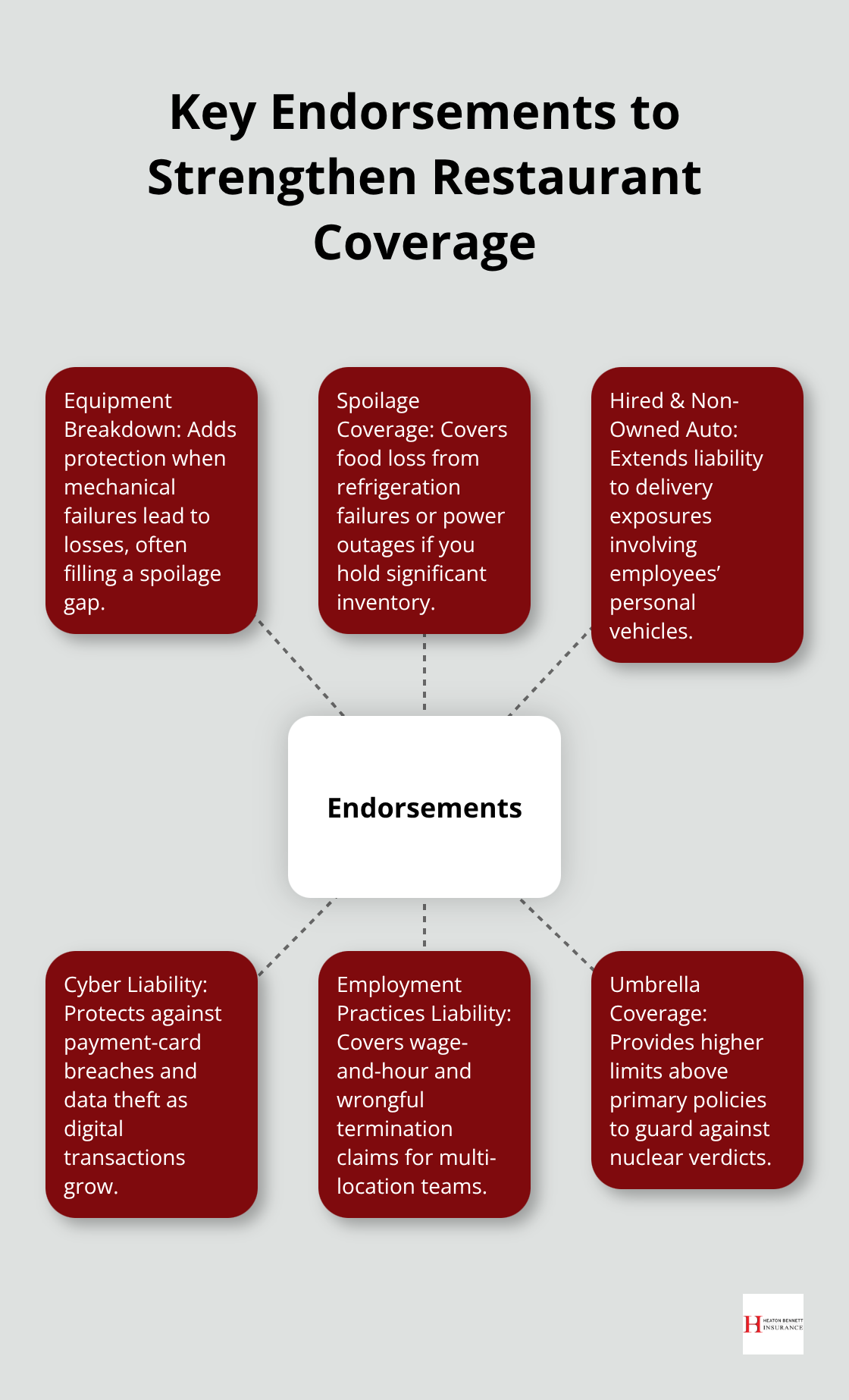

These exclusions aren’t negotiable in standard policies, but endorsements can expand coverage or reduce exclusions. If your policy excludes spoilage from equipment breakdown, an equipment breakdown endorsement adds that protection. If standard general liability excludes hired and non-owned auto coverage, you purchase that as a separate endorsement. Ask your insurer specifically what’s excluded for your operation type and what endorsements they recommend.

Spoilage coverage for refrigeration failures and power outages matters if you hold significant inventory. Cyber liability coverage protects against payment-card breaches and data theft, increasingly important as restaurants process more digital transactions. Employment practices liability coverage protects against wage-and-hour claims and wrongful termination suits, particularly relevant if you manage multiple locations. Excess liability or umbrella coverage provides protection above your primary policy limits and becomes essential if you face a nuclear verdict situation where a jury awards damages exceeding your standard limits.

The 2025 commercial insurance market shows umbrella pricing and attachment points remain elevated compared to pre-2020 norms according to Swiss Re Institute data, so securing adequate umbrella protection costs more but protects your business assets more comprehensively.

Final Thoughts

Restaurant liability coverage protects your business from the financial devastation that follows slip-and-fall injuries, foodborne illness claims, kitchen fires, and alcohol-related incidents. The coverage types we’ve outlined-general liability, product liability, liquor liability, and hired and non-owned auto protection-form a comprehensive shield against the risks that threaten restaurants daily. Without these protections in place, a single claim can drain your cash reserves, force temporary closure, or end your business entirely.

Evaluating your coverage starts with honest assessment of your operation. Document your revenue, square footage, employee count, service type, and whether you serve alcohol or deliver, then calculate realistic worst-case scenarios based on your specific business model rather than industry averages. A high-traffic bar with full-service dining faces fundamentally different exposures than a small takeout operation, and your coverage limits should reflect that reality. Try deductibles between $1,000 and $2,500 to balance affordable premiums with manageable out-of-pocket costs when claims occur.

Compare quotes from restaurant-specialist carriers across multiple providers and contact references from similar establishments to verify claims handling quality before committing to any policy. Contact Heaton Bennett Insurance to discuss your restaurant’s liability exposure and receive quotes that reflect your actual risk profile rather than industry averages.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.