Do I Need Workers Compensation Insurance for My Business?

As business owners, we often wonder, “Do I need to get workers compensation insurance?” At Heaton Bennett Insurance, we understand this crucial question.

Workers compensation insurance is a vital protection for both employers and employees, but navigating the requirements can be complex, especially in Texas.

In this post, we’ll explore the ins and outs of workers compensation insurance, helping you make an informed decision for your business.

What Is Workers Compensation Insurance?

Definition and Purpose

Workers compensation insurance serves as a protective measure for businesses and employees. This insurance covers medical expenses and a portion of lost wages for employees who suffer work-related injuries or illnesses. For employers, it provides a shield against potentially costly lawsuits.

Texas Workers Compensation Landscape

Texas stands out in its approach to workers compensation insurance. Unlike most states, Texas does not require private employers to carry this insurance. However, this unique stance does not negate the importance of such coverage for Texas businesses.

Texas-Specific Requirements

While not universally mandated, certain scenarios in Texas necessitate workers compensation insurance:

- Government Contracts: Companies working on government projects often must provide this coverage.

- Construction Industry: Businesses involved in public construction projects typically need to have workers compensation insurance.

Risks of Opting Out

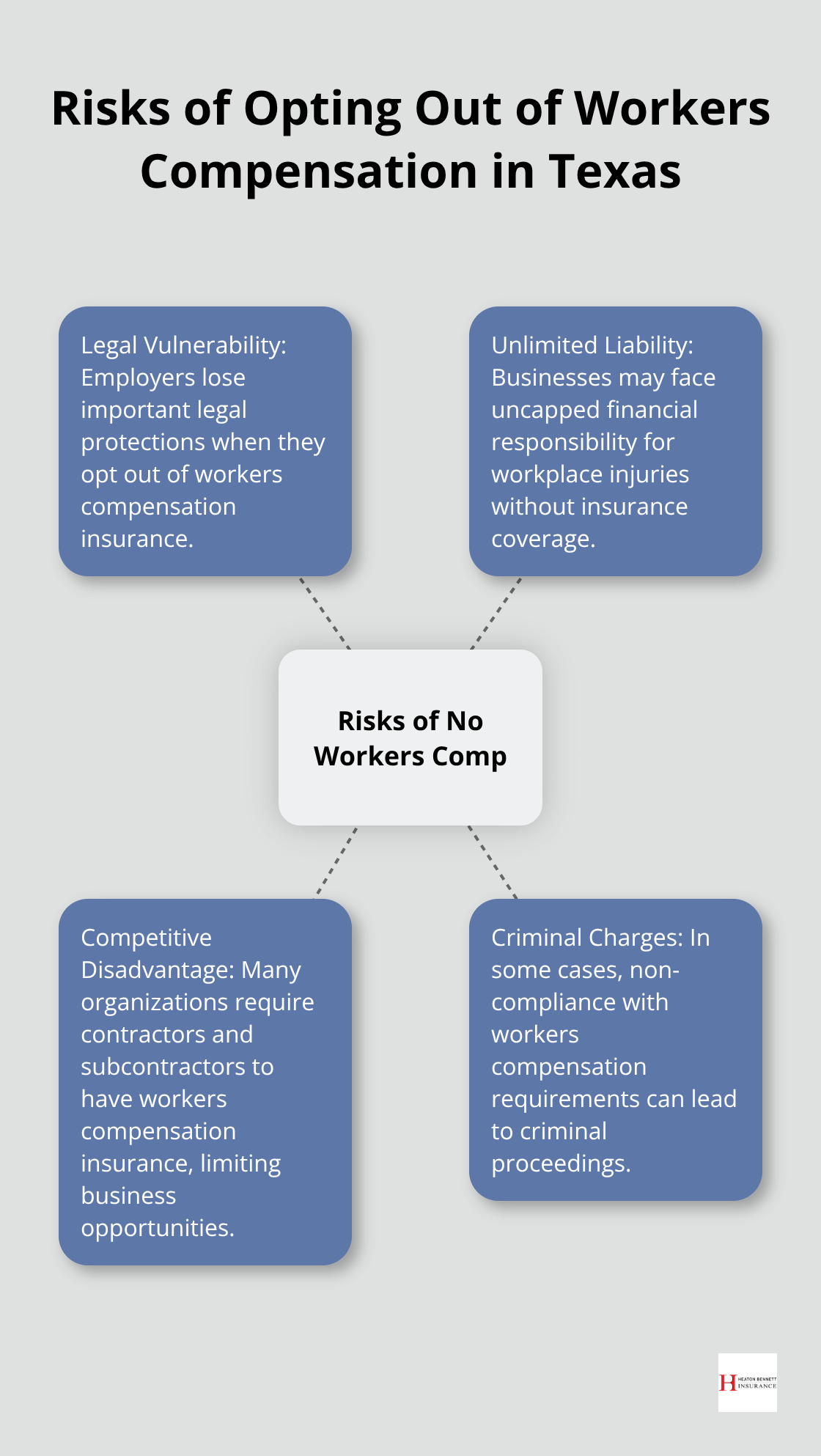

Choosing not to carry workers compensation in Texas exposes businesses to significant risks:

- Legal Vulnerability: Employers lose important legal protections.

- Unlimited Liability: Businesses may face uncapped financial responsibility for workplace injuries.

- Competitive Disadvantage: Many organizations (especially larger companies and government entities) require contractors and subcontractors to have this insurance.

Consequences of Non-Compliance

Even in Texas’s non-mandatory environment, certain situations can lead to penalties:

- False Claims: Businesses that claim to have workers compensation but don’t can face severe consequences (including fines and legal action).

- Criminal Charges: In some cases, non-compliance can lead to criminal proceedings.

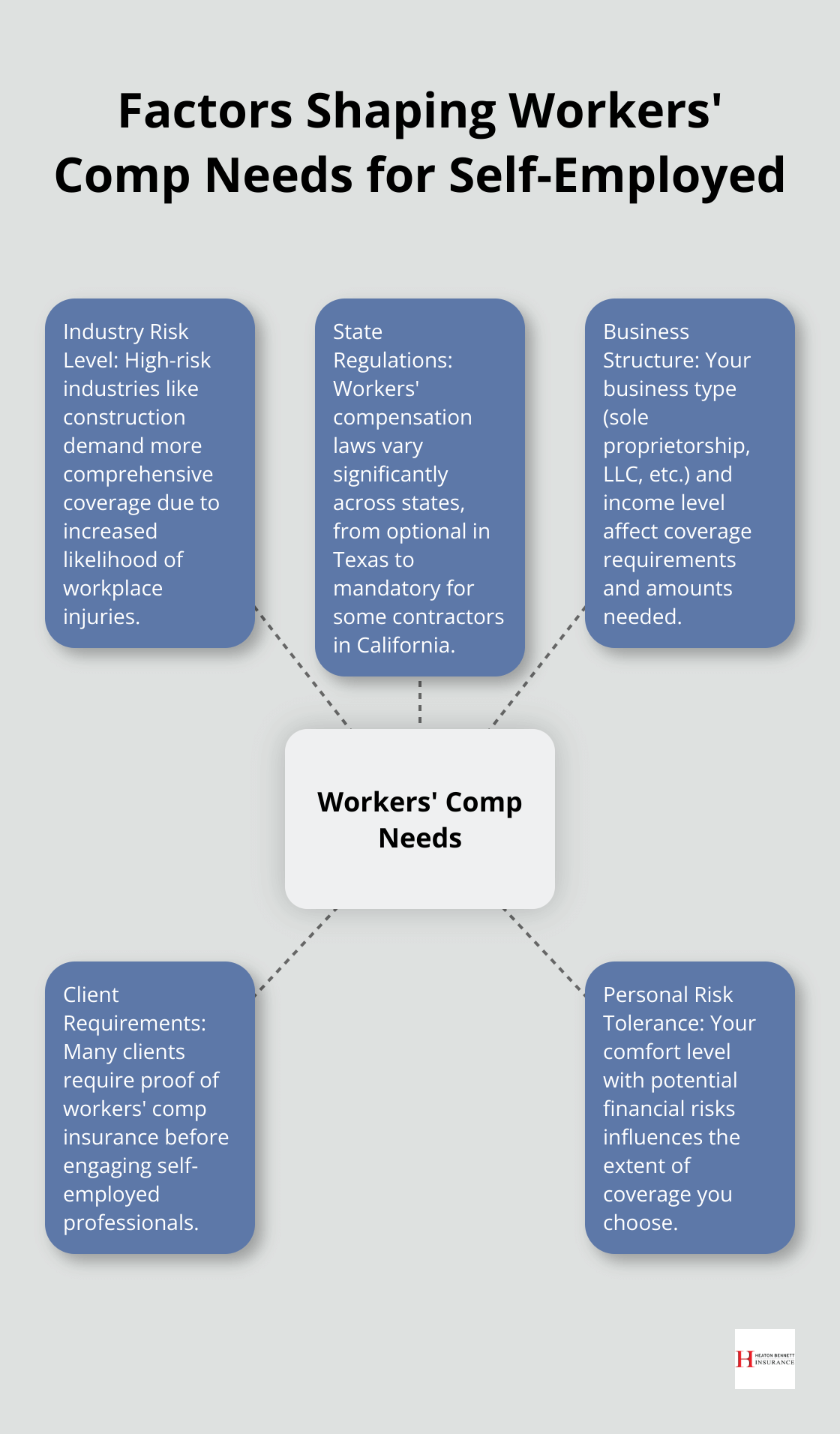

Assessing Your Business Needs

When evaluating the necessity of workers compensation insurance, consider these factors:

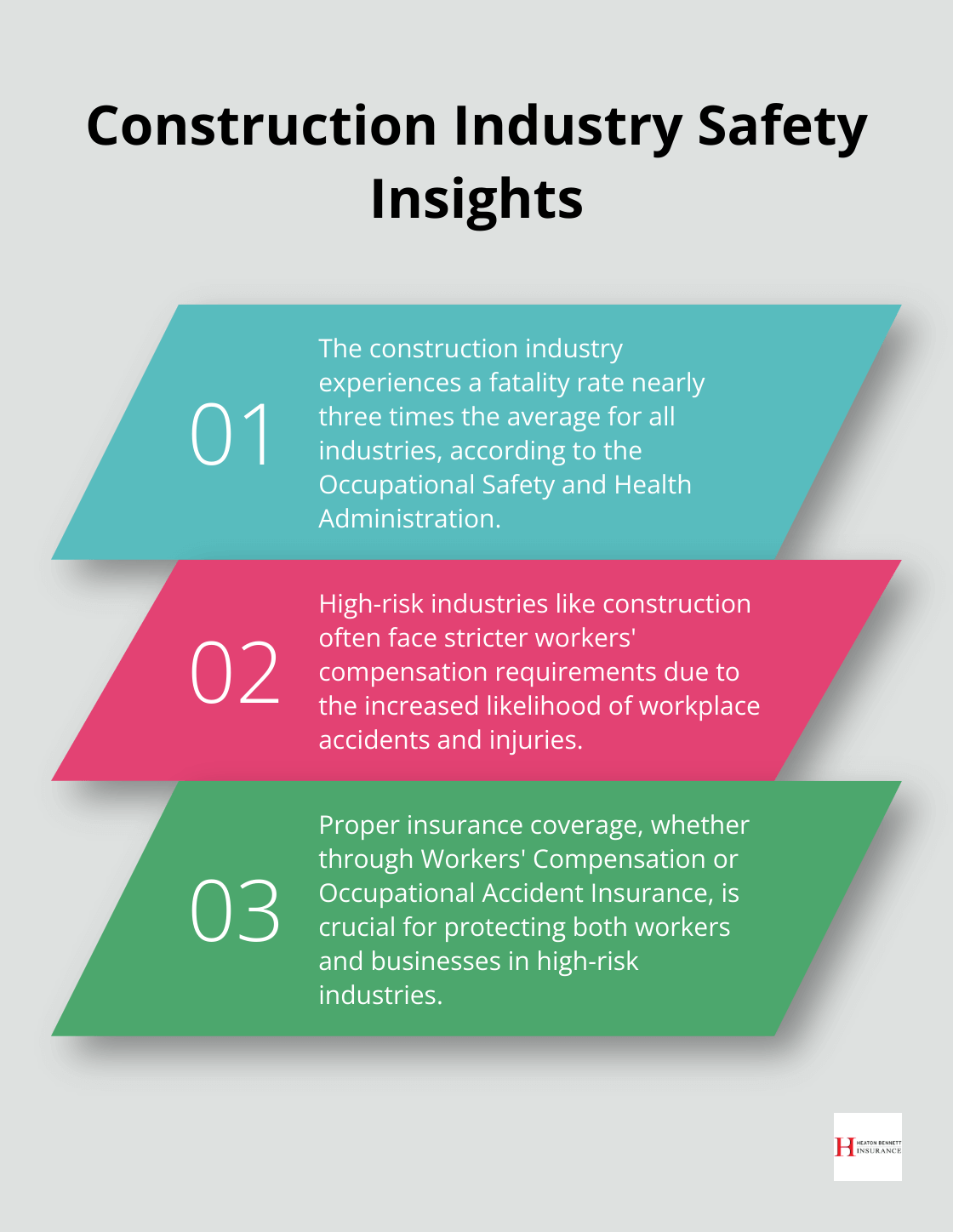

- Industry Risk Level: Some sectors (e.g., construction) have higher injury rates than others.

- Employee Count: The number of workers you employ can influence your insurance needs.

- Financial Capacity: Assess your ability to cover potential workplace injuries out-of-pocket.

It’s important to note that even low-risk industries can experience unexpected accidents. Workers compensation insurance isn’t just about meeting legal requirements-it’s a vital component of a comprehensive risk management strategy.

As we move forward, let’s explore the specific benefits that workers compensation insurance can offer to both employers and employees.

Why Workers Compensation Insurance Matters

Financial Protection for Employers

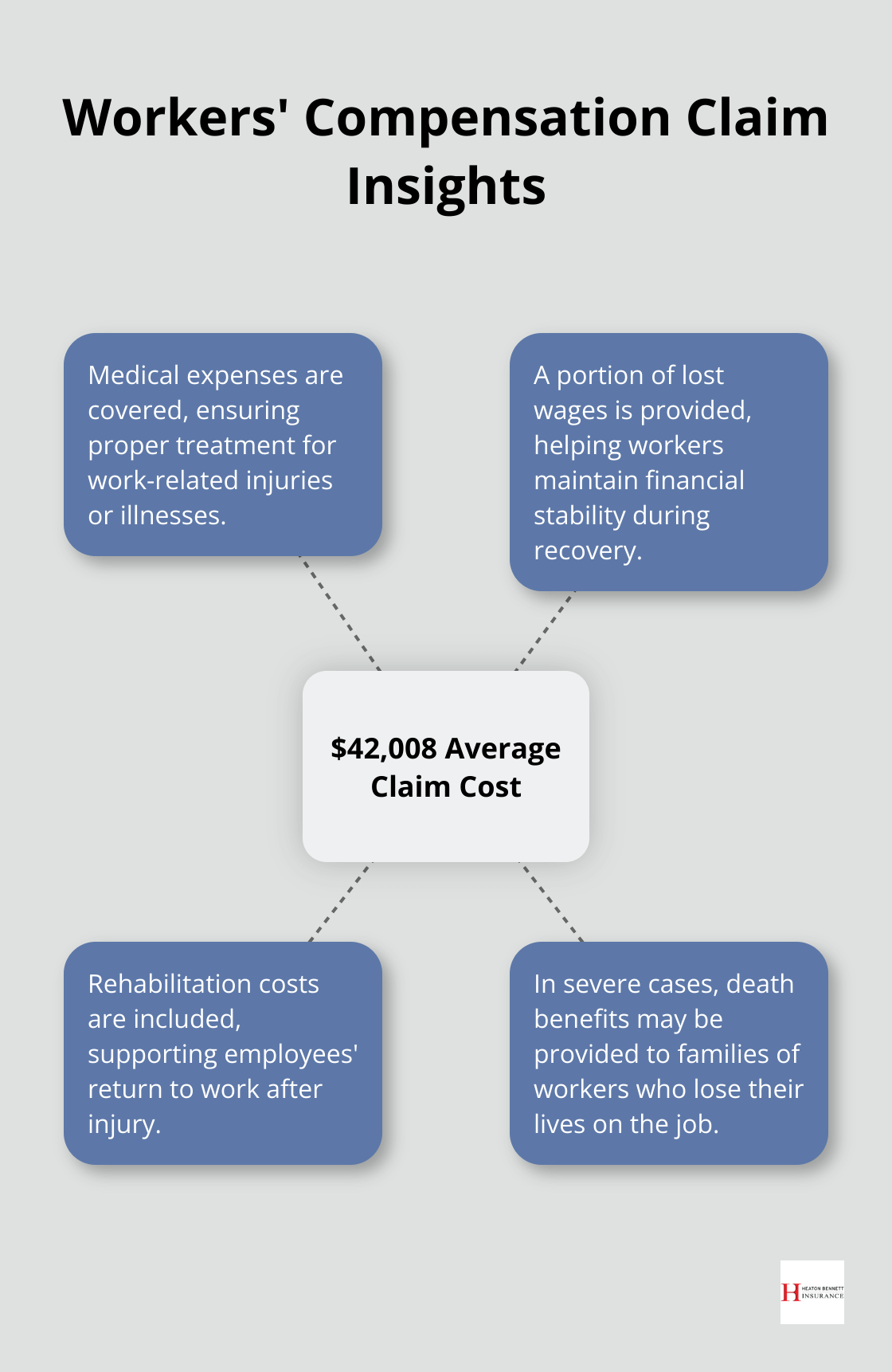

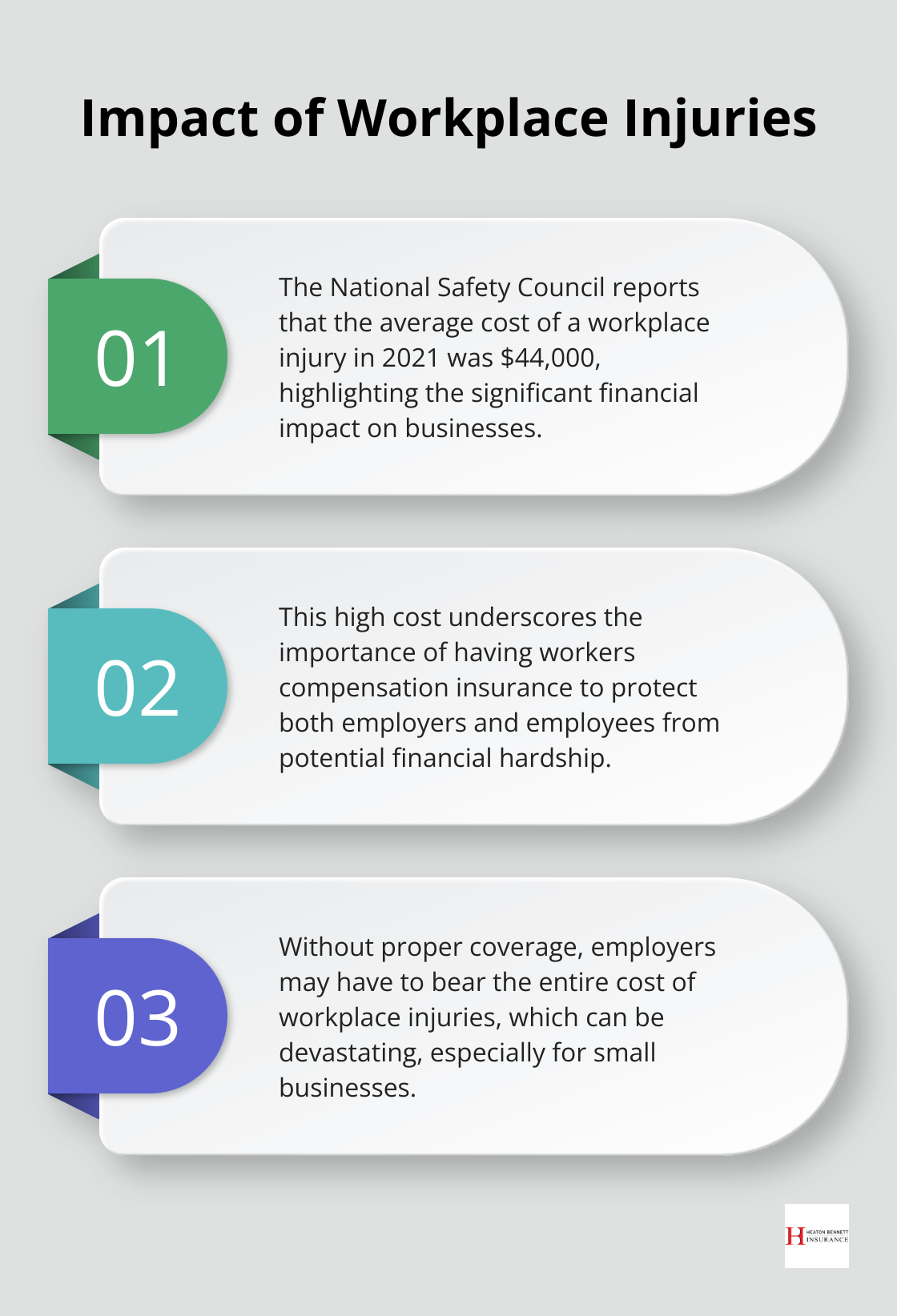

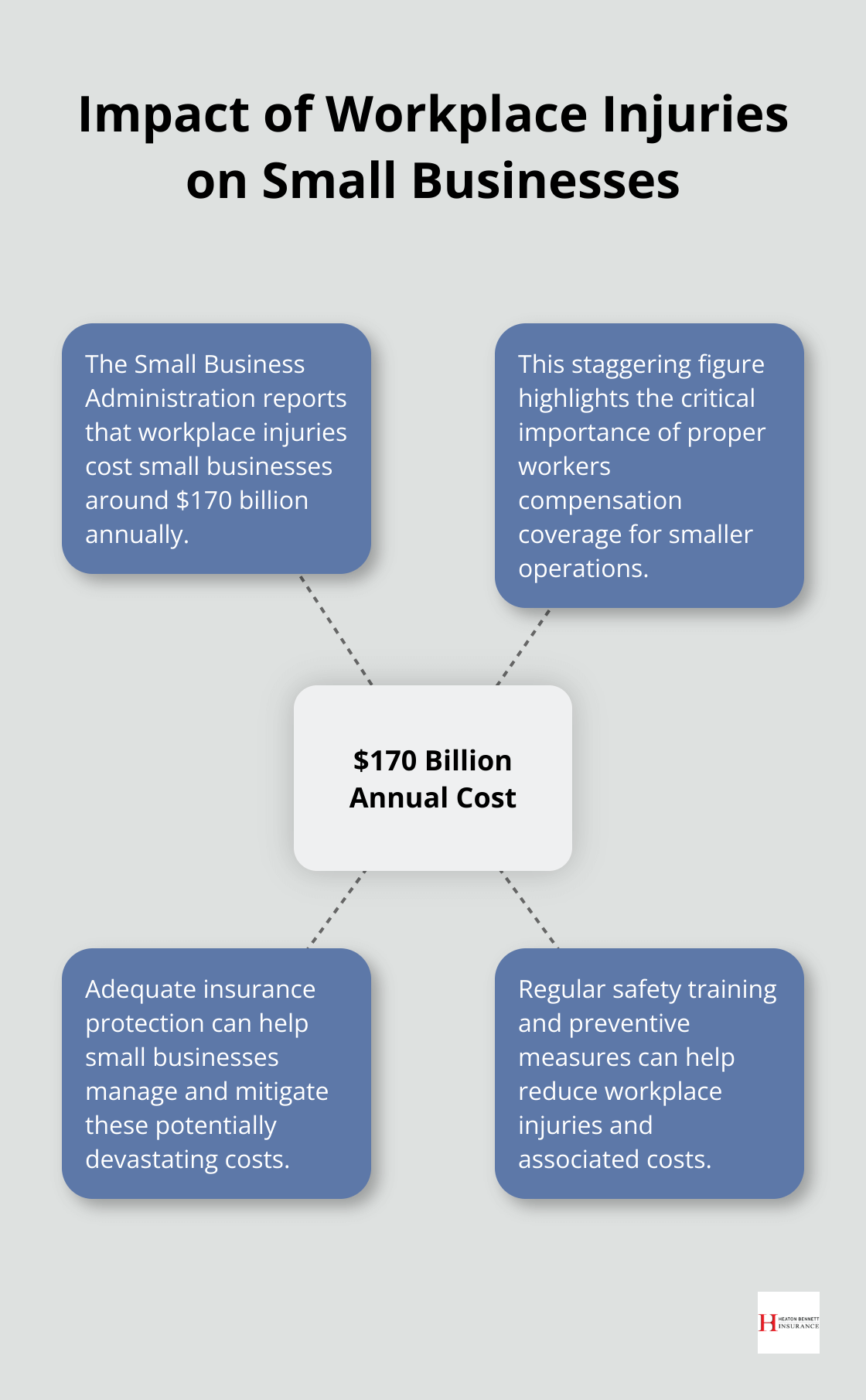

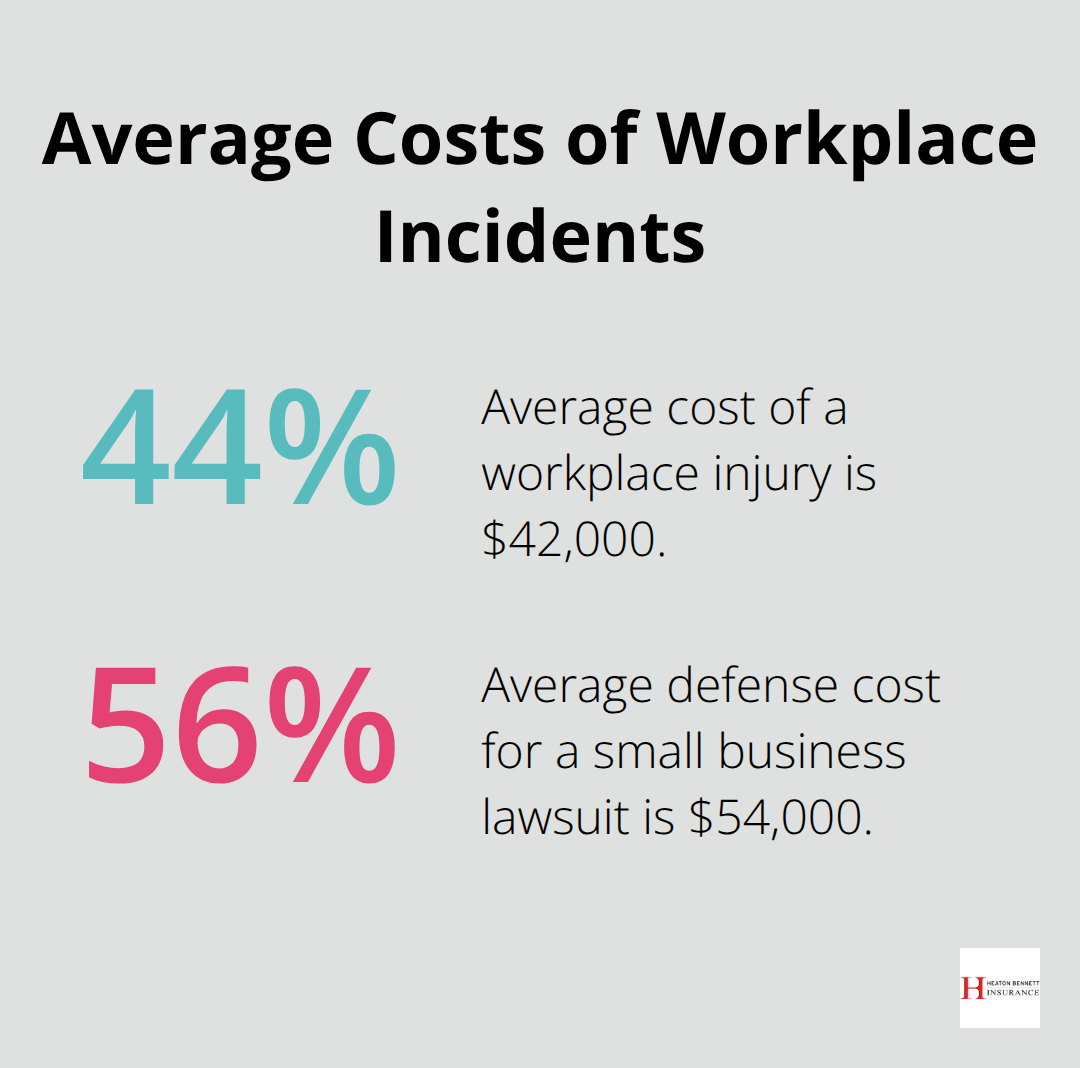

Workers compensation insurance serves as a critical safeguard for employers. Without this coverage, businesses face potentially devastating financial consequences. A single workplace injury could result in astronomical medical expenses, lost wages, and rehabilitation costs. The National Safety Council reports that the average cost of a workplace injury is $42,000 (a hefty sum for any business, but especially crippling for small enterprises).

Legal Shield Against Lawsuits

Workers compensation acts as a powerful legal buffer. It typically prevents employees from suing their employers for workplace injuries. This protection proves invaluable-the average defense cost for a small business lawsuit is $54,000 (according to a study by the U.S. Chamber Institute for Legal Reform). Workers comp not only helps avoid potential payouts but also saves on legal fees and preserves business reputation.

Employee Confidence and Loyalty Boost

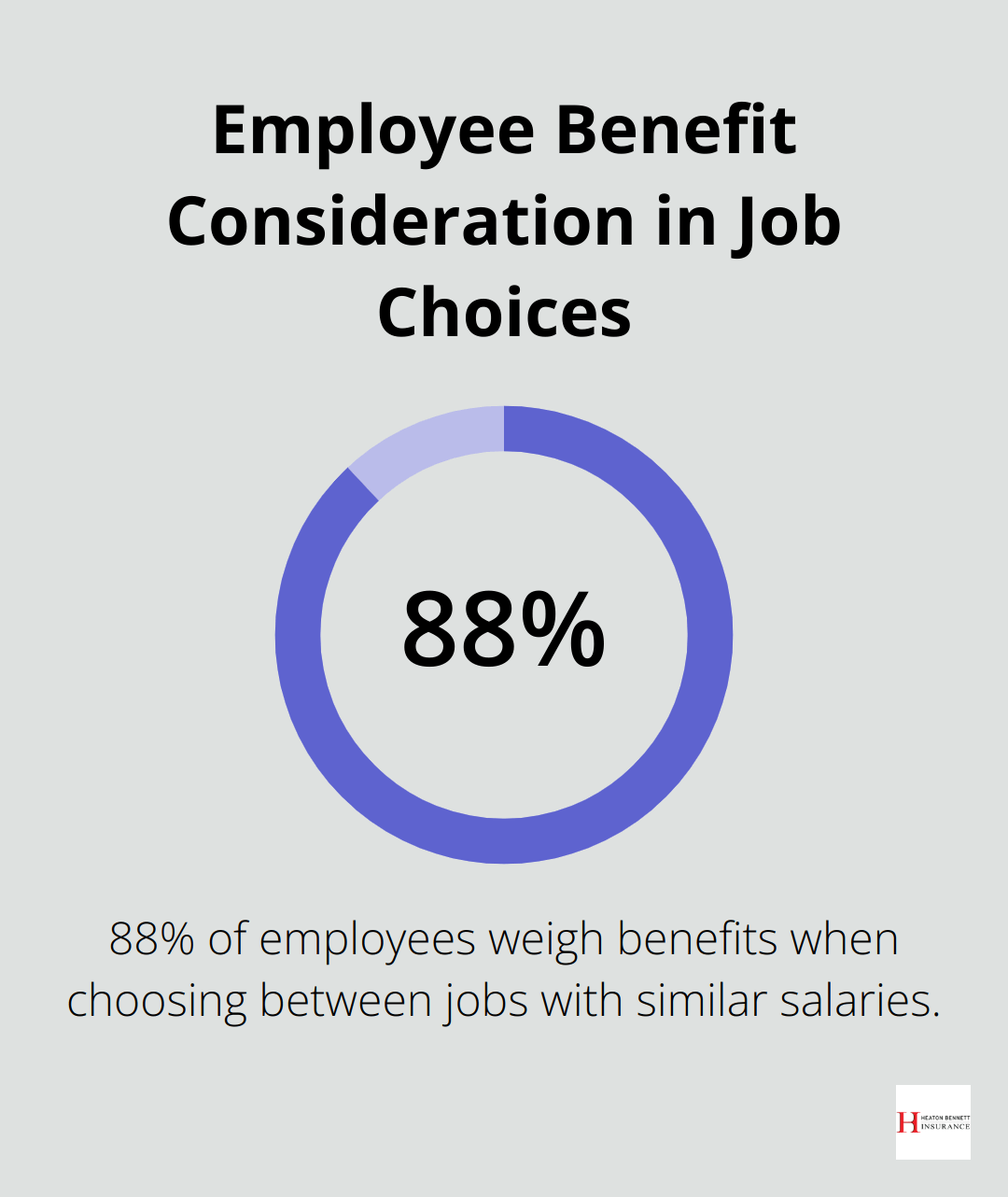

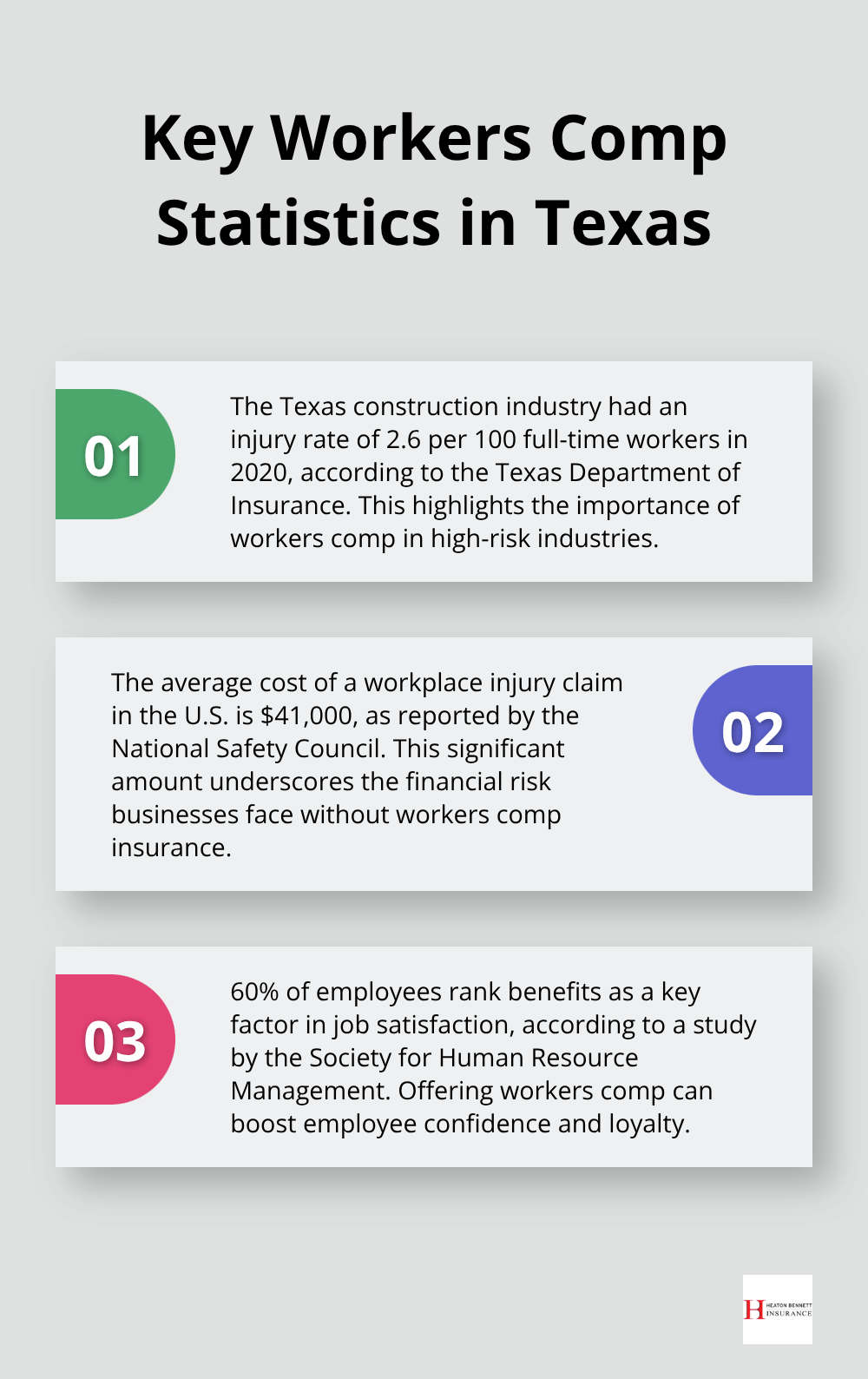

Offering workers compensation insurance sends a clear message to your team: their well-being matters. This can significantly impact employee morale and productivity. A study by the Society for Human Resource Management found that 60% of employees rank benefits as a key factor in job satisfaction. The provision of this essential safety net often leads to increased loyalty and potentially lower turnover rates.

Texas-Specific Considerations

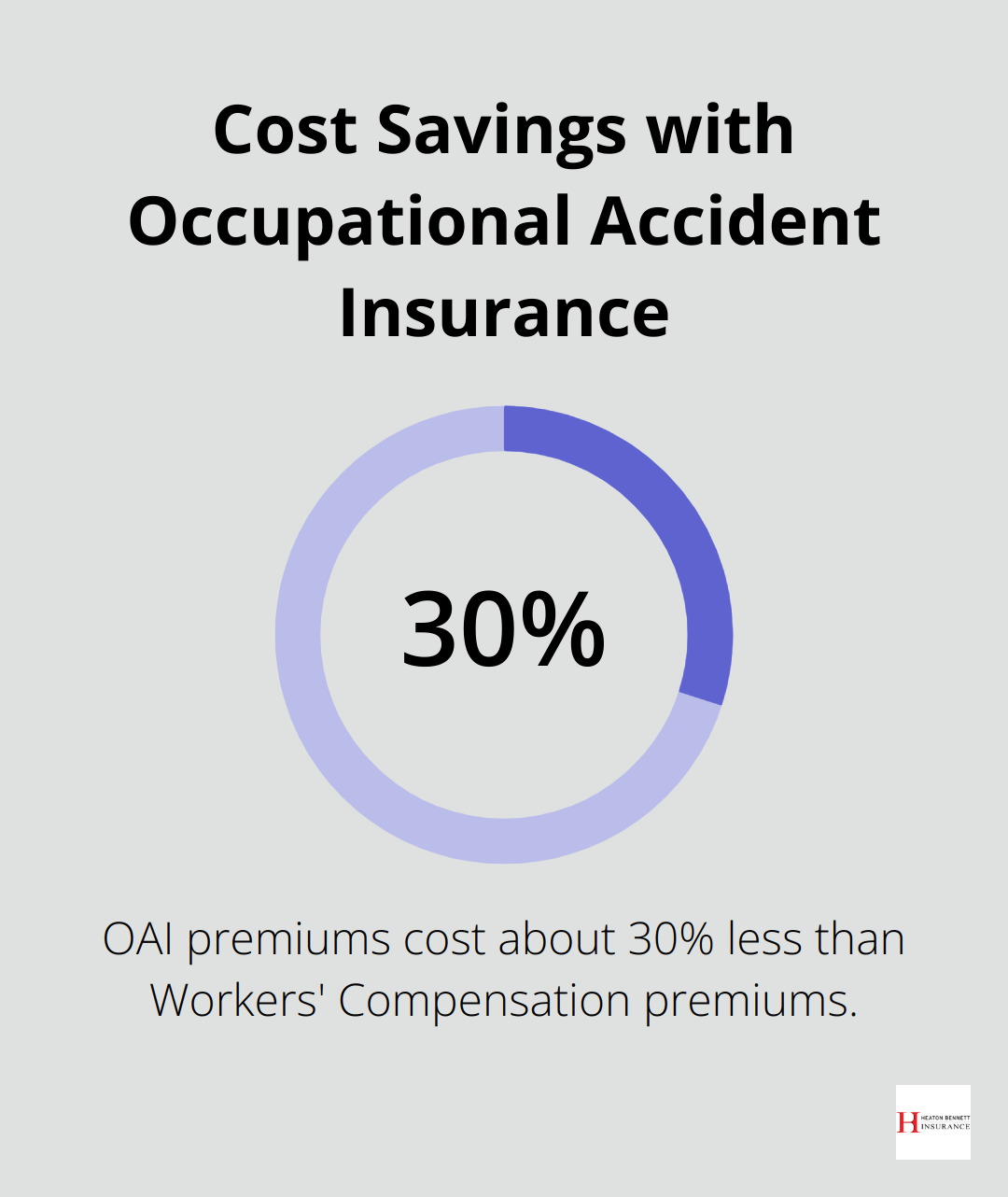

While Texas doesn’t mandate workers compensation for private employers, the benefits often outweigh the costs. Businesses should carefully evaluate their specific needs and risks when deciding on coverage. The unique landscape in Texas requires a thorough understanding of the implications of opting in or out of workers compensation insurance.

Navigating Complex Choices

The world of workers compensation insurance can seem daunting, with various options and considerations. Businesses must weigh factors such as industry risk, employee count, and financial capacity. Professional guidance can help in making informed decisions that align with both legal requirements and business goals.

As we explore the intricacies of determining if your business needs workers compensation insurance, it’s important to understand the specific regulations and exceptions that apply to Texas businesses.

Do You Need Workers Comp in Texas?

Texas Workers Comp Landscape

Texas stands out in its approach to workers compensation insurance. Unlike most states, Texas does not require private employers to carry this insurance. However, this unique stance does not negate the importance of such coverage for Texas businesses.

Industry Risk Assessment

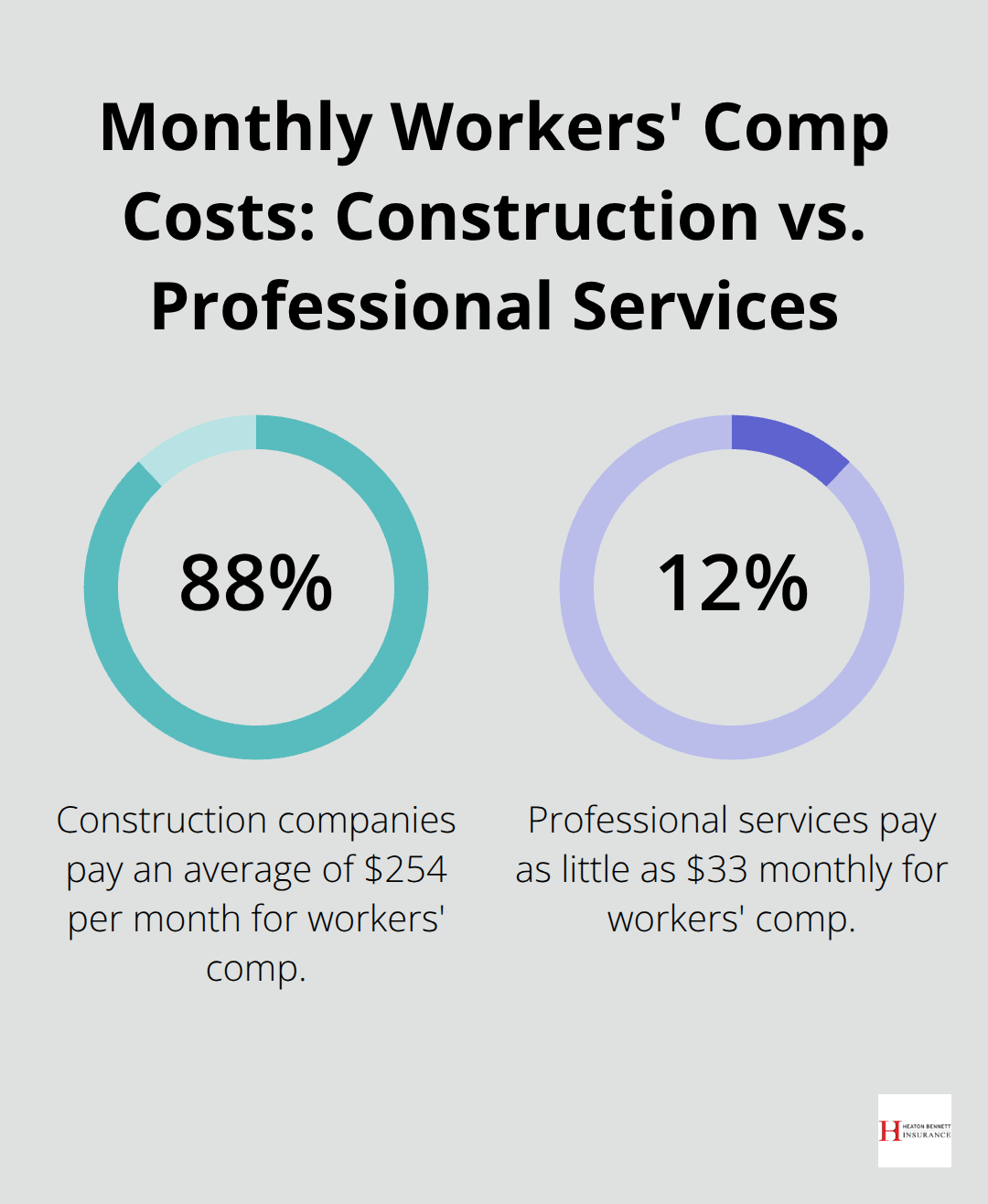

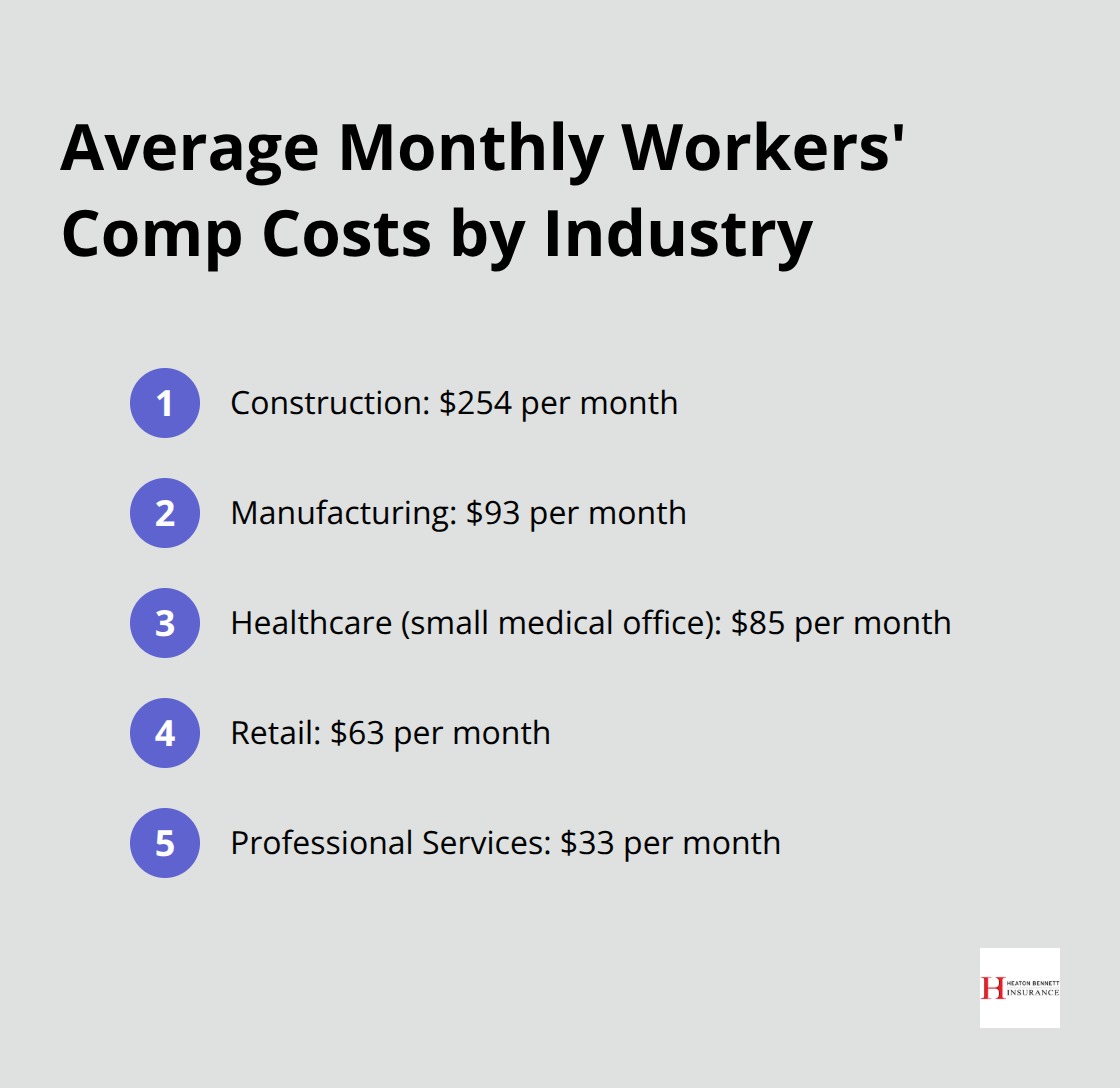

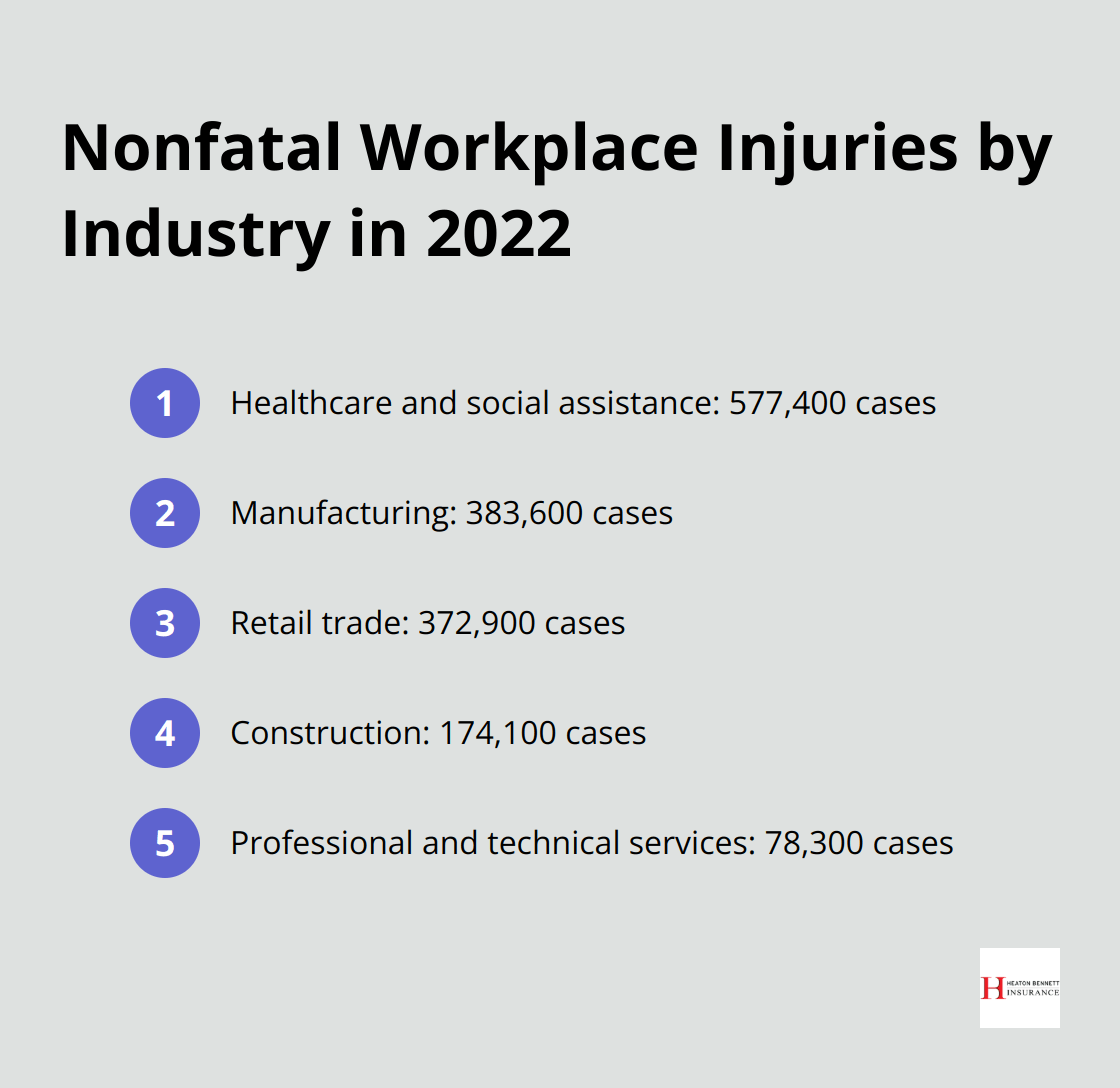

Your industry plays a significant role in determining your need for workers comp. High-risk industries like construction, manufacturing, and healthcare face a greater likelihood of workplace injuries. The construction industry in Texas had an injury rate of 2.6 per 100 full-time workers in 2020 (according to the Texas Department of Insurance). If you operate in a high-risk sector, workers comp becomes more of a necessity than an option.

Employee Count and Type

While Texas doesn’t set a minimum employee threshold for workers comp, the number of employees you have impacts your risk exposure. More employees generally mean a higher chance of workplace injuries. Consider the nature of your workforce: Do you employ full-time, part-time, or seasonal workers? Each category may have different insurance implications.

Client and Contract Requirements

Many clients, especially large corporations and government entities, require their contractors to carry workers compensation insurance. Without it, you might lose out on valuable business opportunities. For example, if you bid on a government construction project in Texas, workers comp is often a non-negotiable requirement.

Financial Implications of Going Without

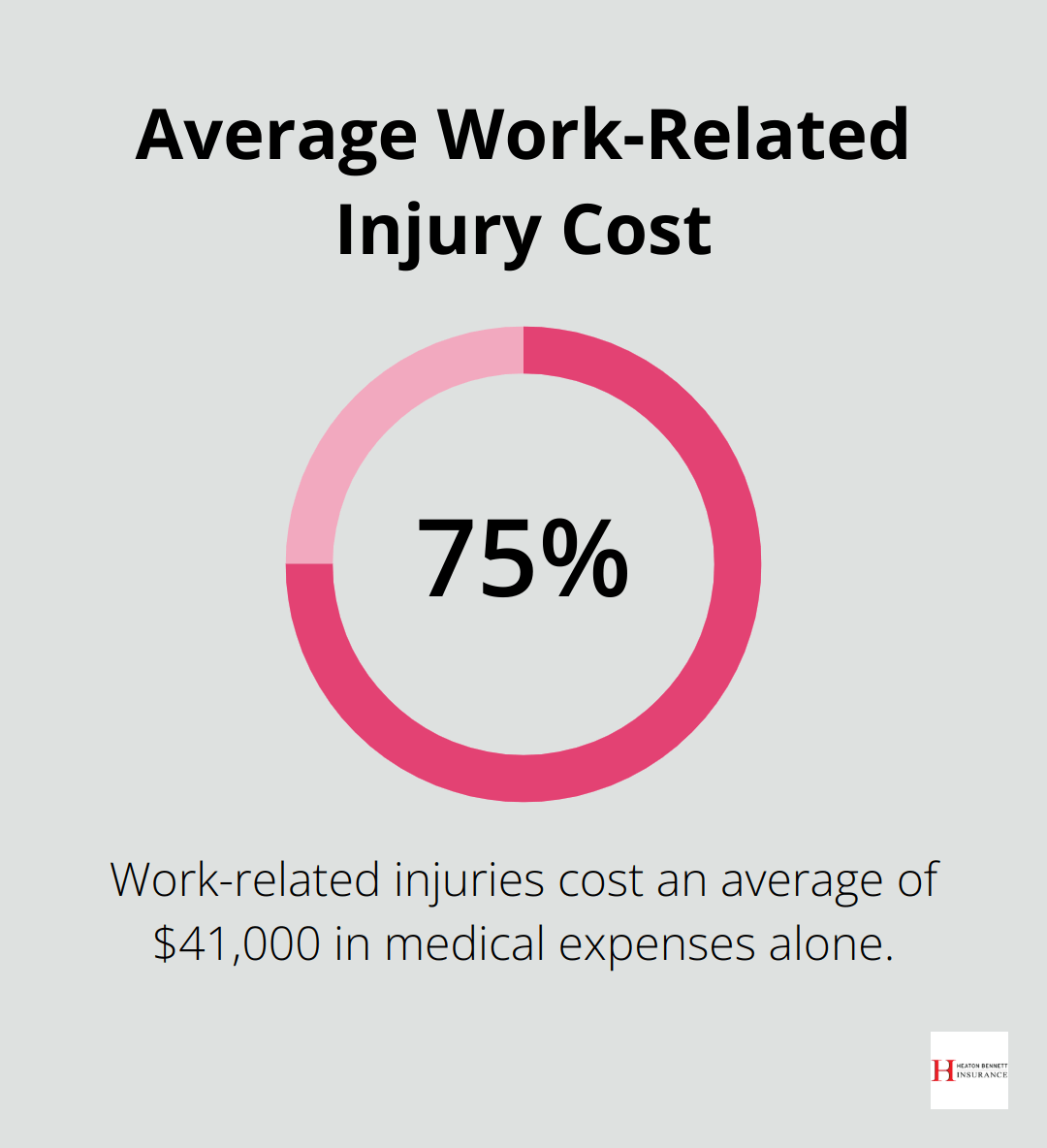

Opting out of workers comp in Texas means becoming a non-subscriber. This might save you money on premiums, but it exposes your business to potentially unlimited liability. A single workplace injury could lead to a lawsuit with no cap on damages. The average cost of a workplace injury claim in the U.S. is $41,000 (according to the National Safety Council). Can your business afford to pay this out of pocket?

Final Thoughts

Workers compensation insurance protects employers and employees in Texas, despite its non-mandatory status. The question “Do I need to get workers compensation insurance?” requires careful consideration from every Texas business owner. Factors to evaluate include industry risk level, employee count, and client requirements.

Workers comp offers financial protection against costly workplace injuries and shields businesses from lawsuits. It demonstrates to employees that their well-being matters, which can improve morale and productivity. A single accident could have devastating financial consequences for an uninsured business (the average cost of a workplace injury claim in the U.S. is $41,000).

At Heaton Bennett Insurance, we understand the unique insurance landscape in Texas. Our team of experts can guide you through the process of evaluating your workers compensation needs. We offer personalized solutions tailored to your specific business requirements, ensuring you have the right coverage without being tied to a single carrier.