How Much Does Workers Comp Cost for Small Businesses?

At Heaton Bennett Insurance, we understand that small business owners often wonder, “How much is workers’ compensation insurance for a small business?” It’s a critical question, as workers’ comp is not just a legal requirement in most states, but also a vital protection for both employers and employees.

The cost of workers’ compensation can vary significantly based on several factors, including your industry, payroll size, and claims history. In this post, we’ll break down these factors and provide insights to help you understand and potentially reduce your workers’ comp costs.

What Drives Workers Comp Costs?

Industry Risk Levels

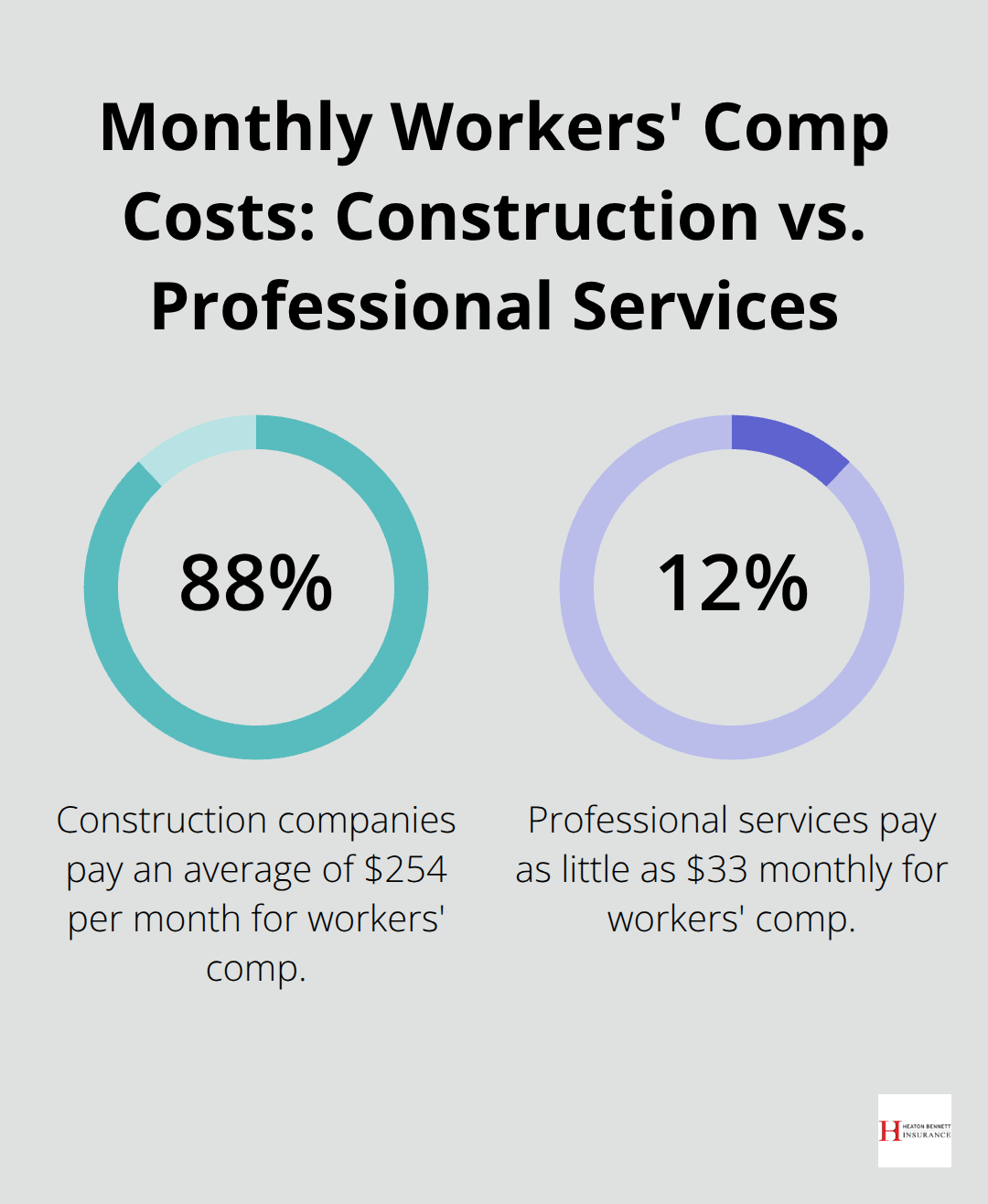

The nature of your business significantly influences workers’ comp costs. High-risk industries (such as construction or manufacturing) typically face higher premiums due to the increased likelihood of workplace injuries. Construction companies pay an average premium of $254 per month, according to Insureon data. Lower-risk sectors (like professional services or finance) may pay as little as $33 monthly.

Payroll and Employee Count

Your total payroll directly impacts your workers’ comp costs. Insurance providers calculate premiums based on a rate per $100 of payroll. As your payroll grows, your insurance costs increase. The number of employees also matters. Businesses with 3-5 employees pay an average of $56 monthly, while those with 10 or more employees see premiums around $116 per month (Insureon reports).

Claims History and Experience Modification

Your company’s past claims significantly affect your future premiums. Frequent or severe claims lead to higher rates. Insurance providers use an Experience Modification Rate (EMR) to adjust premiums based on your claims history compared to similar businesses in your industry. A lower EMR can result in substantial savings. A business with an EMR of 0.8 could see a 20% reduction in their base premium.

State-Specific Regulations

Workers’ comp requirements and costs vary widely by state. Texas businesses pay an average of $32 monthly for coverage, while Alabama businesses face much higher costs at $119 per month. Some states (North Dakota and Ohio) require businesses to purchase coverage exclusively from state funds. Understanding your state’s specific regulations ensures compliance and accurate budgeting.

These factors interplay to determine your workers’ comp costs. The next section will break down average costs by industry, providing a clearer picture of what small businesses in different sectors can expect to pay.

How Much Does Workers Comp Cost Across Industries?

Construction: High Risk, High Cost

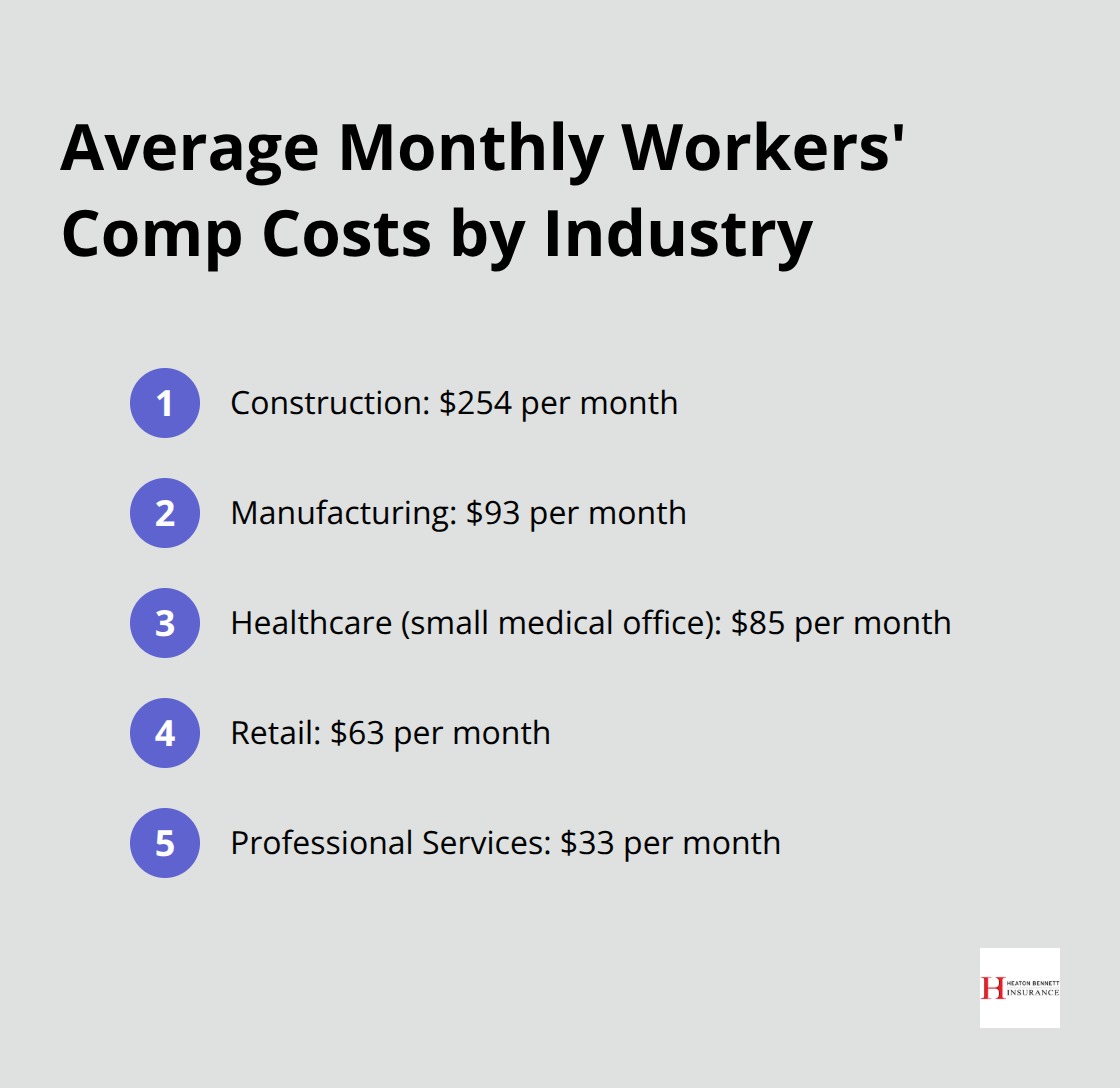

Construction companies face some of the highest workers’ comp premiums due to inherent risks. Insureon data shows these businesses pay an average of $254 per month for coverage. This high cost reflects the frequency and severity of injuries in the field (falls from heights and equipment-related accidents are common, leading to potentially expensive claims).

Manufacturing: Moderate to High Premiums

Manufacturing businesses typically see moderate to high workers’ comp costs, averaging $93 per month. The use of heavy machinery and repetitive motions contribute to injury risks. Costs can vary widely depending on the specific type of manufacturing (a food processing plant might face different risks than a metal fabrication shop, impacting their respective premiums).

Retail: Lower Risk, More Affordable

Retail businesses generally enjoy lower workers’ comp costs, with premiums averaging $63 per month. While slip-and-fall accidents or lifting injuries can occur, the overall risk is lower compared to industries like construction or manufacturing. Retail businesses with high-volume stock rooms or those dealing with heavy items might see higher rates.

Professional Services: Lowest Premiums

Professional services, including fields like accounting, consulting, and IT, typically have the lowest workers’ comp costs. These businesses pay an average of $33 per month. The low-risk nature of office work contributes to these affordable rates. However, even desk jobs can lead to repetitive strain injuries or slip-and-fall accidents, making coverage essential.

Healthcare: Varied Costs Based on Specialization

The healthcare industry sees a wide range of workers’ comp costs depending on the specific field. A small medical office might pay around $85 per month, while a home healthcare service could see higher premiums due to the varied work environments their employees encounter. Factors like patient handling, exposure to infectious diseases, and the use of specialized equipment all play a role in determining costs.

These figures represent averages, and actual costs may differ. Factors like location, claims history, and specific business operations all influence premiums. Small business owners should work closely with experienced insurance professionals to find the most cost-effective workers’ comp solutions tailored to their unique needs and industry risks.

The next section will explore strategies to reduce workers’ comp costs across all industries.

How Small Businesses Can Reduce Workers Comp Costs

At Heaton Bennett Insurance, we understand the importance of managing workers’ compensation costs for small businesses. Here are effective strategies to keep your premiums low while maintaining robust coverage for your employees.

Create a Safer Workplace

A comprehensive safety program serves as your primary defense against high workers’ comp costs. The National Safety Council reports that for every dollar invested in safety, businesses can expect to save $4-6 in reduced injuries. To improve workplace safety:

- Conduct regular safety audits to identify potential hazards

- Train employees on proper safety procedures

- Provide necessary protective equipment

A safer workplace leads to fewer claims and lower premiums (a win-win for both employers and employees).

Establish a Return-to-Work Program

A well-designed return-to-work program can reduce workers’ comp costs by up to 40% (according to studies by the Workers Compensation Research Institute). These programs help injured employees transition back to work with modified duties. To implement an effective program:

- Work with medical providers to understand an employee’s capabilities

- Design transitional work that aids recovery while benefiting your business

- Communicate clearly with employees about the program’s benefits

Improve Claims Management

Efficient claims management plays a vital role in controlling costs. The Hartford found that reporting delays of just one week can increase claim costs by 18%. To streamline your claims process:

- Report injuries promptly

- Establish a clear process for reporting and managing claims

- Maintain proper documentation to prevent minor issues from escalating

Consider Pay-As-You-Go Options

Pay-as-you-go workers’ comp plans offer advantages for small businesses with fluctuating payrolls. These plans:

- Base premiums on actual payroll rather than estimates

- Potentially save money during slower periods

- Help avoid large year-end audit bills

- Improve cash flow management

Work with an Experienced Insurance Agent

An knowledgeable insurance agent can become your greatest asset in managing workers’ comp costs. They can:

- Help you navigate complex state regulations

- Ensure proper employee classification

- Identify cost-saving opportunities unique to your business

Small businesses that implement these strategies can significantly reduce their workers’ compensation costs while still providing essential protection for their employees. The key lies in proactive management, safety prioritization, and collaboration with insurance professionals who understand your unique business needs.

Final Thoughts

Small business owners must understand the factors that influence workers’ compensation costs. Industry risk, payroll size, claims history, and state regulations all affect premiums. Tailored coverage proves essential, as each business faces unique risks and needs.

We at Heaton Bennett Insurance specialize in customized workers’ compensation solutions for small businesses in Austin, Texas, and beyond. Our team guides clients through the process of obtaining the right coverage for their specific needs. We access multiple carriers to find competitive rates without sacrificing quality.

Our “Security Snapshot” process thoroughly assesses your business’s risks and requirements. This approach creates a comprehensive insurance package that protects your employees and bottom line. Contact us to navigate the complexities of workers’ compensation insurance and answer the question: “How much is workers’ compensation insurance for a small business?”