Restaurant Flood Coverage: Protecting A Common Risk

Flooding poses one of the biggest threats to restaurant operations, yet many owners overlook this risk until it’s too late. Water damage can shut down your business for weeks, destroy inventory, and cost tens of thousands in repairs.

At Heaton Bennett Insurance, we’ve seen firsthand how the right restaurant flood coverage makes the difference between a temporary setback and a permanent closure. This guide walks you through what you need to know to protect your business.

Why Flooding Threatens Your Restaurant

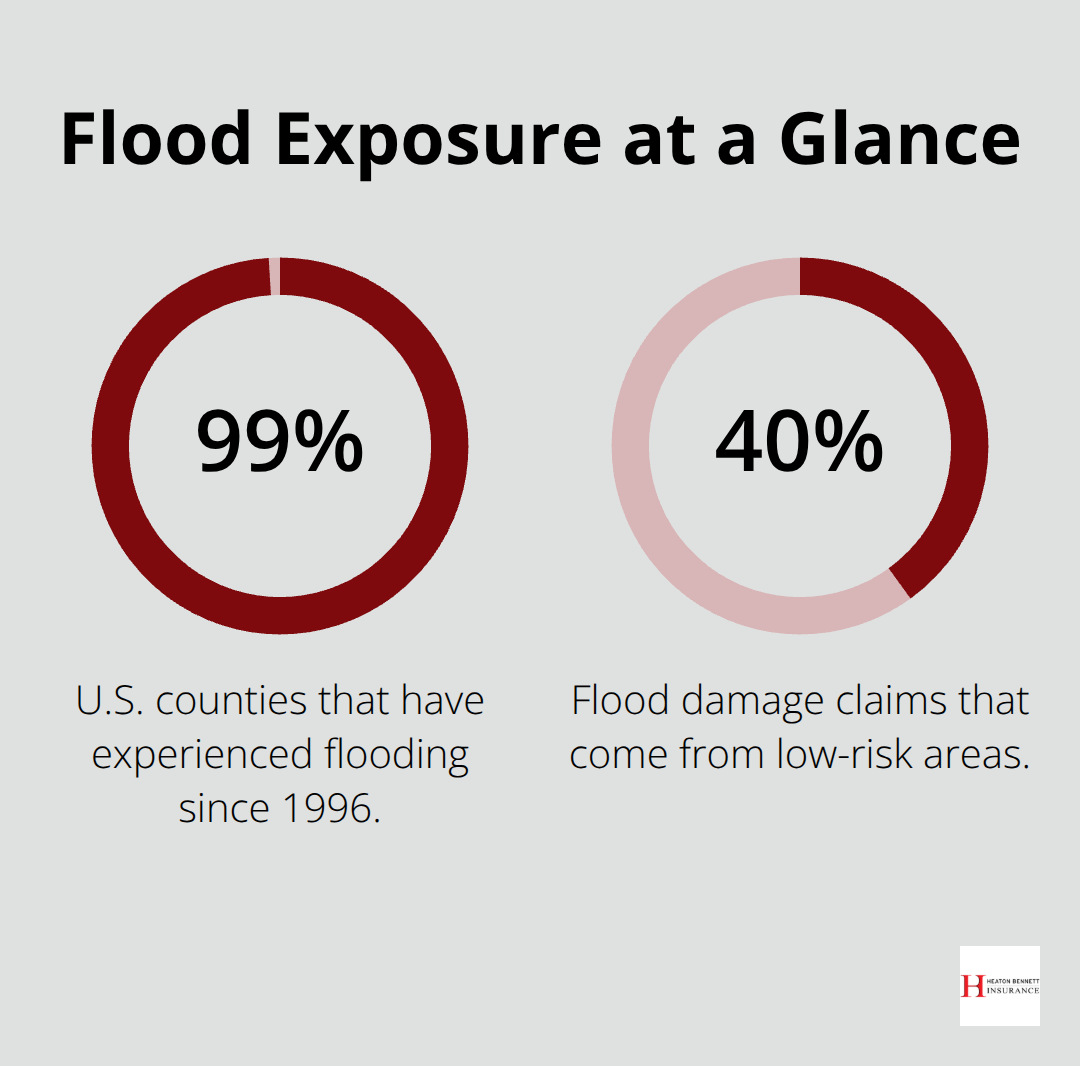

Flooding hits restaurants harder than most businesses because water damage affects every part of operations at once. Your kitchen equipment, inventory, seating areas, and structural systems all face risk simultaneously. Since 1996, floods have affected 99 percent of U.S. counties, meaning your location likely faces some level of exposure regardless of whether you sit in a designated high-risk zone. About 40 percent of flood damage claims come from low-risk areas, so complacency based on your address is dangerous. The Insurance Information Institute reports that floods are among the costliest natural disasters for U.S. businesses, with Florida small business property claims often running into the hundreds of thousands of dollars.

Multiple Entry Points Create Widespread Damage

Restaurants face vulnerability because water enters through multiple pathways. Ground-level entrances, loading docks, and drive-thru windows create direct exposure. Foundation cracks, floor drains, and basement utility areas act as entry points during heavy rainfall or storm surge. Your HVAC systems, electrical panels, and plumbing infrastructure sit in areas where water accumulates first. Walk-in coolers and freezers fail within hours of water exposure, spoiling thousands in food inventory. The longer water sits, the more damage spreads to walls, flooring, and structural components that aren’t visible immediately. Contents damage extends beyond equipment: furniture, finished goods, raw materials, and permanently installed systems all require replacement or extensive restoration.

Financial Impact Extends Far Beyond Repairs

A flooded restaurant doesn’t just lose the building for a few days. The average commercial flood claim from 2011 to 2015 ran around 90,000 dollars, but many restaurants face significantly higher losses. Business interruptions force you to discard perishable inventory, lose reservation revenue, and potentially lose customer loyalty to competitors who reopen first. Cleanup and debris removal alone can stretch into weeks, keeping your doors closed long after water recedes. Without dedicated flood insurance, you’re betting your business on whether standard commercial property coverage includes water damage-and it typically doesn’t. The recovery window directly determines whether customers return or permanently shift their dining habits elsewhere.

Why Standard Insurance Falls Short

Standard commercial property policies exclude flood damage entirely. Your general liability coverage won’t protect your building or contents from rising water. Business interruption coverage only works if your base property policy covers the initial flood loss-which it doesn’t. This gap leaves restaurant owners exposed to catastrophic financial loss. The solution requires dedicated flood insurance, which we’ll explore in the next section, along with how to assess whether your current coverage leaves you vulnerable.

What Flood Insurance Actually Covers

How Flood Insurance Defines Coverage

Your standard commercial property policy stops working the moment water rises. The National Flood Insurance Program defines a covered flood event as an excess of water on normally dry land affecting multiple properties, caused by storm surge, overflowing rivers, heavy rainfall, rapid surface water, or mudflows. This distinction matters because water damage from burst pipes or roof leaks inside your building falls under standard commercial property coverage, not flood insurance. Water entering from outside sources requires dedicated flood protection instead.

Building and Contents Protection Under NFIP

The NFIP offers up to 500,000 dollars in building coverage and 500,000 dollars in contents coverage for nonresidential properties like restaurants. Building coverage protects your structure, foundation, electrical systems, plumbing, HVAC, fire protection systems, permanently installed carpets, attached structures, windows, tanks, and pumps. Contents coverage protects furniture, equipment, seating, appliances, finished inventory, raw materials, and personal property like artwork or rugs. However, the NFIP does not cover sump pump backups, landscaped areas, septic tanks, unattached structures, or business interruption losses.

When NFIP Coverage Limits Fall Short

If your restaurant’s insurable value exceeds the NFIP caps, you need private flood insurance to cover the excess. Insurable value is calculated as the replacement cost value of your building minus the land value, which determines the minimum required coverage your lender demands. For a nonresidential building with an insurable value around 700,000 dollars and contents of 50,000 dollars, the NFIP building coverage maxes out at 500,000 dollars while contents coverage covers the full 50,000 dollars. This gap forces you to purchase additional private coverage or accept uninsured loss.

Premium Factors and Timing Considerations

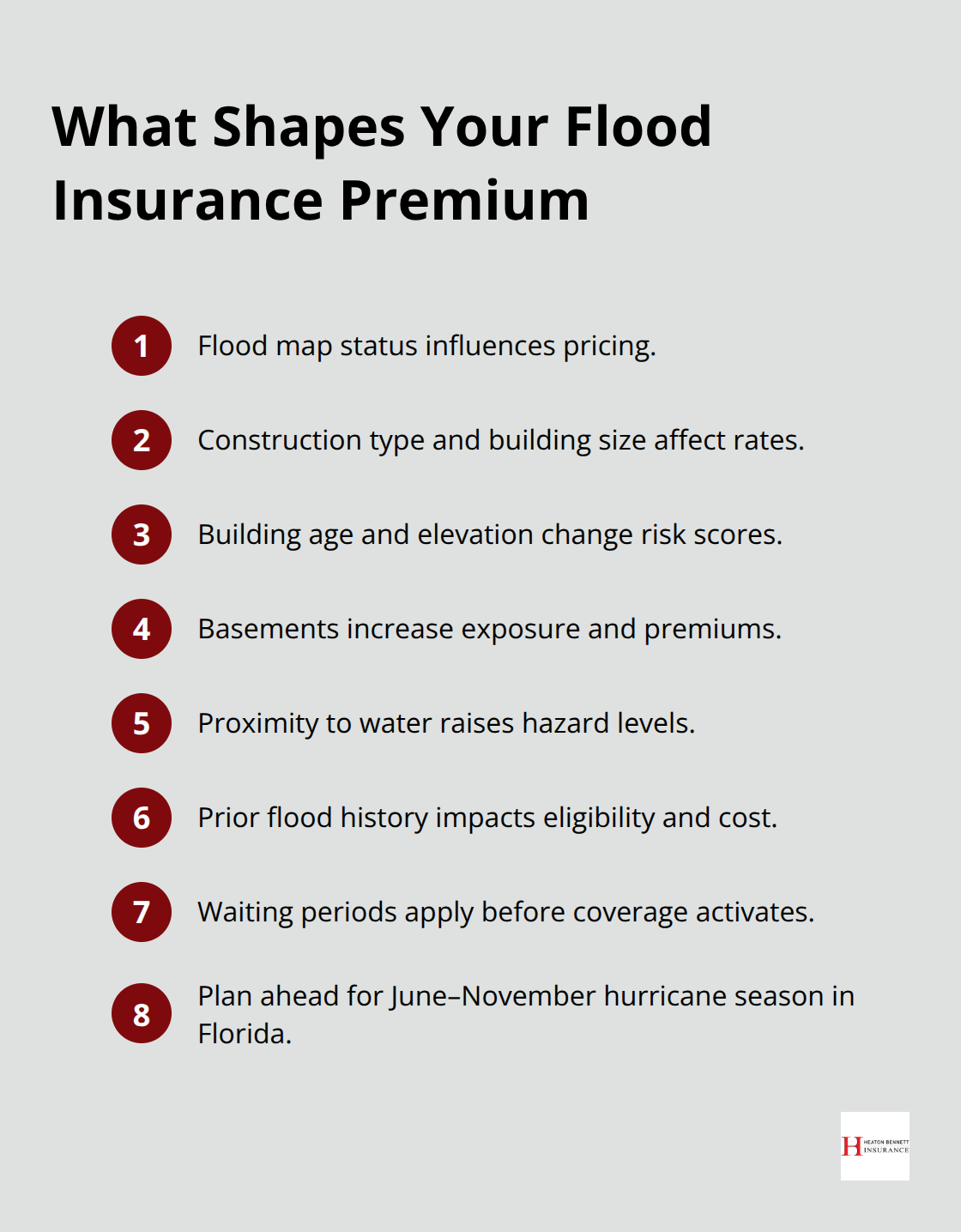

Premiums vary based on your flood map status, construction type, building size, age, elevation, basement presence, proximity to water, and prior flood history. Waiting periods typically apply before coverage activates, so purchasing flood insurance now protects you against claims filed later, not against events occurring before your policy begins. For waterfront restaurants in Florida facing hurricane season from June through November, this advance planning becomes essential to avoid coverage gaps when storms arrive. Understanding what your policy covers sets the foundation for the next critical step: evaluating your specific restaurant’s flood vulnerability and determining the right coverage limits for your operation.

How to Assess Your Restaurant’s Flood Risk

Determine Your Actual Flood Zone Status

Start by knowing your actual flood risk, not assumptions based on your address. Use FEMA’s Flood Map Service Center to enter your restaurant’s address or coordinates and determine your official flood zone designation. This takes five minutes and reveals whether your lender will require flood insurance as a loan condition. However, don’t stop there if the map shows low risk. The National Flood Insurance Program notes that 40 percent of flood damage claims originate from low-risk areas, meaning your restaurant faces exposure regardless of zone classification.

Identify Vulnerable Areas in Your Building

Next, assess your building’s specific vulnerabilities. Ground-level entrances, loading docks, and drive-thru windows create direct water entry points during heavy rainfall or storm surge. Walk-in coolers and freezers positioned at floor level or in basements fail quickly when water enters, destroying thousands in perishable inventory within hours. Check your HVAC systems, electrical panels, and utility areas for their elevation and proximity to water accumulation zones. Basements and crawlspaces amplify risk significantly because water naturally pools in these areas first. If your restaurant occupies a space with a history of water intrusion, previous flood claims on the property, or proximity to rivers, streams, or coastal areas, your vulnerability increases substantially. Waterfront locations in Florida face particular exposure because hurricane season runs from June through November, and coastal erosion combined with storm surge creates compounding risks that inland restaurants simply don’t encounter.

Strengthen Your Physical Defenses

Physical improvements reduce your flood risk before insurance enters the equation. Install hurricane-rated shutters or impact-resistant glass on ground-level windows and doors to prevent water and debris entry during storms. Anchor signage, drive-thru canopies, and outdoor structures securely because wind-driven debris causes secondary water damage when it breaches walls and windows. Elevate critical equipment like HVAC units, electrical panels, and backup generators above your property’s flood level to preserve operational capacity after water recedes. Seal foundation cracks and gaps around utility penetrations where water seeps into your building during heavy rainfall. Improve drainage around your property by clearing gutters, downspouts, and grading away from the foundation so water flows away rather than pools against your building. Install check valves in floor drains and sewer lines to prevent backflow when municipal systems become overwhelmed during flooding events. These measures cost money upfront but reduce both your flood damage exposure and your insurance premiums because carriers reward risk reduction with lower rates. A restaurant in New York City that implemented proper grading and sealed its foundation before 2023’s record rainfall avoided the six feet of basement water that affected dozens of Park Slope businesses that year.

Match Coverage to Your Exposure Level

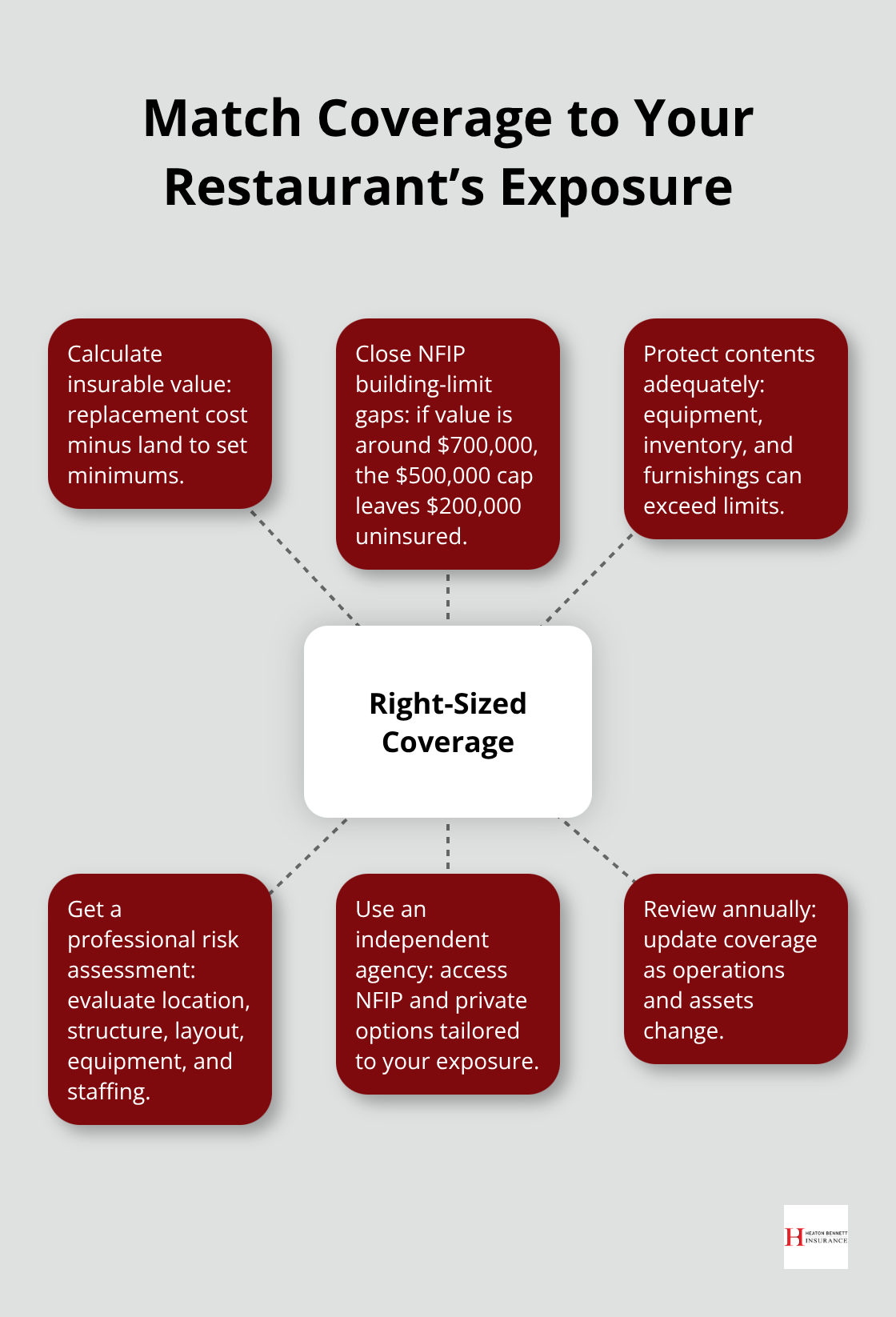

Work with an insurance professional who understands restaurant operations specifically, not general commercial insurance. Your insurable value determines your minimum required coverage and should reflect your building’s replacement cost minus land value. If your restaurant’s insurable value reaches 700,000 dollars, the NFIP building coverage maximum of 500,000 dollars leaves a 200,000 dollar gap that requires private flood insurance.

Contents coverage matters equally because spoiled inventory, damaged equipment, and destroyed furnishings represent substantial losses. The NFIP covers up to 500,000 dollars in contents for nonresidential properties, protecting furniture, appliances, finished inventory, raw materials, and equipment. However, if your restaurant stocks high-value items or operates with significant inventory value, this limit may prove insufficient. Request a professional risk assessment that evaluates your location, building structure, drive-thru layout (if applicable), equipment inventory, and staffing to identify specific vulnerabilities. An independent agency with access to multiple carriers can source both NFIP coverage and private flood insurance options tailored to your exposure rather than forcing you into a single carrier’s limitations. This approach allows your coverage to grow with your business and adjust when you add equipment, expand your menu, or renovate your space. Annual policy reviews become non-negotiable because restaurants change constantly, and your insurance must reflect those changes to avoid coverage gaps when floods occur.

Final Thoughts

Restaurant flood coverage protects your business from a threat that affects 99 percent of U.S. counties and originates 40 percent of damage claims from low-risk areas. Standard commercial property insurance won’t cover water damage from external sources, leaving you exposed to losses that average around $90,000 per claim-often far higher for restaurants when you factor in spoiled inventory, equipment replacement, and structural repairs. Your restaurant faces real exposure regardless of location, and the gap between what your current policy covers and what a flood actually costs determines whether you reopen in weeks or close permanently.

Proper restaurant flood coverage planning requires three concrete actions. Check your actual flood zone using FEMA’s Flood Map Service Center rather than guessing based on your address, assess your building’s specific vulnerabilities like ground-level entrances and basement utility areas, and work with an insurance professional who understands restaurant operations to match your coverage to your actual insurable value. If your building replacement cost exceeds the NFIP maximum of $500,000, you need private flood insurance to cover the gap, and contents coverage matters equally because your equipment, inventory, and furnishings represent substantial loss exposure.

Contact Heaton Bennett Insurance to assess your flood vulnerability and build a coverage plan that protects your restaurant through whatever water damage comes your way. Our team accesses multiple carriers to source both NFIP policies and private flood insurance options matched to your specific exposure. Start protecting your restaurant today.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.