How to Find Affordable Auto Insurance for Young Drivers

Young drivers face insurance premiums that average 50% higher than experienced drivers, with rates often exceeding $3,000 annually. The combination of limited driving history and higher accident statistics creates significant financial pressure for new drivers and their families.

At Heaton Bennett Insurance, we understand that finding affordable auto insurance for young drivers requires strategic planning and smart shopping. The right approach can reduce premiums by 20-40% while maintaining adequate protection.

What Drives Your Insurance Costs Higher

Age Creates the Biggest Premium Jump

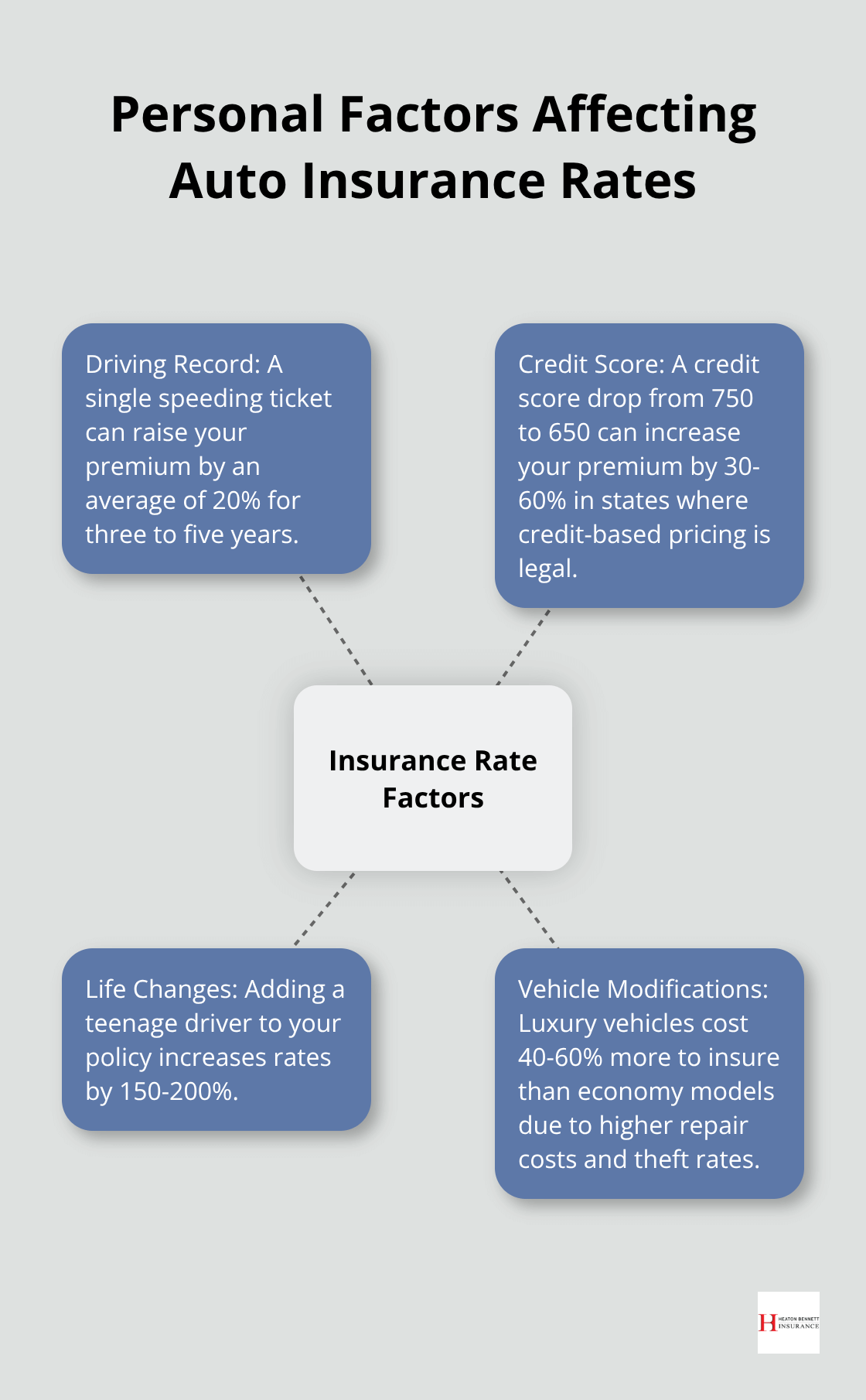

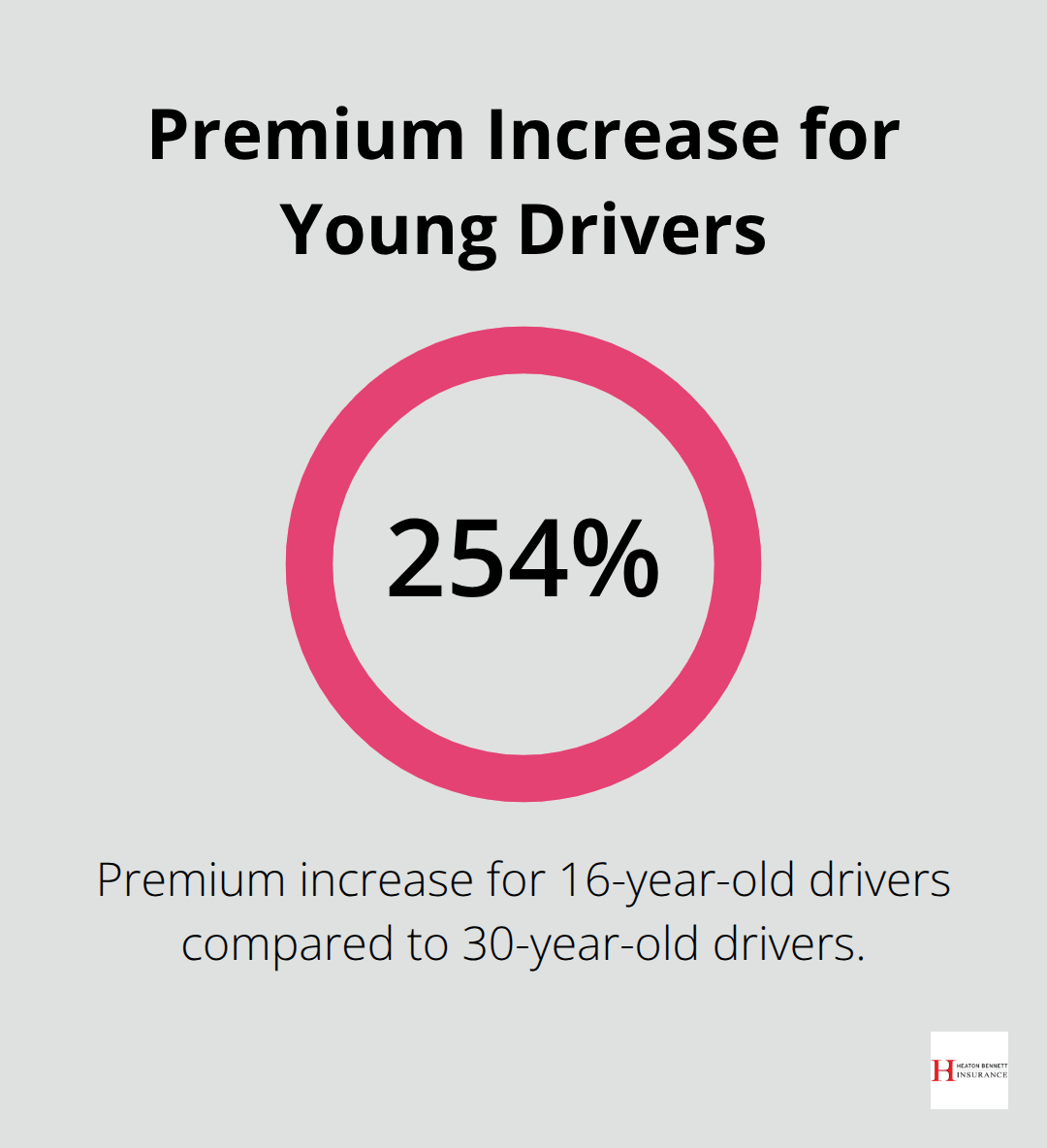

Insurance companies base rates on hard data, and the numbers paint a clear picture. Sixteen-year-old drivers pay $7,658 annually on average, which represents a 254% increase over thirty-year-old drivers who pay $2,189. The National Highway Traffic Safety Administration reports that teen crash rates per mile are three times higher than drivers aged twenty and older.

Even within the teen bracket, sixteen-year-olds crash 1.5 times more often than eighteen and nineteen-year-olds. These statistics directly translate into premium calculations that drop significantly each year until age twenty-five. Insurance carriers adjust rates based on this proven risk data rather than assumptions.

Vehicle Choice Impacts Your Premiums Dramatically

Your car selection affects premiums as much as your age does. Larger vehicles with high crash test ratings and low theft rates generate lower premiums than sports cars or luxury vehicles. The Insurance Institute for Highway Safety maintains detailed safety ratings that insurers reference when they set rates.

A Honda Civic costs thousands less to insure annually than a Dodge Challenger. High-performance cars, luxury vehicles, and cars with poor safety records drive premiums higher, while practical, well-rated vehicles keep costs manageable. Vehicles with advanced safety features like automatic emergency braking and blind spot detection qualify for additional discounts with most carriers.

Location Determines Your Risk Profile

Geographic location creates dramatic premium variations that young drivers often overlook. Louisiana teens pay over $10,000 annually while North Carolina teens pay $3,692 for identical coverage (a difference of nearly $6,400 per year). Urban areas with higher accident rates, theft statistics, and population density generate higher premiums than rural locations.

Even moves within the same state can change rates substantially based on local crime statistics and accident frequency data compiled by state insurance departments. Understanding these cost-saving strategies becomes essential when you start shopping for the best rates available.

How Can Young Drivers Cut Insurance Costs in Half

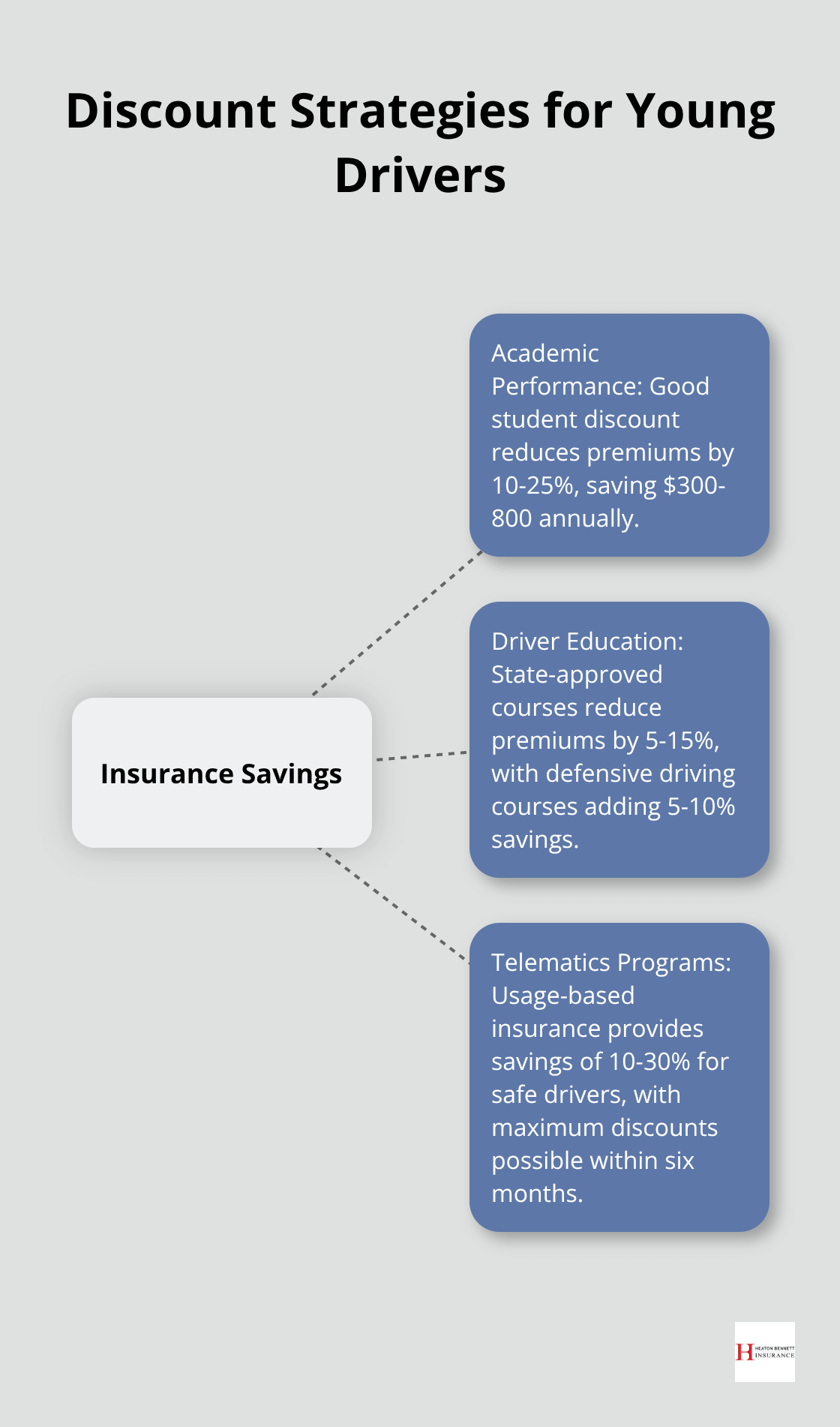

Academic performance creates the most accessible path to immediate savings for young drivers. The good student discount reduces premiums by 10-25% for students who maintain a B average or better, which translates to $300-800 in annual savings. State Farm, Allstate, and Progressive offer these discounts to full-time students under 25, while some carriers extend eligibility through age 27 for graduate students. The National Association of Insurance Commissioners data shows that students who qualify for academic discounts maintain this benefit throughout college, which creates thousands in cumulative savings.

Driver Education Programs Generate Substantial Discounts

State-approved driver education courses reduce premiums by 5-15% with most major carriers. The Insurance Institute for Highway Safety reports that formal training programs decrease accident rates by 20% among new drivers, which insurers reward with lower rates. Defensive driving courses provide additional savings of 5-10% and remain valid for three years in most states. Online courses from AAA or the National Safety Council cost $25-50 but generate annual savings of $200-400. Most insurers require course completion within six months of policy inception to qualify for discounts.

Telematics Programs Offer the Highest Savings Potential

Usage-based insurance through telematics programs provides savings of 10-30% for safe drivers, with top performers who earn maximum discounts within six months. Progressive Snapshot, State Farm Drive Safe & Save, and Allstate Drivewise monitor acceleration, braking, speed, and nighttime driving to calculate personalized rates. Young drivers who avoid hard braking and maintain speeds within 10 mph of posted limits achieve the highest discount tiers. The Federal Highway Administration data indicates that telematics participants reduce risky driving behaviors by 40% (creating long-term premium benefits that extend beyond program completion).

These discount strategies work best when you combine them with smart shopping techniques. The next step involves comparing quotes from multiple carriers to find the lowest base rates before you apply these money-saving discounts.

How Do You Find the Best Insurance Deal

Compare Multiple Carriers for Maximum Savings

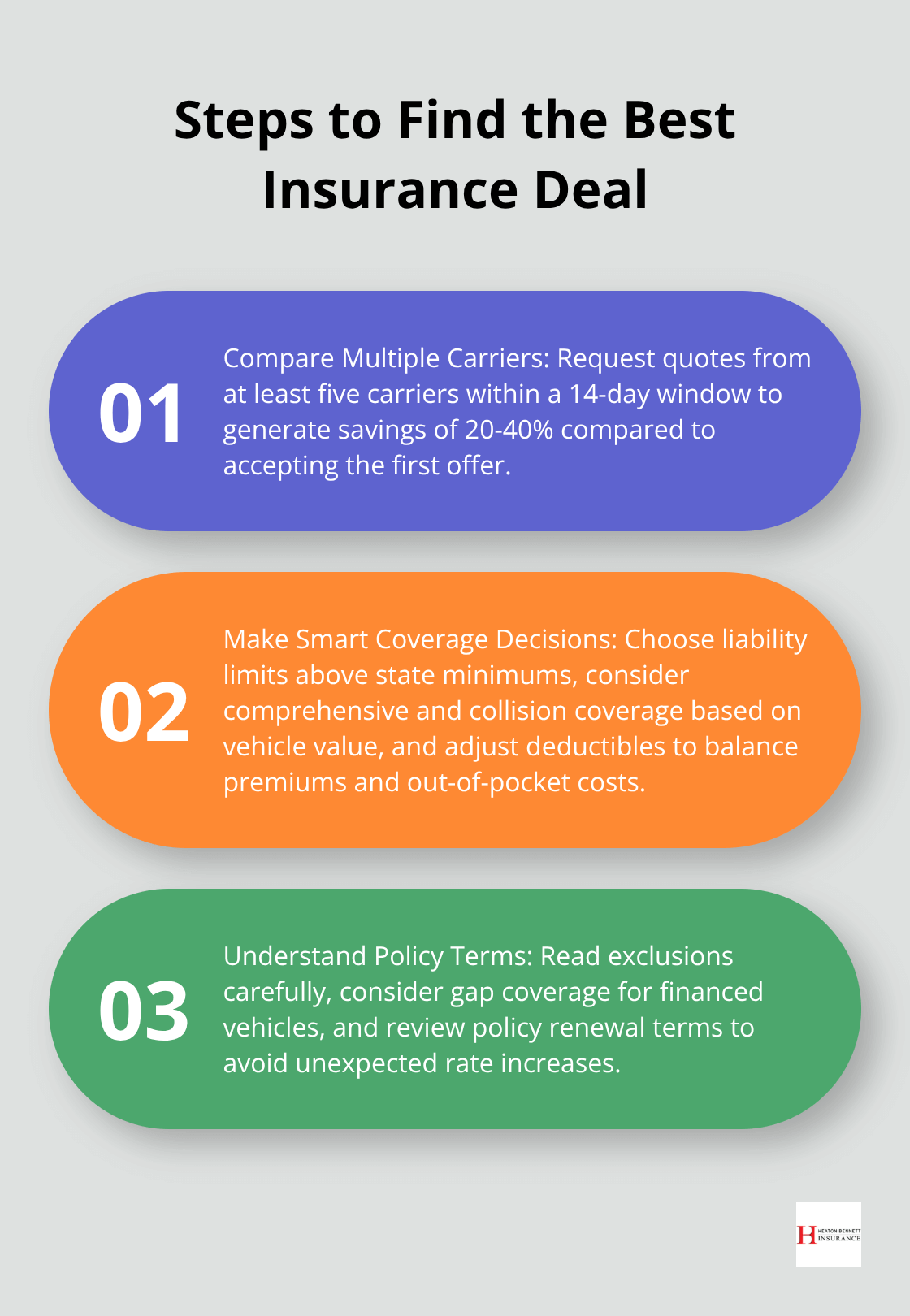

Request quotes from at least five carriers to generate savings of 20-40% compared to accepting the first offer, according to the National Association of Insurance Commissioners. Progressive, State Farm, Geico, Allstate, and USAA consistently offer competitive rates for young drivers, but their rates vary dramatically based on individual risk factors. Submit all quote requests within a 14-day window to minimize credit report impacts, and provide identical information to each carrier for accurate comparisons.

Online quote tools deliver faster results, but direct conversations with agents reveal additional discounts that automated systems miss. Independent agencies access multiple carriers simultaneously, which saves time while providing comprehensive coverage options that single-carrier agents cannot match.

Make Smart Coverage Decisions Without Risk

Choose liability limits above state minimums because young drivers face higher lawsuit risks after accidents. Texas requires 30/60/25 coverage, but 100/300/100 limits cost only 10-15% more while providing substantially better protection. Comprehensive and collision coverage make financial sense for vehicles worth more than $4,000, but skip these coverages on older cars where annual premiums exceed 20% of vehicle value.

Increase deductibles from $500 to $1,000 to reduce premiums by 15-20%, but maintain emergency funds to cover higher out-of-pocket costs. Personal injury protection and uninsured motorist coverage cost minimal amounts but provide essential protection against underinsured drivers (who cause 13% of accidents according to the Insurance Research Council).

Understand Policy Terms and Hidden Costs

Read exclusions carefully because standard policies exclude racing, commercial use, and intentional acts that young drivers commonly encounter. Gap coverage becomes essential for financed vehicles because new cars depreciate 20% immediately after purchase, which leaves owners responsible for loan balances after total losses.

Rental car coverage costs $20-40 annually but prevents $30-50 daily expenses during repairs that average 12 days for collision claims. Review policy renewal terms because some carriers increase rates substantially after the first year, particularly for drivers with claims or violations (making annual policy reviews essential for cost control).

Final Thoughts

Young drivers who apply these strategies reduce their auto insurance for young drivers costs by 30-50% annually. Academic discounts, driver education programs, and telematics programs create immediate savings that compound over time. Smart comparison shopping across multiple carriers generates additional reductions that single-carrier quotes cannot match.

Regular policy reviews become essential because rates change frequently based on record improvements, age milestones, and market conditions. Young drivers should reassess their coverage every six months to capture new discounts and competitive rates from different insurers. This practice helps drivers stay ahead of rate increases and take advantage of improved risk profiles.

We at Heaton Bennett Insurance help young drivers find competitive rates through our access to multiple carriers and personalized coverage analysis (which identifies all available discounts while matching coverage to individual needs and budgets). Our team works to reduce premiums through strategic policy selection and comprehensive carrier comparisons. Contact our Austin team to start lowering your auto insurance costs today.