Protecting Your Family: Term Life Insurance Explained

At Heaton Bennett Insurance, we understand the importance of safeguarding your family’s financial future.

Term life insurance provides protection for a specific period of time, offering a cost-effective way to ensure your loved ones are financially secure if the unexpected happens.

In this post, we’ll explore the key aspects of term life insurance, helping you make an informed decision about your coverage needs.

What Is Term Life Insurance?

The Basics of Term Life Coverage

Term life insurance offers a straightforward approach to protect your family’s financial future. This type of insurance provides coverage for a specific period, typically ranging from 10 to 30 years. If the policyholder dies during this term, their beneficiaries receive a predetermined death benefit.

Term Life vs. Permanent Life Insurance

Term life insurance differs significantly from permanent life insurance. While permanent life insurance covers you for your entire life and often includes a cash value component, term life insurance focuses solely on protection. This pure protection approach results in more affordable premiums. For instance, a healthy 30-year-old might pay $25 per month for a $500,000 20-year term policy, whereas a comparable whole life policy could cost $300 or more per month.

Key Features That Make Term Life Attractive

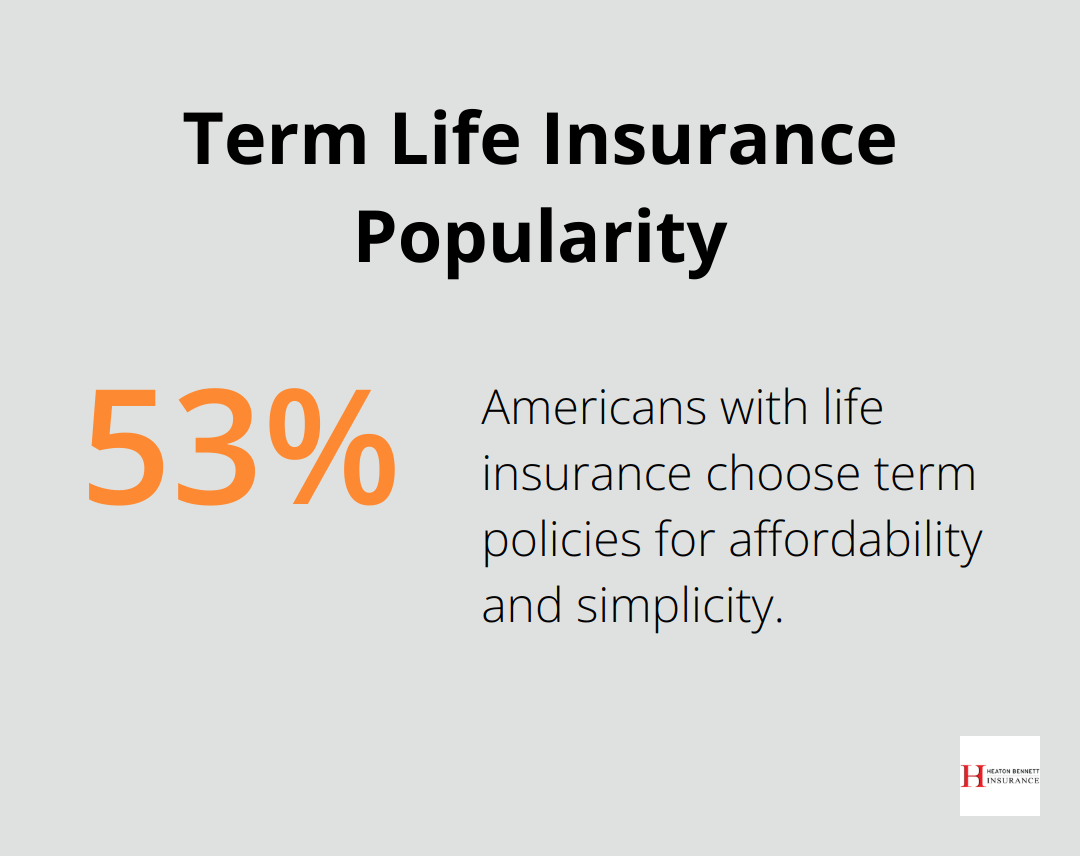

Term life insurance stands out for its flexibility. You can select a term that aligns with your specific needs, such as covering your children until they achieve financial independence or protecting your mortgage until you pay it off. A 2023 study by LIMRA revealed that 53% of Americans with life insurance choose term policies due to their affordability and uncomplicated nature.

Benefits for Young Families

For young families, term life insurance acts as a financial safety net. The death benefit can replace lost income, eliminate debts, or fund future expenses (like college tuition). A 2022 Bankrate survey found that 68% of parents with children under 18 reported increased financial security after purchasing term life insurance.

Customizing Your Coverage

Term life insurance allows you to tailor your coverage to your unique situation. You can adjust the term length and coverage amount to match your family’s needs and financial goals. This customization ensures you don’t overpay for unnecessary coverage while still providing adequate protection for your loved ones.

As we move forward, let’s explore how to determine the right coverage amount for your family’s specific needs and financial situation.

How Much Coverage Do You Need?

Assessing Your Financial Obligations

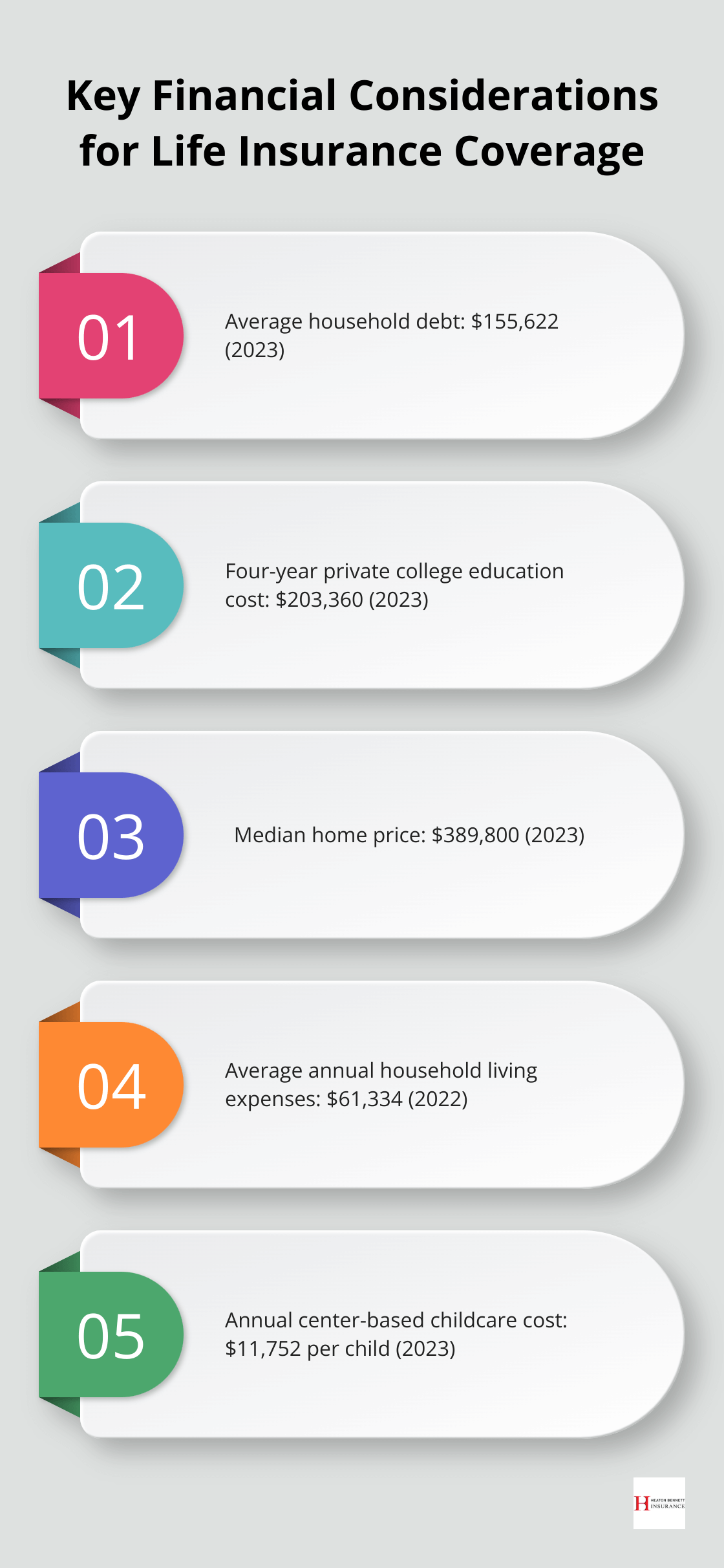

Determining the right amount of term life insurance coverage protects your family’s financial future. You should start by evaluating your current financial situation. Consider your outstanding debts, including mortgages, car loans, and credit card balances. The Federal Reserve reports that the average American household carried $155,622 in debt in 2023. Your coverage should suffice to pay off these debts, preventing your family from inheriting financial burdens.

Next, factor in your income replacement needs. A common guideline suggests 10-15 times your annual salary in coverage. However, this varies based on your family’s lifestyle and future goals. For example, if you earn $75,000 annually, you might try for $750,000 to $1,125,000 in coverage.

Planning for Future Expenses

Consider future expenses that your family might face. The College Board reports that the average cost of a four-year private college education in 2023 was $203,360. If you have two children, you might need an additional $400,000 in coverage to fund their education.

Don’t overlook everyday living expenses. The Bureau of Labor Statistics found that the average American household spent $61,334 on living expenses in 2022. Multiply this by the number of years you want to provide for your family to get a baseline figure.

Adjusting for Life Stages

Your insurance needs will evolve as you progress through different life stages. For newlyweds, coverage might focus on income replacement and mortgage protection. The National Association of Realtors reported the median home price in 2023 was $389,800, so your coverage should account for this significant asset.

As your family grows, your coverage should increase to accommodate childcare and education costs. The Care.com 2023 Cost of Care Survey found that the average weekly cost for center-based childcare was $226 (nearly $12,000 annually per child). This represents a significant expense to factor into your coverage.

For those nearing retirement, you might reduce your coverage as your financial obligations decrease and your savings grow. However, consider leaving enough to cover final expenses and provide a financial cushion for your spouse.

Tailoring Your Coverage

A comprehensive evaluation of these factors will help you determine the right amount of term life insurance coverage to protect your family’s financial future. Working with experienced professionals can further refine your coverage needs, ensuring you have comprehensive protection without unnecessary costs.

Now that we’ve explored how to calculate your coverage needs, let’s examine how to select the appropriate term length for your policy.

How Long Should Your Term Life Policy Last?

Aligning Policy Length with Life Events

Selecting the right term length for your life insurance policy ensures your family’s financial security matches your long-term goals. Many clients struggle with deciding between 10, 20, or 30-year terms.

Your policy’s term should cover your most significant financial obligations. For many, this means matching the term with their mortgage payoff date. The National Association of Realtors reports that the average mortgage term in the United States is 30 years. A 30-year term policy could provide peace of mind until your mortgage is paid off if you’ve just purchased a home.

Parents should consider their children’s ages and future education costs. The College Board states that the average time to complete a bachelor’s degree is 4.1 years. A 25-year term could cover a newborn’s childhood and potential college years, ensuring financial support through their education.

Considering Financial Milestones

Your term length should account for major financial milestones. A study by Fidelity Investments found that Americans expect to retire at age 66 (on average). A 30-year term policy could protect your family until you reach retirement age and potentially have substantial savings if you’re currently 35.

Shorter terms might be more appropriate for those closer to retirement. The Social Security Administration reports that a man reaching age 65 today can expect to live until 84 (on average). A 20-year term policy for someone in their early 60s could provide coverage through their retirement years.

Adapting to Changing Needs

Life is unpredictable, and your insurance needs may change. Many insurers offer conversion options, allowing you to switch your term policy to a permanent one without a medical exam. This flexibility proves invaluable if your health deteriorates during the policy term.

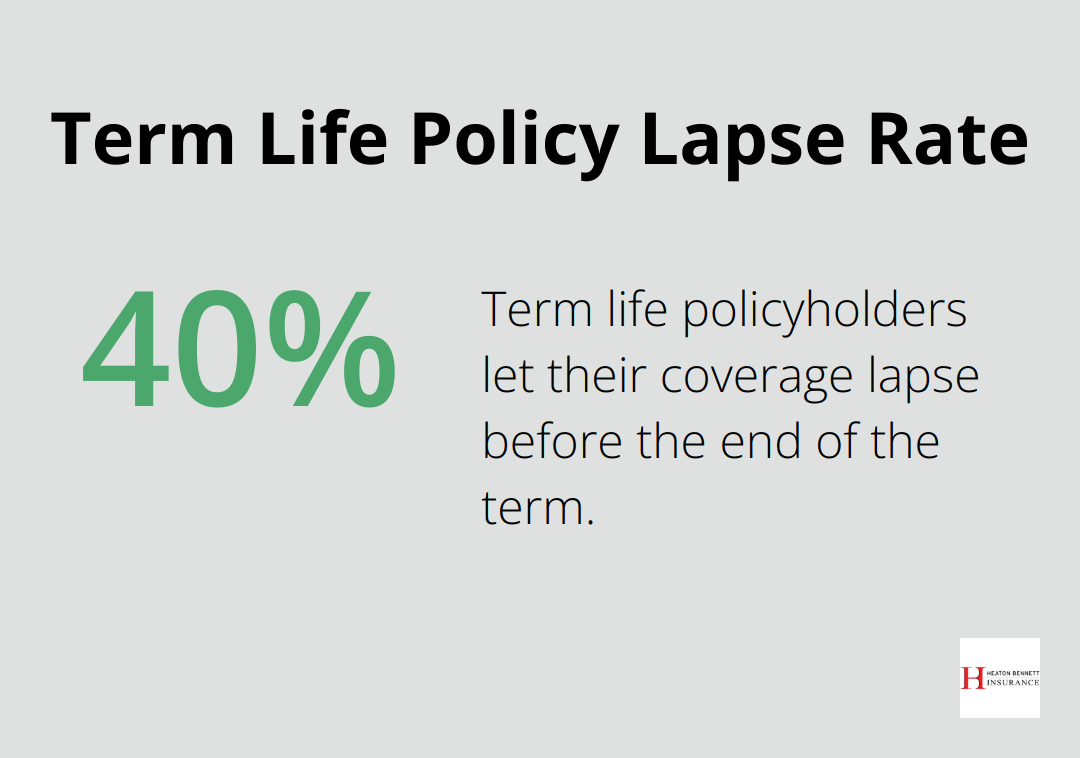

Some policies also offer a renewal option. While premiums typically increase upon renewal, this feature ensures continued coverage even if your health has changed. LIMRA reports that 40% of term life policyholders let their coverage lapse before the end of the term, often due to changing needs or financial situations.

Evaluating Policy Features

When selecting a term length, consider additional policy features that may benefit you. Some insurers offer riders (additional benefits) that can customize your coverage. For example, a disability income rider could provide financial support if you become unable to work.

Try to find policies with level premiums, which keep your payments consistent throughout the term. This feature helps with long-term financial planning and budgeting.

Final Thoughts

Term life insurance provides protection for a specific period of time, offering a cost-effective way to safeguard your family’s financial future. You should select the appropriate coverage and term length to ensure your loved ones receive protection during the years they need it most. Regular policy reviews will help you maintain adequate coverage as your life circumstances change.

Our team at Heaton Bennett Insurance can guide you through the process of selecting the right term life insurance policy for your unique situation. We offer personalized advice and access to multiple carriers, which ensures you find suitable coverage at competitive rates. Our “Security Snapshot” process allows us to assess your needs and tailor a comprehensive insurance solution.

Don’t leave your family’s financial security to chance. Contact Heaton Bennett Insurance today to explore your term life insurance options and take the first step towards a more secure future. We will help you make informed decisions about your coverage, whether you’re a young parent or a seasoned professional planning for retirement.