How Long-Term Care Insurance Can Help with Assisted Living Costs

As we age, the possibility of needing assisted living becomes a reality for many. The costs associated with this type of care can be substantial, often catching families off guard.

At Heaton Bennett Insurance, we understand the importance of planning for the future. Long-term care insurance can be a valuable tool in managing the financial burden of assisted living expenses.

What Is Long-Term Care Insurance?

Definition and Purpose

Long-term care insurance is a specialized coverage that helps pay for extended care services not typically covered by health insurance, Medicare, or Medicaid. This type of insurance acts as a financial safeguard for assisted living, nursing home care, or in-home care services.

Types of Care Covered

Long-term care insurance policies cover a wide range of services, primarily focusing on assistance with activities of daily living (ADLs) such as bathing, dressing, and eating. The coverage extends to various care settings:

- Assisted living facilities

- Nursing homes

- Adult day care centers

- In-home care services

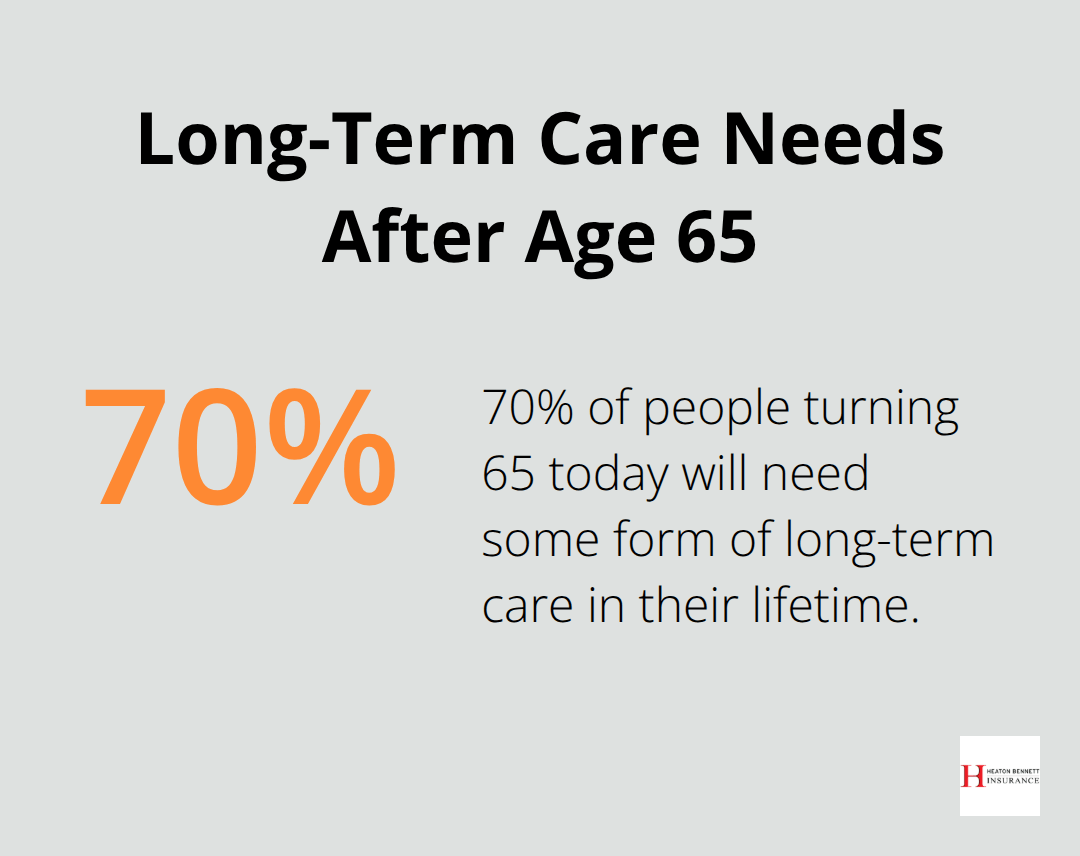

The U.S. Administration for Community Living reports that about 70% of people turning 65 today will need some form of long-term care in their lifetime. This statistic highlights the importance of including long-term care insurance in financial planning.

Key Policy Features

Understanding the key features of long-term care insurance policies is essential when exploring options:

- Benefit Period: This can range from two to five years, with some policies offering lifetime coverage.

- Elimination Period: This waiting period (typically 30 to 90 days) occurs before benefits begin. During this time, policyholders must cover their own care costs.

- Inflation Protection: This feature helps ensure coverage keeps pace with rising care costs over time. It’s particularly important considering that the national median cost of assisted living is $5,190 per month (according to A Place for Mom’s 2025 long-term care cost report).

Timing and Premiums

The ideal time to purchase long-term care insurance is before age 65. This strategy allows individuals to secure lower premiums and ensures coverage availability when it’s most needed. Premiums can vary significantly based on factors such as age, health status, and the level of coverage selected.

As we move forward, it’s important to understand how long-term care insurance specifically addresses assisted living costs. Let’s explore this connection in more detail.

How Long-Term Care Insurance Covers Assisted Living Costs

Long-term care insurance plays a significant role in managing the expenses of assisted living. These facilities provide a middle ground between independent living and nursing home care, offering support with daily activities while maintaining a level of independence. However, the costs can be substantial.

The Reality of Assisted Living Expenses

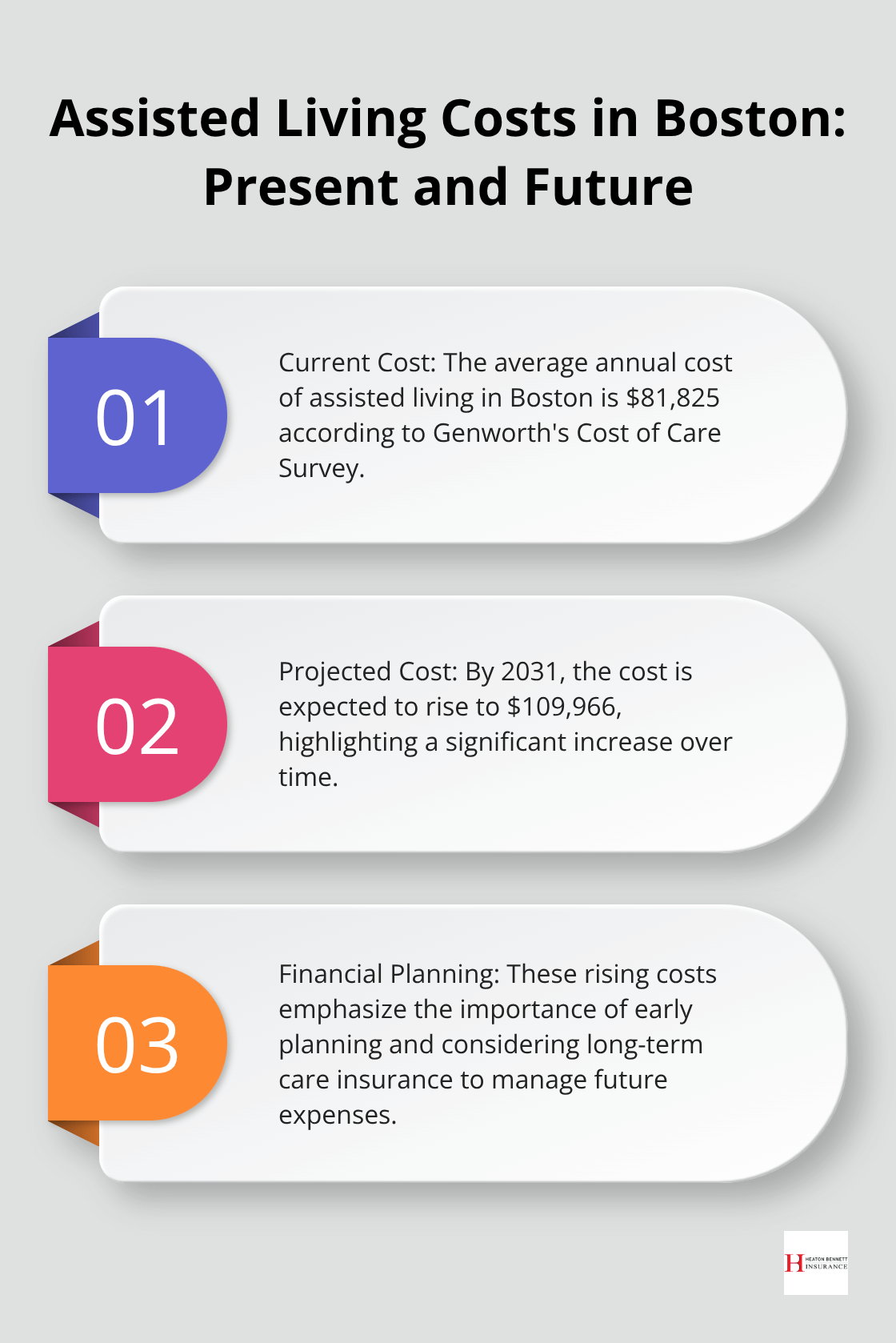

According to Genworth’s Cost of Care Survey, the average annual cost of assisted living in Boston is currently $81,825, with projections indicating a rise to $109,966 by 2031. This steep increase highlights the importance of financial planning for long-term care needs.

Coverage Percentages and Benefit Limits

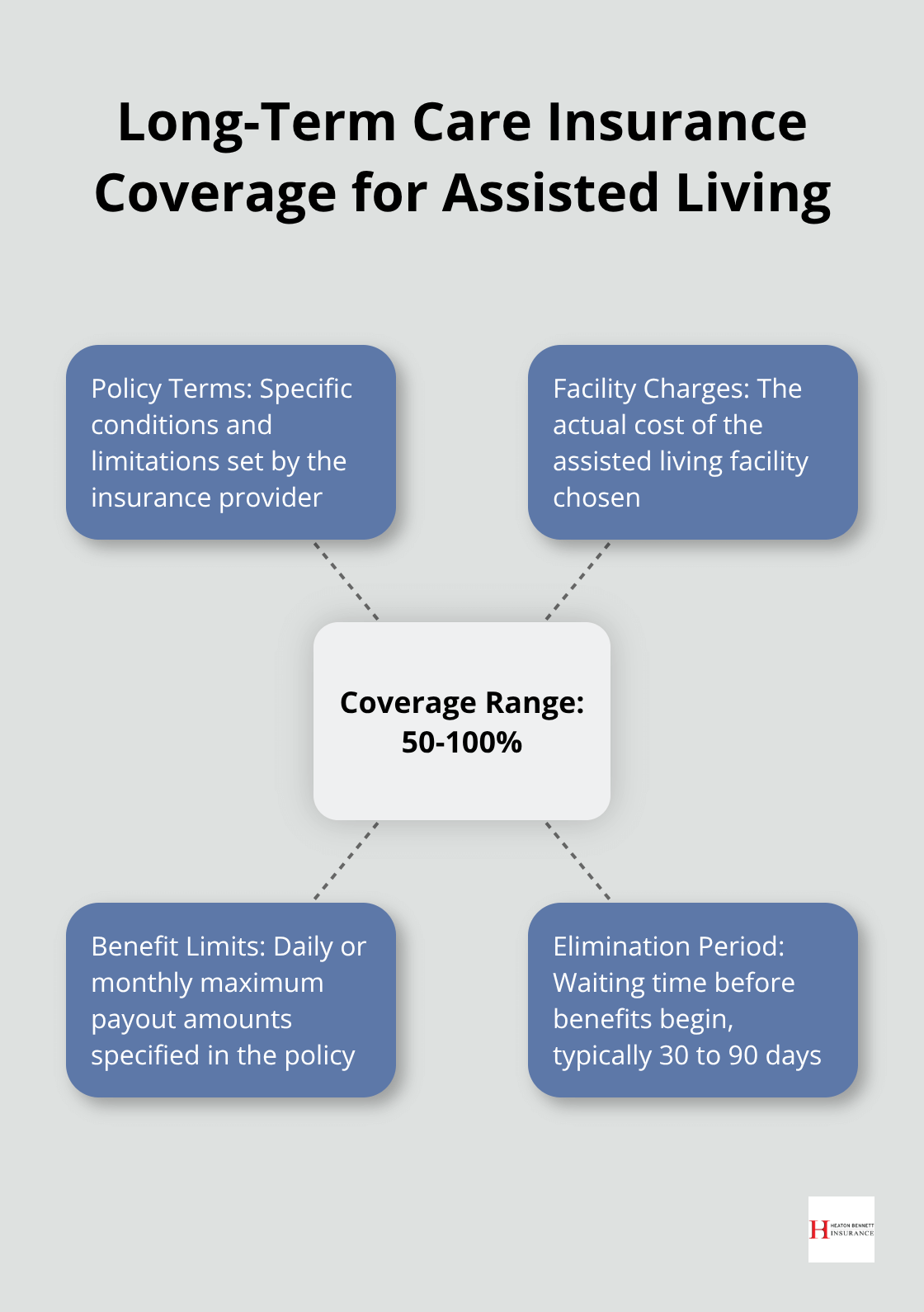

Long-term care insurance typically covers a significant portion of assisted living costs, but it’s not a universal solution. Policies often pay up to a set daily limit, which can range from $100 to $500 per day. It’s important to ensure that this amount aligns with local care costs to avoid substantial out-of-pocket expenses.

Most policies cover between 50% to 100% of assisted living costs, depending on the specific terms and the facility’s charges. Some policies offer a pool of money that can be used over time (rather than a strict daily limit), providing more flexibility in coverage.

Activation of Benefits

To start receiving benefits, policyholders must meet specific “benefit triggers.” These typically include:

- Needing assistance with at least two Activities of Daily Living (ADLs) such as bathing, dressing, or eating

- Having a cognitive impairment like Alzheimer’s disease

Once these triggers are met, there’s usually an elimination period – a waiting time before benefits begin. This period can range from 30 to 90 days, during which the policyholder must cover their own care costs. Shorter elimination periods often result in higher premiums, so it’s essential to balance immediate needs with long-term affordability.

Maximizing Your Coverage

To get the most out of your long-term care insurance for assisted living:

- Select a policy with inflation protection to keep pace with rising care costs

- Consider a longer elimination period if you can manage short-term costs to lower your premiums

- Choose a benefit period that aligns with the average stay in assisted living (which is about 22 months according to A Place for Mom)

Understanding these aspects of long-term care insurance can help you make informed decisions about coverage for potential assisted living needs. It’s a complex topic, and working with a knowledgeable insurance agent can provide clarity and ensure you’re adequately protected. The next section will explore the advantages of having long-term care insurance specifically for assisted living situations.

Why Long-Term Care Insurance Is a Game-Changer for Assisted Living

Financial Security in an Uncertain Future

The costs of assisted living are staggering and continue to rise. Without proper planning, these expenses can quickly deplete your life savings. Long-term care insurance acts as a buffer against this financial strain. In Boston, the average annual cost of assisted living is currently $81,825 (according to Genworth’s Cost of Care Survey). Your insurance could cover a substantial portion of this expense. This coverage allows you to maintain your standard of living without the constant worry of running out of money.

Freedom to Choose Your Care

One of the most significant advantages of long-term care insurance is the flexibility it provides in selecting your care options. Without insurance, your choices might limit you to the most affordable options, which may not align with your preferences or needs. With a comprehensive policy, you have the freedom to choose high-quality assisted living facilities that offer the amenities and level of care you desire. This flexibility extends to the location as well – you’re not restricted to facilities based solely on cost, allowing you to stay closer to family or in a preferred area.

Protecting Your Legacy

Long-term care insurance plays a crucial role in preserving your assets for future generations. Without it, you might need to liquidate investments, sell property, or use funds earmarked for your children or grandchildren to cover assisted living costs. Insurance coverage for these expenses can protect the wealth you’ve worked hard to accumulate throughout your life. This protection ensures that your legacy remains intact, allowing you to pass on your assets as you’ve always intended.

Peace of Mind for You and Your Family

The right long-term care insurance policy provides peace of mind not just for you, but for your entire family. It eliminates the potential burden on your loved ones to provide or finance your care. This assurance allows you to focus on enjoying your retirement years without worrying about becoming a financial strain on your family. Moreover, it gives your family members the comfort of knowing that you’ll receive quality care without jeopardizing their own financial stability.

Tailored Coverage for Your Unique Needs

Long-term care insurance policies offer various options to suit individual needs and budgets. You can choose the daily benefit amount, the length of coverage, and additional features like inflation protection. This customization allows you to create a policy that aligns perfectly with your projected needs and financial situation. For example, you might opt for a policy that covers 80% of the average cost of assisted living in your area (which could save you thousands of dollars annually) while also including a 3% annual increase to keep pace with rising care costs.

Final Thoughts

Long-term care insurance protects your finances and future quality of life when considering assisted living options. The costs of assisted living can catch families unprepared, making this insurance a valuable investment. Your decision to purchase should factor in your health history, family longevity, and retirement savings.

Heaton Bennett Insurance understands the complexities of long-term care insurance. Our team of experts will guide you through the process and help you find a policy that fits your needs and budget. We offer a Security Snapshot process to provide tailored, comprehensive coverage without tying you to a single carrier.

Take action now to explore long-term care insurance options. The right coverage will protect your assets, preserve your independence, and provide peace of mind for you and your loved ones. Let us help you secure a policy that prepares you for potential assisted living needs in the future.