The Hidden Costs of Aging How Long-Term Care Insurance Helps

As we age, the financial landscape can shift dramatically, often catching us off guard. At Heaton Bennett Insurance, we’ve seen how unexpected healthcare costs can quickly deplete retirement savings.

Long-term care expenses are a significant concern, frequently overlooked in financial planning. This blog post will explore the hidden costs of aging and how long-term care insurance can provide a safety net for your future.

The True Cost of Aging: Unveiling Hidden Financial Challenges

Escalating Healthcare Expenses

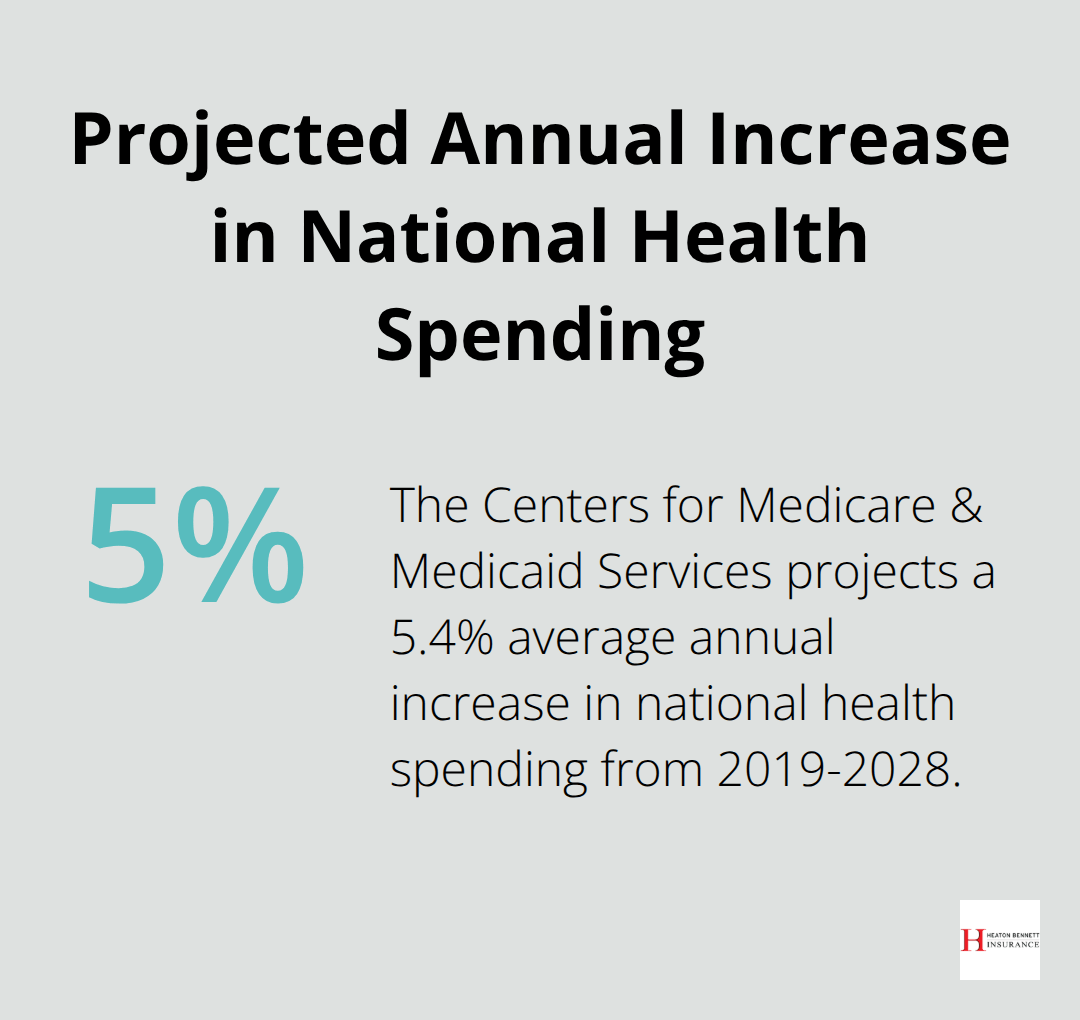

Healthcare costs for seniors continue to rise at an unprecedented rate. The Centers for Medicare & Medicaid Services projects national health spending to increase by an average annual rate of 5.4% from 2019-2028, reaching a staggering $6.2 trillion by 2028. This surge outpaces general inflation, placing a significant burden on retirees’ financial resources.

Medicare’s Limitations

While Medicare provides essential health coverage for seniors, it falls short in several critical areas. Many individuals express surprise when they learn that Medicare doesn’t cover long-term care, most dental procedures, eye exams for glasses, dentures, or hearing aids. These gaps in coverage often result in substantial out-of-pocket expenses, especially for those who require ongoing care or manage chronic conditions.

The Erosion of Retirement Savings

The combination of increasing healthcare costs and Medicare’s coverage gaps leads to a significant drain on retirement savings. A recent study by Fidelity Investments estimates that the average 65-year-old couple retiring in 2022 will need approximately $315,000 (after tax) to cover healthcare expenses in retirement. This figure doesn’t even account for potential long-term care costs, which can be substantial.

Financial Strain on Seniors and Families

For many seniors, these unexpected costs force difficult decisions. Some may delay retirement, reduce their quality of life, or rely on family members for financial support. These challenges can strain relationships and create stress for both seniors and their loved ones.

The Importance of Proactive Planning

Understanding these financial challenges marks the first step in creating a comprehensive plan to protect assets and ensure a comfortable retirement. Proper planning and the right insurance coverage can make a significant difference in maintaining financial independence and peace of mind during retirement years.

As we move forward, we’ll explore how long-term care insurance serves as a proactive solution to address these hidden costs of aging, providing a safety net for your financial future.

How Long-Term Care Insurance Protects Your Future

Long-term care insurance stands as a powerful shield against the rising costs of aging. This type of coverage can make a significant difference in people’s lives as they navigate their later years.

Comprehensive Coverage for Extended Care

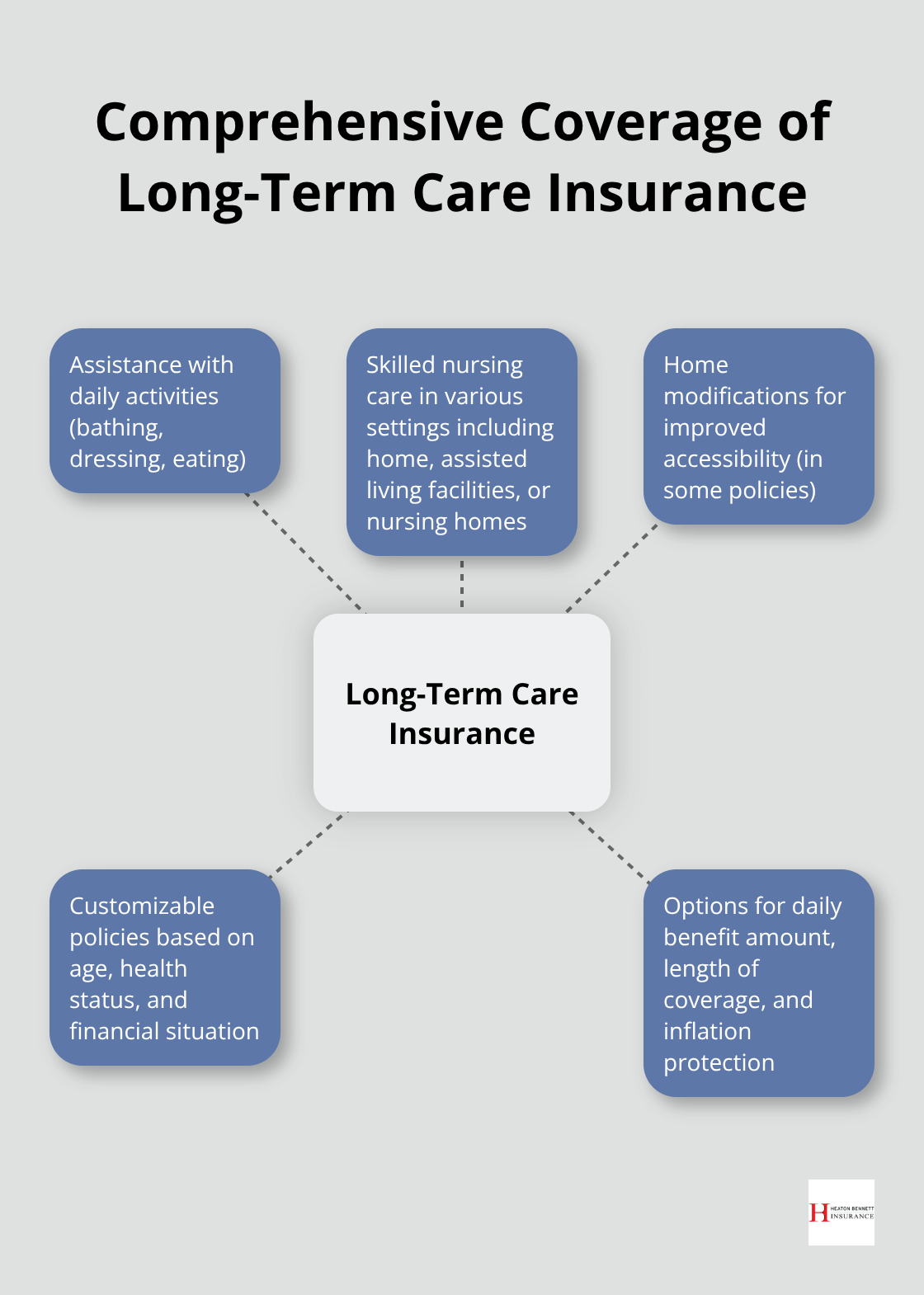

Long-term care insurance covers a wide range of services that regular health insurance or Medicare typically exclude. These services include:

- Assistance with daily activities (bathing, dressing, eating)

- Skilled nursing care

- Care provided at home, in assisted living facilities, or nursing homes

- Home modifications for improved accessibility (in some policies)

This comprehensive coverage allows individuals to receive necessary care without depleting their savings or burdening their families.

Customizable Policies for Individual Needs

No two individuals have identical long-term care needs. Insurance policies in this field offer customization based on factors such as age, health status, and financial situation. Policy holders can select:

- Daily benefit amount

- Length of coverage

- Inflation protection options

Some policies even offer shared care options for couples, creating a pool of benefits that spouses can share (a feature that can provide additional flexibility and value).

Financial Impact and Considerations

The National Association of Insurance Commissioners reports that the average annual premium for long-term care insurance in 2020 was $2,675. However, premiums vary widely based on the age at purchase and the level of coverage chosen. Generally, purchasing a policy earlier in life results in lower premiums.

Integration with Existing Financial Strategies

Long-term care insurance complements other financial planning tools. While retirement savings and investments cover day-to-day expenses, long-term care insurance acts as a safety net for potential high-cost care needs. This approach allows individuals to:

- Preserve assets for other purposes (e.g., leaving an inheritance)

- Maintain a spouse’s quality of life

- Avoid depleting savings on unexpected care costs

Some life insurance policies now offer long-term care riders, providing death benefits if long-term care isn’t needed. These hybrid policies offer additional flexibility and peace of mind.

The decision to invest in long-term care insurance requires careful consideration of one’s financial situation, health history, and future goals. A thorough evaluation of different policy options can help individuals find coverage that aligns with their overall financial strategy and protects their income, health, and future.

As we move forward, we’ll examine the costs and benefits associated with long-term care insurance, helping you make an informed decision about this important financial tool.

Is Long-Term Care Insurance Worth the Cost?

Understanding Premium Costs

Long-term care insurance represents a significant investment. The American Association for Long-Term Care Insurance reports that a healthy 55-year-old man can expect to pay an average annual premium of $1,700 for a policy with an initial pool of benefits of $164,000. For a woman of the same age and health status, the average premium increases to $2,675 annually. These figures highlight the importance of considering long-term care insurance earlier in life when premiums are generally lower.

Factors Influencing Policy Costs

Several key elements affect the cost of long-term care insurance:

Age and Health: Younger, healthier applicants typically secure lower premiums. The American Association for Long-Term Care Insurance states that each year an individual delays purchasing a policy after age 60 results in a 3-4% increase in premium costs.

Coverage Amount: Higher daily or monthly benefit amounts and longer benefit periods increase premiums. A policy that pays $150 per day for three years will cost less than one that pays $250 per day for five years.

Elimination Period: This period represents the time between when an individual needs care and when the policy starts paying. Longer elimination periods (e.g., 90 days vs. 30 days) can lower premiums but require more out-of-pocket spending initially.

Inflation Protection: While important for maintaining the policy’s value over time, this feature can significantly increase premiums. The U.S. Department of Health and Human Services estimates that inflation protection can double the premium.

Evaluating Potential Savings

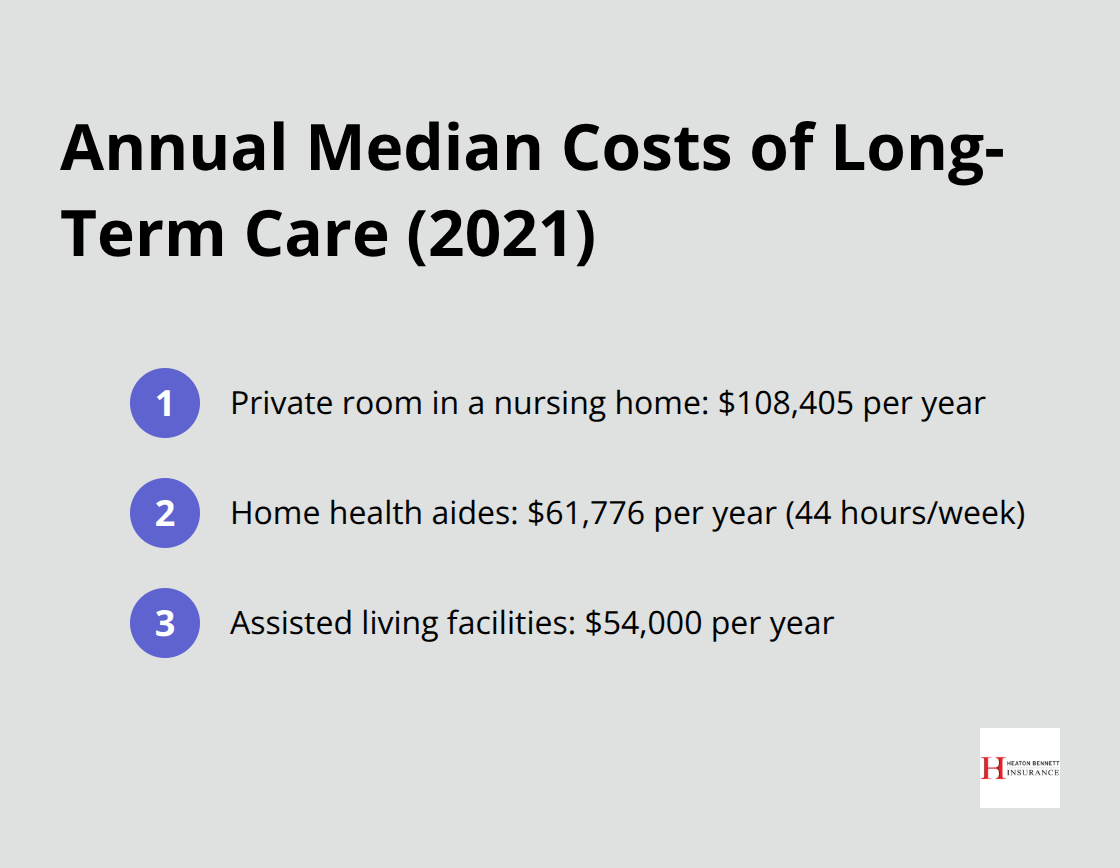

To assess the value of long-term care insurance, it’s essential to compare potential out-of-pocket costs for care against the cumulative cost of premiums. The Genworth Cost of Care Survey 2021 provides some sobering figures:

- The national median cost for a private room in a nursing home is $108,405 per year.

- Assisted living facilities average $54,000 annually.

- Home health aides cost an average of $61,776 per year (for 44 hours of care per week).

Given these figures, even a few years of care can quickly deplete savings. A long-term care insurance policy that costs $2,500 annually for 20 years ($50,000 total) could save hundreds of thousands in out-of-pocket expenses if long-term care becomes necessary.

Impact on Family Caregivers

The emotional and financial strain on family caregivers can be substantial. The AARP Public Policy Institute reports that family caregivers spend an average of $7,242 per year on out-of-pocket costs related to caregiving. Long-term care insurance can alleviate this burden, allowing family members to focus on emotional support rather than financial concerns.

Weighing the Investment

Long-term care insurance protects assets and provides options for care that might otherwise be financially out of reach. While the cost of premiums is a significant consideration, the potential savings and peace of mind often outweigh the investment for many individuals. The decision to purchase long-term care insurance requires careful evaluation of personal financial situations, health histories, and future goals.

Final Thoughts

Proper financial planning proves essential for a secure retirement. The financial risks of aging without adequate coverage can deplete savings and burden families. Long-term care expenses pose a major threat to financial stability in later years.

Long-term care insurance acts as a safeguard against the high costs of extended care. It offers peace of mind and financial protection when needed most. We recommend you assess your current financial situation and future care needs to secure a stable financial future.

Our team at Heaton Bennett Insurance can help you select the right coverage to protect your assets. We offer personalized solutions tailored to your unique situation (including long-term care options). Take action today to safeguard your tomorrow and maintain your quality of life in your golden years.