What Does Full Coverage Auto Insurance Actually Cover?

At Heaton Bennett Insurance, we often hear the question: “What does full coverage auto insurance actually cover?” It’s a common misconception that this type of policy protects you from everything.

In reality, full coverage auto insurance typically combines several types of coverage to provide comprehensive protection for your vehicle and financial well-being. Let’s break down what’s usually included and why it matters for your peace of mind on the road.

What’s Really Included in Full Coverage Auto Insurance?

The Core Components of Full Coverage

Full coverage auto insurance isn’t a specific policy type, but a combination of different coverages that provide comprehensive protection for your vehicle. Many drivers misunderstand what full coverage actually includes.

Typically, full coverage auto insurance consists of three main components:

- Liability protection (mandatory in most states)

- Collision coverage

- Comprehensive coverage

Liability protection covers damages you cause to others. Collision coverage pays for repairs to your vehicle after an accident, regardless of fault. Comprehensive coverage protects against non-collision incidents like theft, vandalism, or natural disasters.

Beyond the Basics

Many drivers assume full coverage protects them from every possible scenario, but this isn’t true. Additional coverages often not included in standard full coverage policies are:

- Personal injury protection

- Uninsured/underinsured motorist coverage

- Roadside assistance

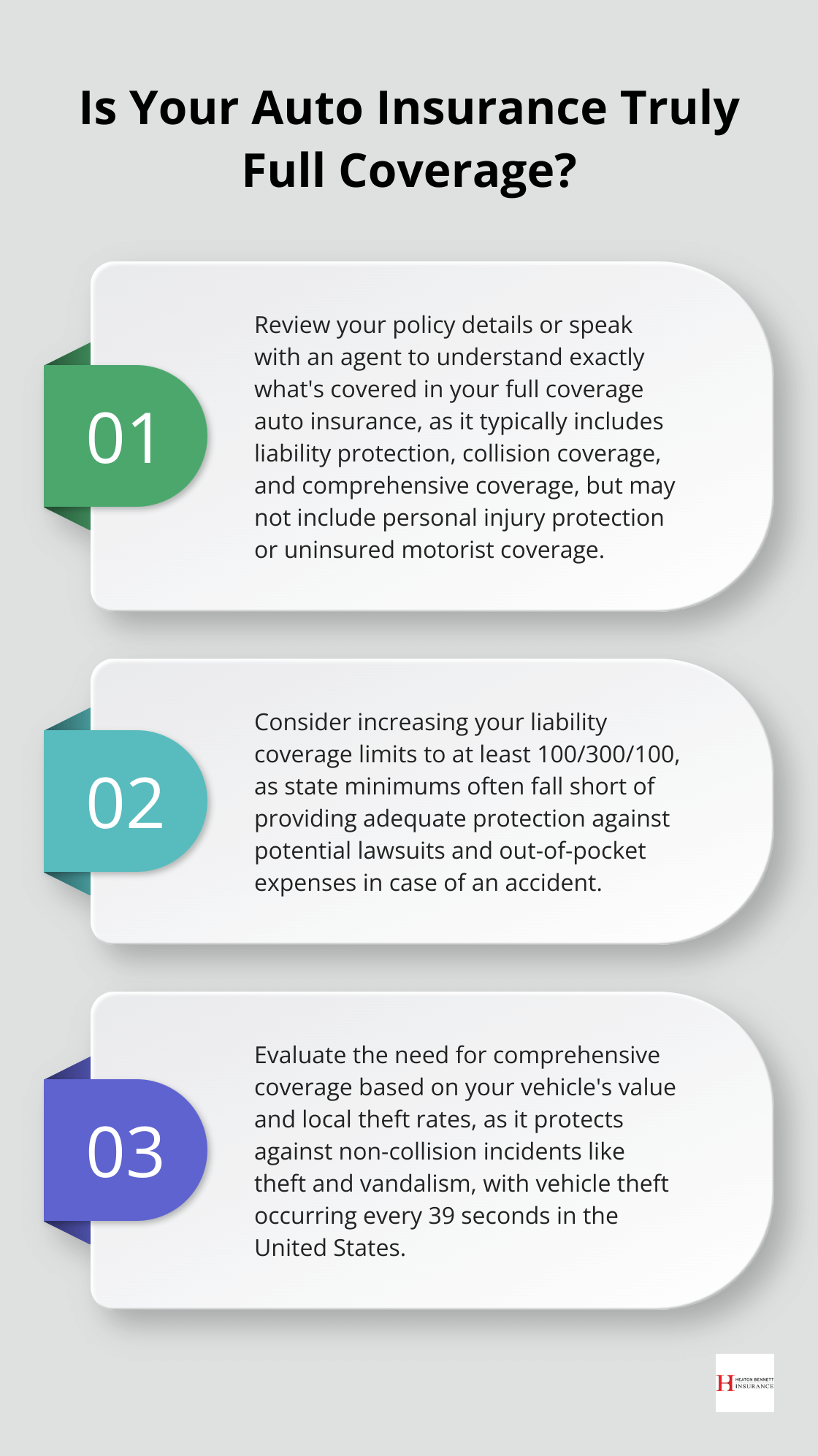

It’s important to review your policy details or speak with an agent to understand exactly what’s covered (and what’s not).

The Cost Factor

The National Association of Insurance Commissioners reports that the average auto insurance expenditure in the U.S. increased by 6.1% to $1,127 in 2022. This figure varies significantly based on coverage levels, location, and individual factors. Florida, for example, had the highest average expenditure at $1,625.

When you consider full coverage, it’s essential to weigh the additional cost against the potential financial protection it provides. Some factors that influence the cost of full coverage include:

- Your driving record

- The make and model of your vehicle

- Your location

- Your age and gender

- Your credit score (in some states)

Tailoring Your Coverage

Every driver’s needs are unique, which is why it’s crucial to tailor your coverage to your specific situation. Some questions to ask yourself when considering full coverage include:

- What’s the value of your vehicle?

- Do you have a car loan or lease?

- How much could you afford to pay out-of-pocket in case of an accident?

- What are the traffic and weather conditions like in your area?

By answering these questions, you can better determine if full coverage is right for you and what additional coverages you might need.

As we move forward, let’s examine each component of full coverage auto insurance in more detail, starting with the foundation: liability coverage.

Understanding Liability Coverage in Auto Insurance

The Foundation of Auto Insurance

Liability coverage forms the core of any auto insurance policy, including full coverage plans. This essential component protects you financially if you cause harm to others or their property while driving.

Bodily Injury and Property Damage Liability Explained

Liability coverage consists of two main parts:

- Bodily Injury Liability: This covers medical expenses, lost wages, and legal fees if you injure someone in an accident.

- Property Damage Liability: This pays for repairs or replacement of other people’s property you damage in a collision.

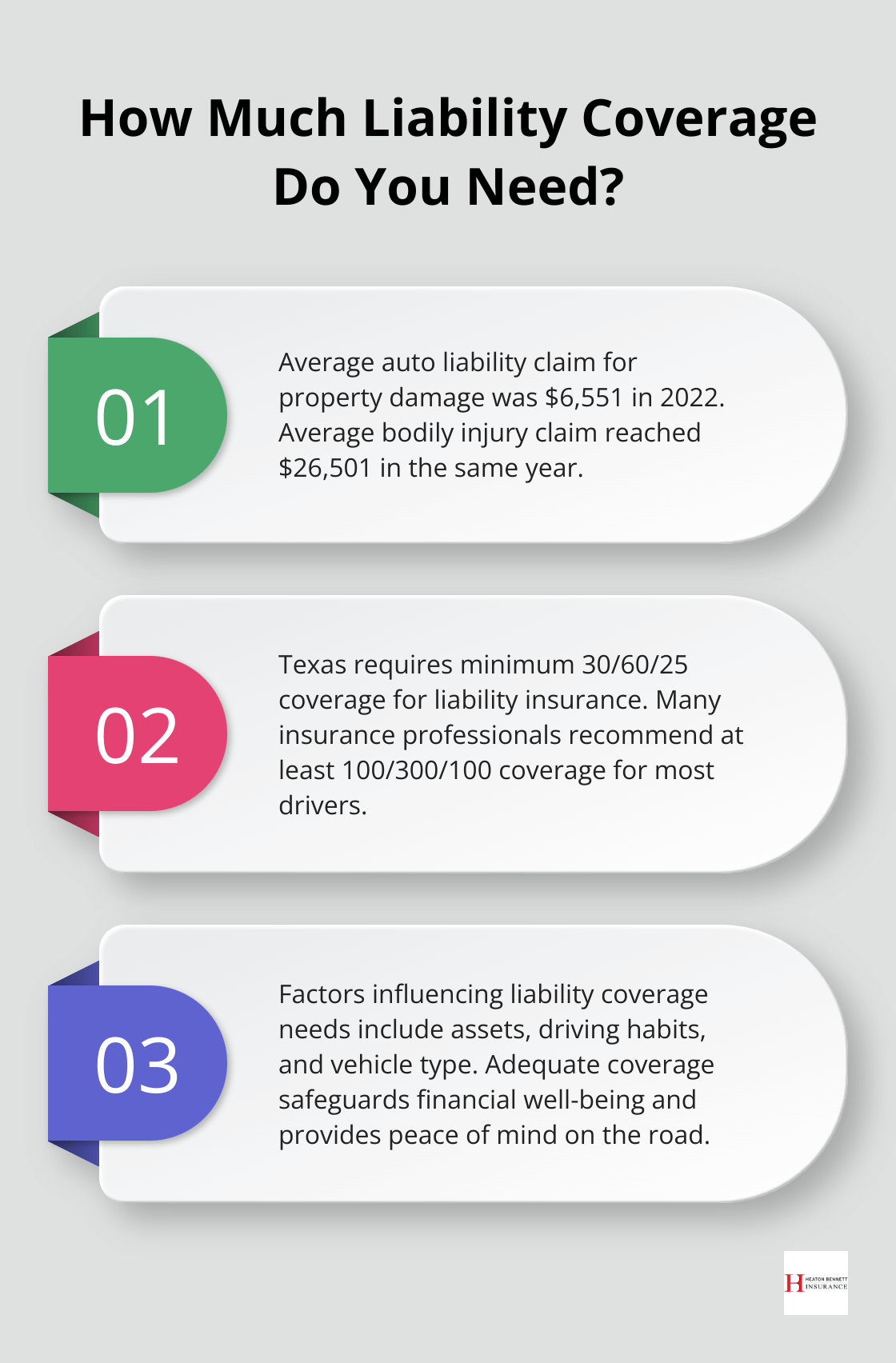

The Insurance Services Office (ISO) reported that in 2022, the average auto liability claim for property damage was $6,551, while the average bodily injury claim reached $26,501. These figures underscore the potential financial impact of accidents (and the importance of sufficient coverage).

State Minimums vs. Recommended Coverage Levels

States set minimum liability requirements, but these often fall short of providing adequate protection. For example, Texas requires 30/60/25 coverage ($30,000 per person for bodily injury, $60,000 per accident for bodily injury, and $25,000 for property damage).

However, considering the average claim amounts mentioned earlier, these minimums may expose you to significant out-of-pocket expenses. Many insurance professionals recommend coverage limits of at least 100/300/100 for most drivers.

Factors Influencing Your Liability Coverage Needs

Your ideal liability coverage depends on various factors:

- Assets: The more assets you own, the more coverage you need to protect them from potential lawsuits.

- Driving habits: Frequent driving in high-traffic areas or long commutes might warrant higher limits.

- Vehicle type: Operating a larger vehicle that could cause more damage in an accident might necessitate increased coverage.

The Long-Term Benefits of Adequate Coverage

While it might seem tempting to opt for state minimums to save on premiums, the potential long-term costs of inadequate coverage far outweigh the short-term savings. Proper insurance coverage safeguards your financial well-being and provides peace of mind on the road.

As we explore the components of full coverage auto insurance, it’s clear that liability coverage lays the groundwork. However, to truly protect your vehicle and finances, additional coverages play a vital role. Let’s examine these supplementary protections in the next section.

What Extra Protection Does Full Coverage Offer?

Comprehensive Coverage: Protection Beyond Collisions

Full coverage auto insurance extends protection beyond basic liability. Comprehensive coverage shields your vehicle from non-collision incidents such as theft, vandalism, fire, natural disasters, and animal damage. The National Insurance Crime Bureau reports that a vehicle is stolen every 39 seconds in the United States. This statistic highlights the importance of comprehensive coverage, particularly in urban areas with higher theft rates.

If hail damages your car or thieves steal it from your driveway, comprehensive coverage will help cover repair or replacement costs. Without this protection, you would bear the full expense out of pocket.

Collision Coverage: Safeguarding Your Vehicle

Collision coverage pays for repairs to your vehicle after an accident, regardless of fault. This protection proves particularly valuable for newer or more expensive vehicles where repair costs can be substantial.

The Highway Loss Data Institute reports that the average collision claim in 2023 was $9,655 for passenger vehicles. This figure continues to rise due to increasing repair costs and more advanced vehicle technologies. Collision coverage ensures you avoid a hefty bill after an accident.

Personal Injury Protection: Coverage for Medical Expenses

Personal Injury Protection (PIP) or Medical Payments coverage assists with medical expenses for you and your passengers after an accident, regardless of fault. This can include hospital bills, lost wages, and even funeral expenses in severe cases.

The Insurance Research Council found that the average auto injury claim cost exceeded $20,000 in 2022. PIP can help bridge the gap between your health insurance coverage and these unexpected medical costs.

Uninsured/Underinsured Motorist Coverage: Protection from Others

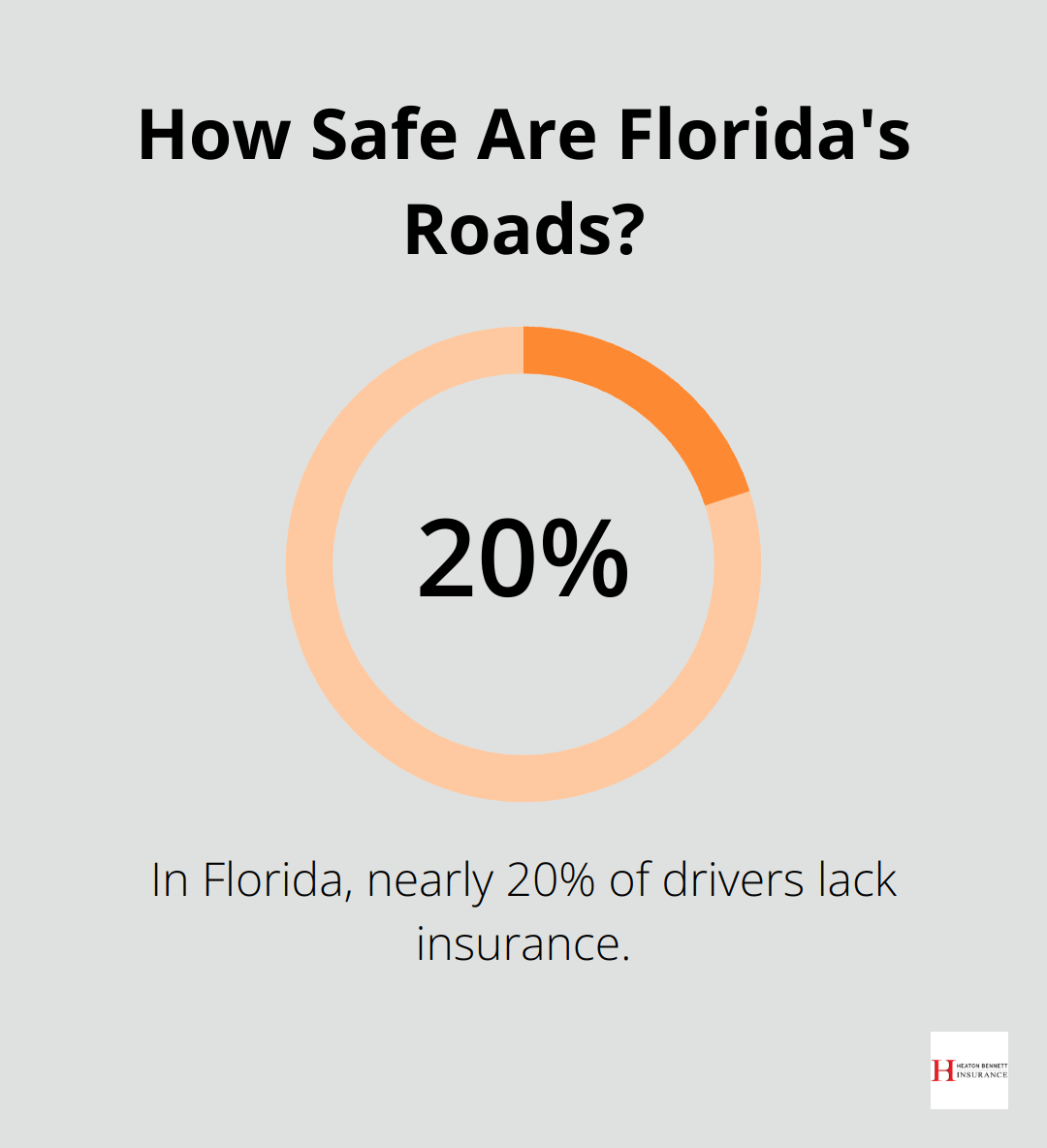

Despite legal requirements, the Insurance Information Institute estimates that about 12.6% of motorists lack insurance. Uninsured/Underinsured Motorist coverage protects you if you’re in an accident with a driver who doesn’t have insurance or doesn’t have enough coverage.

This coverage can save you financially, especially in states with high rates of uninsured drivers. For instance, in Florida, nearly 20% of drivers lack insurance, making this coverage particularly important.

Full coverage auto insurance provides a robust safety net for various scenarios. While it may come at a higher premium, the potential financial protection it offers can far outweigh the cost. Insurance professionals work closely with clients to determine the right balance of coverage and cost for their unique situations.

Final Thoughts

Full coverage auto insurance offers protection against various road risks, but it doesn’t cover everything. This package typically includes liability protection, collision coverage, and comprehensive coverage. These components work together to safeguard you financially in case of accidents, theft, or other unforeseen events. However, you should review your policy details carefully to understand any exclusions or limitations.

When choosing the right coverage, you should consider your vehicle’s value, driving habits, and financial situation. Full coverage might be a wise investment for newer or more expensive cars. You should also reassess your coverage regularly to ensure it still meets your requirements as your needs can change over time.

At Heaton Bennett Insurance, we help you find the right balance of coverage and cost for your unique situation. Our team offers personalized guidance to ensure you have the protection you need (without paying for unnecessary extras). We strive to provide you with comprehensive protection and peace of mind on the road.