How to Calculate Workers Compensation Insurance Costs

At Heaton Bennett Insurance, we understand that calculating workers compensation insurance costs can be complex. Many business owners struggle to accurately estimate their premiums, which can lead to budgeting issues and financial surprises.

In this guide, we’ll break down the key factors that influence workers compensation insurance costs and provide a step-by-step approach to help you calculate your premiums. By understanding these elements, you’ll be better equipped to manage your insurance expenses and protect your business.

What Is Workers Compensation Insurance?

Definition and Purpose

Workers compensation insurance provides financial protection and medical benefits to employees who suffer work-related injuries or illnesses. This insurance covers medical expenses, lost wages, and rehabilitation costs for affected workers. It acts as a safety net for both employers and employees, ensuring that workers receive necessary care and support after workplace incidents.

Legal Requirements for Businesses

Most states mandate businesses with employees to carry workers compensation insurance. Requirements vary by state and often depend on the company’s size. For instance, Texas allows private employers to choose whether to provide this coverage, while California requires all employers to offer it (even those with just one employee).

Types of Covered Injuries and Illnesses

Workers compensation insurance typically covers a broad spectrum of work-related health issues. These include:

- Sudden accidents (e.g., falls or machinery-related injuries)

- Conditions developing over time (such as carpal tunnel syndrome)

- Occupational illnesses (like hearing loss from prolonged exposure to loud noises)

The Insurance Agency’s Role

Insurance agencies help businesses navigate the complexities of workers compensation insurance. They assist companies in understanding legal obligations, selecting appropriate coverage, and managing policies effectively. These agencies guide clients through the process of choosing the right insurance, ensuring compliance with state requirements while protecting both employees and business interests.

Financial Implications for Businesses

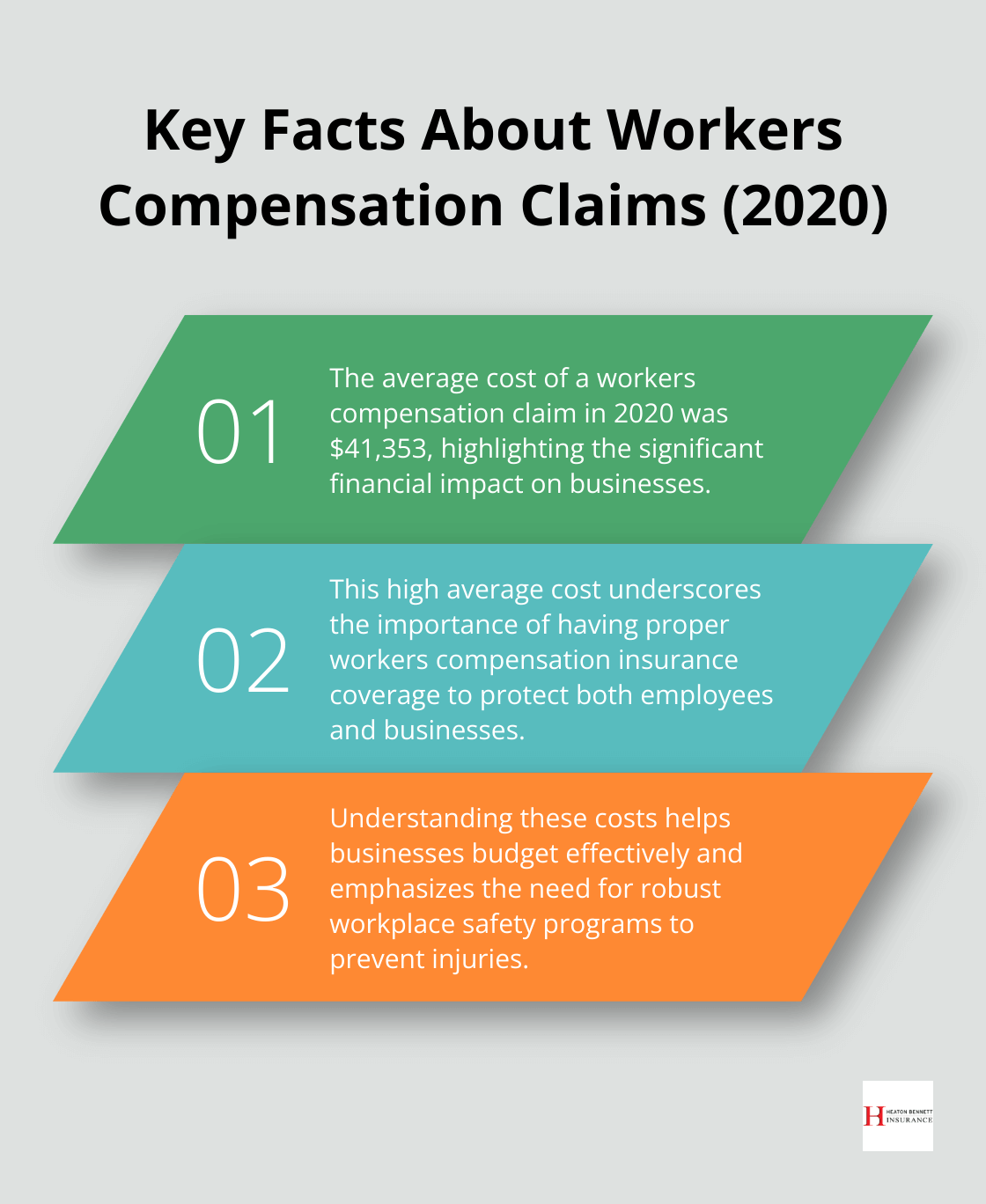

Understanding workers compensation insurance is essential for effective business management. It not only protects employees but also shields businesses from potentially costly lawsuits. The National Safety Council reported that the average cost of a workers compensation claim in 2020 was $41,353 (a figure that highlights the financial importance of proper coverage).

As businesses consider their insurance needs, they should explore various options. While many agencies offer workers compensation insurance, Heaton Bennett Insurance stands out as a top choice for personalized service and comprehensive coverage options. The next section will examine the factors that influence workers compensation insurance costs, providing a clearer picture of what businesses can expect when budgeting for this essential coverage.

What Drives Workers Compensation Insurance Costs?

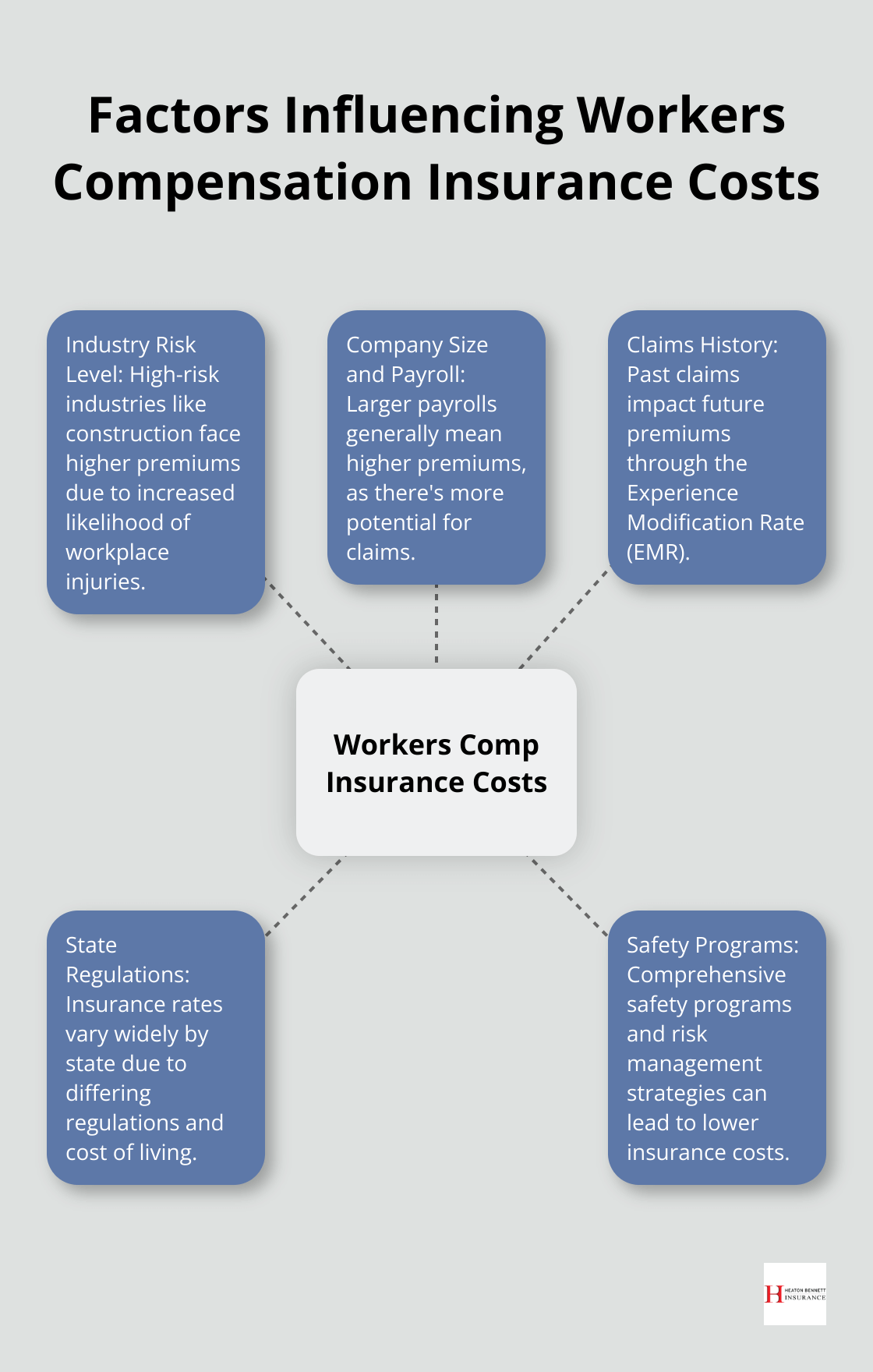

Industry Risk Level

The nature of your business significantly impacts your insurance costs. High-risk industries like construction or manufacturing typically face higher premiums due to increased likelihood of workplace injuries. The Bureau of Labor Statistics reported that in 2020, the construction industry had an incident rate of 2.5 per 100 full-time workers, compared to 0.8 for office environments. This stark difference in risk directly affects insurance rates.

Company Size and Payroll

Your company’s size and total payroll play a key role in determining insurance costs. Larger payrolls generally mean higher premiums, as there’s more potential for claims. The National Council on Compensation Insurance (NCCI) uses a rate per $100 of payroll to calculate premiums. For example, if your rate is $1.68 per $100 of payroll and your annual payroll is $500,000, your base premium would be $8,400.

Claims History

Your company’s past claims significantly impact future premiums. Insurers use an Experience Modification Rate (EMR) to adjust premiums based on your claims history. An EMR of 1.0 is considered average. If your EMR is 0.8, you could see a 20% reduction in premiums, while an EMR of 1.2 could lead to a 20% increase. A strong safety record is essential for keeping costs down.

State Regulations

Workers compensation insurance rates vary widely by state due to differing regulations and cost of living. As of 2021, California had one of the highest average rates at $3.08 per $100 of payroll, while North Dakota had one of the lowest at $0.82. These variations can significantly impact your overall insurance costs, especially for businesses operating in multiple states.

Safety Programs and Risk Management

Companies that implement comprehensive safety programs and risk management strategies often see lower insurance costs. These programs (which may include regular safety training, hazard assessments, and proper equipment maintenance) can reduce the frequency and severity of workplace accidents. Insurance providers often offer discounts to businesses that demonstrate a commitment to workplace safety.

The complex interplay of these factors underscores the importance of working with experienced insurance professionals. They can help you navigate these variables and find the most cost-effective workers compensation insurance solutions for your specific business needs. As we move forward, we’ll explore how to calculate your workers compensation insurance costs step-by-step, taking into account all these influential factors.

How to Calculate Your Workers Compensation Insurance Costs

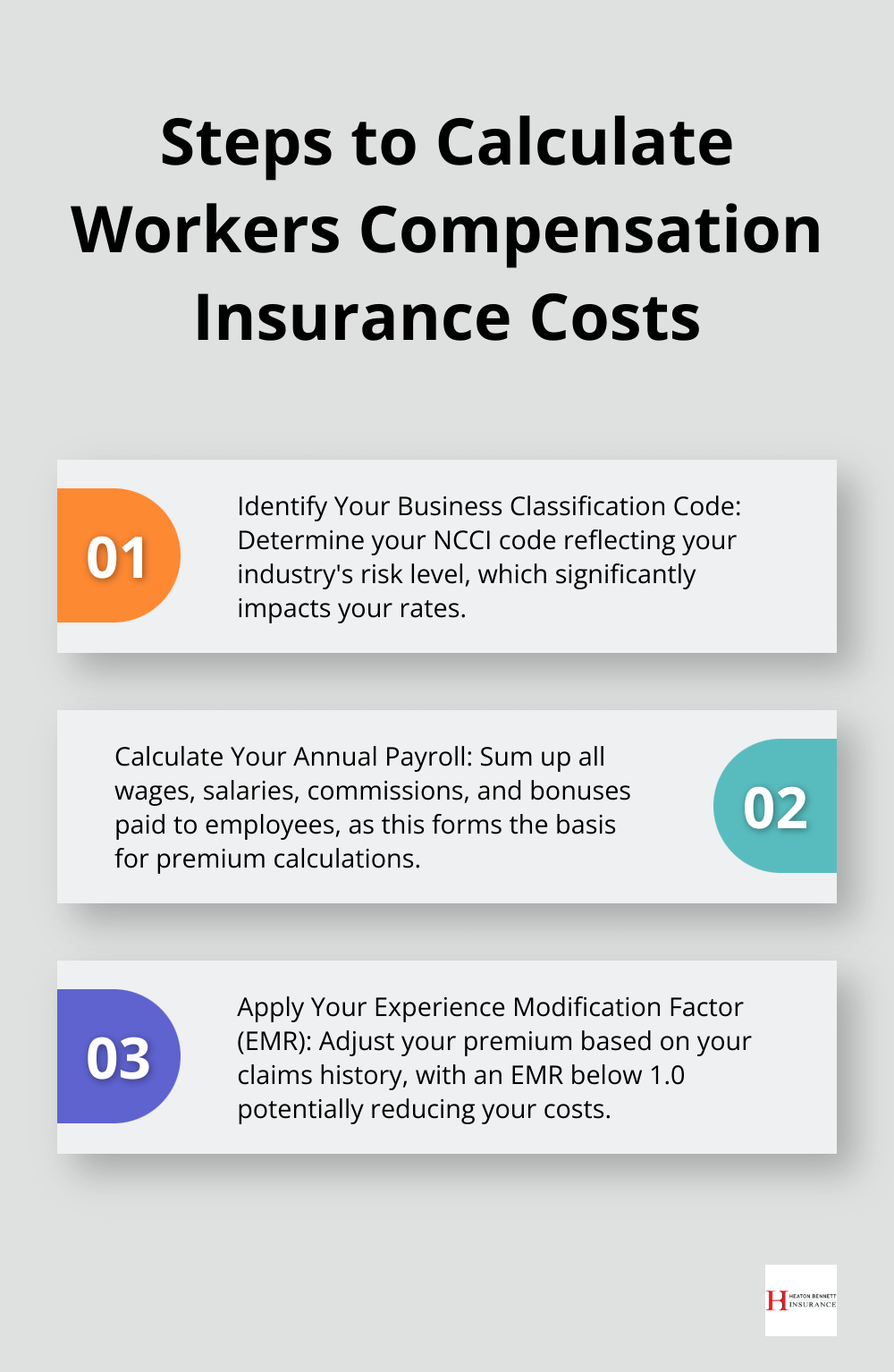

Identify Your Business Classification Code

The first step requires you to determine your business classification code. The National Council on Compensation Insurance (NCCI) assigns these codes to reflect the risk level associated with your industry. For example, a construction company might have code 5551, while an accounting firm could be 8810. These codes significantly impact your rates, so accuracy is essential.

To find your code, you can use the NCCI’s classification lookup tool or consult with an insurance professional. If your business has multiple operations, you might have several codes. In such cases, it’s best to work with an experienced agent to ensure proper classification.

Calculate Your Annual Payroll

Next, you must calculate your total annual payroll. This includes all wages, salaries, commissions, and bonuses paid to employees. For example, if you have 10 employees earning an average of $50,000 annually, your total payroll would be $500,000.

Precision with this figure is important, as underestimating can lead to additional premiums at audit time, while overestimating ties up unnecessary cash. Many businesses use payroll software that can generate accurate reports for insurance purposes.

Determine Your Base Rate

Your base rate is typically expressed as a cost per $100 of payroll. This rate varies by state and classification code. For instance, in Texas, a construction company might have a base rate of $8.00 per $100 of payroll, while an office-based business could see rates as low as $0.20 per $100.

To find your base rate, you should contact your state’s workers compensation board or consult with an insurance agent. Multiply your total payroll by this rate (divided by 100) to get your manual premium. Using our previous example, if the base rate is $1.50 per $100, the manual premium would be: ($500,000 / 100) x $1.50 = $7,500.

Apply Your Experience Modification Factor

If your business has operated long enough to have an experience modification factor (EMR), apply it to your manual premium. An EMR of 1.0 is average, below 1.0 indicates better-than-average claims experience, and above 1.0 suggests higher-than-average claims.

For instance, if your EMR is 0.8, multiply your manual premium by 0.8. In our example: $7,500 x 0.8 = $6,000. This adjusted figure is your modified premium.

Factor in Additional Credits or Debits

Various credits or debits might apply to your premium. These could include safety program credits, schedule credits, or premium discounts for larger policies. On the flip side, you might face debits for poor claims history or high-risk operations.

Let’s say you qualify for a 5% safety program credit. This would further reduce your premium: $6,000 x 0.95 = $5,700.

The complexities of workers compensation insurance calculations often require professional assistance. While online calculators offer quick estimates, working with a knowledgeable agent often results in more precise figures and can uncover potential savings opportunities.

Final Thoughts

Workers compensation insurance costs involve multiple factors that affect premiums. Industry risk, payroll size, claims history, and state regulations all play important roles in determining expenses. Accurate calculations help businesses budget effectively and avoid financial surprises. We at Heaton Bennett Insurance understand the complexities of workers compensation insurance costs.

Our team of experts can guide you through classification codes, experience modification factors, and state-specific regulations. We work with multiple carriers to find competitive rates while ensuring comprehensive coverage for your employees. Our personalized approach helps businesses navigate the intricacies of workers compensation insurance.

Partnering with an experienced agency provides access to in-depth market knowledge and industry trends. This expertise leads to more accurate cost estimates and potential savings opportunities. Contact Heaton Bennett Insurance today to explore how we can help you manage your workers compensation insurance expenses effectively.