Short-Term vs. Long-Term Disability Insurance What’s the Difference?

Disability insurance protects your income when illness or injury prevents you from working. Short-term disability covers temporary conditions, while long-term policies handle extended periods of inability to work.

We at Heaton Bennett Insurance see many people confused about which type they need. Understanding the key differences helps you make the right choice for your financial security.

How Does Short-Term Disability Work?

Short-term disability insurance replaces income for three to six months when you cannot work due to illness or injury. Most policies pay 60-70% of your gross income, with benefits that start after an elimination period of seven to 30 days. The Social Security Administration reports that over 25% of today’s 20-year-olds will experience at least one year of disability during their careers, which makes this coverage more important than many realize.

What Conditions Qualify for Coverage

Pregnancy complications, mental health episodes, and cancer treatments represent the most common reasons people file short-term disability claims (according to LIMRA research from 2021). Surgery recovery, broken bones, and severe infections also qualify. Most policies exclude pre-existing conditions that doctors diagnose within six months before coverage begins and injuries from illegal activities or substance abuse.

Employer Plans Beat Individual Policies

Employer-sponsored short-term disability costs significantly less than individual coverage. Group rates through employers average 0.5-1% of your salary annually, while individual policies can cost 2-3% of your income. Only five states (including California and New York) mandate employer coverage, which leaves most workers dependent on voluntary employer programs. Individual policies offer portability when you change jobs but come with higher premiums and stricter medical underwriting requirements that can exclude coverage for health conditions.

How Benefits Work in Practice

Short-term policies typically activate after you submit medical documentation that proves you cannot perform your job duties. The elimination period acts as a deductible in time rather than money. Most people exhaust their short-term benefits before they return to work or transition to long-term coverage, which creates a gap that long-term disability insurance fills.

Why Long-Term Disability Matters More

Long-term disability insurance provides income replacement for years or even decades when you cannot work due to severe illness or injury. These policies typically cover 60% of your gross monthly income and can pay benefits until retirement age. The Social Security Administration data shows that disability claims that last more than 90 days often extend for years, which makes long-term coverage far more valuable than most people realize. Unlike short-term policies that handle temporary setbacks, long-term disability kicks in after elimination periods of 90 days to two years (with 90 days as the standard choice).

Coverage That Adapts to Your Needs

The best long-term policies include cost of living adjustments that increase your benefits annually to match inflation rates. This feature becomes critical when extended disabilities span multiple years. Own-occupation riders represent another must-have feature that pays benefits when you cannot perform your specific job, even if you could work in a different field. Professional workers like doctors and lawyers should never purchase long-term disability without own-occupation protection.

Premium Costs and Payment Structure

Annual premiums typically cost 1-3% of your salary, but high earners may pay $165 to $885 monthly (based on their occupation risk level and benefit amount selection). The average annual cost of disability insurance reaches approximately $2,200, though individual factors affect this amount. Shorter elimination periods lead to higher premiums since they increase the insurer’s risk level.

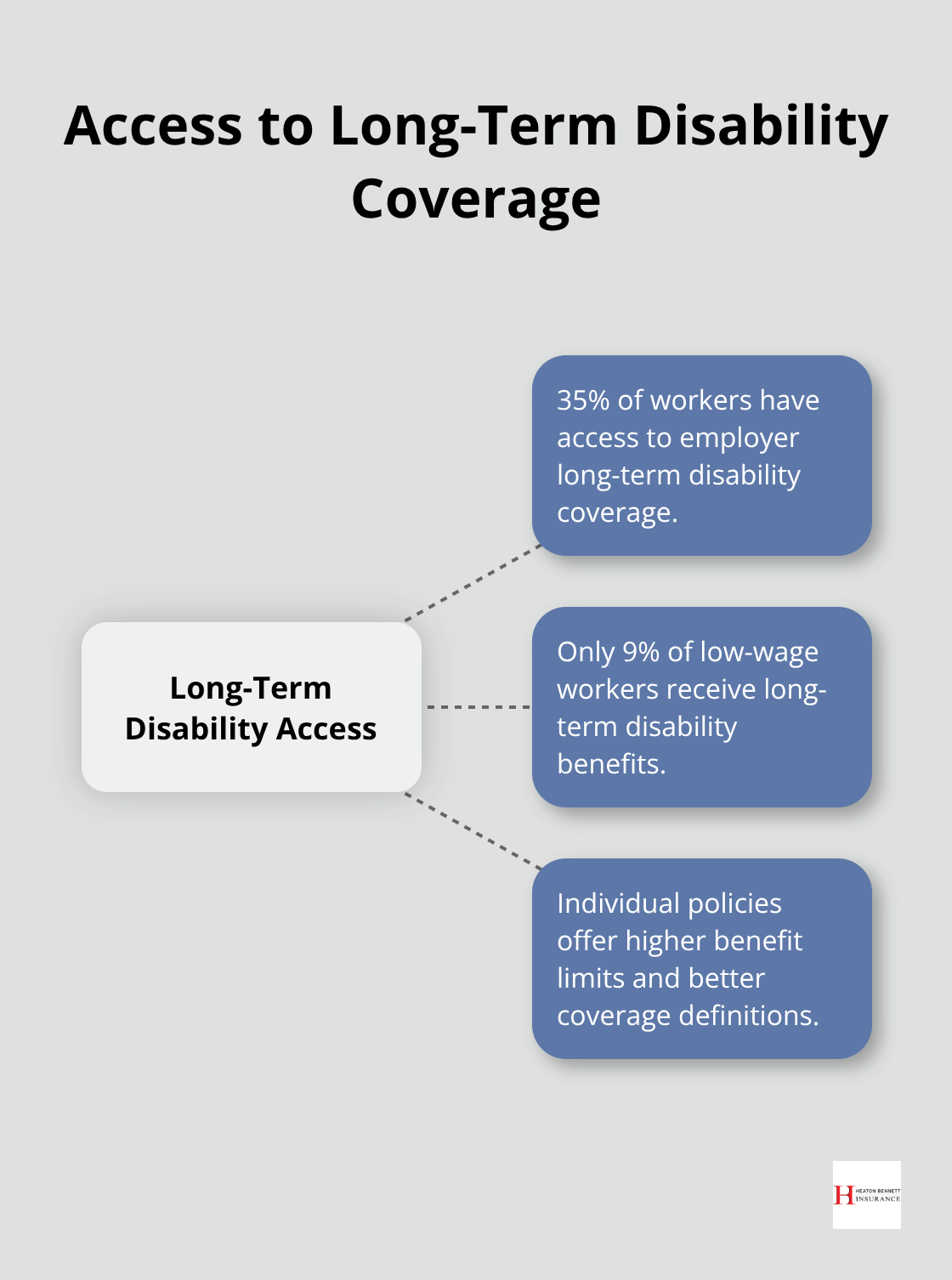

Individual Policies Beat Group Coverage

Employer-provided long-term disability often caps benefits at $5,000 monthly and disappears when you change jobs. Individual policies offer higher benefit limits, better definitions of disability, and portable coverage that follows you throughout your career. The National Compensation Survey found that only 35% of workers have access to employer long-term disability, with just 9% of low-wage workers who receive this benefit. Individual policies cost more upfront but provide superior protection and tax advantages when you pay premiums with after-tax dollars.

These fundamental differences between short-term and long-term coverage create important considerations when you evaluate which type of protection fits your specific situation.

What Makes These Two Coverage Types So Different

Short-term and long-term disability insurance operate on completely different timelines and benefit structures that directly impact when you receive money and how much you get. Short-term policies activate benefits after elimination periods of seven to 30 days, while long-term coverage requires you to wait 90 days to two years before payments begin. This difference creates a critical gap that many people overlook when they plan their coverage strategy.

When Your Benefits Actually Start

The elimination period functions as your financial responsibility before insurance kicks in. Short-term policies with 14-day elimination periods cost significantly more than 30-day options, but the extra premium pays for faster access to benefits. Long-term policies with 90-day elimination periods represent the sweet spot for most people and balance affordable premiums with reasonable wait times.

Workers who choose 720-day elimination periods save substantial money on premiums but risk financial disaster during extended disabilities. The Bureau of Labor Statistics reports that only 40% of civilian workers had access to short-term disability in March 2020, while just 35% could access long-term coverage through their employers.

How Much Money You Actually Receive

Short-term policies typically replace 60-70% of your gross income with higher percentages available through some employer plans, while long-term coverage usually caps benefits at 60% of gross monthly income. The calculation methods differ substantially between policy types.

Short-term benefits often use your current salary as the baseline, but long-term policies may average your income over the past two years to determine benefit amounts. Individual long-term policies frequently offer higher benefit limits than group coverage, with some professional policies that provide up to $15,000 monthly compared to typical group plan caps of $5,000.

Premium Costs Reflect Coverage Differences

Premium costs reflect these benefit differences, with long-term coverage that costs 1-3% of annual salary compared to short-term policies at 0.5-1% for employer plans. Higher earners among professionals like doctors may pay monthly premiums that range from $165 to $885 for disability coverage (depending on their occupation risk level and benefit amount selection).

The average annual cost of disability insurance reaches approximately $2,200, though individual factors affect this amount. Shorter elimination periods lead to higher premiums since they increase the insurer’s risk level.

Final Thoughts

Your financial situation determines which disability coverage works best for you. Workers with substantial emergency funds can choose longer elimination periods on long-term policies to reduce premiums, while those who live paycheck to paycheck need short-term disability for immediate protection. The statistics paint a clear picture: over 25% of 20-year-olds will face disability during their careers, yet only 40% of workers have access to short-term coverage through employers.

Most financial experts recommend that you combine both coverage types for complete protection. Short-term disability bridges the gap during your long-term policy’s elimination period, while long-term coverage protects against extended disabilities that could last years or decades. This dual approach costs more upfront but prevents income loss during any disability scenario (whether temporary or permanent).

Individual policies offer superior benefits compared to employer plans, especially for high earners who need coverage above typical group plan limits. Professional workers should prioritize own-occupation riders and cost-of-living adjustments that maintain purchasing power over time. We at Heaton Bennett Insurance help Austin residents navigate these complex coverage decisions and compare multiple carriers to find the best disability insurance solutions that match your specific needs and budget.