Workers Comp Insurance for Self-Employed: What to Know

Are you self-employed and wondering about workers’ compensation insurance? You’re not alone. Many independent professionals struggle to understand their obligations and options when it comes to this crucial coverage.

At Heaton Bennett Insurance, we’ve helped countless self-employed individuals navigate the complex world of workers’ compensation insurance. In this post, we’ll break down what you need to know about workers’ compensation insurance for self-employed professionals, including legal requirements, benefits, and how to obtain coverage.

What Is Workers Comp for Self-Employed?

A Safety Net for Independent Professionals

Workers’ compensation insurance acts as a safety net for self-employed professionals. It covers medical expenses and lost wages if you suffer an injury or illness due to work-related activities. This insurance isn’t just for large companies; it’s equally important for independent contractors and freelancers.

State-Specific Legal Requirements

The legal landscape for workers’ comp varies significantly across states. Texas doesn’t mandate workers’ comp for any business, while California requires even some independent contractors to carry this insurance. It’s essential to check your local regulations to avoid potential fines or legal issues.

Coverage Beyond Standard Health Insurance

Many self-employed individuals incorrectly assume their health insurance suffices. However, standard health policies often exclude work-related injuries. Workers’ comp fills this critical gap, covering medical bills and providing income replacement if a job-related incident prevents you from working.

Financial Protection for Your Business

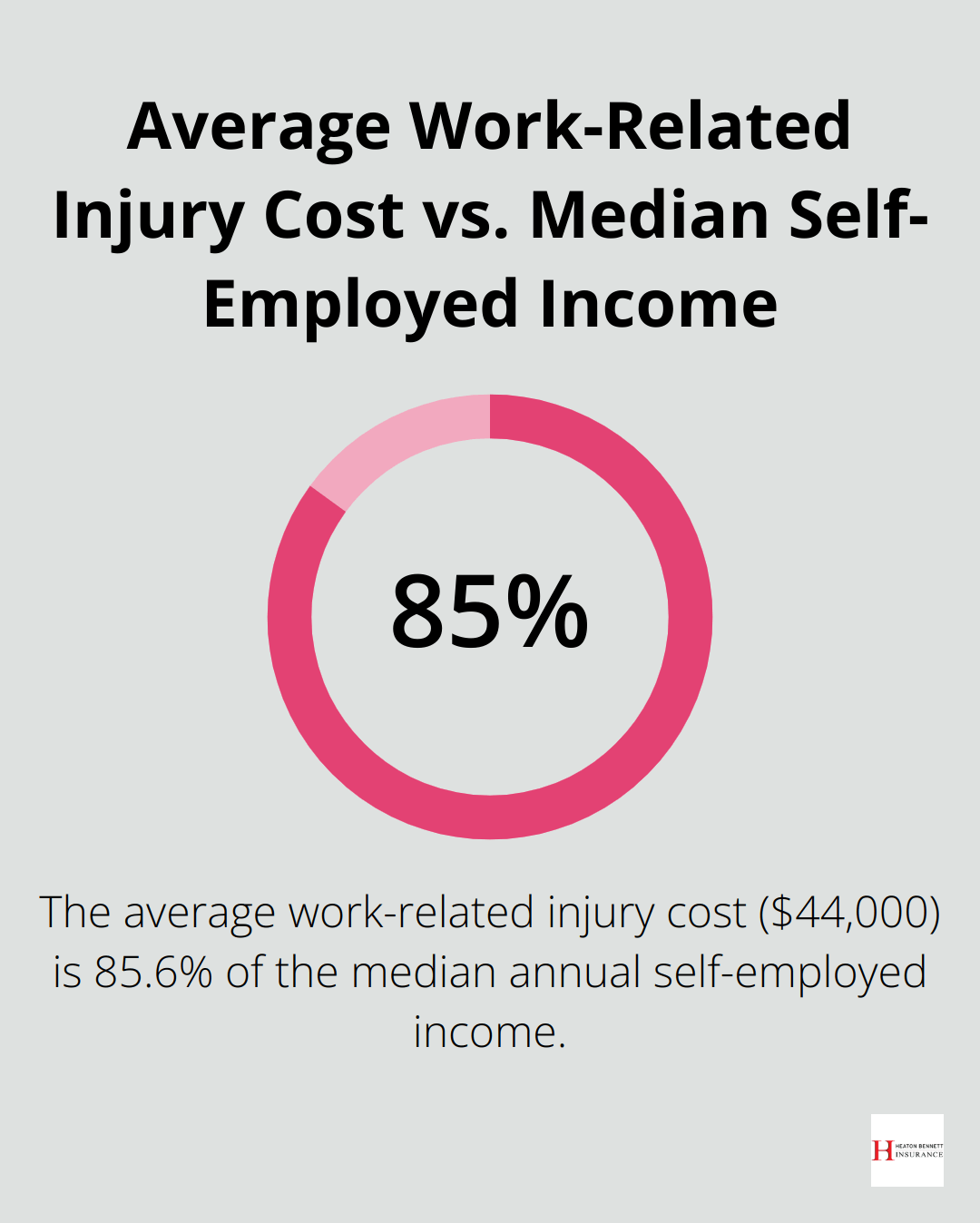

Self-employment comes with inherent risks. A serious injury could derail your business and personal finances. Workers’ comp serves as a financial buffer, potentially saving you from bankruptcy in worst-case scenarios. The National Safety Council reports that the average work-related injury costs $44,000 in medical expenses and lost wages.

The Value of Peace of Mind

While workers’ comp represents an additional expense, the protection it offers often outweighs the cost for many independent workers. It provides peace of mind, allowing you to focus on growing your business without worrying about the financial impact of potential work-related injuries.

As we move forward, let’s explore the factors that affect workers’ compensation for self-employed individuals, including the type of work you do and the associated risks.

What Shapes Your Workers’ Comp Needs?

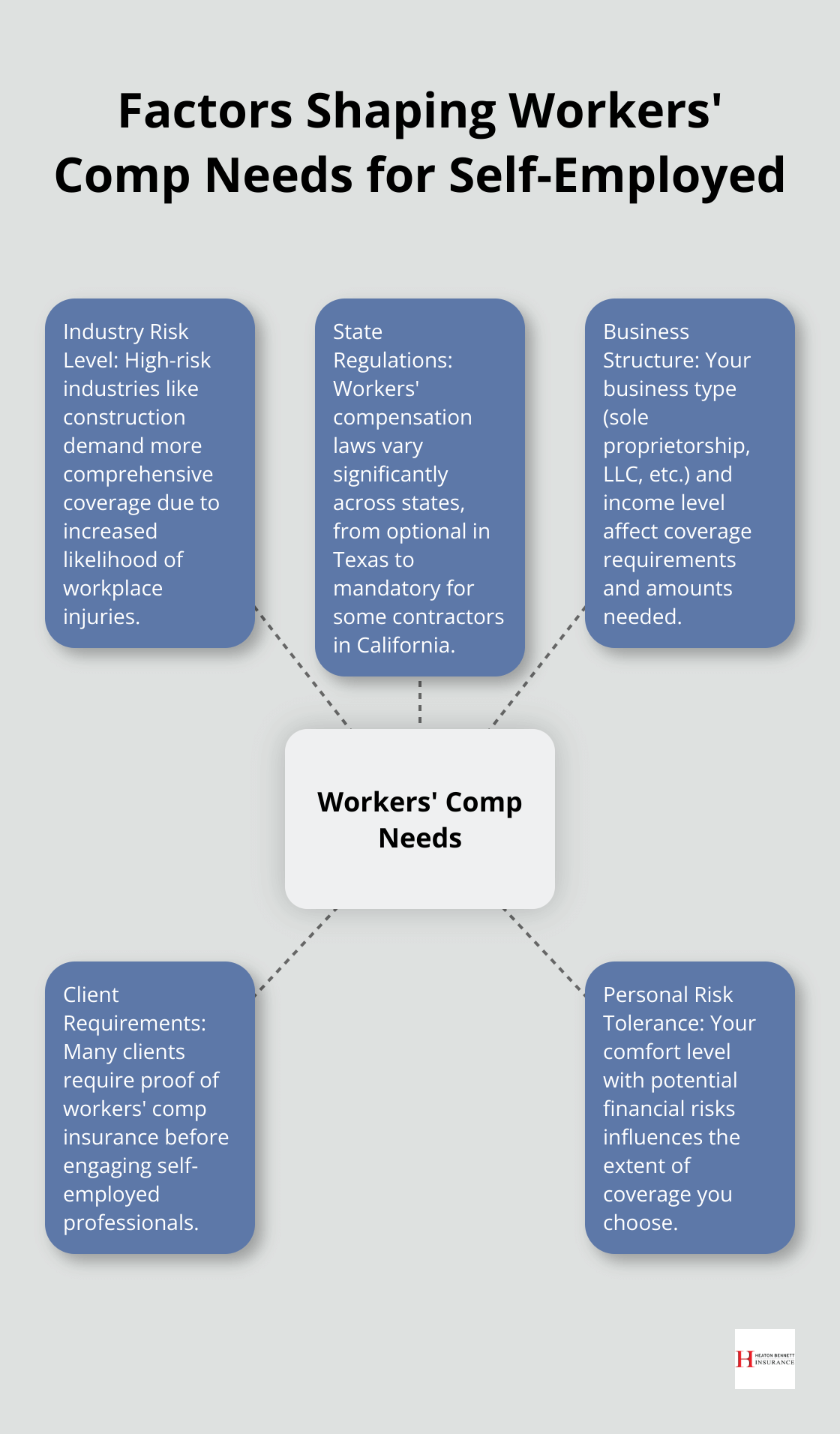

Industry Risk Level

Your line of work significantly influences your workers’ comp requirements. High-risk industries (such as construction or manufacturing) typically demand more comprehensive coverage due to the increased likelihood of workplace injuries. The U.S. Bureau of Labor Statistics reports that construction workers face a fatal injury rate nearly three times higher than the average for all industries. Office-based professions like consulting or graphic design generally have lower risk profiles and may require less extensive coverage.

State-Specific Regulations

Workers’ compensation laws differ dramatically across states. Texas makes workers’ comp optional for most employers, while California mandates coverage even for some independent contractors. Understanding your local requirements is essential to avoid potential legal issues. The National Federation of Independent Business (NFIB) notes that fines for non-compliance can range from $1,000 to $10,000 per violation in some states.

Business Structure and Income

Your business structure and income level impact your workers’ comp needs. Sole proprietors often face different requirements than incorporated businesses. Your income level affects the amount of coverage you might need to adequately protect your earnings in case of a work-related injury. The Workers Compensation Research Institute found that the average workers’ comp claim costs about $40,000, underscoring the importance of adequate coverage relative to your income.

Client Requirements

Many clients require proof of workers’ compensation insurance before engaging with self-employed professionals. This requirement protects clients from potential liability if you suffer an injury while working on their projects. Meeting these client demands can open up new business opportunities and demonstrate your professionalism.

Personal Risk Tolerance

Your personal risk tolerance plays a role in determining your workers’ comp needs. Some self-employed individuals prefer comprehensive coverage for peace of mind, while others might opt for minimal coverage to reduce expenses. Consider your comfort level with potential financial risks and how a work-related injury could impact your business and personal life.

As you weigh these factors, you’ll need to explore your options for obtaining workers’ comp coverage. The next section will guide you through the process of securing the right insurance for your self-employed status.

How to Obtain Workers’ Comp as a Self-Employed Professional

Exploring Your Coverage Options

Self-employed individuals have multiple avenues for obtaining workers’ comp coverage. State-run insurance funds offer competitive rates in some areas. Private insurance companies provide coverage, often with more flexible options. The Texas Department of Insurance reports that 28% of employers in the state obtain coverage through the state-run fund, while the rest choose private insurers.

Some professional associations offer group workers’ comp policies, which can be more cost-effective for members. The National Association for the Self-Employed (NASE) provides access to such group policies, potentially saving members up to 40% on premiums compared to individual plans.

Understanding the Costs

The cost of workers’ comp insurance varies widely based on several factors. Your industry risk level is a primary determinant. According to the National Council on Compensation Insurance (NCCI), the average workers’ comp rate for office workers is $0.35 per $100 of payroll, while construction workers might pay $8.99 per $100.

Your claims history also impacts your premiums. A clean record can lead to lower rates, while previous claims might increase your costs. The Insurance Information Institute notes that a single claim can increase premiums by 20-40% for three years.

Location plays a role too. The Oregon Department of Consumer and Business Services reports that workers’ comp rates can vary by as much as 380% between states (with California having the highest rates and North Dakota the lowest).

Navigating the Application Process

To apply for workers’ comp insurance, you must provide detailed information about your business. This typically includes:

- Your business structure (sole proprietorship, LLC, etc.)

- Annual revenue and payroll estimates

- Detailed description of your work activities

- Number of employees or subcontractors, if any

- Past claims history

Many insurers now offer online applications, which streamline the process. However, working with an experienced agent can help you navigate complex questions and ensure you get the most appropriate coverage.

The approval process usually takes 24-48 hours but can be longer for high-risk industries or complex business structures. Once approved, you’ll receive a certificate of insurance, which you can provide to clients or regulatory bodies as proof of coverage.

Regular Policy Reviews

Workers’ comp requirements can change, so it’s wise to review your coverage annually. Regular policy reviews ensure your coverage evolves with your business needs. This proactive approach helps you maintain adequate protection while potentially identifying cost-saving opportunities.

Seeking Expert Guidance

Navigating the complexities of workers’ comp insurance can be challenging for self-employed professionals. Consider consulting with insurance experts who specialize in coverage for independent contractors and small businesses. These professionals can provide valuable insights into your specific needs and help you find the most suitable policy.

Final Thoughts

Workers’ compensation insurance for self-employed professionals protects your business and livelihood. This coverage shields you from financial devastation in case of work-related injuries or illnesses. It provides a safety net that standard health insurance often fails to address, allowing you to focus on growing your business without constant worry about potential risks.

The legal requirements and benefits of workers’ comp vary based on your industry, location, and business structure. Understanding these elements will help you make informed decisions about your insurance needs. You must consider factors such as state regulations, client requirements, and your personal risk tolerance when choosing the right coverage.

We at Heaton Bennett Insurance offer tailored insurance solutions for self-employed individuals and businesses in Austin, Texas. Our team can guide you through the complexities of workers’ comp and help you find the right coverage to protect your finances (both business and personal). Don’t leave your hard-earned success to chance – take action today to safeguard your self-employed venture with appropriate workers’ compensation insurance.